weight: normal;”>Common Mortgage Terms

Any individual looking to buy a new home may feel stressed because the mortgage language may seem foreign. Many of the terms used to describe loan programs can be overwhelming and confusing to understand if you are unfamiliar. Below is a simple reference to describing the most common terms used during the home buying process.

Arm (Adjustable rate mortgage): A mortgage with interest rates that fluctuate once the initial term is complete.

Amortization: Part of each payment is applied to the interest and part to the balance. The newer the loan, the greater the amount is applied to interest. Over time, the more interest you have paid, will slowly decrease and majority of the payment goes to the principal balance until the loan is paid in full.

Amortization Schedule: Illustrates how much each scheduled mortgage payment is and the amount applied to the interest and principal balance each month.

APR (Annual Percentage Rate): This is not the actual note rate. It is higher then the note rate because it reflects the annual cost of borrowing as a percentage.

Appraisal: A written estimate of the value of the home generally including living area and permanent fixtures.

Assessed Value: The value that the tax assessor places on the home for tax purposes.

Bridge Loan: A form of second trust that is collateralized by the borrower’s present home (which is usually for sale) in a manner that allows the proceeds to be used for closing on a new home before the present home is sold.

Broker: Realtors who work under a broker are considered agents. Sometimes agents are also brokers who work for themselves or someone else. A broker in the mortgage industry is someone who brokers a loan to a lender or investor.

Cash-out refinance: Borrowers can refinance their mortgages for a greater amount then the current loan balance to use for personal reasons.

