Unlock the door to homeownership in 2026 with just a 5% down payment, making what once seemed out of reach a real possibility for many buyers.

This guide will demystify the conventional loan with 5 down, giving you the knowledge and confidence to make informed decisions in today’s evolving real estate market.

With home prices rising and lending rules shifting, a low down payment option is more attractive than ever. Imagine how a 5% down payment could help you secure your dream home, even in competitive markets.

You will discover real-world examples, eligibility criteria, and smart strategies to increase your buying power. Ready to get started? Follow this step-by-step guide to fast-track your path to homeownership with a conventional loan with 5 down.

We’ll break down what a 5% down conventional loan is, who qualifies, the application process, pros and cons, and expert strategies for approval.

Understanding Conventional Loans With 5% Down

Navigating the world of mortgages can feel overwhelming, especially when considering a conventional loan with 5 down as your path to homeownership. Understanding how this loan type works, its unique advantages, and its requirements will equip you to make the right choice in 2026’s housing market.

What Is a Conventional Loan?

A conventional loan with 5 down is a mortgage not backed by a government agency. Instead, it is offered by private lenders and follows guidelines set by Fannie Mae and Freddie Mac. Unlike FHA, VA, or USDA loans, these rely on your creditworthiness and financial profile rather than government insurance.

Conventional loans typically offer more flexibility with property types and fewer restrictions on income or location. Borrowers who choose a conventional loan with 5 down often do so to access competitive rates and faster PMI removal.

The 5% Down Payment Threshold in 2026

In 2026, the 5% down payment threshold has become a game-changer. Historically, many believed that 20% down was required to buy a home. Today, the conventional loan with 5 down lets you purchase with much less cash upfront, making homeownership more attainable.

Fannie Mae and Freddie Mac have expanded their guidelines to support low down payment borrowers. For most buyers, 5% down represents a sweet spot: less savings required than traditional loans, yet broader eligibility than the strictest 3% down programs.

Comparing Down Payment Options

Choosing between 3%, 5%, or 10%+ down depends on your goals and financial situation. Here’s a simplified table:

