Are you a Seattle homeowner searching for ways to lower your monthly payments or unlock your home’s equity in 2026? The home loans refinance landscape is evolving rapidly, and knowing how to navigate it can mean major savings or new financial opportunities.

This guide gives homeowners in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett expert-backed strategies for a successful home loans refinance. You will find clear explanations of refinance basics, the latest Seattle market trends, step-by-step processes, loan options, cost breakdowns, and professional tips tailored to your community.

Imagine cutting your interest rate or funding those long-awaited renovations without stress. With local insights and proven advice, you can approach your home loans refinance confidently and maximize your results in 2026.

Understanding Home Loan Refinancing in Seattle

Navigating home loans refinance in Seattle requires clear understanding and a local perspective. Whether you want to save on interest, tap into home equity, or restructure your finances, knowing your options is essential. Let us break down the basics and highlight what makes refinancing unique in the Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett areas.

What Is Home Loan Refinancing?

Home loans refinance means replacing your current mortgage with a new loan, often to secure better financial terms. Seattle homeowners typically refinance to lower their interest rate, reduce monthly payments, consolidate debt, or access cash for renovations. For example, a Shoreline homeowner might pursue refinancing to update a classic Craftsman bungalow. In 2025, 37% of King County homeowners considered refinancing as interest rates dipped, according to local MLS data. Remember, home loans refinance is not a one-size-fits-all solution—each situation is unique and should be evaluated carefully.

Reasons to Refinance in 2026

There are several compelling reasons to consider home loans refinance in 2026, especially given Seattle’s dynamic real estate environment. Motivations often include:

- Lowering your interest rate as economic conditions shift

- Adjusting your loan term to better fit your financial goals

- Switching from an adjustable to a fixed-rate mortgage for greater stability

- Accessing home equity for large expenses or investments

For instance, an Everett family might use a cash-out refinance to pay for college tuition. With Seattle’s tech-driven market, homeowners could encounter unique opportunities that make home loans refinance particularly attractive this year.

How Seattle’s Market Impacts Refinancing

Seattle’s robust housing market directly influences home loans refinance opportunities. Significant home value appreciation in Seattle, Lynnwood, and Mill Creek has increased homeowner equity. This boost, combined with competition among local lenders, often leads to improved rates and faster closing times. City-specific regulations, such as energy efficiency incentives, can further impact the process. According to NWMLS, the median Seattle home price rose 6.2% year-over-year in 2025. Timing your refinance to align with local market cycles can maximize your benefits.

Common Refinancing Myths and Mistakes

Many Seattle homeowners believe home loans refinance is too expensive or overly complicated, but this is often a misconception. Common mistakes include failing to shop with multiple Seattle-area lenders and missing out on potential savings. For example, a Lake Forest Park homeowner who didn’t compare lenders lost out on thousands. In reality, closing costs are frequently recouped within two to three years. Education and preparation are crucial—explore Seattle mortgage refinancing tips to avoid these common pitfalls and make informed decisions.

