Purchasing your first home represents one of the most significant financial decisions you'll make in your lifetime. For first time home buyers navigating the Seattle housing market in 2026, understanding mortgage options, qualification requirements, and strategic planning can make the difference between competing successfully and watching opportunities pass by. This comprehensive guide breaks down everything you need to know about entering the Greater Seattle real estate market, from Everett to Bellevue, with confidence and clear direction.

Understanding Your Mortgage Options as a First Time Buyer

The mortgage landscape offers several distinct pathways for first time home buyers, each with unique advantages depending on your financial situation, employment structure, and long-term goals. Making an informed decision starts with understanding how each loan type functions.

Conventional Loans: The Foundation of Seattle Home Buying

Conventional mortgages remain the most popular choice for buyers with stable income and solid credit profiles. These loans aren't backed by government agencies, which means lenders assume more risk and typically require higher credit standards.

Key conventional loan features include:

- Down payments as low as 3% for qualified first time home buyers

- Competitive interest rates for borrowers with credit scores above 680

- Private mortgage insurance (PMI) required when putting down less than 20%

- Flexibility in property types, including condos common in Seattle neighborhoods

- Ability to remove PMI once you reach 20% equity

For tech professionals in Seattle, Bellevue, and Redmond, conventional mortgages offer the flexibility to qualify using restricted stock units (RSUs) and bonus income, which significantly increases purchasing power in competitive markets.

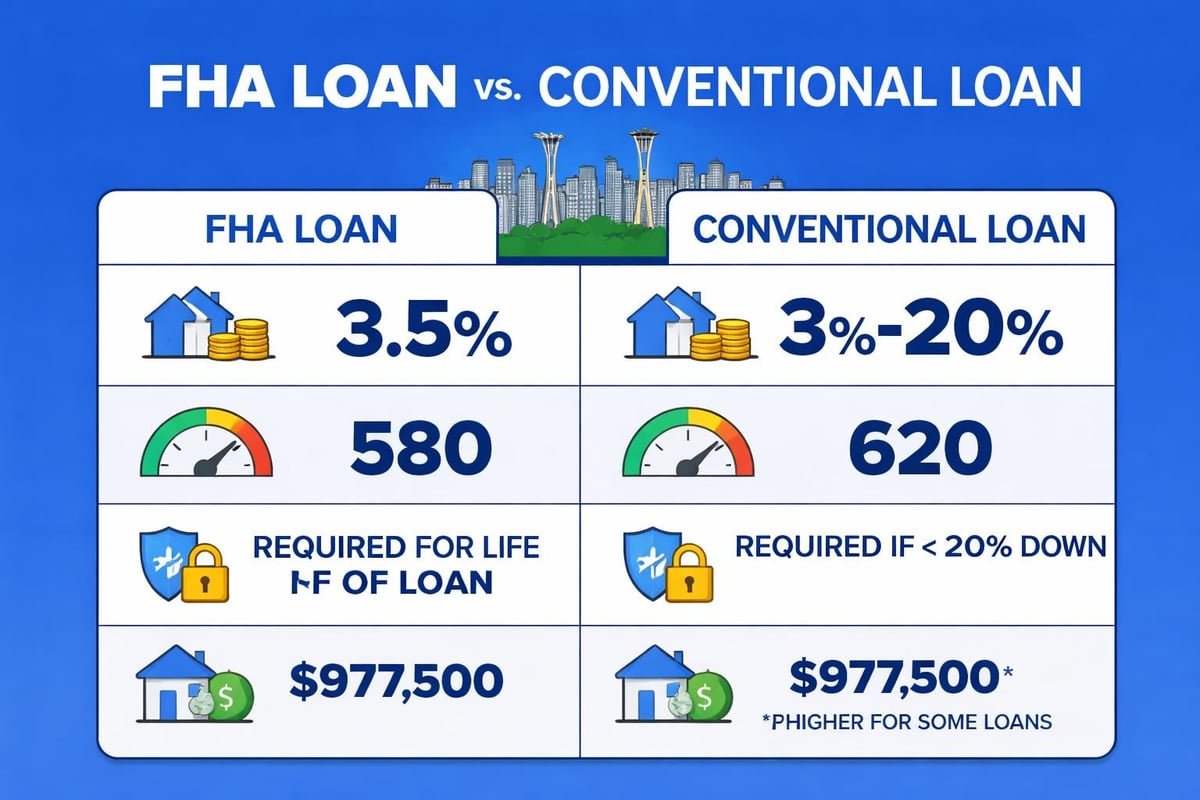

FHA Loans: Accessible Entry Points

Federal Housing Administration loans serve as an excellent option for first time home buyers who may have lower credit scores or limited down payment funds. The FHA program requires just 3.5% down for borrowers with credit scores of 580 or higher.