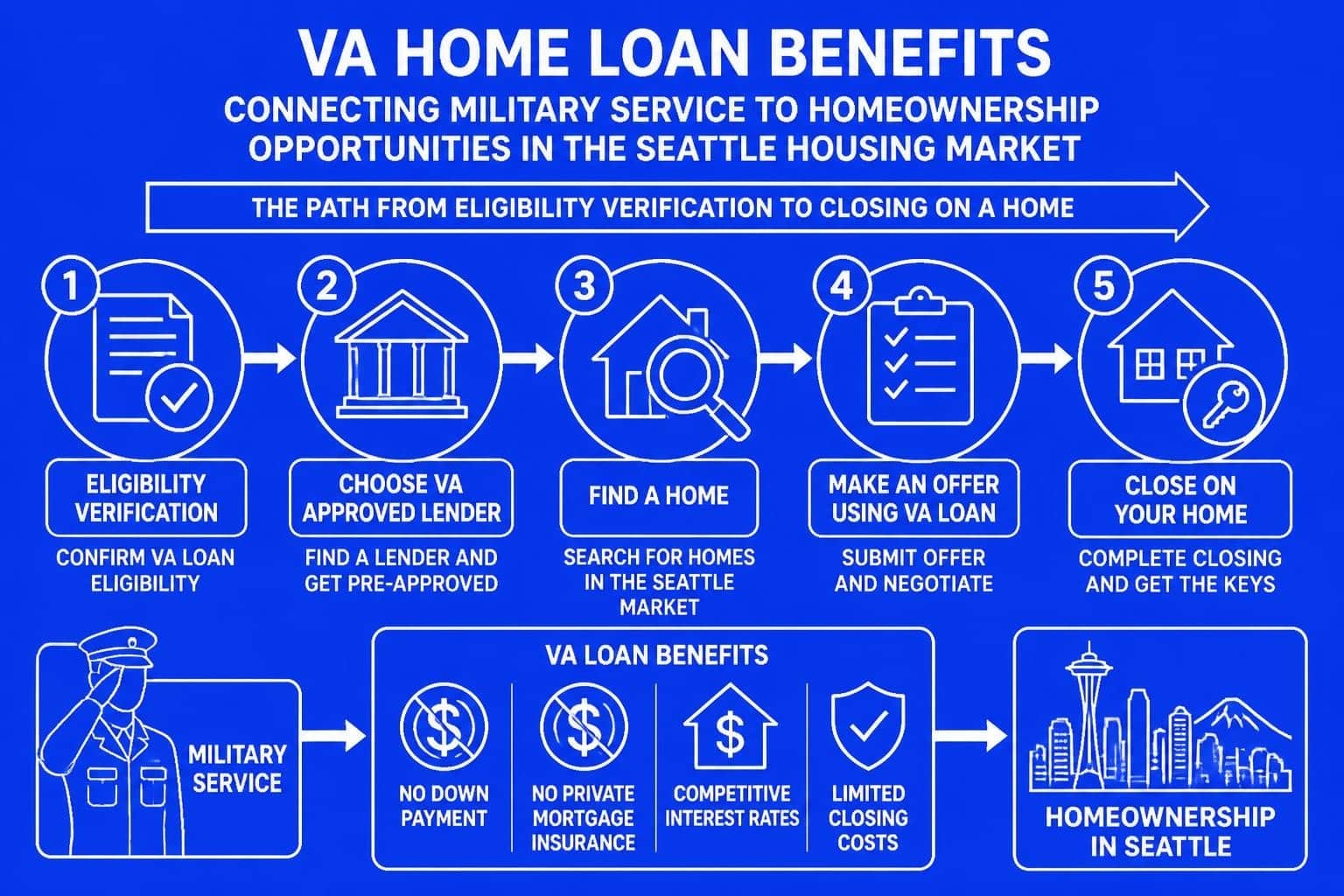

Certificate of Eligibility: From the Veterans Administration (VA), used to certify eligibility for a VA loan.

Closing: A loan is closed when all the documents have been recorded at the clerk and recorder’s office.

Collateral: Your home is considered collateral for your mortgage. You can lose the home if the loan is not repaid.

Construction Loan: A short-term loan that is obtained to finance construction.

