Understanding the various loan types mortgage lenders offer is essential for making informed decisions in Seattle's competitive housing market. Whether you're purchasing your first home in Shoreline, upgrading in Bellevue, or investing in Redmond real estate, selecting the right financing structure impacts your monthly payment, down payment requirements, and long-term financial health. With mortgage rates and housing inventory fluctuating throughout 2026, Seattle-area homebuyers benefit from working with experienced professionals who can match their unique financial situation to the most advantageous loan product available.

Major Loan Types Mortgage Borrowers Should Know

The mortgage industry offers several distinct financing categories, each designed for specific borrower profiles and property types. Understanding these fundamental loan types mortgage options helps you identify which programs align with your financial goals, income structure, and homeownership timeline.

Conventional Loans

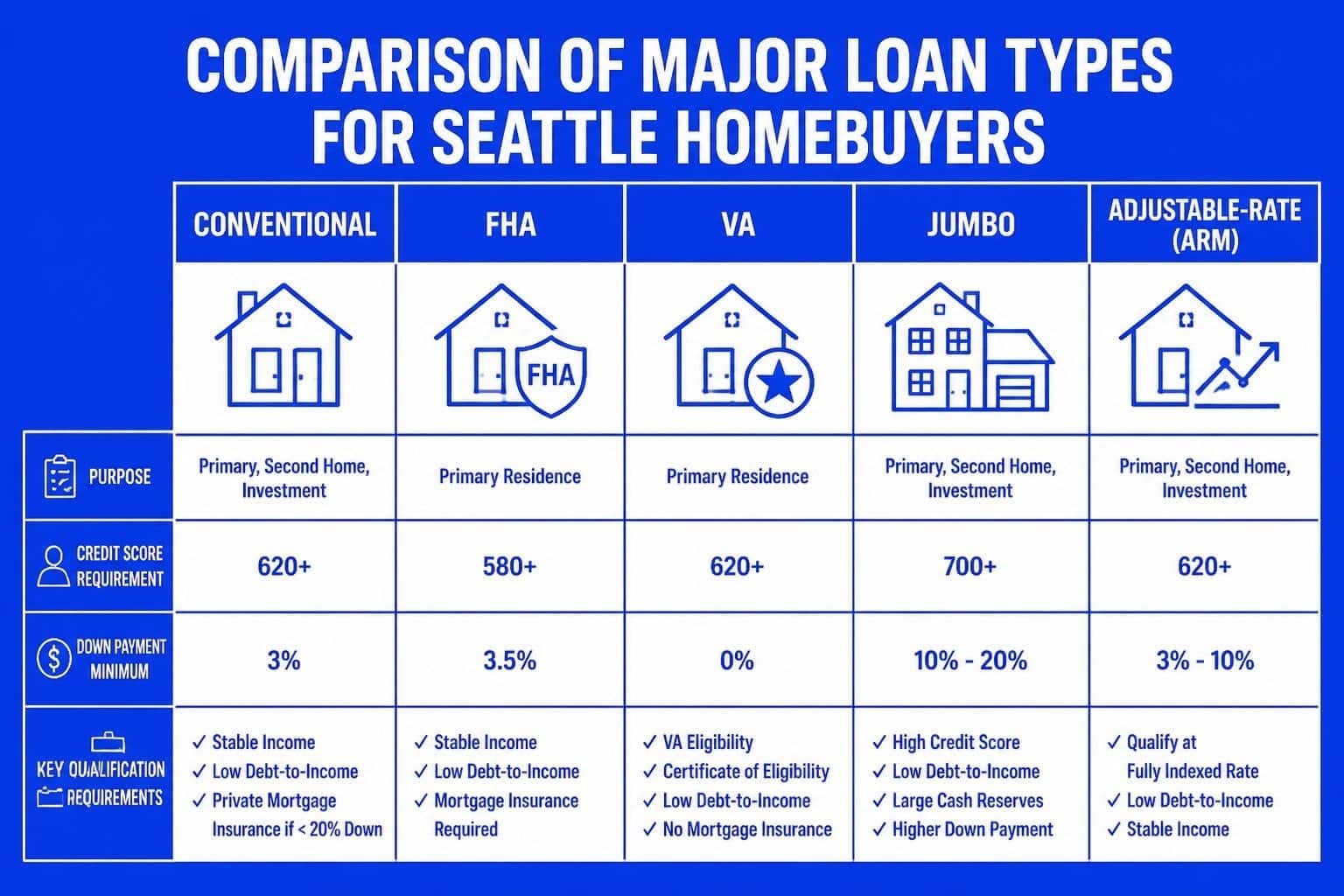

Conventional mortgages represent the most common loan types mortgage borrowers select in Seattle and surrounding areas. These loans are not insured by government agencies, which means lenders assume greater risk and typically require stronger credit profiles and larger down payments.