However, FHA loans come with mortgage insurance for the life of the loan unless you refinance, and they have loan limits that may restrict options in higher-priced Seattle neighborhoods. In King County, the 2026 FHA loan limit is $1,089,300 for single-family homes.

VA Loans: Zero Down for Veterans

For eligible veterans and active-duty service members, VA loans provide exceptional benefits including zero down payment requirements, no private mortgage insurance, and competitive interest rates. These loans work particularly well in markets like Mill Creek and Lynnwood where home prices may stretch conventional budgets.

USDA Loans: Rural and Suburban Opportunities

While Seattle proper doesn't qualify, certain areas in Snohomish County may be eligible for USDA loans offering zero down payment for income-qualified buyers in designated rural areas.

Financial Preparation and Qualification Requirements

Success as a first time home buyer depends heavily on financial preparation well before you start house hunting. Understanding what lenders evaluate helps you strengthen your position and negotiate better terms.

Credit Score Impact on Mortgage Rates

Your credit score directly influences both your qualification chances and the interest rate you'll receive. Here's how different score ranges typically affect your options:

| Credit Score Range | Loan Options | Expected Rate Impact |

|---|---|---|

| 760+ | All programs, best rates | Lowest available rates |

| 700-759 | All programs, good rates | Slightly above best rates |

| 660-699 | Most programs available | Moderate rate adjustment |

| 620-659 | Limited to FHA, some conventional | Higher rates, larger down payment |

| Below 620 | FHA only, manual underwriting | Highest rates, 10%+ down required |

For first time home buyers working to improve credit before applying, focus on paying down credit card balances below 30% of limits, addressing any late payments, and avoiding new credit inquiries in the six months before application.

Down Payment Strategies and Assistance Programs

The down payment requirement often presents the biggest hurdle for first time home buyers. Washington State and local municipalities offer several assistance programs worth exploring.

Washington State Housing Finance Commission provides down payment assistance loans up to $100,000 for qualified buyers. These programs often come with income limits and homebuyer education requirements but can make homeownership accessible years earlier than saving independently.

Seattle Office of Housing administers programs specifically for city residents, with particularly favorable terms for educators, healthcare workers, and public service employees. Similar programs exist in Shoreline and Lake Forest Park, tailored to local workforce needs.

Beyond government programs, first time home buyers should consider:

- Gift funds from family members (properly documented)

- Employer assistance programs (common at Microsoft and Amazon)

- IRA withdrawals up to $10,000 penalty-free for first homes

- Selling investments or reallocating portfolios strategically

According to NerdWallet’s first-time homebuyer resources, many buyers underestimate closing costs, which typically run 2-5% of the purchase price in Washington State.

Debt-to-Income Ratio Calculations

Lenders evaluate your debt-to-income (DTI) ratio to determine how much house you can afford. This calculation divides your total monthly debt payments by your gross monthly income.

Most conventional loans allow DTI ratios up to 45%, though stronger applications typically stay below 43%. For first time home buyers with student loans, understanding how lenders calculate those payments matters significantly-income-driven repayment plans can help lower your calculated DTI.

Navigating the Seattle Housing Market

The Greater Seattle area presents unique challenges and opportunities for first time home buyers in 2026. Understanding local market dynamics helps you compete effectively and make strategic decisions.

Neighborhood Selection and Affordability Trade-offs

Seattle's neighborhoods vary dramatically in price, commute times, and lifestyle offerings. First time home buyers often find better value by expanding their search beyond central Seattle to areas like Everett, Lynnwood, and Mill Creek.

Typical price ranges by area (2026):

- Seattle (Capitol Hill, Fremont, Ballard): $650,000-$950,000

- Bellevue/Redmond: $700,000-$1,200,000

- Shoreline/Lake Forest Park: $550,000-$800,000

- Lynnwood/Mill Creek: $475,000-$675,000

- Everett: $400,000-$600,000

Working with buyers across these markets reveals that commute tolerance and remote work flexibility significantly impact optimal neighborhood selection. Tech professionals with hybrid schedules increasingly prioritize home features over proximity to downtown offices.

Multiple Offer Strategies

Seattle's competitive market frequently generates multiple offer situations, especially for well-priced properties in desirable neighborhoods. First time home buyers need strategic approaches to compete against cash buyers and seasoned investors.