| Option | Down Payment | Typical Buyer Profile | PMI Required? | Notes |

|---|---|---|---|---|

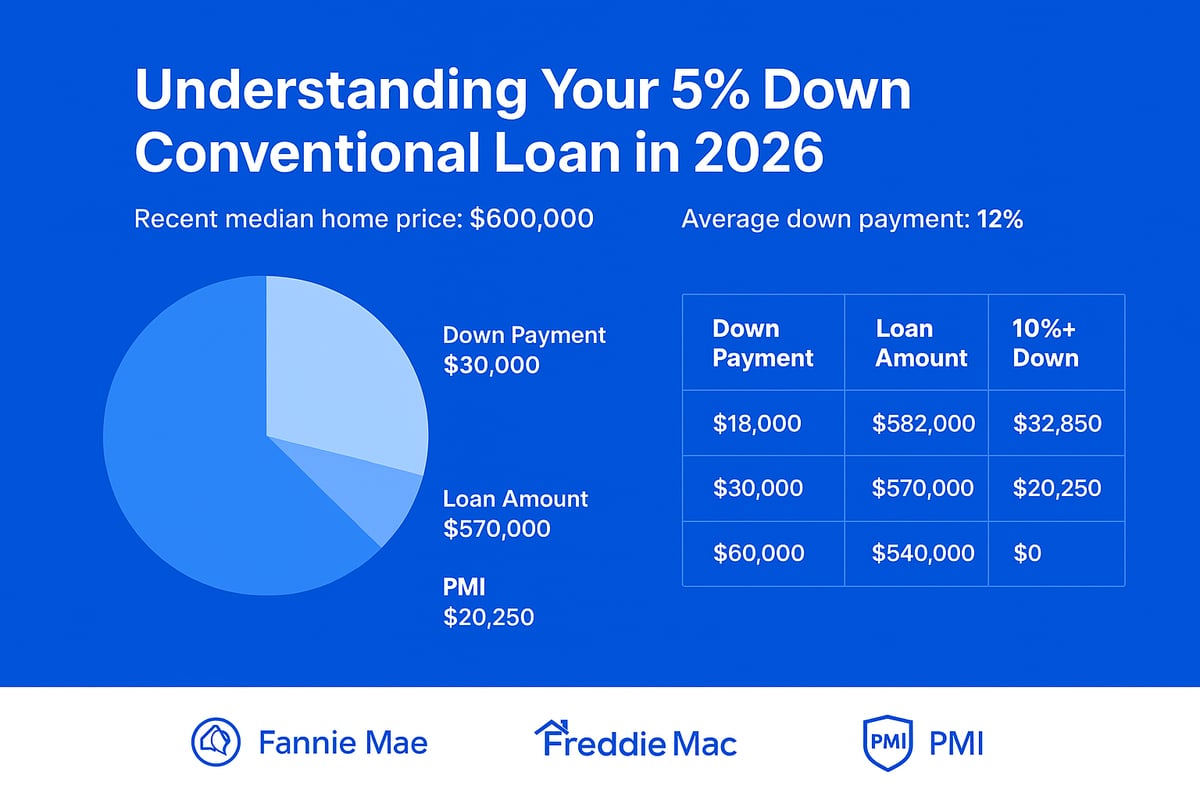

| 3% Down | $18,000 | First-time buyers | Yes | Stricter eligibility, higher PMI |

| 5% Down | $30,000 | First-time/move-up buyers | Yes | Broader eligibility, lower PMI |

| 10%+ Down | $60,000+ | Repeat buyers, high savings | Sometimes | Lower rates, PMI drops faster |

For a $600,000 home, a conventional loan with 5 down means coming up with $30,000, plus closing costs.

Loan Limits and Eligibility

Loan limits determine if your mortgage qualifies as "conforming." For 2026, the Federal Housing Finance Agency (FHFA) sets these limits, which vary by area and property type. Staying within these limits ensures you can access a conventional loan with 5 down. Exceeding them may require a jumbo loan, which often needs a higher down payment.

Lenders follow Fannie Mae Loan Guidelines to assess your eligibility, including credit score, income, and property type.

PMI Requirements and Costs

Private Mortgage Insurance (PMI) is required for any conventional loan with 5 down, since you’re putting less than 20% down. PMI protects your lender in case of default.

Typical PMI costs range from 0.5% to 1.5% of the loan amount annually, depending on your credit score and down payment. The good news: PMI can usually be canceled once you reach 20% equity, unlike FHA loans which often require longer-term insurance.

Real-World Example

Imagine a buyer purchasing a $600,000 home in 2026. With a conventional loan with 5 down, they put $30,000 down and finance $570,000. Monthly payments include principal, interest, taxes, insurance, and PMI. Once their equity hits 20%, PMI can be removed, reducing monthly costs.

Trends and Popularity

Recent data from 2023-2024 shows the average down payment nationwide hovered around 6-7%, while median home prices continued to rise. The conventional loan with 5 down is increasingly popular among both first-time and move-up buyers. This option offers a balance between accessibility and long-term affordability, helping more people achieve homeownership despite rising costs.

Understanding the nuances of a conventional loan with 5 down is crucial for making informed decisions. By leveraging updated guidelines and smart planning, you can step confidently into the market and secure your future home.

Who Qualifies for a 5% Down Conventional Loan?

Qualifying for a conventional loan with 5 down in 2026 is both accessible and competitive. Lenders look for well-documented financials, creditworthiness, and clear proof you can manage monthly mortgage payments. Let’s break down the key eligibility elements and see how you can position yourself for approval.