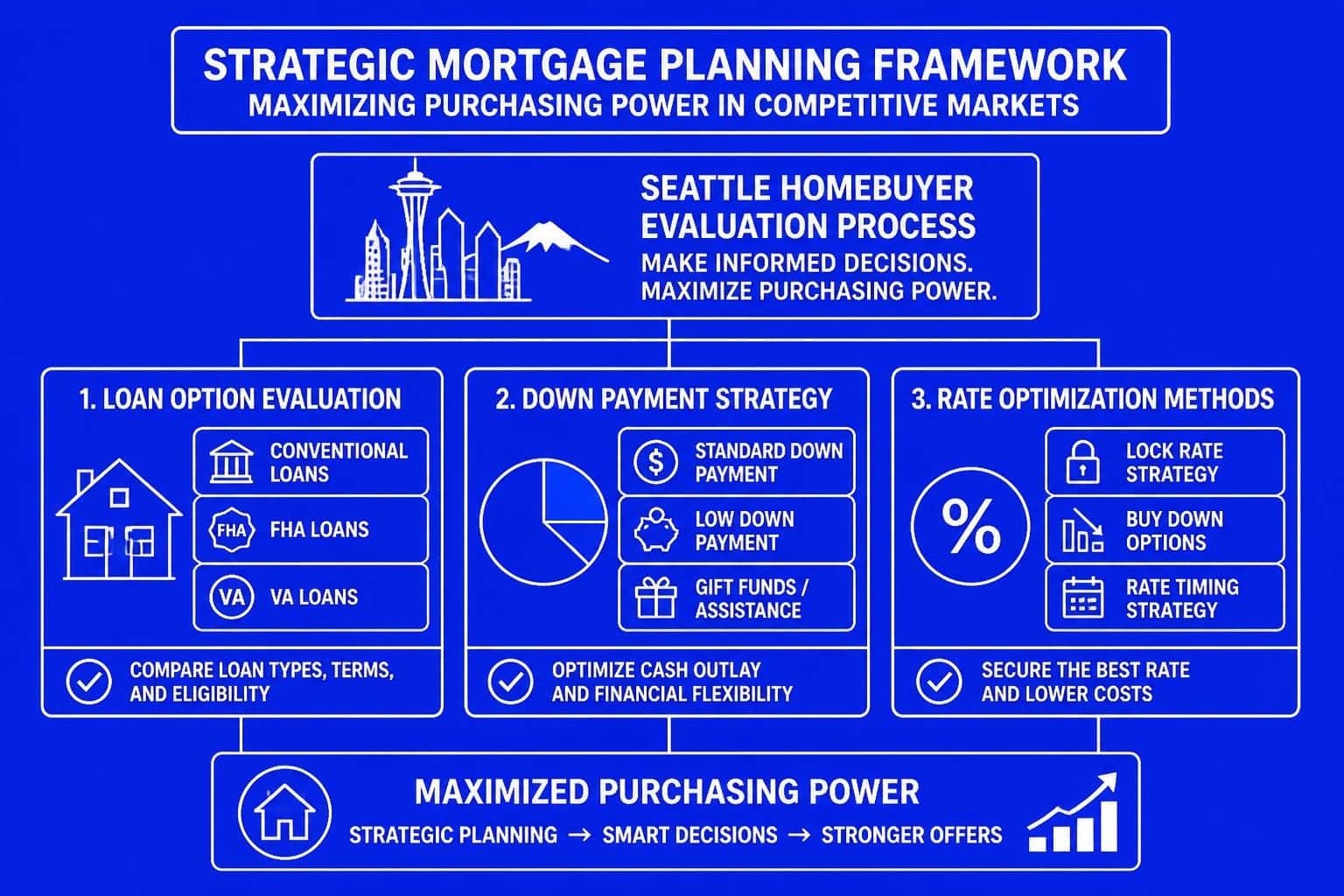

Conventional Mortgage: A non-government backed loan.

COFI (Cost of Funds Index): An index that helps determine interest rate changes on adjustable rate mortgages.

Credit Report: A report of an individual’s credit history prepared by a credit bureau and used by a lender in determining a loan applicant’s creditworthiness.

Default: When a payment on a first mortgage is more then 30-days late.

Earnest Money Deposit: Given to the sellers by the buyers in anticipation of buying the home. After a particular date, if you back out on the sale of the home, you may lose this deposit.

Discount Points: This refers to government-backed loans such as FHA or VA. This applies to points, which are paid in addition to the loan origination fee.