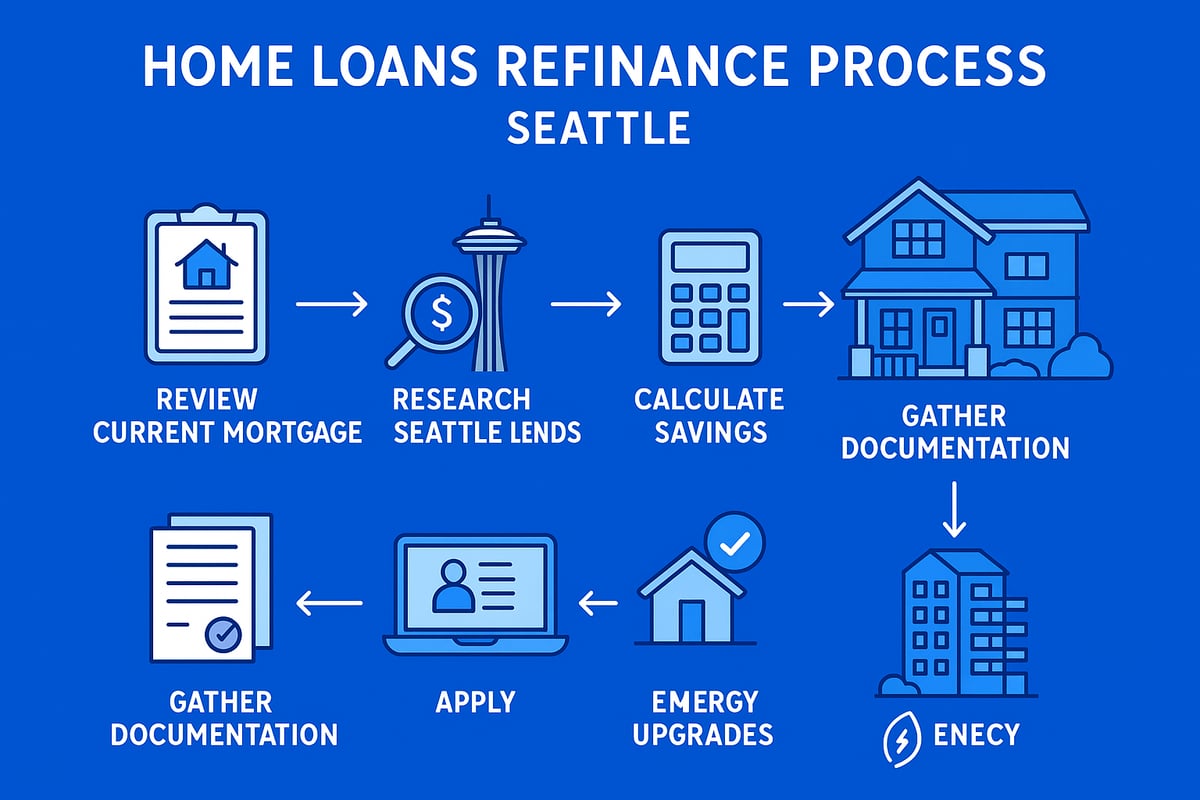

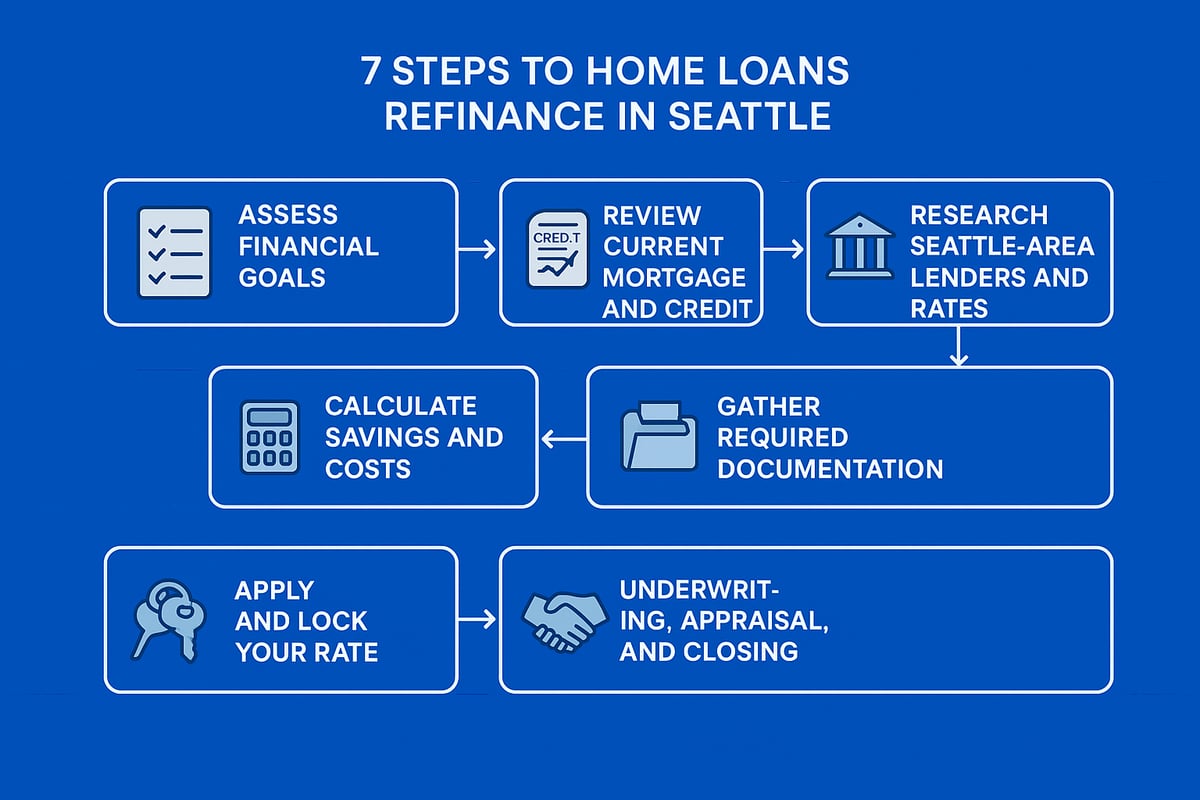

Step-by-Step Guide to Refinancing Your Home Loan in Seattle

Refinancing your mortgage in the Seattle area can seem complex, but breaking it into clear steps makes the process manageable. Whether you live in Shoreline, Lynnwood, Mill Creek, or Everett, following these best practices ensures your home loans refinance journey is efficient and rewarding. Let’s walk through each phase to help Seattle homeowners maximize savings and peace of mind.

Step 1: Assess Your Financial Goals

Begin your home loans refinance by defining what you want to achieve. Are you looking to lower monthly payments, reduce your loan term, tap into equity, or consolidate debt? For example, a Mill Creek couple may debate whether to access equity for renovations or shorten their term for faster payoff.

Clarifying your objectives ensures you select the right loan product. Consider how your refinance aligns with your long-term financial plans. A clear goal is the foundation for a successful home loans refinance.

Step 2: Review Your Current Mortgage and Credit

Next, collect your latest mortgage statement and note your current interest rate, balance, and payment details. Check your credit score before starting a home loans refinance, as higher scores can unlock better rates.

Suppose an Everett homeowner improves their credit from 680 to 740. This can result in substantial savings over the life of the loan. Review your debt-to-income ratio and gather documents that reflect your financial profile.

Step 3: Research Seattle-Area Lenders and Rates

Comparing banks, credit unions, and mortgage brokers is crucial for a competitive home loans refinance. Seattle-based lenders may offer programs tailored to local needs, like tech professionals with RSUs or those seeking green incentives.

Use online tools and consult experts to track current rates. For in-depth insights on rate trends, visit Understanding Seattle mortgage rates. In 2025, King County’s average refinance APR ranged from 5.2 to 6.3 percent, making lender comparison essential.