Credit Score Requirements

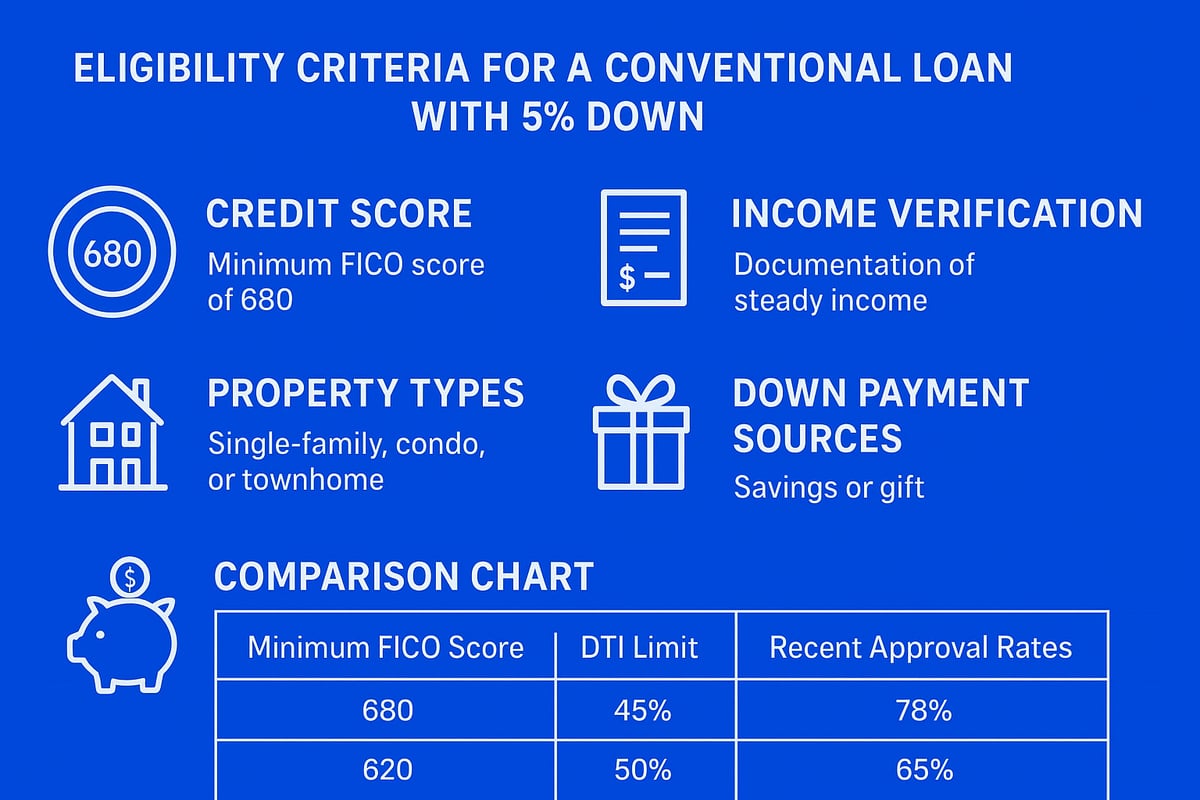

Lenders generally require a minimum FICO score of 620 for a conventional loan with 5 down. However, aiming for a score of 680 or higher can help you secure a better interest rate and smoother approval. If your score is on the lower end, you may face higher private mortgage insurance (PMI) costs or stricter loan terms.

Maintaining consistent credit habits—such as paying bills on time and reducing outstanding debts—will boost your chances. Review your credit report for errors and address any issues before applying. Some lenders may use automated underwriting systems that weigh higher credit scores more favorably, especially in competitive real estate markets.

Income and Employment Verification

Stable, verifiable income is essential when seeking a conventional loan with 5 down. Lenders calculate your debt-to-income (DTI) ratio, which typically must not exceed 43 percent, though some programs allow up to 45 percent with strong compensating factors.

Prepare to provide recent pay stubs, W-2s, tax returns, and bank statements. Consistent employment history—usually two years in the same field—strengthens your application, though exceptions can be made for recent graduates or those with career advancements. Self-employed applicants should expect to show two years of tax returns and possibly profit-and-loss statements.