Key Features of Conventional Mortgages:

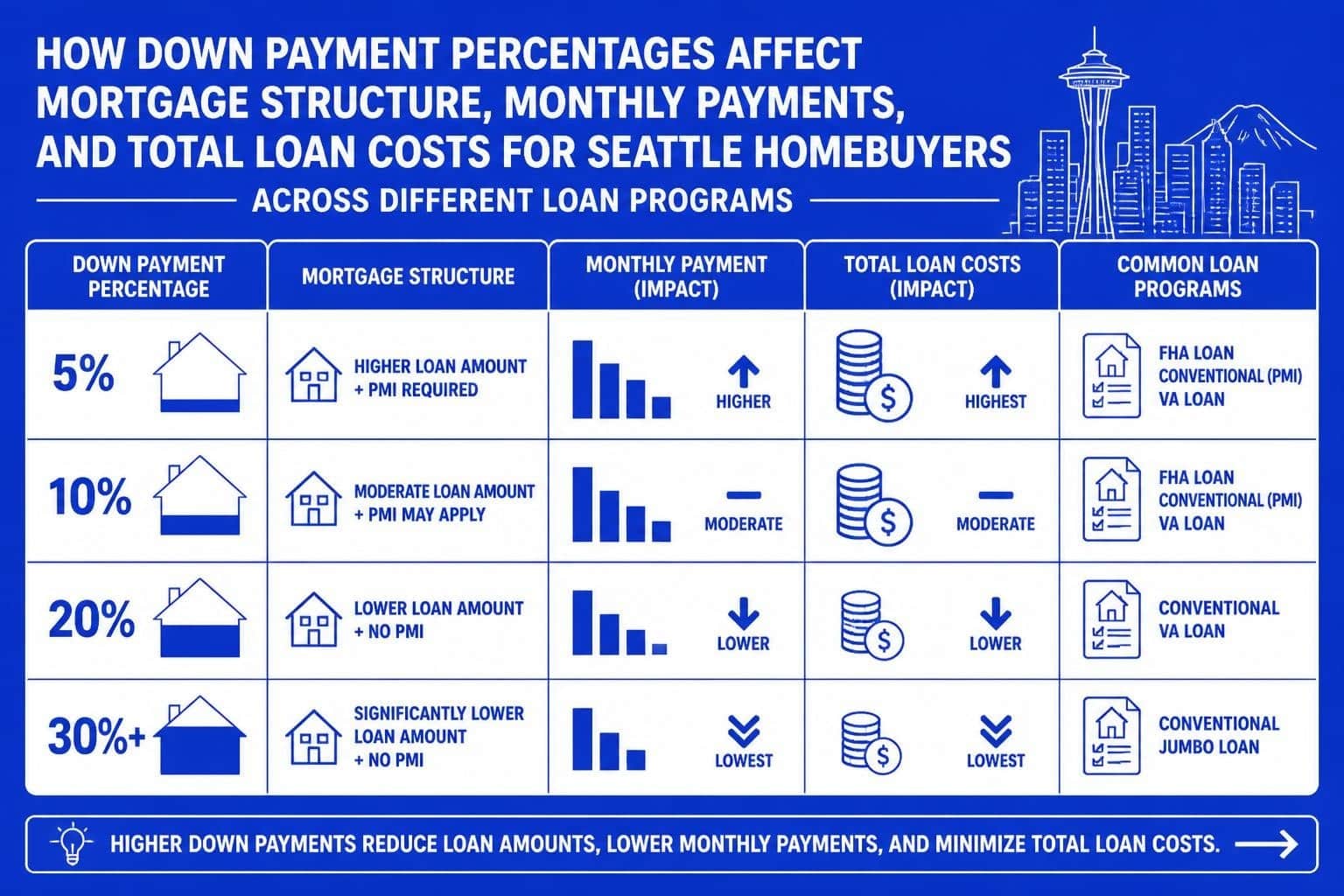

- Down payments ranging from 3% to 20% depending on the program

- Private mortgage insurance (PMI) required when down payment is below 20%

- Competitive interest rates for borrowers with credit scores above 680

- Loan limits up to $806,500 in King County for 2026 (conforming loans)

- Flexible terms including 15-year, 20-year, and 30-year fixed options

For Seattle tech professionals with steady W-2 income and strong credit, conventional loans often provide the best combination of rate and flexibility. The ability to remove PMI once you reach 20% equity makes these products particularly attractive for buyers planning to stay in their homes long-term. You can explore more about conventional loan lenders and their specific requirements.