Effective competitive strategies include:

- Pre-approval letters with verified income documentation

- Flexibility on closing timelines to match seller needs

- Pre-inspection contingencies to shorten due diligence periods

- Escalation clauses with clear caps and terms

- Personal letters (where legally appropriate and effective)

Strong pre-approval documentation matters immensely. When sellers receive multiple offers, knowing a buyer has verified employment, income, and assets through full underwriting review provides confidence that distinguishes your offer from generic pre-qualification letters.

Qualification Considerations for Tech Professionals

Seattle's concentration of technology employers creates unique qualification opportunities for first time home buyers earning significant portions of their compensation through equity and bonuses.

RSU and Stock Compensation Income

Most conventional guidelines allow lenders to use restricted stock unit income after establishing a two-year history of receiving equity compensation. The calculation typically averages the most recent two years of RSU vesting, with adjustments for granted but unvested shares.

For first time home buyers at Amazon, Microsoft, or Google, this often adds $50,000-$150,000 in qualifying income beyond base salary, significantly expanding buying power. Proper documentation including grant agreements, vesting schedules, and historical tax returns enables accurate income calculations.

Bonus Income Documentation

Annual bonuses become usable income once you demonstrate a two-year history. Lenders average the bonus amounts and may use a conservative calculation if bonuses fluctuate significantly year to year.

Sign-on bonuses typically don't qualify as ongoing income, though they can fund down payments and reserves. Understanding these distinctions helps first time home buyers set realistic budgets rather than overextending based on one-time compensation events.

Jumbo Loan Considerations

When home prices exceed conventional loan limits ($806,500 for most of King County in 2026), buyers need jumbo financing. These loans require stronger credit profiles, larger reserves, and more documentation, but rates remain competitive for qualified borrowers.

First time home buyers pursuing jumbo loans should expect:

- Credit scores above 700 (ideally 740+)

- 10-20% down payment requirements

- 6-12 months of reserves (mortgage payments, taxes, insurance)

