If your compensation is heavy on RSUs and bonuses, you have probably had this moment: your pay stub looks modest, your offer letter looks impressive, and the online mortgage calculator treats you like neither one is real. That disconnect matters more in Seattle than almost anywhere because pricing moves fast, appraisal gaps happen, and sellers reward certainty.

Tech workers do not need “special treatment” in the mortgage process. You need the right structure and the right documentation so your income is understood the same way you and your employer understand it.

In the world of personal finance, particularly when it comes to mortgages, there’s often a misconception that tech workers require unique processes or “special treatment.” This notion overlooks a fundamental truth: the mortgage process fundamentally relies on clear, accurate documentation and a standard understanding of income. Tech workers, like any other professionals, possess diverse income structures, including base salaries, bonuses, and equity compensation. However, it’s crucial that these elements are thoroughly documented and clearly presented to lenders. With the right structure in place, tech employees can demonstrate their financial viability to mortgage underwriters just as effectively as individuals in more traditional careers.

The key to navigating the mortgage process successfully lies in transparency and clarity. Tech workers should focus on providing comprehensive documentation, such as pay stubs, tax returns, and statements regarding stock options or other variable income. These documents help lenders understand the full scope of an applicant’s earning potential, eliminating any ambiguity that might arise from unconventional income sources common in the tech industry. By ensuring that their financial picture is clearly communicated, tech workers can expedite their mortgage approval process without the need for special concessions. In essence, the mortgage industry operates on established principles; thus, anyone—regardless of their profession—can secure a mortgage when they’re prepared and fully equipped with the right evidence of their income.

Navigating the mortgage process can often feel overwhelming, especially for tech workers whose income structures may not fit the traditional mold. The key to successfully securing a mortgage lies in transparency and clarity throughout the application process. Lenders need a complete understanding of an applicant’s financial situation, which is why it’s essential for tech professionals to provide thorough documentation. This includes pay stubs, tax returns, and detailed statements regarding stock options or other forms of variable income. By presenting a comprehensive financial picture, tech workers can eliminate ambiguity surrounding their earning potential, making it easier for lenders to assess their application.

Navigating the mortgage process can often feel overwhelming, especially for tech workers whose income structures may not fit the traditional mold. Many professionals in the tech industry receive compensation that includes a mix of base salary, bonuses, and stock options, which can complicate the mortgage application process. Unlike more conventional income streams, these variable components may not always be straightforward for lenders to evaluate. As a result, understanding the nuances of your financial situation and effectively communicating that information is crucial. Transparency is key, as it allows lenders to assess your capacity to repay a loan accurately, thereby increasing your chances of securing favorable mortgage terms.

Navigating the mortgage process can often feel overwhelming, particularly for tech workers whose income structures tend to deviate from the traditional paycheck model. Many professionals in the tech industry receive a compensation package that blends base salary, performance bonuses, and stock options. While these elements can significantly enhance one’s overall earnings, they can also introduce complexity when applying for a mortgage. Lenders typically prefer consistent, easily verifiable income streams, and the variable nature of bonuses and stock options may not be straightforward for them to evaluate. Tech workers must understand how these components are viewed within the context of a mortgage application to present themselves more favorably to lenders.

To successfully navigate this intricate process, transparency and effective communication of your financial situation are essential. Clearly outlining how your compensation works—whether it involves detailing the history of bonus payments or the reliability of your stock options—will enable lenders to assess your capacity to repay a loan accurately. Proactively sharing this information not only builds trust but also positions you better for securing favorable mortgage terms. By educating yourself about how lenders evaluate diverse income streams and preparing the necessary documentation, you can mitigate some of the anxiety associated with the mortgage application process, making it a more manageable part of your journey toward homeownership.

To enhance the clarity of your application, it’s essential for tech professionals to provide thorough documentation that reflects their complete financial picture. This should include not just recent pay stubs and tax returns, but also detailed statements regarding stock options or other forms of variable income. Providing this comprehensive information helps eliminate ambiguity about your earning potential, enabling lenders to make informed decisions. By fortifying your application with clear and organized documentation, you can demystify your income sources and demonstrate your financial stability. This proactive approach not only strengthens your application but also paves the way for a smoother mortgage approval process, allowing you to focus more on finding your dream home rather than getting caught up in the complexities of mortgage lending.