The Consumer Financial Protection Bureau explains different kinds of mortgage loans, providing detailed consumer protections and comparison tools for conventional options.

Government-Backed Loan Programs

Government-insured loan types mortgage programs provide access to homeownership for borrowers who may not qualify for conventional financing. These products offer reduced down payment requirements and more flexible credit guidelines.

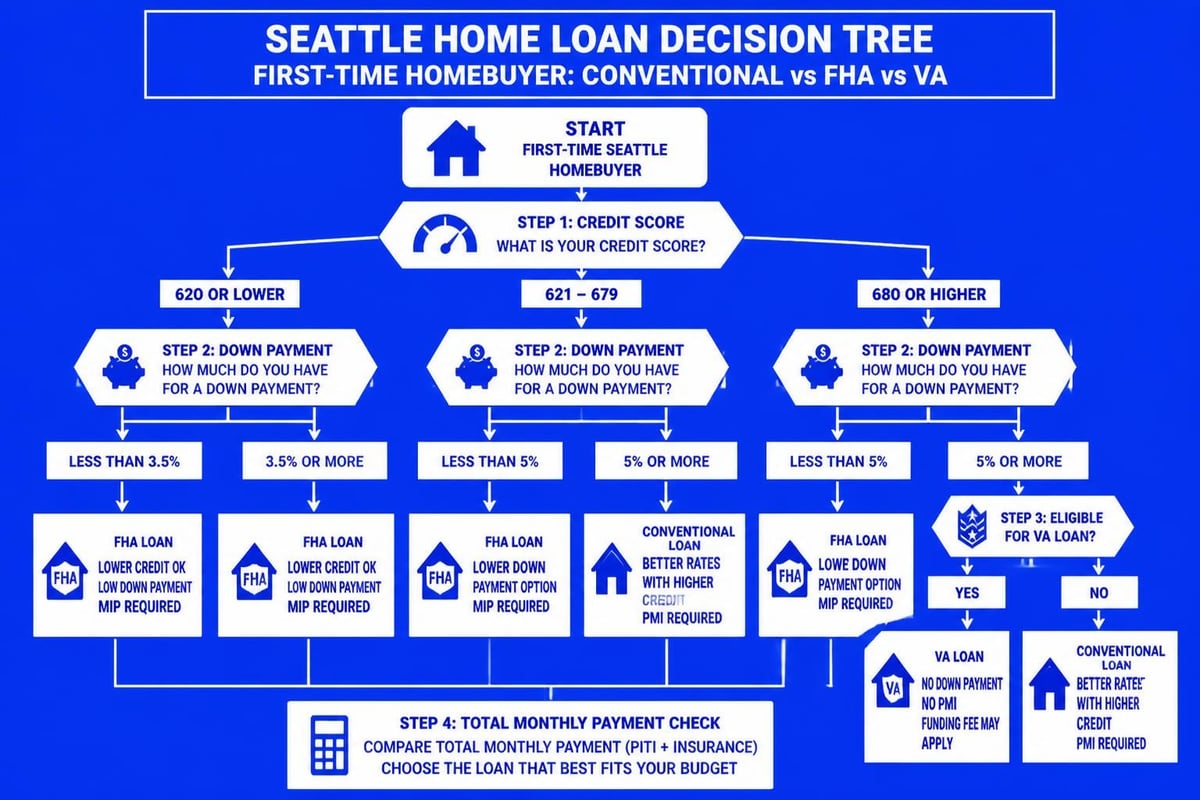

FHA Loans

Federal Housing Administration loans serve first-time buyers and those with limited savings or credit challenges. In Lynnwood, Mill Creek, and throughout King County, FHA financing opens doors for buyers who can afford monthly payments but struggle to accumulate large down payments.

| Feature | FHA Requirement |

|---|---|

| Minimum Down Payment | 3.5% with credit score 580+ |

| Mortgage Insurance | Upfront (1.75%) + annual premium |

| Credit Score | 500-579 requires 10% down |

| Debt-to-Income Ratio | Up to 50% with compensating factors |

| Loan Limits (Seattle 2026) | $806,500 (single-family) |

The upfront and ongoing mortgage insurance premiums represent the primary cost consideration with FHA loans. However, for buyers with credit scores below 680 or down payments under 10%, FHA often provides better approval odds and competitive rates compared to conventional alternatives. Learn more about FHA home loan down payment strategies.

VA Loans

Veterans, active military members, and eligible spouses access VA financing with zero down payment requirements. For qualified borrowers purchasing in Everett, Kirkland, or anywhere in Washington State, VA loans represent one of the most powerful loan types mortgage products available.