Eligible Property Types and Occupancy

A conventional loan with 5 down is available for a range of property types. These include single-family homes, condos, townhomes, and, in certain cases, 2-4 unit properties. The property must generally be your primary residence, though some lenders allow second homes with specific restrictions.

Investment properties usually require a higher down payment and stricter qualifications. Condos may have additional eligibility requirements related to the homeowner association’s financial health and insurance coverage.

Source of Down Payment

You can use personal savings, retirement funds, or acceptable gift funds from relatives for your 5 percent down payment. Some buyers leverage grants or down payment assistance programs, provided they meet lender guidelines.

Lenders will verify the source of all funds to ensure compliance. Large, unexplained deposits can delay approval, so keep a paper trail for every transfer. Review the Fannie Mae and Freddie Mac 5% Down Payment Guidelines for specific rules on acceptable sources and documentation.

Recent Credit Events and Restrictions

If you’ve experienced a bankruptcy, foreclosure, or short sale in the past, you may face waiting periods before qualifying for a conventional loan with 5 down. For example, most lenders require at least four years after a Chapter 7 bankruptcy or two years after a Chapter 13 discharge.

Foreclosures typically require a seven-year waiting period, though extenuating circumstances can sometimes shorten this. Rebuilding your credit and maintaining solid financial habits post-event are crucial.

Example Scenarios and Approval Data

Consider these examples. A first-time buyer with a 690 FICO score, steady income, and minimal debt is likely to qualify for a conventional loan with 5 down on a $500,000 home. A repeat buyer with a recent job change but strong savings can also be eligible, especially with a solid employment offer letter. Self-employed applicants must provide detailed tax documentation but are not excluded.

According to recent data, approval rates for conventional loans with low down payments remain robust, particularly among buyers with strong credit and documented income. As more buyers embrace this option, lenders have become increasingly familiar with flexible sources of down payment and employment types.

Understanding these requirements puts you in control. By preparing your finances and documentation, you can confidently pursue a conventional loan with 5 down and move closer to homeownership.

Step-By-Step Guide: Securing Your Conventional Loan With 5% Down

Ready to unlock your path to homeownership? The following step-by-step guide breaks down each phase of obtaining a conventional loan with 5 down, equipping you to navigate the process confidently. From financial preparation to closing day, each step is designed to help you maximize your chances of approval and secure the keys to your new home.

Step 1: Assess Your Financial Readiness

Begin your journey with a clear picture of your finances. Review your credit report and score, as a strong credit profile significantly boosts your chances of approval for a conventional loan with 5 down. Check for errors and address any outstanding debts to improve your standing.

Next, calculate your budget. Factor in your monthly income, expenses, and any existing debts. Use mortgage calculators to estimate your monthly payment, including principal, interest, taxes, insurance, and PMI, which is required for a conventional loan with 5 down.

Determine the total cash needed for your purchase. This includes the 5 percent down payment, closing costs (typically 2-5 percent of the purchase price), and any reserve funds your lender may require. Consider additional expenses such as moving costs and initial repairs.

Gathering knowledge early is key. Explore resources like the Homeownership Education Guide to better understand the financial responsibilities and long-term benefits of owning a home with a conventional loan with 5 down.

Step 2: Get Pre-Approved by a Lender

Pre-approval is essential in 2026’s competitive market. It shows sellers you’re a serious, qualified buyer. Start by choosing lenders experienced with the conventional loan with 5 down program. Gather required documents: W-2s, recent pay stubs, two years of tax returns, and bank statements showing your down payment and reserves.

Submit your documents for a preliminary review. The lender will check your credit score, verify your income, and calculate your debt-to-income ratio. This step is critical for a conventional loan with 5 down, as lenders want to ensure you can handle both the payment and additional costs like PMI.

