When purchasing a home in Seattle, Bellevue, or surrounding areas, most buyers will encounter a conventional mortgage as their primary financing option. Unlike government-backed loans such as FHA or VA mortgages, a conventional mortgage is issued by private lenders and follows guidelines established by Fannie Mae and Freddie Mac. Understanding how these loans work, what qualifications you need, and how to maximize your approval odds can make the difference between securing your dream home in a competitive market or watching opportunities pass by. For tech professionals earning stock compensation at Amazon, Microsoft, or Google, conventional loans offer flexibility that aligns particularly well with higher incomes and larger down payment capabilities.

What Defines a Conventional Mortgage

A conventional mortgage represents any home loan not guaranteed or insured by a federal government agency. The Consumer Financial Protection Bureau provides comprehensive guidance on these loan products, which account for the majority of home purchases nationwide. According to the National Association of Realtors, conventional loans represent over 70% of home financing transactions.

These mortgages come in two main categories: conforming and non-conforming loans. Conforming conventional loans meet the standards set by Fannie Mae and Freddie Mac, including maximum loan limits that adjust annually based on regional housing costs. For 2026, the conforming loan limit in King County stands at $806,500 for single-family homes, reflecting Seattle's status as a high-cost area.

Non-conforming loans, commonly called jumbo mortgages, exceed these limits and typically require stronger financial qualifications. In Seattle's housing market where median home prices frequently surpass conforming limits, many buyers in neighborhoods like Ballard, Queen Anne, and Capitol Hill need jumbo loan options to complete their purchases.

Credit Score and Financial Requirements

Conventional mortgage qualification begins with your credit profile. Most lenders require a minimum credit score of 620, though better rates and terms become available at 680 and above. The strongest pricing typically appears at 740 or higher.

Key credit considerations include:

- Payment history across all credit accounts

- Credit utilization ratios below 30%

- Length of established credit history

- Recent credit inquiries and new accounts

- Public records such as bankruptcies or foreclosures

Beyond credit scores, debt-to-income ratios play a crucial role. Lenders typically limit your total monthly debt payments, including your proposed mortgage, to 43-45% of your gross monthly income. For Seattle tech professionals with complex compensation packages, this calculation requires careful documentation of base salary, RSUs, bonuses, and stock compensation.

Employment stability matters significantly. Most conventional loans require two years of consistent employment history in the same field. However, recent graduates from technical programs who immediately enter high-paying roles at companies like Amazon or Microsoft may qualify with less history when their income trajectory demonstrates strong stability.

| Credit Score Range | Typical Rate Impact | PMI Cost Impact | Approval Likelihood |

|---|---|---|---|

| 620-659 | Higher rates | Highest PMI | Possible with strong compensating factors |