VA Loan Advantages:

- No down payment required on purchase prices up to $806,500

- No monthly mortgage insurance premiums

- Competitive interest rates typically 0.25%-0.50% below conventional

- Flexible credit requirements with manual underwriting available

- Seller can contribute up to 4% toward closing costs

The VA funding fee (typically 2.3% for first-time use with zero down) can be financed into the loan amount, making VA loans genuinely accessible for service members with minimal cash reserves.

USDA Loans

Rural development loans through USDA serve eligible properties in suburban and rural areas. While most of Seattle proper doesn't qualify, portions of Snohomish County and areas northeast of Lake Forest Park may be eligible for this zero-down financing option.

Fixed-Rate vs. Adjustable-Rate Mortgage Structures

Beyond the loan types mortgage programs based on insurance or guarantor, borrowers must also choose between fixed and adjustable interest rate structures. This decision significantly impacts payment stability and long-term costs.

Fixed-Rate Mortgages

Fixed-rate loans maintain the same interest rate throughout the entire loan term, providing payment predictability that Seattle homeowners value in uncertain economic climates. The 30-year fixed mortgage remains America's most popular home loan product, though 15-year and 20-year terms offer faster equity building with higher monthly payments.

When Fixed-Rate Makes Sense:

- You plan to own the property for 7+ years

- Current interest rates are historically favorable

- You prefer budget certainty over potential rate savings

- You're purchasing a primary residence rather than an investment property

For Bellevue and Redmond buyers working in tech, fixed-rate mortgages provide stability that complements variable compensation from RSUs and bonuses. Even as stock compensation fluctuates, your housing payment remains constant. Kiplinger examines the pros and cons of fixed-rate loans in greater detail.

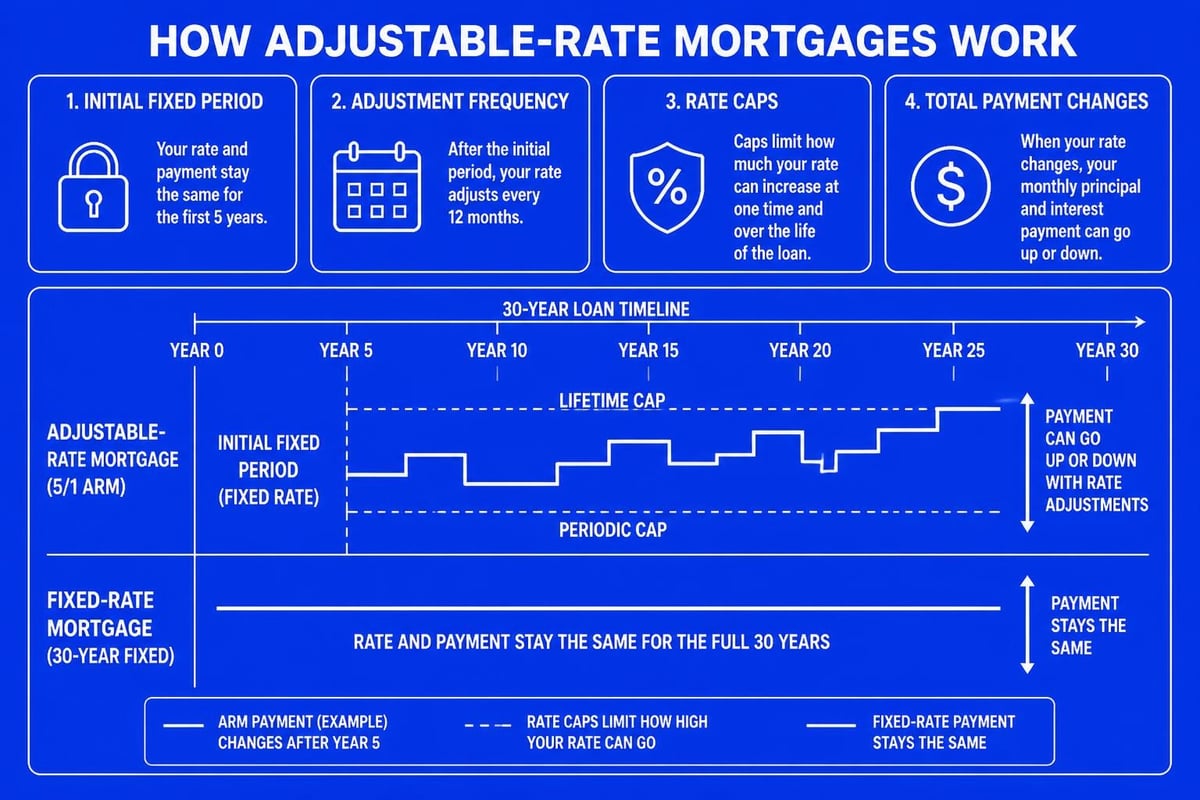

Adjustable-Rate Mortgages (ARMs)

ARMs feature an initial fixed period (commonly 5, 7, or 10 years) followed by periodic rate adjustments based on market indices. These loan types mortgage products typically offer lower initial rates compared to 30-year fixed alternatives.