| Lender Type | Rate Programs | Local Expertise | Specialized Options |

|---|---|---|---|

| Bank | Standard, Jumbo | Moderate | Some |

| Credit Union | Member Discounts | High | Yes |

| Mortgage Broker | Multiple Lenders | High | Yes |

Step 4: Calculate Potential Savings and Costs

Before committing to a home loans refinance, use calculators to estimate your break-even point. Seattle closing costs typically range from $3,000 to $6,000 depending on loan size and complexity.

For instance, a Shoreline homeowner lowering their rate by 1 percent may recoup costs in just 18 months. Factor in property taxes, insurance, and potential escrow adjustments to get a clear financial picture.

Step 5: Gather Required Documentation

Be prepared to provide:

- Income verification (W-2s, paystubs, RSU statements for tech workers)

- Asset and bank statements

- Homeowner’s insurance policy

- Government-issued ID

If you have an ADU or recent energy-efficient upgrades in Seattle, bring documentation, as these can impact your home’s value and eligibility for incentives during your home loans refinance.

Step 6: Apply and Lock Your Rate

Once you’ve selected a lender, submit a complete application for your home loans refinance. Timing matters: monitor rate trends and consider locking when rates dip.

A Lynnwood applicant who locked during a brief April 2026 rate drop secured significant long-term savings. Ask about rate lock duration and the process for re-locking if market conditions improve.

Step 7: Underwriting, Appraisal, and Closing

Your lender will order a new appraisal, especially important as Seattle, Everett, and Mill Creek home values continue to rise. Underwriters will review your documentation and may request clarification or additional items.

Address any outstanding conditions quickly to keep your home loans refinance on track. The final step is closing, where you sign documents, pay closing costs, and your new loan funds. Most Seattle-area refinances close within 21 to 30 days.