| 660-699 | Moderate rates | Moderate PMI | Good with adequate reserves |

| 700-739 | Competitive rates | Lower PMI | Very good across most programs |

| 740+ | Best rates | Lowest PMI | Excellent with standard qualifications |

Down Payment Options and Private Mortgage Insurance

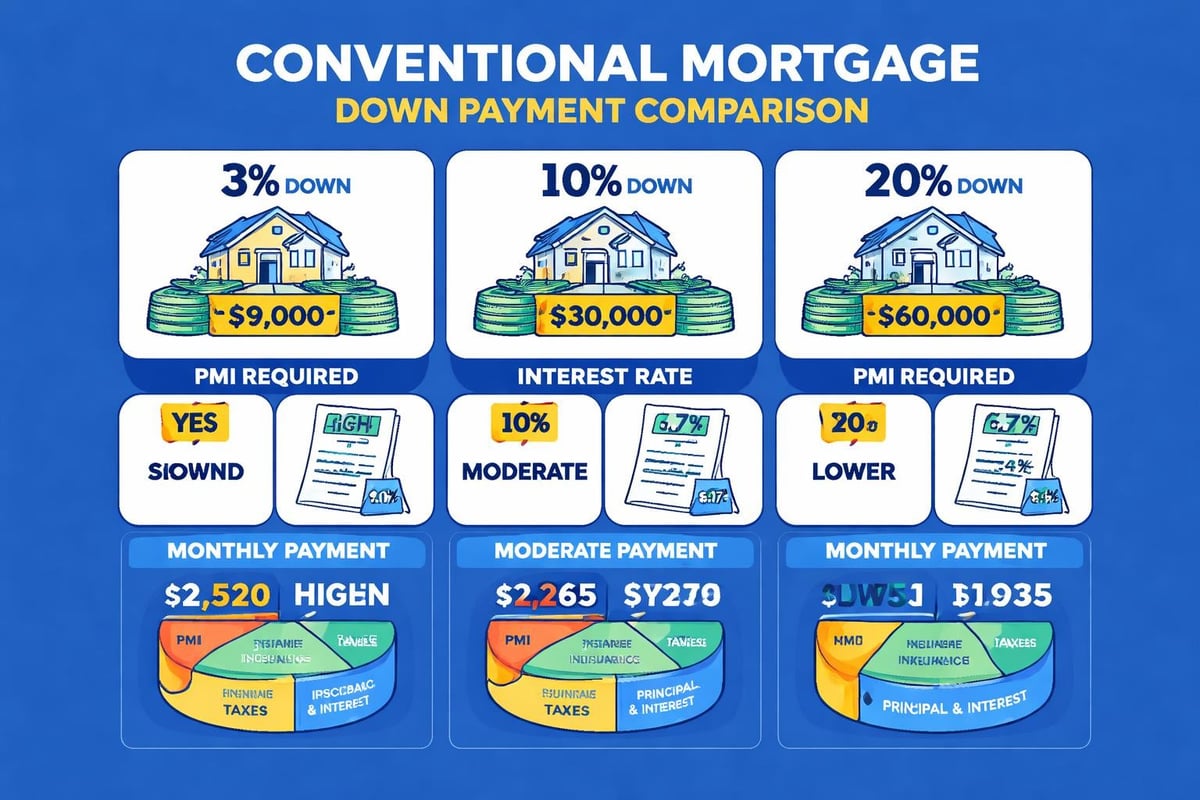

One of the defining characteristics of conventional mortgages involves down payment flexibility. While many buyers believe 20% down represents a requirement, conventional loans actually accept down payments as low as 3% for qualified first-time homebuyers.

Down payment tiers directly impact your loan structure:

- 3-5% down: Available for primary residences with higher interest rates and mandatory private mortgage insurance (PMI)

- 10-15% down: Moderate PMI costs with improved rate options

- 20% or more: Eliminates PMI requirement and unlocks best pricing

Private mortgage insurance protects the lender if you default on the loan. Unlike FHA mortgage insurance that persists for the loan's life, conventional PMI can be removed once you reach 20% equity through payments or property appreciation. In Seattle's historically appreciating market, buyers in neighborhoods like Shoreline, Lynnwood, and Lake Forest Park often build equity quickly enough to cancel PMI within a few years.

For buyers considering smaller down payments, understanding PMI costs proves essential. Monthly PMI typically ranges from 0.3% to 1.5% of the original loan amount annually, divided across twelve monthly payments. On a $600,000 loan with 5% down, expect PMI between $150 and $750 monthly depending on your credit profile.

Income Documentation and Verification Standards

Conventional mortgages require thorough income documentation, particularly for self-employed borrowers or those with variable compensation. The verification process ensures you can reliably afford your monthly payments over the long term.

Standard W-2 employees typically provide:

- Two years of W-2 statements

- Recent pay stubs covering 30 days

- Two years of tax returns (if claiming additional income)

- Verification of Employment (VOE) from employer

For Seattle's substantial population of tech workers earning significant stock compensation, qualifying income extends beyond base salary. Restricted stock units (RSUs), employee stock purchase programs (ESPP), and performance bonuses can all count toward qualifying income when properly documented and averaged over time.

Self-employed borrowers face additional scrutiny. Lenders typically average two years of tax returns, adding back non-cash deductions like depreciation while subtracting business expenses. This calculation often results in a qualifying income lower than actual cash flow, making advance tax planning essential for entrepreneurs and small business owners in Mill Creek, Everett, and surrounding communities.

The FDIC provides valuable resources for understanding mortgage qualification standards across different employment types. Working with an experienced broker helps navigate complex income scenarios and maximize your qualifying power.