Compare rate quotes from several lenders. Review estimated interest rates, closing costs, and loan terms. A pre-approval letter strengthens your offer when you begin house hunting, giving you a vital edge over buyers without financing in place.

Step 3: Shop for Your Home

With pre-approval in hand, partner with a knowledgeable real estate agent who understands the local market and the nuances of a conventional loan with 5 down. Focus your search on homes within your approved price range and that meet conforming loan limits.

Consider neighborhoods with growth potential and strong resale values. View a variety of property types—single-family homes, condos, or eligible multi-units—ensuring they fit conventional loan with 5 down guidelines.

Attend open houses, tour properties, and compare features. Keep an eye on condition, location, and future value. Your agent can help you analyze recent sales data and identify homes likely to appreciate, maximizing your investment potential.

Step 4: Make an Offer and Negotiate

When you find the right property, work with your agent to craft a compelling offer. A conventional loan with 5 down is viewed favorably in many markets, but you may face competition. Include a pre-approval letter with your offer to demonstrate your financial readiness.

Use negotiation strategies to strengthen your position. Consider offering a flexible closing date or higher earnest money deposit. In some cases, you can request seller concessions to help cover closing costs, making your conventional loan with 5 down even more affordable.

Include essential contingencies for inspection, appraisal, and financing to protect your interests. These safeguards allow you to address issues or renegotiate if surprises arise during the process.

Step 5: Complete the Loan Application Process

Once your offer is accepted, submit a full mortgage application with all supporting documents. The lender will order an appraisal to confirm the home’s value meets the requirements for a conventional loan with 5 down.

The underwriting process involves reviewing your credit, verifying employment, assessing assets, and ensuring the property qualifies. Respond promptly to any additional requests from your lender to prevent delays with your conventional loan with 5 down.

Schedule a home inspection to uncover potential issues. Address repairs with the seller if needed, and finalize your homeowner’s insurance policy. Stay in close contact with your lender and agent to keep everything on track.

Step 6: Close on Your New Home

As closing day approaches, review your final Closing Disclosure. This document outlines the terms of your conventional loan with 5 down, itemized closing costs, and the total amount due at settlement.

Complete a final walk-through of the property to ensure agreed-upon repairs are finished and the home is in expected condition. On closing day, sign legal documents and transfer funds for your down payment and closing costs.

After the transaction is funded, you’ll receive the keys to your new home. Celebrate the achievement—your disciplined approach to the conventional loan with 5 down process means you are officially a homeowner, ready to enjoy all the benefits that come with it.

Comparing 5% Down Conventional Loans to Other Low Down Payment Options

For many buyers, choosing the right mortgage means weighing a conventional loan with 5 down against other low down payment options. The right path depends on your credit, savings, eligibility, and long-term goals. Let’s break down how these loan types compare and what sets each apart for today’s homebuyer.

Side-by-Side Comparison Table

Below is a quick reference table comparing the most common low down payment loans. Notice how a conventional loan with 5 down offers flexibility and competitive terms for a wide range of buyers.

| Loan Type | Down Payment | Upfront Insurance | Ongoing Insurance | Loan Limits | Who Qualifies |