A smooth home loans refinance process relies on preparation, clear communication, and understanding each stage. By following these steps, Seattle homeowners can confidently navigate refinancing and achieve their financial goals.

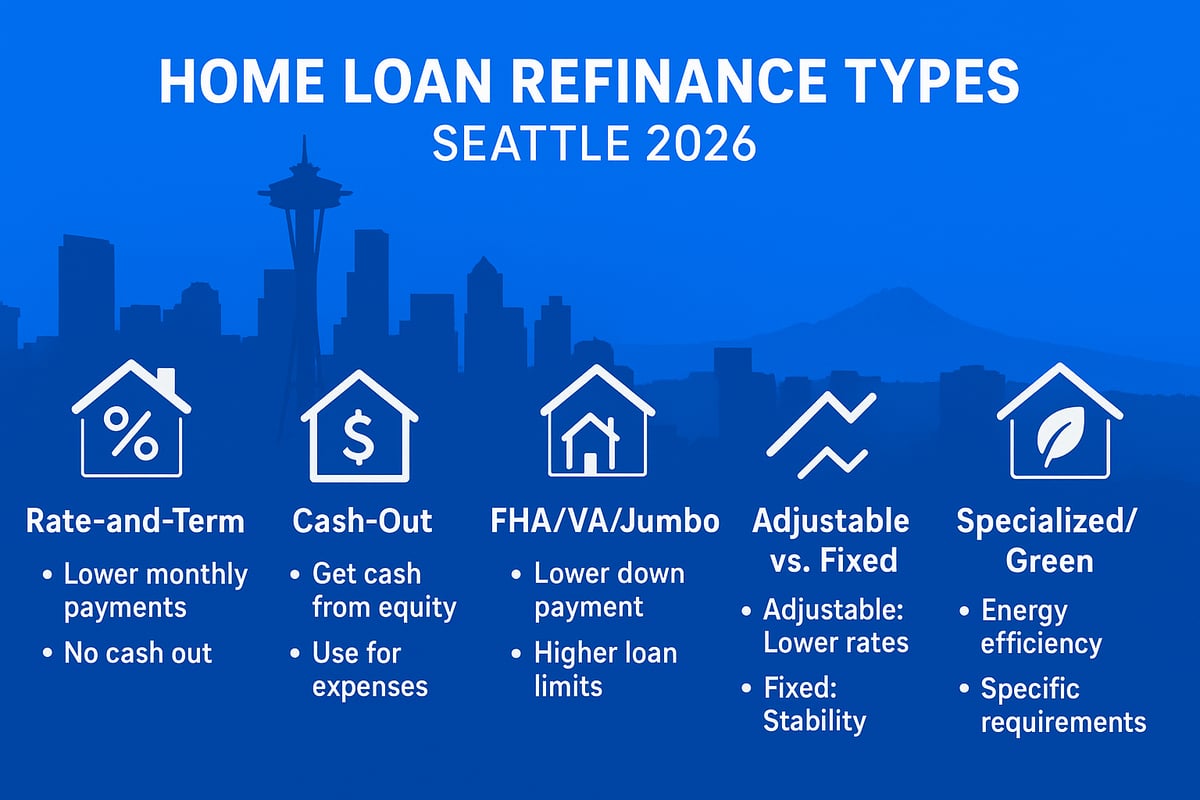

Types of Home Loan Refinancing Options in 2026

Seattle-area homeowners in 2026 have a diverse menu of home loans refinance solutions tailored to unique goals, property types, and financial profiles. Understanding the differences between each option is essential for making informed decisions that align with your needs in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

Rate-and-Term Refinance

A rate-and-term refinance replaces your current mortgage with a new one, adjusting the interest rate, the term, or both. In Seattle, this is the most common home loans refinance strategy for those seeking lower payments or a quicker payoff.

For example, a Redmond homeowner might switch from a 30-year to a 15-year fixed loan, reducing interest costs long-term. In 2025, 65% of Seattle refinances were rate-and-term, reflecting local demand for payment relief and stability.

This option is ideal if you want to improve your loan terms without tapping your equity. Always compare offers from Seattle-based lenders to maximize savings.

