Seattle’s housing market is diverse and vibrant, attracting tech professionals, first-time buyers, and seasoned investors alike. As one of the fastest-growing cities in the U.S., it offers a wide range of home styles and neighborhoods. To navigate this competitive landscape, many buyers turn to FHA loans, which are designed to make home ownership more accessible with lower down payment requirements.

Understanding FHA Loans

Federal Housing Administration (FHA) loans are government-backed mortgages aimed at helping individuals with lower credit scores or higher debt-to-income ratios qualify for home ownership. Unlike conventional loans requiring higher credit scores, FHA loans provide greater flexibility, making them a popular choice among Seattle’s tech-savvy populace.

Why FHA Loans Matter in Seattle

In a city like Seattle, where home prices are consistently on the rise due to high demand, FHA loans serve as a critical tool for many potential homeowners. They allow buyers to enter the market without needing a hefty down payment. This is particularly beneficial in Seattle, where high home prices can otherwise be a barrier to entry.

Key Features of FHA Loans

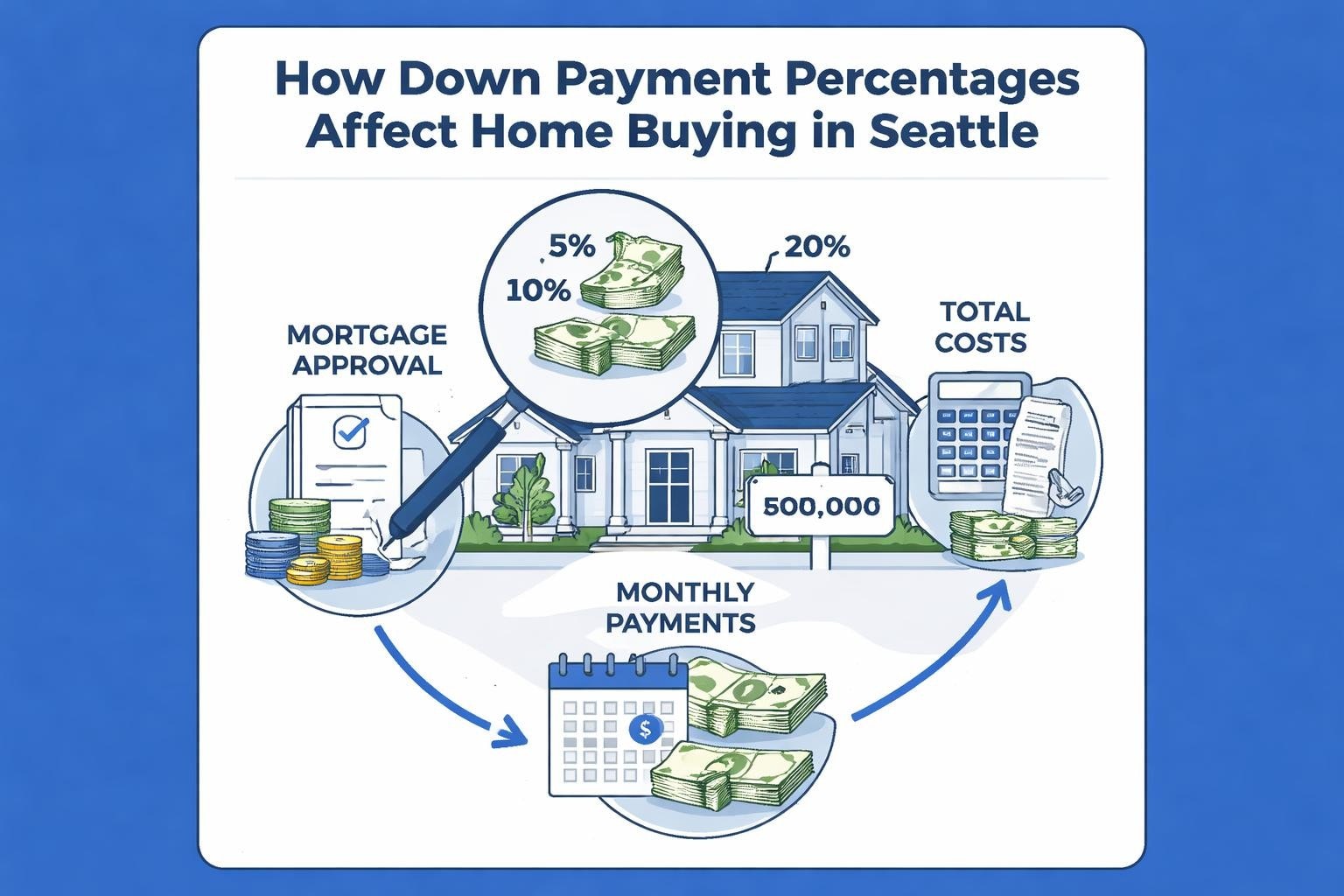

- Lower Down Payments: Typically require as little as 3.5% down, compared to the 20% commonly demanded by conventional loans.