In Seattle's appreciation-heavy market, many buyers utilize ARMs strategically, planning to sell or refinance before the adjustment period begins. A 7/1 ARM might save you 0.50%-0.75% in interest rate during the fixed period, translating to substantial monthly savings on a $900,000 Kirkland home purchase.

| ARM Type | Fixed Period | Common Use Case |

|---|---|---|

| 5/1 ARM | 5 years | Short-term ownership plans |

| 7/1 ARM | 7 years | Medium-term homeownership |

| 10/1 ARM | 10 years | Long-term with refinance option |

Jumbo Loan Types Mortgage Products for Seattle's High-Value Market

Seattle's median home prices exceed conforming loan limits in many neighborhoods, requiring jumbo financing for property values above $806,500. These specialized loan types mortgage products serve the region's competitive real estate landscape where single-family homes routinely command seven-figure prices.

Jumbo Loan Characteristics

Jumbo mortgages aren't backed by Fannie Mae or Freddie Mac, meaning each lender sets its own guidelines and pricing. However, common requirements include:

- Credit scores of 700+ (720+ for best rates)

- Down payments of 10%-20% depending on loan amount

- Debt-to-income ratios typically below 43%

- Significant cash reserves (6-12 months of payments)

- Full income documentation and verification

For Amazon, Microsoft, and Google employees, qualifying RSUs and stock-based compensation for jumbo loans requires specialized expertise. Understanding how underwriters evaluate equity compensation, vesting schedules, and bonus income can add hundreds of thousands to your buying power. The jumbo home loans resource provides Seattle-specific guidance.

Super Jumbo and Portfolio Loan Options

Property values exceeding $2-3 million often require super jumbo or portfolio loan products. These loan types mortgage lenders keep on their own books rather than selling to investors, allowing for more flexible underwriting and customized terms for high-net-worth borrowers.

NerdWallet provides an overview of five common mortgage loan types, including detailed jumbo loan considerations for high-cost markets like Seattle.

Specialized Loan Types Mortgage Programs for Unique Situations

Beyond the primary categories, several niche loan types mortgage products serve specific borrower needs or property types in the Seattle area.

Construction-to-Permanent Loans

These combination products fund both construction and permanent financing in a single closing. Popular in Shoreline and Mill Creek where custom builds and teardown-rebuilds remain common, construction loans require detailed budgets, builder vetting, and progressive draw schedules.

Construction Loan Process:

- Approval based on plans, budget, and lot value

- Funds disbursed in stages as construction progresses

- Interest-only payments during construction phase

- Automatic conversion to permanent mortgage at completion

- Single closing reduces fees and rate-lock complexity

Renovation Loans (FHA 203k and Conventional HomeStyle)

Renovation financing allows buyers to purchase and improve properties with a single loan. In Seattle's competitive market, these loan types mortgage products help buyers compete for homes needing updates while preserving cash reserves.

The FHA 203k program permits buyers to finance both purchase price and renovation costs up to FHA loan limits, while Conventional HomeStyle loans extend this concept to higher loan amounts with more flexible property types.

Bank Statement and Non-QM Loans

Self-employed borrowers, gig economy workers, and business owners often struggle to document income through traditional W-2 and tax return verification. Bank statement loans underwrite based on deposit patterns rather than tax returns, while non-qualified mortgage (Non-QM) products offer even greater flexibility for complex income situations.

These alternative loan types mortgage solutions typically carry higher interest rates (0.50%-2.00% above conventional) but provide financing access when traditional programs fall short. For Seattle entrepreneurs and consultants with significant business write-offs reducing taxable income, bank statement programs can unlock substantially higher loan amounts than tax-return-based underwriting.

Matching Loan Types Mortgage Products to Your Seattle Purchase Strategy

Selecting the optimal financing structure requires analyzing your specific financial situation, property goals, and timeline. LendingTree’s comprehensive guide discusses ten types of mortgage loans, providing additional context for decision-making.

First-Time Buyers in Seattle

If you're purchasing your first home in Lake Forest Park or Everett, prioritize loan types mortgage programs offering low down payments and accessible credit requirements:

- Conventional 97 (3% down for first-time buyers)

- FHA loans (3.5% down with credit scores 580+)

- VA loans (zero down for eligible veterans)

Working with knowledgeable mortgage broker Seattle professionals helps first-time buyers navigate down payment assistance programs and optimize their loan selection. Consider exploring first-time mortgage loans designed specifically for new homeowners.