Moreover, when tech workers prepare their documentation effectively, they can avoid the need for special concessions that may arise due to unconventional income streams typical within the tech industry. Lenders operate on established principles and preferences for clear, verifiable income, regardless of profession. Therefore, by being upfront and organized with their financial information, tech workers can expedite the mortgage approval process, allowing them to focus on finding their ideal home rather than navigating potential setbacks. In essence, anyone, including tech professionals, can secure a mortgage when they are well-prepared and present the right evidence of their income. This clarity not only fosters trust with lenders but also empowers applicants to take control of their home-buying journey.

In the world of personal finance, particularly when it comes to mortgages, there’s often a misconception that tech workers require unique processes or “special treatment.” This notion overlooks a fundamental truth: the mortgage process fundamentally relies on clear, accurate documentation and a standard understanding of income. Tech workers, like any other professionals, possess diverse income structures, including base salaries, bonuses, and equity compensation. However, it’s crucial that these elements are thoroughly documented and clearly presented to lenders. With the right structure in place, tech employees can demonstrate their financial viability to mortgage underwriters just as effectively as individuals in more traditional careers.

The key to navigating the mortgage process successfully lies in transparency and clarity. Tech workers should focus on providing comprehensive documentation, such as pay stubs, tax returns, and statements regarding stock options or other variable income. These documents help lenders understand the full scope of an applicant’s earning potential, eliminating any ambiguity that might arise from unconventional income sources common in the tech industry. By ensuring that their financial picture is clearly communicated, tech workers can expedite their mortgage approval process without the need for special concessions. In essence, the mortgage industry operates on established principles; thus, anyone—regardless of their profession—can secure a mortgage when they’re prepared and fully equipped with the right evidence of their income.

Seattle mortgage solutions for tech workers start with how income is counted

Lenders are required to document and calculate income in specific ways. That can feel rigid, but it is also predictable once you know what they are looking for.

For many W-2 tech employees, base salary is the easy part. RSUs, bonuses, commissions, and refreshers are where approvals get won or lost. Most lenders will not count variable income unless they can show it is likely to continue. In practice, that often means a two-year history, although there are exceptions depending on the investor guidelines and your overall profile.

RSUs are the most common pain point. Even if your vesting schedule is reliable, underwriters want evidence: vesting history, brokerage statements, and sometimes employer verification. Some lenders will average RSU income using a documented history of sales proceeds. Others may accept vested amounts without requiring you to sell, but they still need a consistent pattern.

The trade-off is speed vs. flexibility. The more complex the income, the more important it is to set expectations early: what can be counted now, what needs seasoning, and what can be used as assets instead of income.

RSUs: income, assets, or both?

There are two common ways RSUs get used in underwriting. The first is as income, which typically requires a paper trail showing regular vesting and a reasonable expectation it continues. The second is as assets, where vested shares (or cash proceeds from sales) strengthen reserves and may help with qualification in other ways.

Using RSUs as income can increase buying power, but it can also invite more scrutiny. If you are close to a debt-to-income limit, you may push for RSU income. If you are already well-qualified on base salary, using RSUs as assets often keeps things cleaner and can still make your offer more competitive because reserves matter.

Bonuses and sign-on packages

Bonuses and sign-on payments can sometimes be used, but lenders want consistency. A one-time sign-on bonus might not be counted as qualifying income even if it is large. However, it can still help as an asset for down payment, closing costs, or reserves.

If your compensation includes an annual bonus that has been paid for at least two years, it is more likely to be averaged and counted. If it is newer, a strong employment profile and clear documentation can still help, but it depends on the program.

The Seattle market demands speed and certainty

Seattle and the Eastside reward offers that look “clean” to a seller and listing agent. That is not only about purchase price. It is about the chance of closing on time with minimal surprises.

A few practical realities show up again and again:

Appraisal gaps can happen in fast-moving pockets of King County. If the appraisal comes in low, you may need to bring additional funds or renegotiate. This is where liquidity and reserves matter, and where a pre-underwritten approach can reduce stress.

Condos and townhomes can have HOA and project review requirements. Some buildings are straightforward. Others slow things down. If you are buying a condo in Seattle proper, assume the lender will need condo docs and plan for it early.