Cash-Out Refinance

A cash-out refinance lets you borrow more than your remaining mortgage balance, receiving the difference in cash. Many Seattle homeowners use this home loans refinance method to fund remodels, pay off high-interest debt, or invest in additional property.

For instance, a Lake Forest Park family may leverage rising home values to update their kitchen. However, it is crucial to remember that your new balance and monthly payment may be higher.

Review your financial plan to ensure a cash-out refinance aligns with your long-term goals, especially as Seattle equity continues to grow.

FHA, VA, and Jumbo Refinancing

Specialized loans—FHA, VA, and Jumbo—expand home loans refinance access for different borrower profiles. FHA options suit lower credit or smaller down payments, though Seattle’s high median prices often exceed FHA limits.

VA loans benefit veterans and active military, offering zero down and flexible terms. Jumbo loans cover amounts above $1,063,750, common for homes in Bellevue and Seattle. For a detailed breakdown of these options, see FHA, VA, and jumbo loan options.

A Bellevue tech professional might use a jumbo cash-out refinance to purchase an investment property, demonstrating the versatility of these products.

Adjustable-Rate vs. Fixed-Rate Refinance

Choosing between an adjustable-rate and a fixed-rate refinance is a key step in any home loans refinance process. Fixed-rate loans offer predictable payments, making them popular as rates rise.

Adjustable-rate loans start with lower rates, but payments can increase in the future. In 2025, 78% of Seattle refinancers chose fixed rates for peace of mind, especially in long-term scenarios.

If you plan to move within a few years, an adjustable-rate may suit you. Otherwise, fixed-rate stability is often preferred in Seattle’s dynamic market.

Specialized Programs and Green Incentives

Seattle and cities like Everett, Lynnwood, and Mill Creek offer unique home loans refinance programs. Energy-efficient mortgage (EEM) programs reward upgrades like solar panels or insulation with better rates or credits.

Some lenders in Shoreline and other areas provide incentives for green renovations, reducing costs for eco-conscious homeowners. For instance, a Mill Creek homeowner could qualify for a rate reduction after installing solar panels.

Explore local and state programs to maximize your refinance benefits, especially if you are planning energy upgrades.