Move-Up Buyers and Growing Families

Second-time buyers typically have equity from their starter homes and stronger credit profiles. This positions you to leverage:

- Conventional loans with equity-based down payments avoiding PMI

- 7/1 or 10/1 ARMs for rate savings if you plan to move again within a decade

- Jumbo financing for moves into higher-priced Bellevue or Kirkland neighborhoods

Real Estate Investors

Investment property financing follows stricter guidelines across all loan types mortgage categories. Expect higher down payments (15%-25%), elevated interest rates, and tighter debt-to-income requirements. Many Seattle investors utilize portfolio loans or DSCR (debt service coverage ratio) products that underwrite based on rental income rather than personal income.

Tech Professionals with Stock Compensation

Microsoft, Amazon, and Google employees represent a significant portion of Seattle's homebuyer pool. Maximizing buying power requires lenders experienced in qualifying RSUs, ESPP income, and bonus structures. The jumbo home mortgage landscape particularly benefits from specialized underwriting knowledge.

Rate Shopping and Timing Considerations for 2026

Mortgage rates fluctuate based on Federal Reserve policy, economic indicators, and global market conditions. Throughout 2026, Seattle borrowers should monitor rate trends while recognizing that timing the absolute bottom is nearly impossible.

Lock Strategies Across Loan Types Mortgage Products

Different loan types mortgage products offer varying rate lock periods and extension options:

- Conventional loans: Typically 30-60 day locks with extension options

- Construction loans: Extended locks (180-360 days) with premium pricing

- Purchase vs. refinance: Purchase locks often feature better pricing due to closing date certainty

Chase Bank’s guide outlines various mortgage options, including rate lock considerations for each product type.

Points and Rate Buydowns

Paying points (upfront fees to reduce your interest rate) makes more sense with certain loan types mortgage structures. On a 30-year fixed mortgage you plan to keep for decades, buying down your rate 0.375% might break even within 3-4 years. However, paying points on a 5/1 ARM you'll refinance or sell before adjustment makes little financial sense.

Underwriting Timeline Differences

Various loan types mortgage products feature different processing timelines in 2026. Understanding these timeframes helps Seattle buyers make competitive offers in fast-moving markets:

| Loan Type | Typical Timeline | Documentation Level |

|---|---|---|

| Conventional | 15-25 days | Moderate |

| FHA | 20-30 days | Extensive |

| VA | 25-35 days | Extensive |

| Jumbo | 20-30 days | Very Extensive |

| Portfolio/Non-QM | 30-45 days | Varies significantly |

Working with established Seattle lenders offering expedited underwriting can compress these timelines substantially. Some experienced mortgage teams close conventional and jumbo loans in as few as 9-12 business days when borrowers provide complete documentation promptly.

Common Mistakes When Selecting Loan Types Mortgage Products

Seattle homebuyers frequently make avoidable errors during loan selection that cost thousands in unnecessary fees or missed opportunities.

Mistake 1: Choosing Based Solely on Rate

The lowest advertised rate often comes with higher fees, stricter requirements, or limited lender reliability. Total cost comparison across loan types mortgage options should include origination fees, discount points, lender credits, and third-party costs.

Mistake 2: Overlooking Equity Acceleration

Many buyers default to 30-year terms without analyzing 15 or 20-year alternatives. For borrowers who can afford slightly higher payments, shorter terms build equity faster and save enormous interest costs over time.

Mistake 3: Mismatching Loan Type to Occupancy Plans

Selecting a 30-year fixed mortgage when you plan to sell within five years often means paying a rate premium for stability you won't use. Conversely, choosing an ARM when you intend to stay long-term exposes you to future rate risk.

Mistake 4: Not Pre-Qualifying for Multiple Loan Types

Understanding what you qualify for across conventional, FHA, VA, and jumbo loan types mortgage categories provides negotiating flexibility and fallback options if your first-choice property doesn't appraise or meets unexpected issues.