Jumbo loans are common in higher-priced neighborhoods. Jumbo underwriting can be more documentation-heavy, and rate pricing can change based on down payment, credit profile, and reserves.

A practical playbook for tech buyers (without overcomplicating it)

Navigating the tech landscape as a buyer can often feel overwhelming, especially with the rapid pace of innovation and an ever-growing range of solutions. A practical playbook for tech buyers streamlines this process by equipping you with actionable strategies to make informed decisions. The core of this playbook lies in understanding your organization’s specific needs, evaluating potential solutions against those requirements, and fostering clear communication with stakeholders. By creating a checklist that prioritizes essential features, budget constraints, and scalability, you significantly improve your chances of selecting the right technology for your business.

Navigating the tech landscape as a buyer can often feel overwhelming, particularly given the relentless pace of innovation and the expansive array of available solutions. Every day, new technologies emerge, promising to enhance efficiency, productivity, and overall business performance. However, without a structured approach, the process of selecting the right tech tools can lead to confusion and decision fatigue. A practical playbook for tech buyers is designed to ease this burden by equipping organizations with actionable strategies tailored to their unique contexts. By focusing on defining specific needs, assessing potential solutions, and engaging in transparent discussions with stakeholders, buyers can make informed decisions that align with their strategic goals.

At the heart of this playbook is the creation of a comprehensive checklist that prioritizes essential features, considers budget constraints, and evaluates scalability. This checklist not only streamlines the decision-making process but also ensures that buyers remain focused on their organization’s core objectives. By systematically comparing available technologies against pre-defined criteria, businesses can eliminate options that do not meet their requirements, ultimately narrowing down choices to those that truly enhance operations. Additionally, fostering open communication with all stakeholders involved helps to ensure alignment and minimizes the risk of costly missteps. In essence, harnessing these strategies can significantly improve your chances of selecting technology that not only meets immediate needs but also supports long-term growth and adaptability in an ever-evolving landscape.

At the heart of this playbook lies the creation of a comprehensive checklist designed to prioritize essential features, assess budget constraints, and evaluate scalability. This tailored checklist serves as a powerful tool to simplify the decision-making process for organizations navigating the complex landscape of technology solutions. By focusing on their core objectives, businesses can efficiently identify what truly matters in their search for new tools and systems. The systematic approach of comparing available technologies against these pre-defined criteria allows organizations to eliminate options that fail to meet their specific needs, thus narrowing down their choices to those solutions that genuinely enhance operational efficiency and productivity.

At the heart of this playbook lies a meticulously crafted checklist aimed at helping organizations prioritize essential features, assess budget constraints, and evaluate scalability. This comprehensive tool simplifies the often overwhelming decision-making process for businesses facing the intricate landscape of technology solutions. By laying out a structured framework, the checklist empowers organizations to focus on their core objectives, ensuring they identify and prioritize what’s most important when searching for new tools and systems. This targeted approach not only streamlines the research phase but also aligns technology selections with the specific needs of the organization.

At the heart of this playbook lies a meticulously crafted checklist aimed at helping organizations prioritize essential features, assess budget constraints, and evaluate scalability. In an era where the technology landscape is constantly evolving, businesses often find themselves overwhelmed with options that can seem both enticing and daunting. This comprehensive checklist serves as a reliable tool, guiding organizations through the maze of available technology solutions. By providing a structured framework that emphasizes clarity and focus, it allows teams to hone in on what is truly vital for their operations, minimizing the risk of getting sidetracked by superfluous features or unnecessary expenditures.

Moreover, this targeted approach not only streamlines the research phase but also ensures that technology selections align closely with the unique needs and objectives of the organization. By clearly laying out the features that matter most, organizations can avoid the common pitfalls of premature commitments to solutions that don’t fully serve their purpose. This process fosters informed decision-making, enabling companies to invest in tools that will genuinely enhance their productivity and efficiency. Ultimately, the checklist acts as an essential companion on the journey to finding the right technological fit, empowering organizations to make strategic choices that propel them toward their goals.