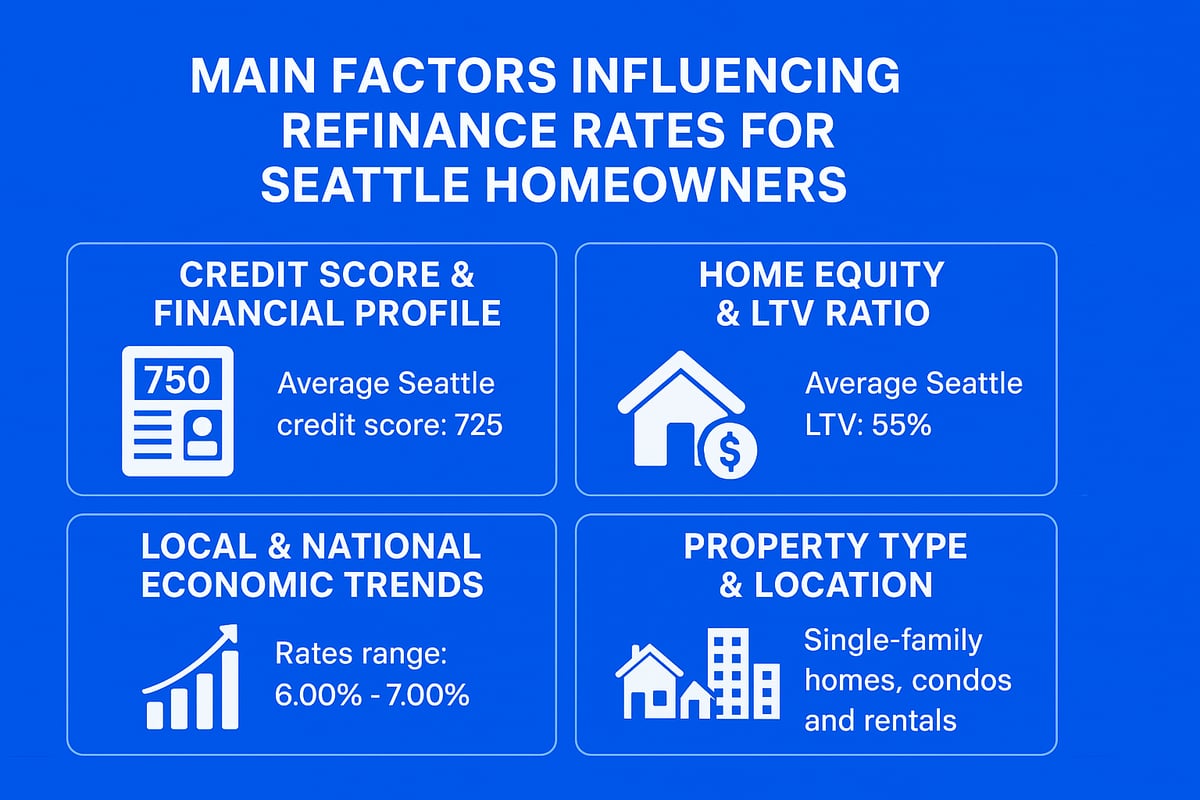

Factors Influencing Refinance Rates in Seattle

Understanding what shapes refinance rates is crucial for Seattle homeowners planning a home loans refinance. Multiple elements come into play, from your credit profile to the unique dynamics of the local market. Let’s break down the major factors affecting your options in Seattle, Shoreline, Lynnwood, Mill Creek, Lake Forest Park, and Everett.

Credit Score and Financial Profile

Your credit score is one of the most significant factors in determining your home loans refinance rate in Seattle. Lenders typically reserve the best rates for borrowers with scores of 740 or higher. If your score falls below that threshold, you may still qualify, but expect slightly higher rates.

Debt-to-income ratio (DTI) and asset verification also influence lender decisions. For example, an Everett homeowner who pays down credit card balances and avoids new loans before applying can often secure a lower rate. Tech professionals, especially in Lynnwood and Mill Creek, should document RSUs or bonuses, as these can strengthen your financial profile for a home loans refinance.

Home Equity and Loan-to-Value (LTV) Ratio

The amount of equity you have in your property directly affects your ability to qualify for a home loans refinance and secure the most competitive rates. In Seattle and surrounding cities, rising home values help many homeowners achieve a favorable loan-to-value (LTV) ratio, often between 75 and 85 percent.

A lower LTV means less risk for the lender and typically lower rates for you. For instance, a Lake Forest Park family with significant equity from recent appreciation may qualify for better terms than someone with minimal equity. Remember, the more equity you bring to your home loans refinance, the more options you unlock.

Local and National Economic Trends

Wider economic conditions, both locally and nationally, play a key role in home loans refinance rates. Federal Reserve policy, inflation, and job market strength all impact what lenders offer. Seattle’s tech sector and employment trends can cause rates to shift quickly—especially in hot markets like Shoreline and Bellevue.

Additionally, local market dynamics such as Seattle housing market experiencing low turnover influence lender risk and refinance availability. When fewer homes change hands, lenders may adjust rates or incentives to attract refinancing business. Staying informed on these trends helps you time your home loans refinance for maximum benefit.

Property Type and Location

The type and location of your property also influence home loans refinance rates in Seattle and nearby areas. Single-family homes, condos, and multi-family residences each carry different risk profiles for lenders. For example, a Mill Creek condo may have stricter appraisal requirements than a Shoreline single-family home.

Locations with lower property taxes or insurance costs, such as certain neighborhoods in Everett, can also impact your total refinance expenses. Green-certified properties or those with recent energy-efficient upgrades may even qualify for additional rate discounts, making your home loans refinance more affordable.

Costs, Fees, and Break-Even Analysis for Seattle Refinancing

Navigating the costs and fees of home loans refinance in Seattle is essential for homeowners aiming to maximize savings. Understanding each expense, from application to closing, helps you make informed decisions and avoid surprises when refinancing in neighborhoods like Shoreline, Mill Creek, or Everett.

Typical Closing Costs in Seattle Area

When considering a home loans refinance in Seattle, expect closing costs to range from $3,500 to $6,000 depending on your loan type and property value. These fees typically include:

- Origination charges from your lender

- Appraisal and credit report fees

- Title insurance and escrow services

- Recording and notary charges

For example, a Mill Creek borrower might negotiate lender credits to offset some of these expenses, especially if their property has recent energy-efficient upgrades. In some cases, incentives for green improvements can reduce closing costs. Always request a loan estimate to see a full breakdown before proceeding.