Working with Experienced Mortgage Professionals in Seattle

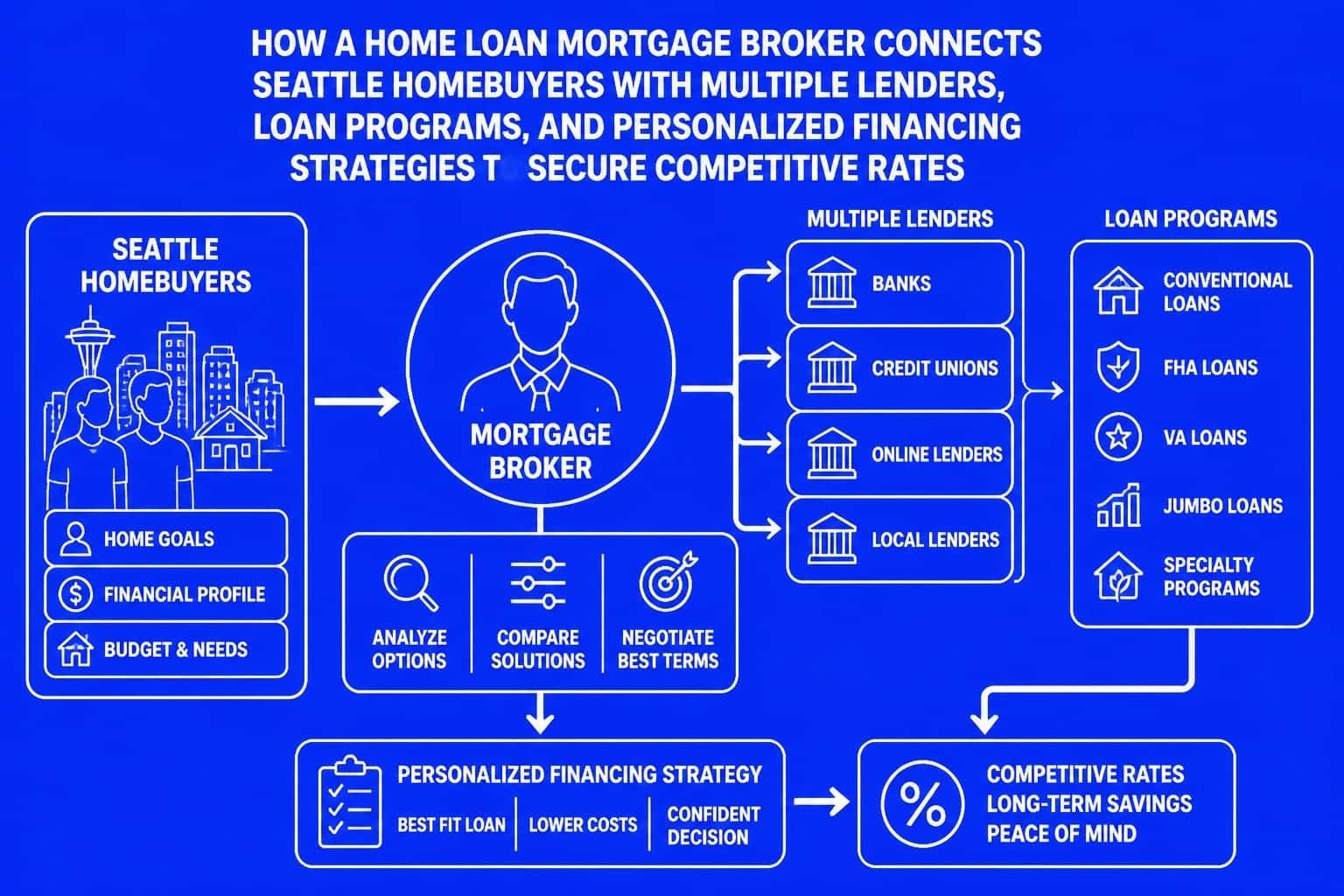

The complexity of modern loan types mortgage products, combined with Seattle's unique market dynamics, makes professional guidance invaluable. Experienced mortgage brokers access multiple lenders and programs, providing choice that direct lender relationships cannot match.

Questions to Ask Your Mortgage Advisor

- What loan types mortgage programs do I qualify for based on my income, assets, and credit?

- How do you evaluate stock compensation and RSUs for loan qualification?

- What down payment options minimize my monthly payment while avoiding PMI?

- Which loan structure provides the best total cost for my timeline and property goals?

- How do current rate trends affect my decision between fixed and adjustable products?

Transparent mortgage professionals educate rather than sell, helping you understand tradeoffs across loan types mortgage options without pressure toward any particular product. The down payment guide for Seattle homebuyers in 2026 offers additional strategic insights.