- Full income and asset documentation with no exceptions

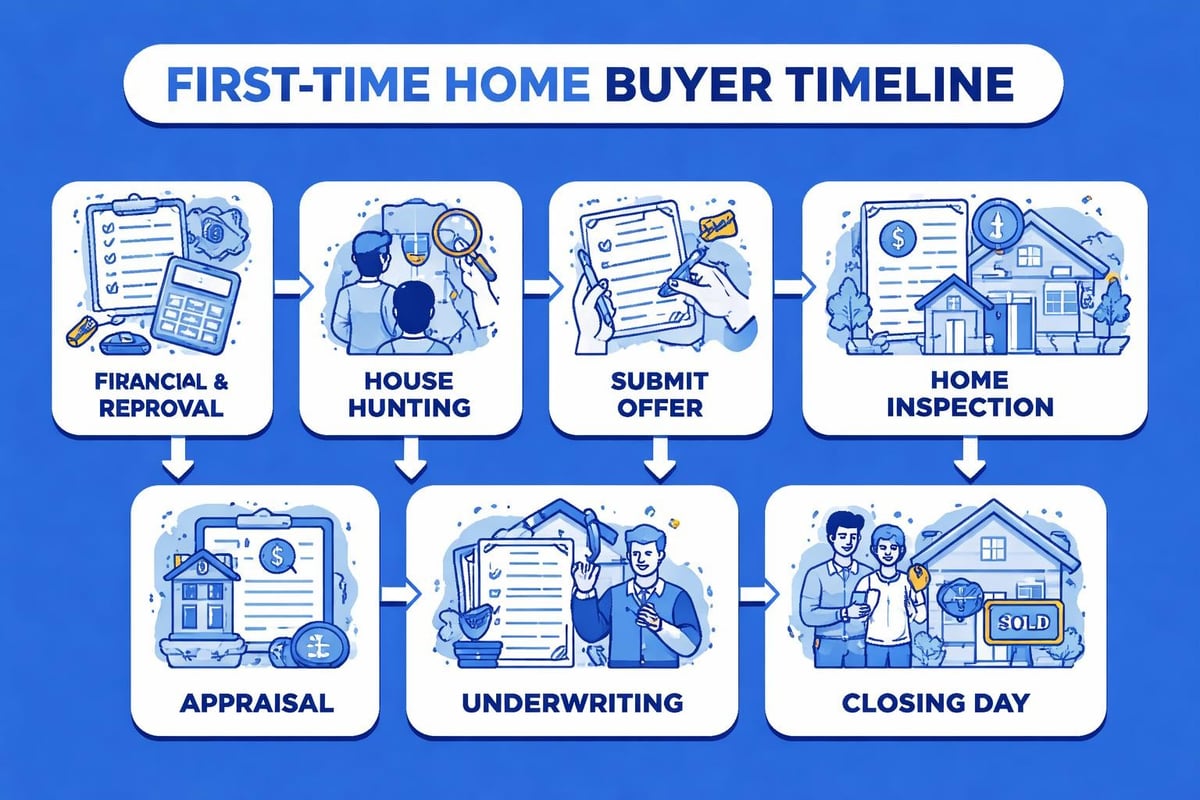

The Pre-Approval and Application Process

Understanding the mortgage application timeline prevents surprises and helps first time home buyers plan their search effectively. The process involves several distinct phases, each requiring different documentation and attention.

Initial Pre-Approval Steps

Pre-approval begins with a detailed financial review including credit report analysis, income verification, and asset documentation. For employed borrowers, this typically means providing:

- Most recent two years of W-2s and tax returns

- Recent pay stubs covering 30 days

- Two months of bank statements for all accounts

- Explanation letters for any credit issues or large deposits

- Grant agreements and vesting schedules for equity compensation

Self-employed first time home buyers need additional documentation including profit and loss statements, business tax returns, and sometimes CPA letters verifying income stability.

The initial review typically completes within 24-48 hours for complete application packages. Strong pre-approval letters specify loan amount, program type, and include verification that income and assets have been reviewed by an underwriter, not just estimated through automated systems.

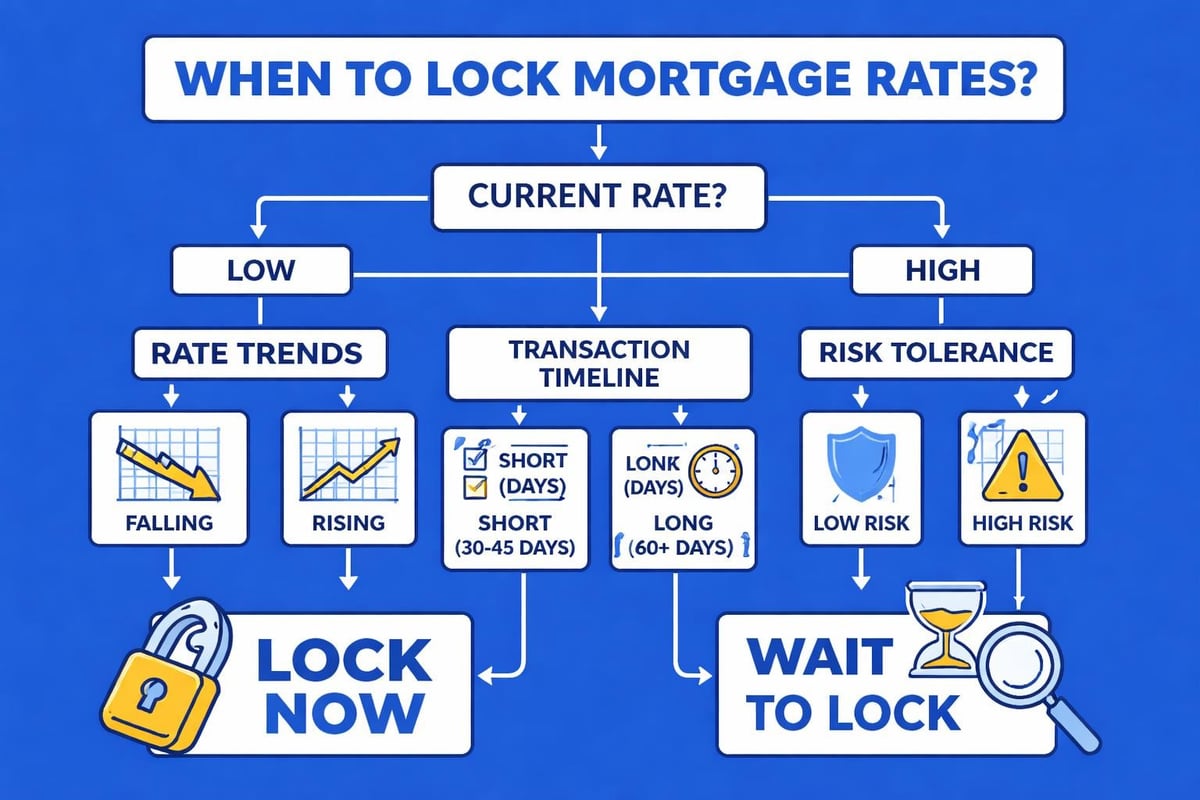

Rate Locks and Timing Considerations

Interest rates fluctuate daily based on economic conditions, Federal Reserve policy, and investor demand for mortgage-backed securities. First time home buyers should understand that pre-approval doesn't lock your rate until you have a signed purchase agreement.