|---|---|---|---|---|---|

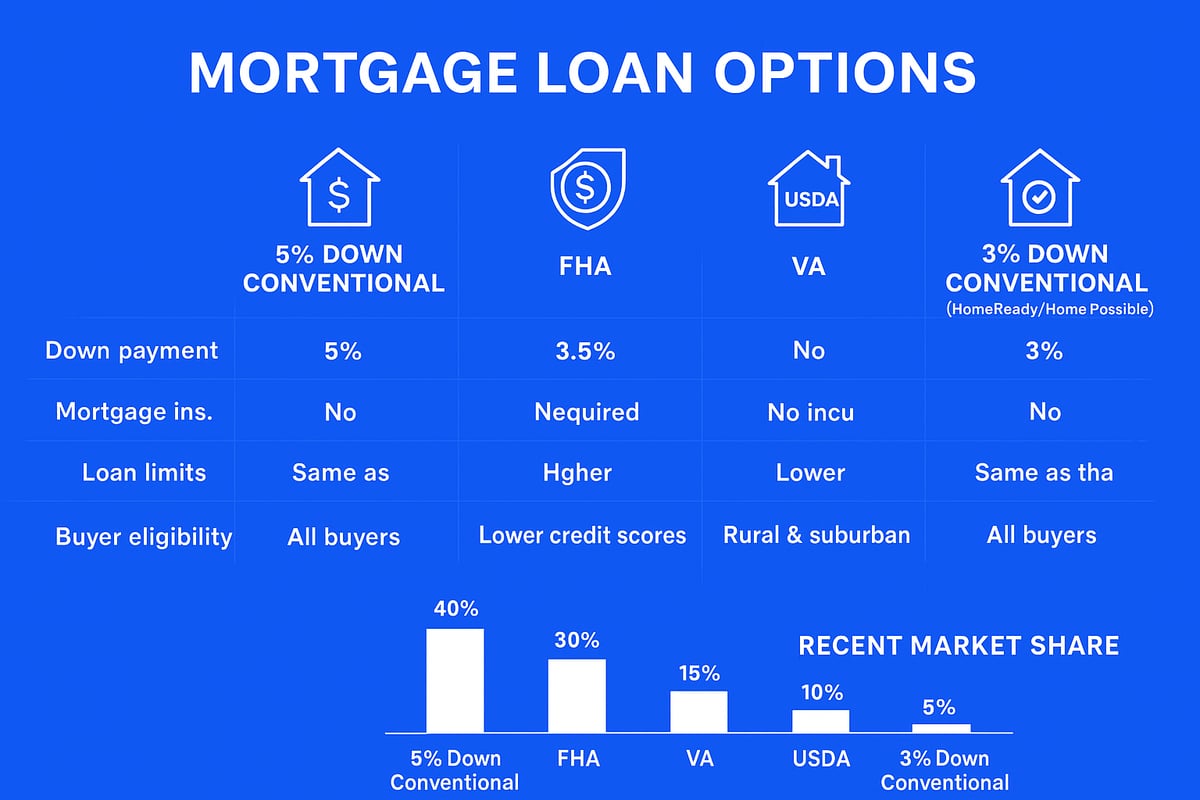

| Conventional 5% | 5% | None | PMI, cancellable | Conforming | Most buyers, good credit |

| FHA | 3.5% | Upfront MIP | Monthly MIP | FHA limits | Lower credit OK |

| VA | 0% | Funding Fee | None | Conforming | Eligible veterans |

| USDA | 0% | Guarantee Fee | Annual Fee | USDA limits | Rural, income capped |

| Conventional 3% | 3% | None | PMI, cancellable | Conforming | First-time/Income limits |

*PMI = Private Mortgage Insurance, MIP = Mortgage Insurance Premium

How Each Option Stacks Up

A conventional loan with 5 down is appealing for buyers who want to avoid the upfront mortgage insurance premium required by FHA loans. Unlike FHA, PMI for conventional loans can be removed once you reach 20% equity, which lowers your long-term costs. VA and USDA loans allow for zero down, but have strict eligibility rules—VA loans are for veterans, while USDA loans require a rural location and meet income caps.

FHA loans remain popular for those with lower credit scores or limited savings. However, the ongoing mortgage insurance cannot be dropped unless you refinance. If you want more details on how mortgage insurance works and how it impacts your payments, see Mortgage Insurance Explained.

Conventional 3% down loans, such as HomeReady and Home Possible, target first-time buyers or those with moderate incomes. These programs offer even lower entry barriers, but have extra eligibility requirements.

Real-Life Scenario: Which Loan Fits Best?

Consider a first-time buyer choosing between an FHA loan and a conventional loan with 5 down. With a strong credit score, the buyer qualifies for both. The conventional loan with 5 down means no upfront insurance premium and the ability to cancel PMI later, which can save thousands over the life of the loan. For buyers who want flexibility and plan to stay in their home for years, the conventional route is often the smarter play.