Moreover, the systematic comparison of available technologies against these pre-defined criteria enables businesses to effectively eliminate options that do not meet their requirements. By doing so, organizations can narrow down their choices to solutions that genuinely contribute to enhanced operational efficiency and productivity. This refined selection process not only saves time but also assists in making informed decisions, reducing the risk of costly missteps. Ultimately, the checklist serves as a vital resource for any organization seeking to navigate the complexities of technology choices, ensuring that their investments lead to sustainable growth and success.

In the ever-evolving landscape of technology, businesses face the daunting task of selecting the best solutions to enhance their operational efficiency and drive productivity. One effective strategy for navigating this complex decision-making process is the systematic comparison of available technologies against pre-defined criteria. This approach enables organizations to thoroughly evaluate potential options by establishing a clear set of requirements tailored to their specific needs. By doing so, companies can efficiently eliminate solutions that do not align with their goals, streamlining the selection process and ensuring that only the most suitable candidates remain under consideration.

Moreover, employing a refined checklist not only saves valuable time but also empowers business leaders to make informed decisions with greater confidence. By narrowing down options to those that have been critically assessed, organizations can significantly reduce the risk of costly missteps that often arise from hasty or uninformed choices. This disciplined approach fosters an environment where technology investments are more likely to yield sustainable growth and success, as businesses can rest assured that their investments are strategic and well-suited to their long-term objectives. Ultimately, a thorough checklist acts as an indispensable resource for organizations navigating the complexities of technology selection, transforming potential confusion into clarity and ensuring a more effective alignment between technology and operational goals.

In today’s fast-paced business environment, technology selection can often feel overwhelming due to the sheer volume of options available. This is where a well-crafted and refined checklist becomes a valuable asset for business leaders. By utilizing such a tool, organizations can streamline their decision-making processes, saving crucial time that can be better spent on strategic initiatives. A checklist allows leaders to focus on key criteria, providing a structured framework for evaluating technology alternatives. This critical assessment not only narrows down the options but also enhances confidence in the final decisions being made, ensuring that they are rooted in thoughtful analysis rather than hasty reactions.

Moreover, this disciplined approach significantly minimizes the risk of costly missteps that might occur from poorly informed decisions. By thoughtfully considering each criterion laid out in the checklist, organizations can make investments that are far more aligned with their long-term objectives. This alignment transforms the often chaotic selection process into a more organized and strategic endeavor, ultimately leading to technology choices that support sustainable growth and success. When business leaders leverage a thorough checklist, they can navigate the complexities of technology selection with clarity and precision, paving the way for more effective integration of technology with operational goals and ensuring that each investment contributes meaningfully to the organization’s future.

Moreover, fostering open communication among all stakeholders is crucial for aligning expectations and ensuring that everyone involved is on the same page. This collaborative approach minimizes the risk of costly missteps that can arise from misunderstandings or misalignments in priorities. By actively involving team members from various departments, businesses can gather diverse insights that refine the checklist further and enhance the overall decision-making process. Ultimately, harnessing these strategies significantly increases the likelihood of selecting technology that not only addresses immediate requirements but also supports long-term growth and adaptability in today’s rapidly evolving business environment. Through a thoughtful and organized evaluation, organizations can position themselves to thrive in an era characterized by constant change and innovation.

In addition to a structured approach, it’s crucial to engage with trusted vendors and seek feedback from peers who have faced similar challenges. Building a network of insights can often reveal nuances about product performance and user experience that isn’t readily available through marketing materials alone. Furthermore, consider setting up trial periods or demos to test how well a solution fits within your existing ecosystem. This hands-on experience not only helps in understanding the effectiveness of a product but also aids in garnering buy-in from teams who will ultimately use the technology. By implementing these practical steps, you can ensure a more efficient and effective purchasing process that aligns with your organization’s goals.

Most tech professionals do well with a simple strategy: prove stability, keep documentation tight, and build an offer that closes.

Start by separating what you want from what you can safely commit to. Seattle buyers often feel pressure to “stretch” because everyone else is. The better approach is to define a payment range that still works if your stock price drops, your bonus is smaller than expected, or you decide to change roles.

Next, get your documentation organized earlier than you think you need it. If RSUs are part of your plan, that means brokerage statements and vesting history. If you have multiple income streams, expect the lender to ask follow-up questions. This is normal, not a sign something is wrong.