Credit Score Impact Across Different Loan Types

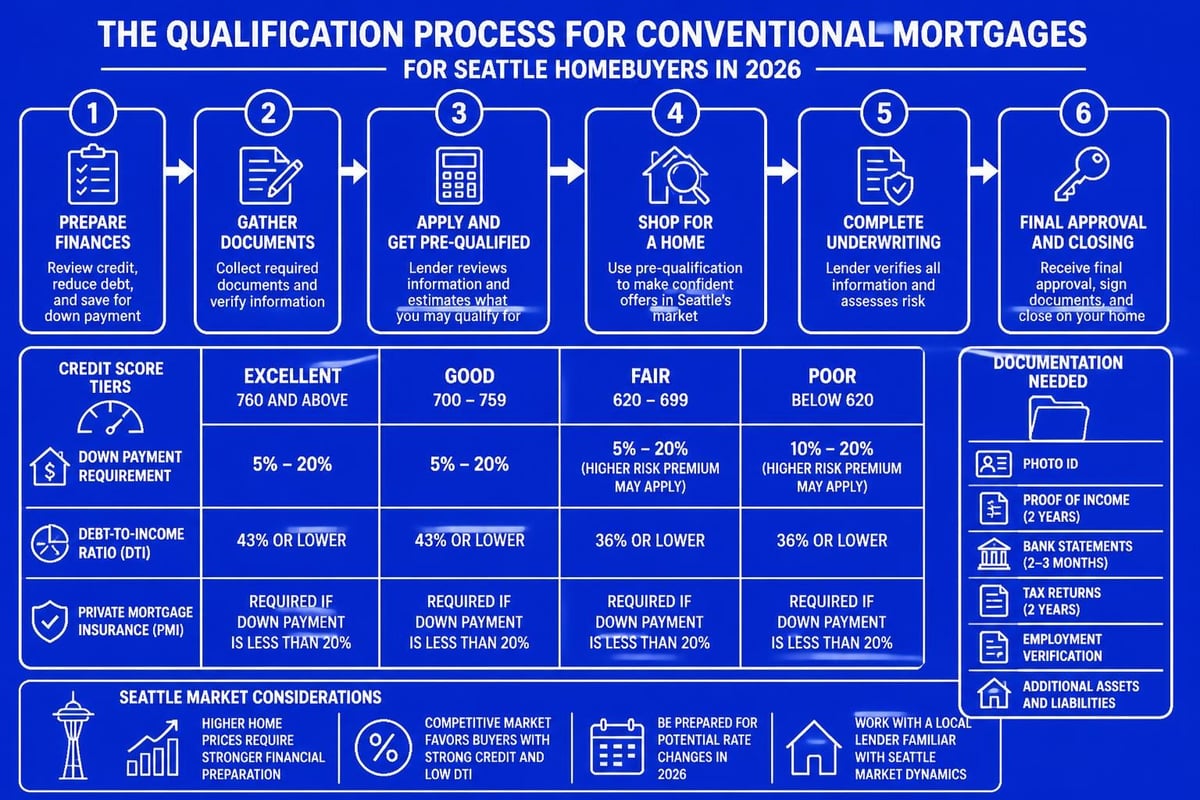

Your credit score dramatically affects both approval odds and pricing across various loan types mortgage lenders offer. Understanding these thresholds helps you improve qualification before applying.

Credit Score Ranges and Loan Access:

- 760+: Best rates across all conventional and jumbo products

- 700-759: Good conventional rates, competitive jumbo pricing

- 680-699: Moderate conventional rates, limited jumbo access

- 640-679: FHA competitive, conventional rates increase

- 580-639: FHA only option for most borrowers

- Below 580: 10% down FHA or alternative financing required

For Seattle tech professionals with excellent credit, the rate difference between 740 and 780 might seem minimal on a single loan type. However, that 0.125%-0.250% difference on a $1.2 million jumbo loan translates to $1,500-$3,000 annually in interest savings.

Documentation Requirements Vary by Loan Type

Different loan types mortgage products demand varying documentation levels, affecting both approval timeline and borrower burden.

Full Documentation Loans

Conventional, FHA, VA, and most jumbo loans require comprehensive income and asset verification:

- Two years of W-2s or business tax returns

- 30-60 days of pay stubs

- Two months of bank and investment account statements

- Explanations for large deposits or withdrawals

- Purchase contract and property details

Alternative Documentation Programs

Bank statement and Non-QM loan types mortgage products accept alternative income verification:

- 12-24 months of business or personal bank statements

- 1099s and profit/loss statements for self-employed

- Asset depletion calculations for high-net-worth borrowers

- Foreign national income documentation for international buyers

Yahoo Finance explores various mortgage loan types available in 2026, including alternative documentation options for non-traditional borrowers.

Selecting the right loan types mortgage product requires understanding your financial profile, property goals, and Seattle's unique market conditions. Whether you're a first-time buyer in Shoreline exploring FHA options, a tech professional in Bellevue maximizing jumbo loan qualification with stock compensation, or a move-up buyer in Kirkland weighing ARM versus fixed-rate structures, informed decisions start with expert guidance. Keith Akada brings 25+ years of experience helping Seattle-area homebuyers navigate conventional, FHA, VA, and jumbo financing with transparency and strategic insight. Connect with Mortgage Reel to explore which loan structure best supports your homeownership goals.