Prepayment Penalties and Other Hidden Fees

Before finalizing a home loans refinance, review your existing mortgage for any prepayment penalties. Some older loans in Lake Forest Park or Lynnwood still carry these charges, which can impact your overall savings. Watch for:

- Escrow shortages or property tax adjustments at closing

- Additional recording fees, which in Seattle can add $400 to $700

- Charges for wire transfers or overnight document delivery

Understanding these hidden fees ensures you accurately compare offers and avoid unexpected costs. If you have questions, ask your lender for a detailed fee explanation upfront.

Calculating Your Break-Even Point

A critical step in home loans refinance is determining your break-even point—the time it takes to recover refinancing costs through monthly savings. Use this formula:

Break-Even (months) = Total Closing Costs ÷ Monthly Payment Savings

For instance, if a Shoreline homeowner pays $4,500 in closing costs and saves $225 a month, the break-even point is 20 months. Online refinance calculators make this process fast and transparent.

| Example | Closing Costs | Monthly Savings | Break-Even (months) |

|---|---|---|---|

| Shoreline | $4,500 | $225 | 20 |

Always factor in property taxes and insurance changes, which can affect your true savings.

When Refinancing Makes (and Doesn’t Make) Sense

A home loans refinance is a smart move if you plan to stay in your Seattle-area home long term, see a meaningful rate drop, or need to access equity. However, if you’re considering selling soon, or if rate improvement is marginal, refinancing may not be cost-effective.

Seattle’s dynamic market means timing matters. Consider future appreciation, job mobility, and available local programs. For those investing in upgrades, energy-efficient home upgrades and refinancing can sometimes unlock additional incentives, reducing your overall costs.

Always weigh the total investment against your financial goals before moving forward with a home loans refinance.

Pro Tips for a Smooth and Successful Refinance in 2026

If you are preparing for a home loans refinance in Seattle, a strategic approach can make all the difference. Homeowners in Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett can benefit from these expert-backed tips, designed to streamline the process and maximize savings.

Shop Multiple Lenders and Programs

Start your home loans refinance journey by gathering at least three to five offers from a variety of lenders. Include Seattle-based credit unions, national banks, and online mortgage providers. This comparison helps ensure you secure the best rate, as local lenders in Lynnwood or Everett may offer unique incentives.

Ask each lender about available credits, rate buydowns, and city-specific programs. Do not hesitate to switch lenders during the process if you find better terms elsewhere. This flexibility can save you significant money throughout your home loans refinance.

Prepare for the Appraisal Process

A strong appraisal is key to a successful home loans refinance in Seattle. Before the appraiser visits, tidy up your property, address minor repairs, and compile documentation of recent upgrades. Homes in Everett and Redmond that feature energy-efficient improvements or updated landscaping often receive higher valuations.

Providing records of completed renovations or green upgrades, such as solar panels, can also make a difference. These details help your home loans refinance application stand out and maximize your available equity.

Maximize Your Credit and Financial Profile

Your credit profile plays a crucial role in home loans refinance approval and the interest rates offered. Pay down outstanding debts, avoid new credit inquiries, and update your income documentation. For tech professionals in Bellevue or Mill Creek, be sure to include RSUs, stock options, and bonuses when submitting paperwork.

Improving your credit score by even a few points can lower your refinance rate and monthly payment. Lenders in the Seattle area reward well-prepared applicants with more competitive terms on home loans refinance.

Time Your Application Strategically

Seattle’s market can shift quickly, so timing is everything for a home loans refinance. Monitor mortgage rate trends and consider locking in your rate during seasonal dips, such as those seen in late March or October. When mortgage applications surge, as they did in 2025, lenders often become more competitive, offering better deals to attract business. For more on recent application trends, see Mortgage applications reach highest level since 2022.

Working with a lender familiar with Seattle’s spring and summer cycles can also provide insight into the most favorable windows for home loans refinance.

Understand Seattle-Specific Regulations and Programs

Seattle and surrounding cities offer a variety of programs that can reduce costs or provide additional benefits during a home loans refinance. Research local incentives for green renovations, such as Everett’s Home Energy Rebate or Lynnwood’s lender credits for solar installations.