Finally, choose the right loan structure for your timeline. If you are writing offers now, you want a path that supports a fast close. If you are six months out, you may have time to optimize credit, build reserves, or let variable income “season” so it can be counted.

Down payment strategy: it depends, and that is fine

There is no single correct down payment in Seattle. Some buyers want to minimize monthly payment and bring more down. Others prefer to keep liquidity because they are using cash to cover an appraisal gap, fund renovations, or preserve flexibility.

A larger down payment can improve rate pricing and reduce or eliminate mortgage insurance. But putting too much down can leave you cash-tight in a market where surprises happen. Underwriters also like to see post-close reserves, especially on jumbo loans.

If you are deciding between, say, 10% and 20% down, the right answer often comes down to your reserves after closing, how volatile your variable comp is, and whether you might need cash for a gap or repairs.

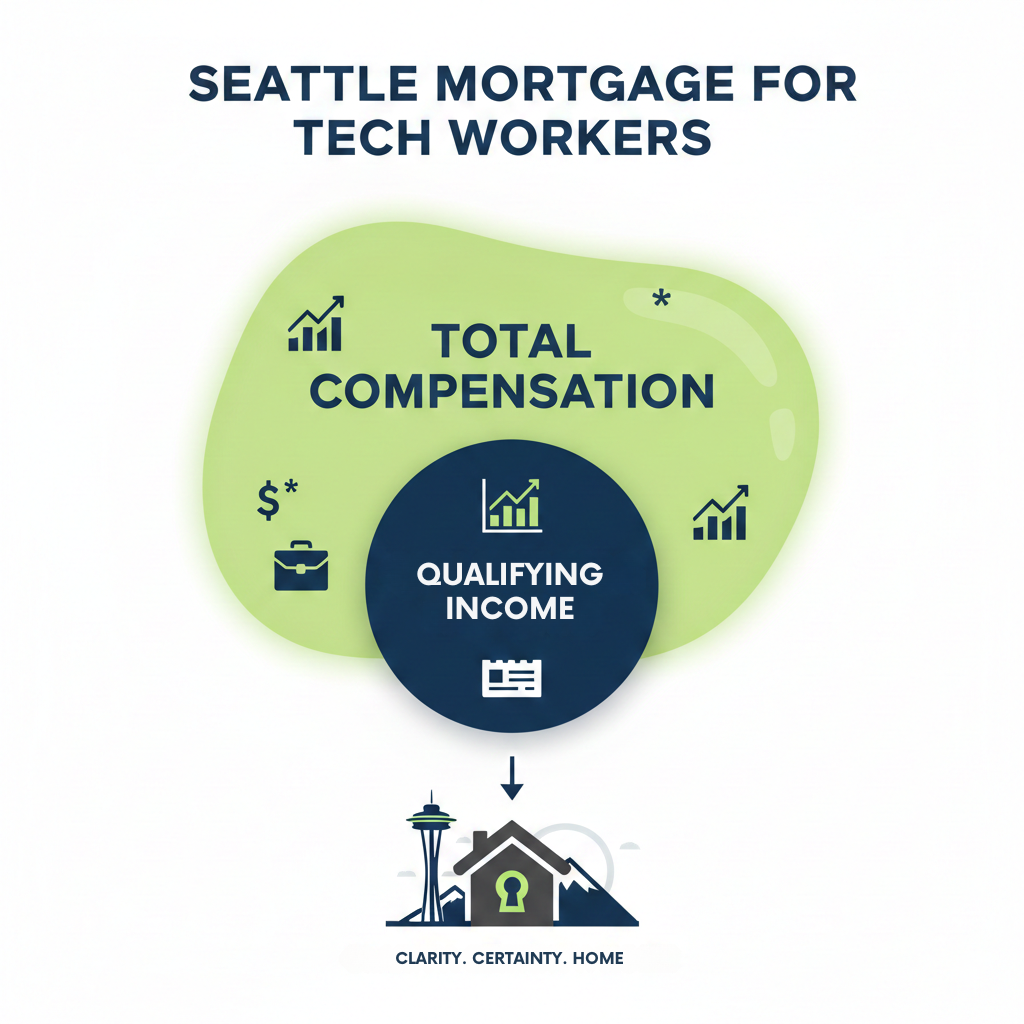

DTI for tech workers: your “real” income is not always the qualifying income

Debt-to-income ratio is calculated using qualifying income, not projected income. If your base salary qualifies you comfortably, you have leverage. If you are counting variable income to qualify, you need documentation that meets guidelines.