- Credit Score Requirements: Generally accept scores as low as 580, although some lenders may accept lower scores with a higher down payment.

- Flexible Debt-to-Income Ratios: Allow more leniency in terms of how much debt you can have relative to your income.

- Mortgage Insurance Premium (MIP): Borrowers must pay an upfront premium, as well as annual premiums, to secure the loan.

Steps to Qualify for an FHA Loan in Seattle

Qualifying for an FHA loan involves several steps. Here’s how to enhance your chances and ensure a smooth application process:

1. Assess Your Financial Health

Before diving into the loan application process, get a clear picture of your financial situation. This includes:

- Evaluating Your Credit Score: Check your credit score using free online resources. Aim for a minimum of 580 to qualify for the standard down payment rate.

- Managing Your Debt: Calculate your debt-to-income ratio. Ideally, this should not exceed 43%, though some lenders allow up to 50%.

- Savings and Assets: Ensure you have funds for the down payment and any closing costs.

2. Gather Necessary Documentation

FHA loans require documentation to verify your financial status:

- Income Proof: Recent pay stubs, W-2 forms, or tax returns.

- Employment Verification: Written verification from current employers.

- Credit Report: Official report from a recognized credit bureau.

- Asset Statements: Bank statements or documentation of other financial assets.

3. Choose the Right Lender

Partner with a lender who understands the Seattle market and can offer personalized advice, like The Mortgage Reel. A local broker can provide insights into neighborhood-specific trends and opportunities.

4. Pre-Approval Process

A pre-approval letter gives you a better standing in negotiations by demonstrating financial readiness to potential sellers. During this process:

- Submit financial documents

- Undergo a credit check

- Discuss loan options with your lender

5. Property Appraisal

An appraisal is required to ensure the property meets FHA standards and is worth the amount of the loan.

6. Navigate FHA Loan Limits in Seattle

Kings County, where Seattle is located, has its own FHA loan limit, which is higher than the national average due to the cost of living. Make sure your intended purchase does not exceed this cap.

Common Pitfalls and How to Avoid Them

FHA loans are accessible, but several common pitfalls can derail your application:

Overlooking Credit Issues

Even with the lower credit score requirements, any red flags like late payments can be detrimental. Hence, addressing credit issues beforehand is vital.

Ignoring Budget Constraints

Being pre-approved doesn’t mean you should max out your budget. Take care to choose a home that fits comfortably within your financial means.

Skipping Pre-Approval

In a competitive market like Seattle’s, a pre-approval boosts your offers’ credibility. Not securing one can put you at a disadvantage against more prepared buyers.

Misunderstanding MIP

Failing to account for mortgage insurance premiums can lead to unexpected costs. Be sure to budget both upfront and annual premiums.

FAQs About FHA Loans in Seattle

What credit score do I need for an FHA loan?

A minimum score of 580 is needed for most FHA loans with a 3.5% down payment. Scores below this require a larger down payment.

Are there income limits for FHA loans in Seattle?

No income limits exist for FHA loans, but your income affects your debt-to-income ratio, influencing eligibility.

Can I use an FHA loan for a jumbo property in Seattle?

FHA loans target average-priced homes. For high-end properties, consider jumbo loans.

Closing Thoughts

In a dynamic and fast-paced market, understanding the ins and outs of FHA loans can empower you to make informed decisions. By preparing thoroughly and leveraging local expertise through experienced brokers like those at The Mortgage Reel, Seattle homebuyers can not only enter the market but thrive within it. Whether you’re eyeing a cozy apartment or a spacious family home, ensuring you meet the requirements for an FHA loan is a practical step toward achieving homeownership in Seattle’s competitive real estate scene.

Understanding the specifics of the Seattle housing market—like its fluctuating loan limits and diverse property values—is key to successfully navigating your purchase. Partnering with knowledgeable, trustworthy advisors will provide clarity and confidence as you move forward, empowering you to unlock your future home with informed decision-making.