Asset Verification and Reserve Requirements

Beyond income, conventional mortgage underwriting examines your liquid assets. Lenders verify you have sufficient funds for your down payment, closing costs, and cash reserves after the transaction completes.

Source of funds documentation proves critical. Lenders track large deposits appearing in your bank accounts during the application period. Acceptable sources include:

- Regular payroll deposits

- Sale of investments or property

- Gift funds from family members (with proper documentation)

- Tax refunds and bonuses

- Retirement account withdrawals (with considerations for taxes and penalties)

Reserve requirements vary by loan amount and property type. Most conventional mortgages for primary residences require two to six months of housing payment reserves after closing. Investment properties and higher loan amounts demand more substantial reserves, sometimes extending to twelve months or beyond.

For tech professionals with significant assets held in RSUs or stock options, converting some equity to liquid reserves before applying strengthens your application. While unvested RSUs may support income calculations, lenders prefer seeing accessible funds in checking, savings, or investment accounts when evaluating reserves.

Property Type and Appraisal Considerations

Conventional mortgages finance various property types, each with specific guidelines. Single-family homes receive the most favorable terms, while condominiums, multi-unit properties, and manufactured homes face additional scrutiny.

Property eligibility factors include:

- Occupancy status (primary residence, second home, investment)

- Number of units (one to four units qualify)

- Condominium project approval status

- Property condition and safety standards

- Comparable sales supporting appraised value

Seattle's competitive market creates unique appraisal challenges. Properties in desirable neighborhoods may receive multiple offers above asking price, but the appraised value ultimately determines your maximum loan amount. If your contract price exceeds the appraisal, you'll need to either negotiate a lower price, increase your down payment to cover the gap, or walk away using your appraisal contingency.

Working with a knowledgeable Seattle mortgage broker helps identify potential appraisal issues before they derail your transaction. Understanding comparable sales, recent market trends, and appraiser tendencies in specific neighborhoods provides strategic advantages.

Interest Rates and Points Strategy

Conventional mortgage rates fluctuate based on economic conditions, Federal Reserve policy, and individual borrower qualifications. Unlike government loans with set fee structures, conventional rates vary significantly between lenders and loan programs.

Your specific rate depends on multiple factors:

- Credit score and credit history depth

- Loan-to-value ratio (down payment size)

- Property type and occupancy

- Loan term (15-year versus 30-year)