Check King County’s property tax exemptions for seniors and veterans, as well as city-level assistance with closing costs. These resources can significantly impact the total expense and outcome of your home loans refinance.

Frequently Asked Refinance Questions in Seattle

Seattle homeowners often have questions about home loans refinance, including:

- Can I refinance with less than 20% equity?

- How do condo rules in Seattle affect refinancing?

- What if my home value has dropped since purchase?

- Are there options for first-time refinancers?

- How long does the process take locally?

If you are considering tapping into home equity, learn how homeowners are leveraging cash-out refinancing amid equity gains to fund renovations or investments. Staying informed and consulting local experts ensures your home loans refinance process is smooth and successful.

Refinancing in 2026: What Seattle Homeowners Should Watch For

Seattle homeowners considering home loans refinance in 2026 face a dynamic landscape shaped by both local and national trends. Staying informed about projected rates, evolving regulations, and market shifts in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett is essential for making confident refinancing decisions.

Projected Rate Trends and Economic Outlook

In 2026, most experts anticipate mortgage rates will stabilize between 5.5 percent and 6.2 percent, following recent shifts in Federal Reserve policy and steady inflation levels. Seattle’s robust tech sector and strong job market are expected to support continued home value growth in Mill Creek and Everett, making home loans refinance an appealing option for many.

Local housing trends also play a role. For example, Seattle home sellers offering more buyer incentives could mean more negotiating power for buyers, indirectly affecting refinance appraisals and loan terms. Monitoring employment data and home price forecasts in Shoreline and Lynnwood will help you identify the right window for your home loans refinance application.

Regulatory and Program Changes

Seattle homeowners should watch for updates to FHA, VA, and jumbo loan limits for King County in 2026. Adjustments to these thresholds can expand or restrict refinancing options, especially as Seattle’s median home price rises. The city and state may also introduce new incentives, such as grants or rate reductions, for energy-efficient upgrades.

Proposed property tax relief for refinancers in Seattle could further impact your break-even analysis when considering home loans refinance. Always verify eligibility for these programs and discuss them with your lender, as requirements may differ for condos in Lynnwood or single-family homes in Lake Forest Park.

Equity-Building and Long-Term Strategy

A strategic home loans refinance can help you accelerate equity growth or unlock funds for additional investments, such as building an ADU in Everett or updating a Craftsman in Shoreline. Seattle and Bellevue’s appreciation trends make long-term planning especially beneficial for those intending to stay in their homes.

Some homeowners use cash-out refinancing to invest in rental properties or fund renovations that boost value. Review your financial goals and evaluate how your home loans refinance aligns with your desired equity timeline. Consider local appreciation rates when estimating future return on investment in Mill Creek and surrounding areas.

Pitfalls to Avoid and Final Expert Tips

Avoid rushing into a home loans refinance without comparing lenders or fully understanding your total loan costs. Skipping a break-even analysis or overlooking city-specific incentives can lead to missed opportunities. Seattle’s market is competitive, so take time to gather multiple quotes and check for closing cost assistance programs.

Stay alert for changing regulations and consult a trusted mortgage professional who knows the Seattle, Shoreline, and Everett markets. Being proactive and informed increases your chances of a smooth, cost-effective home loans refinance experience in 2026.

After exploring the key steps and expert strategies for refinancing your home loan in Seattle, you might be wondering what your next move should be. Every homeowner’s situation is unique—whether you’re optimizing for lower payments, leveraging equity, or navigating the fast-paced Seattle market, having a thoughtful conversation with a local expert can make all the difference. If you’d like personalized guidance tailored to your goals and financial landscape, I invite you to Let’s have a conversation. Together, we can chart a clear, confident path toward your best refinancing outcome in 2026.

Key Takeaways

- Homeowners in Seattle can lower monthly payments and unlock equity through effective home loans refinance strategies in 2026.

- Understanding local market trends and loan options is crucial for a successful refinance process.

- Gather multiple offers from different lenders to secure the best rates and terms for refinancing.

- Consider your financial goals, credit score, and equity when evaluating refinancing options.

- Be aware of closing costs and potential savings to make informed decisions on your home loans refinance.

Estimated reading time: 18 minutes