Market Trends and Data

Recent statistics show that the share of buyers using a conventional loan with 5 down has increased as home prices rise. According to 2023-2024 Average Down Payments and Median Home Prices, more buyers are putting down between 3% and 5%, especially in high-cost markets. FHA and VA loans still serve important roles, but the conventional loan with 5 down is now the most popular choice for many qualified homebuyers.

Ultimately, comparing each loan’s features helps you align your financing with your needs. Review your eligibility, long-term plans, and the true cost of each option before making your decision.

Expert Strategies to Maximize Your Success With a 5% Down Conventional Loan

Unlocking the full potential of a conventional loan with 5 down requires more than just meeting the basic requirements. With a few expert strategies, you can position yourself for approval, secure better rates, and save thousands over the life of your loan.

Boost Your Credit Score for Better Rates

Start by reviewing your credit report well before applying for a conventional loan with 5 down. Even a modest increase in your score can translate to lower interest rates and smaller monthly payments. Pay down high credit card balances, dispute any errors, and avoid new credit inquiries. If your score is below 700, consider a rapid rescore or work with a professional for tailored advice.

Minimize PMI Costs and Plan for Early Removal

Private mortgage insurance (PMI) is required for any conventional loan with 5 down, but you can take steps to reduce its impact. Compare lender-paid versus borrower-paid PMI options to find the best fit. Always ask your lender to outline when and how you can cancel PMI as your equity grows. For more details on costs and cancellation, see Private Mortgage Insurance (PMI) Requirements and Costs.

Leverage Gift Funds and Assistance Programs

Maximize your purchasing power by taking advantage of allowable gift funds from family or approved sources. Many buyers using a conventional loan with 5 down also combine their own savings with grants or down payment assistance programs. Explore local and state options, which can help cover closing costs or supplement your down payment, making homeownership more accessible.

Time Your Home Purchase for Maximum Advantage

The real estate market fluctuates seasonally. If possible, time your home search to less competitive months, like late fall or early winter, to secure better deals. Buyers using a conventional loan with 5 down may find sellers more willing to negotiate during slower periods, which can translate to lower prices or added concessions.

Negotiate Seller Credits for Closing Costs

Negotiating seller credits can significantly reduce your out-of-pocket expenses at closing. With a conventional loan with 5 down, request that the seller contribute toward closing costs or prepaid items. This approach can free up your cash for reserves or future home improvements, strengthening your financial position from day one.

Build Equity Faster With Extra Payments

Accelerate your path to 20 percent equity by making extra principal payments or switching to a biweekly payment plan. Even small additional payments can shorten your PMI timeline and save you thousands in interest over the life of your conventional loan with 5 down. Set up automatic transfers to stay consistent and watch your equity grow.

Avoid Common Pitfalls During the Process

Stay vigilant throughout the mortgage process. Do not take on new debts, open new credit lines, or make large purchases until after closing. Any sudden financial changes can jeopardize your approval for a conventional loan with 5 down. Keep your finances stable and respond promptly to any lender requests for documentation.

Case Study: Optimizing the Loan Structure

Consider a recent buyer in a high-cost metro area who used these strategies with their conventional loan with 5 down. By improving their credit score, negotiating seller credits, and making extra payments, they shaved years off their PMI obligation and saved thousands in interest. With careful planning, you can achieve similar results and confidently navigate the homebuying journey.

As you look ahead to making your homeownership dreams a reality in 2026, it’s clear that understanding your options—like securing a conventional loan with just 5 down—can make all the difference. Whether you’re a first time buyer navigating Seattle’s competitive market or an experienced investor looking for strategic guidance, having an expert by your side can help you move forward with confidence. If you’re ready to explore what’s possible and want tailored advice for your unique situation, Let’s have a conversation about your next steps.