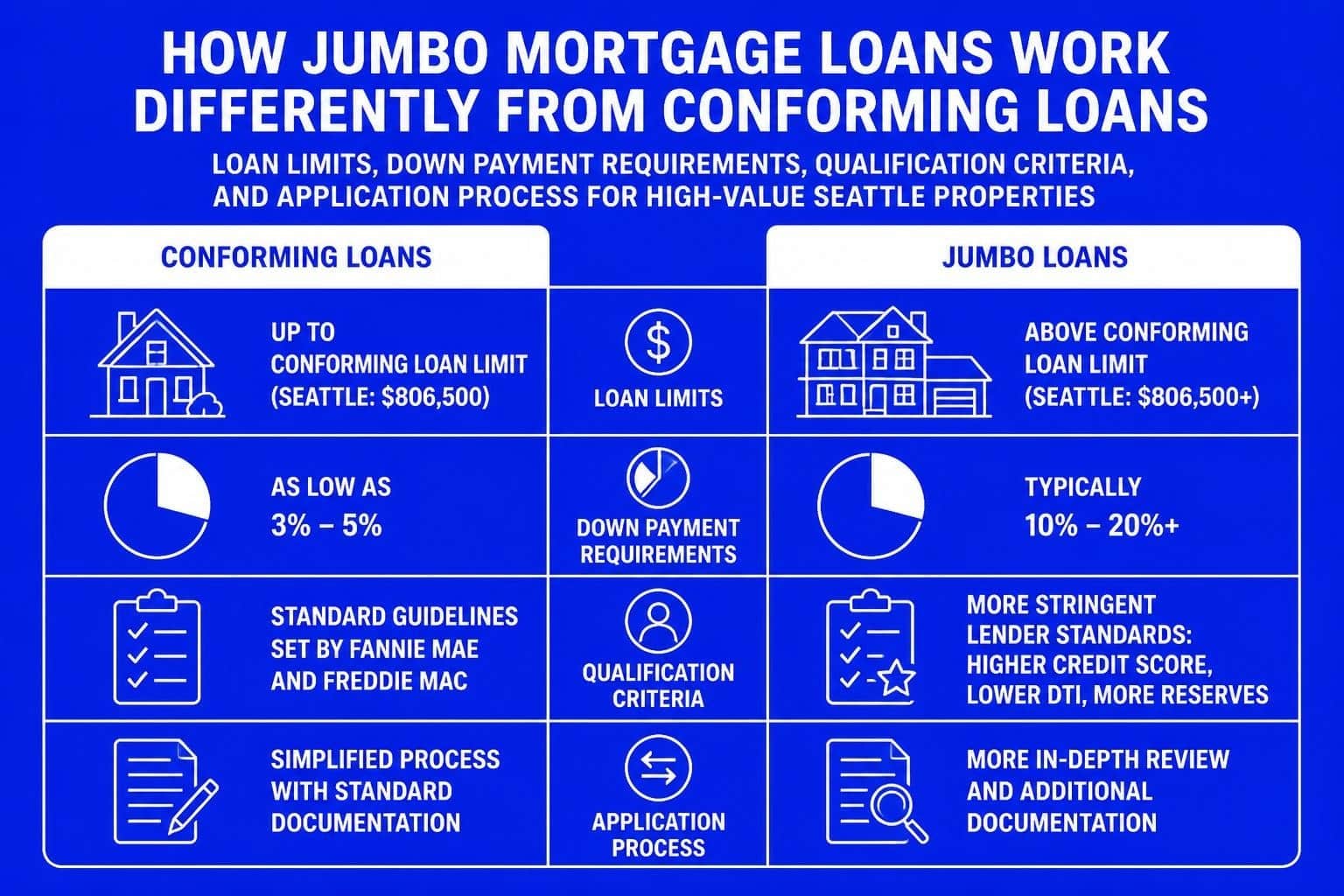

Down Payment: Portion of purchase price paid in cash. If this is less then 20% of the price of the home, you will probably have to pay for private mortgage insurance.

Due-on Sale Provisions: The lender can demand repayment in full if you sell the property on which the mortgage is based.

ECOA (Equal Credit Opportunity Act): Federal law that bans discrimination regarding credit on the basis of race, color, religion, gender or marital status.

Equity: To determine your equity, the loan officer will take the market value of your home and subtract the amount you still owe on your current mortgage.

Federal Home Loan Mortgage Corporation (Freddie Mac): A governmental agency, which makes home loans and rentals more accessible to individuals who normally may not qualify. Those with low incomes for instance.

FHA Loan (Federal Housing Administration): These loans are insured by the government and made available to those who qualify. There is a dollar limit on these loans depending on the area in which you live.

Fixed Rate Mortgage: The interest rate remains the same for the life of the loan.

Foreclosure: The lender forces the sale of a property because the borrower hasn’t met the financial obligation.

Guaranty: One party promises to pay a debt that was contracted by another party if that other party fails to meet its financial obligations.

Housing Expenses to Income Ratio: This is the number you get when you divide your housing expenses by your gross monthly expenses.

Index: Lenders take the difference between the current interest rate on an ARM and the interest rate earned by other investments and then use this number to adjust the ARM interest rate.

Interim Financing: A construction loan you can obtain while your new home is being built.

Jumbo Loan: Fannie Mae and Freddie Mac set annual loan limits and this loan exceeds these limits. A loan like this has higher interest rates and is considered non-conforming.

PMI (Private Mortgage Insurance): When your down payment is less than 20%, your lender will require you to carry insurance on the loan.

Negative Amortization: When your monthly payments are actually less then the interest due on the loan, the difference is added to the overall unpaid balance on the loan. In this case you end up owing more then the original amount of the loan.

Origination Fee: The fee you pay the lender to prepare documents, credit checks, inspections and so on. It’s usually a percentage of the value of the loan.

PITI: Principal, Interest, Taxes and Insurance. Usually added together and paid as a part of your loan.

Points: Prepaid interest that is expressed as 1% of the loan amount per point. Two points on a $100,000 loan would be equal to $2,000.

Prepayment Penalty: A charge imposed when you pay off a loan early.

Principal: The amount of debt on a loan that doesn’t include the interest.

Refinance: A new mortgage on a home that already has a mortgage.

Truth in Lending: Also know as Regulation Z. Lenders are required by the federal government to notify buyers of the Annual Percentage Rate before they close on the home.

VA Loan: This loan is restricted to individuals who have served in the armed services. It generally allows a low down payment or even a zero down payment mortgage.

Leave a Reply