- Current market conditions and treasury yields

- Lender pricing and profit margins

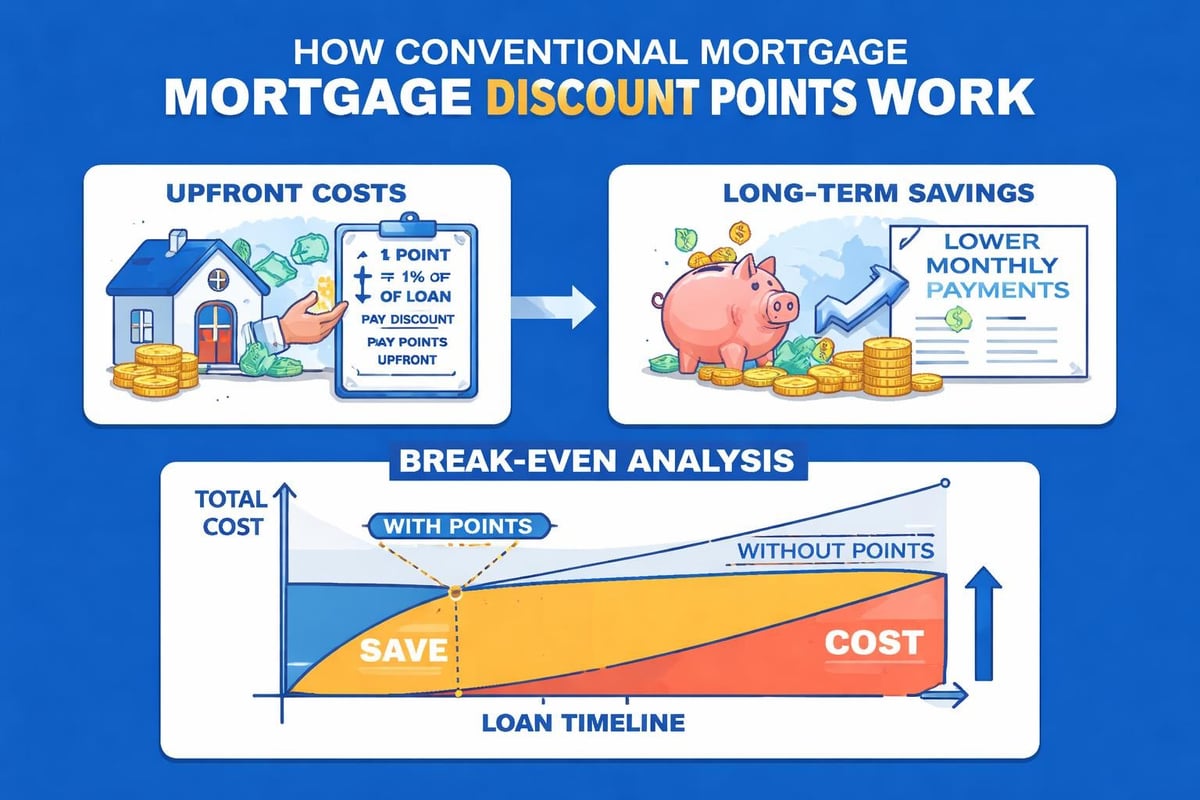

Points represent an option to pay upfront fees in exchange for a lower interest rate. One point equals 1% of your loan amount. On a $500,000 loan, one point costs $5,000. Whether paying points makes financial sense depends on how long you plan to keep the loan and your available cash.

Calculate your break-even point by dividing the point cost by your monthly payment savings. If one point saves you $150 monthly, your break-even occurs at approximately 33 months. If you plan to keep the loan longer, points provide value. For shorter timelines or potential refinancing scenarios, avoiding points preserves your cash for other uses.

Monitoring Seattle mortgage rates helps you understand current market conditions and identify optimal timing for rate locks. In volatile markets, locking your rate early protects against increases during your closing timeline.

Conventional Versus Government-Backed Loans

Understanding when a conventional mortgage makes sense requires comparing alternatives. FHA, VA, and USDA loans each serve specific purposes and borrower profiles.

| Loan Type | Minimum Down Payment | Credit Score Requirement | Mortgage Insurance | Property Restrictions |

|---|---|---|---|---|

| Conventional | 3-5% | 620+ typical | Removable at 20% equity | Minimal |

| FHA | 3.5% | 580+ | Permanent for life of loan | Stricter appraisal standards |

| VA | 0% | No minimum | None | Must meet VA eligibility |

| USDA | 0% | 640+ typical | Annual fee | Rural areas only |

Conventional mortgages typically benefit borrowers with:

- Credit scores above 680

- Ability to make down payments of 5% or more

- Income supporting lower debt-to-income ratios

- Plans to build equity and remove PMI

- Properties in urban or suburban areas

The Consumer Financial Protection Bureau offers detailed mortgage resources comparing loan types and helping borrowers identify the best fit for their situation. In Seattle's higher-priced market, conventional loans often provide the only realistic path for properties exceeding FHA loan limits.

Refinancing With Conventional Loans

Existing homeowners frequently use conventional mortgages to refinance out of higher-rate loans or tap home equity. Refinancing follows similar qualification standards as purchase loans but evaluates your current property value and equity position.

Common refinance scenarios include:

- Rate and term refinance: Lowering your interest rate or changing loan duration

- Cash-out refinance: Accessing equity for renovations, debt consolidation, or investments

- Removing PMI: Refinancing once equity reaches 20% to eliminate mortgage insurance

- Consolidating second mortgages: Combining first and second liens into one loan

Seattle homeowners who purchased several years ago often hold substantial equity due to market appreciation. This equity position enables favorable refinancing terms and access to competitive rates. Before refinancing, calculate your break-even point considering closing costs, which typically range from 2-5% of the loan amount.

The Seattle refinance landscape shifts with interest rate cycles. When rates drop significantly below your current mortgage rate, refinancing may reduce your monthly payment substantially or shorten your loan term without increasing payments.

Special Considerations for Tech Professionals

Seattle's concentration of technology employers creates unique opportunities and challenges for conventional mortgage qualification. Understanding how lenders evaluate stock compensation, equity grants, and variable bonuses helps tech workers maximize their buying power.