On the debt side, student loans, car payments, and credit card minimums all count. If you are close to a limit, small moves can matter. Paying off a monthly debt can improve DTI immediately. Paying down a credit card can help both utilization and monthly obligations if the minimum payment changes.

Loan options that show up most for Seattle and Bellevue tech buyers

Tech professionals in this area tend to land in a few loan categories, and each has a different “best use” case.

Conventional loans are common for primary residences and can work well with a variety of down payments. They are generally straightforward if your income is clean and your purchase fits within conforming limits.

Jumbo loans come into play when prices push above conforming loan limits, which is frequent in many Seattle and Eastside neighborhoods. Jumbo guidelines vary by lender. Some are flexible with assets and reserves, while others are strict about income documentation.

FHA can be a strong option for some first-time buyers, especially if credit history is thinner, but it comes with mortgage insurance rules that may be less attractive at higher price points. In Seattle, FHA is less common for higher-priced homes but can still be useful depending on the purchase and the borrower.

VA loans are powerful for eligible veterans and service members. They can offer competitive terms and often allow zero down. In a competitive market, the key is presenting the offer cleanly and working with a lender who closes VA efficiently.

The point is not that one program is “best.” The point is choosing the program that matches your profile and the property type you are targeting.

Case study: using RSUs without turning the loan into a science project

A recent buyer I worked with (Seattle-based, W-2 at a large tech employer) had strong base income but wanted to push purchasing power using RSUs. The challenge was that the RSUs were meaningful, but the vesting history was shorter than two full years due to a job change.

We treated the RSUs primarily as assets for reserves and down payment flexibility, and we qualified conservatively on base salary plus documented bonus history. That kept underwriting clean and protected the timeline. When an appraisal came in slightly under contract price, the buyer had the liquidity to bridge the gap without panic selling shares at a bad time.

The win was not “maxing out” what the guidelines allowed. It was structuring the loan so the buyer could close fast and still sleep at night if the market moved.

What sellers and listing agents look for in Seattle offers

In many Seattle transactions, the listing agent is quietly evaluating your lender as much as your price. They want to know if the loan is likely to close on time and whether the preapproval is solid.

A strong preapproval is specific, documented, and based on a real review of your profile. If your file involves RSUs, bonuses, or a jumbo scenario, you want the preapproval to reflect that reality. The goal is not to impress anyone with complexity. The goal is to remove uncertainty.

This is also where communication matters. Fast responses, clear documentation requests, and an underwriting plan can make the difference when timelines are tight.

If you want guidance from a broker who works with Seattle-area tech compensation every week, The Mortgage Reel is built around transparent education and fast closings, especially for buyers using RSUs and stock-based pay.

The most common mistakes tech buyers make (and how to avoid them)

One is assuming that a high total compensation number automatically qualifies. Underwriting is about documented, ongoing income and verified assets. If you plan to use RSUs, start documenting early.

Another is moving money around late in the process. Large transfers between accounts can create extra conditions because the lender has to source funds. If you are selling stock for down payment, plan the timing and paper trail so it is easy to document.

The third is optimizing for rate while ignoring execution. A slightly lower rate is not worth it if the lender cannot handle jumbo guidelines, condo reviews, or variable income quickly. In Seattle, the ability to close on time is part of your leverage.

A home purchase here is already demanding. The right mortgage strategy should reduce friction, not add to it. If you build your plan around stable qualifying income, clear documentation, and reserves that protect you from surprises, you can compete confidently without betting your future on a stock chart.

Key Takeaways

- Tech workers face challenges in mortgage applications due to complex income structures like RSUs and bonuses.

- Documentation is crucial; providing clear and comprehensive records helps lenders assess income effectively.

- Understanding how lenders view RSUs and variable income is vital for securing favorable mortgage terms.

- In Seattle’s competitive market, a clean and accurate preapproval can enhance chances of closing successfully.

- Avoid common mistakes like assuming total compensation qualifies; focus on clear documentation and stable income for a smoother mortgage process.

Estimated reading time: 20 minutes