RSU and stock compensation strategies:

- Lenders typically average RSU income over two years of vesting history

- Unvested shares may count toward income with proper documentation

- Stock price volatility requires conservative underwriting approaches

- Exercise and sale timing affects your qualifying income

For employees at Amazon, Microsoft, Google, and similar companies, working with a mortgage professional experienced in tech compensation proves essential. Properly documenting equity compensation can increase your qualifying income by tens or hundreds of thousands of dollars, dramatically expanding your home search parameters.

Sign-on bonuses and relocation packages also factor into the equation. While one-time bonuses don't count as recurring income, they can strengthen your reserve position and fund larger down payments. Some relocation packages include employer assistance with closing costs, which requires specific documentation to satisfy underwriting guidelines.

Common Qualification Challenges and Solutions

Even qualified buyers encounter obstacles during the conventional mortgage process. Recognizing potential issues early allows time to implement solutions before they impact your closing timeline.

Frequent challenges include:

- Recent job changes within the same industry

- Self-employment income declining between tax years

- Large deposits lacking clear documentation

- Credit inquiries from shopping multiple lenders

- Gift funds received without proper paperwork

Address these issues proactively. If you changed jobs recently, obtain a detailed offer letter and explain the career progression. For self-employment income fluctuations, prepare a written explanation with supporting business documentation. Always communicate large deposits to your lender immediately, providing source documentation before they request it.

Some buyers discover mid-process that their debt-to-income ratio exceeds lender limits. Solutions include paying down existing debts, increasing your down payment to lower the loan amount, or documenting additional income sources previously excluded from calculations.

Timeline and Closing Process

Understanding the conventional mortgage timeline helps you coordinate with sellers, real estate agents, and other transaction parties. While every loan varies, expect a typical 21-30 day process from application to closing.

Standard timeline milestones:

- Pre-approval (1-2 days): Initial credit and income review

- Loan application (immediately after offer acceptance): Complete documentation submission

- Processing (3-5 days): Document verification and initial underwriting review

- Appraisal ordered (within 1 week): Property valuation begins

- Underwriting (7-10 days): Detailed file review and conditional approval

- Clear to close (2-3 days before closing): Final approval issued

- Closing (scheduled date): Sign documents and receive keys

In Seattle's competitive market where sellers often favor faster closings, working with lenders offering expedited timelines provides strategic advantages. Some lenders can close conventional loans in as few as 9-15 business days when borrowers submit complete documentation promptly and properties appraise without complications.

Stay responsive throughout the process. Underwriters frequently request additional documentation or clarification on specific items. Quick responses to these requests prevent delays and demonstrate your reliability to all transaction parties.

Working With a Mortgage Professional

Navigating conventional mortgage requirements, comparing lender offerings, and optimizing your qualification strategy requires expertise. While online lenders offer convenience, working with a local mortgage broker provides personalized guidance tailored to Seattle's unique market conditions.

An experienced broker offers distinct advantages:

- Access to multiple lenders and loan programs through one application

- Knowledge of local appraisal trends and property qualification issues

- Relationships with underwriters enabling faster problem resolution

- Strategic advice on timing, rate locks, and documentation

- Advocacy throughout the process protecting your interests

Before selecting a mortgage professional, review their credentials, client testimonials, and track record. Look for someone with extensive experience in your specific property type, loan amount, and financial situation. For buyers pursuing properties in competitive neighborhoods throughout Bellevview, Redmond, and Kirkland, local expertise proves invaluable.

The FDIC’s affordable mortgage lending guide provides additional context on selecting mortgage products and working with lending professionals. This federal resource complements the personalized guidance a qualified broker delivers.

Understanding conventional mortgage requirements positions you to move confidently in Seattle's competitive real estate market. Whether you're purchasing your first home, upgrading to accommodate a growing family, or investing in rental property, conventional financing offers flexible terms that adapt to your specific situation. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle-area buyers navigate complex qualification scenarios, maximize stock compensation income, and close quickly even in challenging markets. With 750+ five-star reviews and specialized expertise serving tech professionals, we're ready to develop a financing strategy tailored to your goals.