Rate lock periods typically run 30-60 days, with longer locks available for new construction purchases. In volatile rate environments, locking immediately upon offer acceptance protects against increases during your transaction timeline.

Closing Process and Final Steps

The period between offer acceptance and closing typically spans 30-45 days, though experienced lenders can compress timelines to as few as nine business days when needed. Understanding what happens during this period helps first time home buyers stay organized and responsive.

Inspection and Appraisal Coordination

Home inspections typically occur within 10 days of offer acceptance. First time home buyers should attend inspections personally to understand property condition and maintenance requirements. Inspection reports often identify repair negotiations or deal breakers requiring quick decisions.

Appraisals usually occur 1-2 weeks after application, once you've completed the inspection period. The appraisal protects both you and your lender by confirming the home's value supports the purchase price. In competitive Seattle markets, appraisal contingencies are often waived, creating risk if the home appraises below contract price.

Underwriting and Condition Clearance

After application submission, your loan file goes to underwriting where a licensed underwriter reviews all documentation against program guidelines. This process typically generates conditions requiring additional documentation or explanations.

Common underwriting conditions for first time home buyers include:

- Updated pay stubs as you approach closing

- Explanation letters for recent credit inquiries

- Source documentation for large deposits

- Verification of continued employment

- HOA documents and condo questionnaires

- Title work and homeowner's insurance policies

Responding quickly to conditions keeps your closing on schedule. Most delays occur when borrowers take several days to provide requested documentation, creating cascading timeline impacts.

Final Walkthrough and Closing Day

The final walkthrough occurs 24-48 hours before closing, allowing you to verify the property's condition matches your purchase agreement. This isn't a second inspection, but rather confirmation that agreed-upon repairs were completed and no new damage occurred.

Closing day involves signing numerous documents including your promissory note, deed of trust, and closing disclosure. First time home buyers should review the closing disclosure at least three days before closing to verify all numbers match expectations. Washington State requires this three-day review period, and any changes to loan terms or costs restart the clock.

You'll need to bring a cashier's check or arrange wire transfer for your down payment and closing costs. Personal checks aren't accepted for amounts over a few hundred dollars, so coordinate with your bank days in advance.

Common Mistakes First Time Home Buyers Should Avoid

Experience working with hundreds of first time home buyers across the Seattle area reveals recurring pitfalls that derail transactions or create unnecessary stress. Learning from others' mistakes saves time, money, and frustration.

Shopping for Major Purchases During the Loan Process

Financing a car, opening new credit cards, or making large purchases between pre-approval and closing can disqualify your loan. Lenders verify your credit immediately before closing, and new debts change your DTI ratio and may drop your credit score.

Wait until after closing to make major purchases, even if you're using cash. Large withdrawals from documented asset accounts create documentation requirements and potential complications.

Overlooking Total Housing Costs

First time home buyers often focus exclusively on the mortgage payment while underestimating property taxes, insurance, HOA fees, and maintenance costs. In Seattle, property taxes run approximately 0.92% of assessed value annually, though this varies by location.

As detailed in American Home Shield’s complete first-time homebuyer guide, budgeting for ongoing maintenance and repairs prevents financial stress after purchase. Set aside 1-2% of your home's value annually for maintenance and replacement of major systems.

Skipping Homebuyer Education

Many first time home buyers skip educational resources that would save thousands of dollars and prevent costly mistakes. Programs offered through the Washington State Housing Finance Commission provide valuable information about mortgages, budgeting, and homeownership responsibilities.

Some down payment assistance programs require completion of homebuyer education courses, creating additional incentive beyond the knowledge gained. These courses typically cost $75-$125 and complete online in 6-8 hours.

Special Programs for First Time Home Buyers in Washington

Washington State and local municipalities offer numerous programs specifically designed to help first time home buyers enter the market. Understanding available assistance can accelerate your timeline significantly.

State and Local Assistance Programs

The Washington State Housing Finance Commission administers several programs worth investigating:

Home Advantage Program provides down payment assistance loans up to 5% of the purchase price at favorable interest rates. These loans require no monthly payment and are forgiven after remaining in the home for specified periods.

House Key Opportunity Program combines competitive interest rates with down payment assistance for income-qualified buyers. Income limits vary by household size and county, with higher limits in King County reflecting local cost of living.

Seattle's Office of Housing offers targeted programs for specific professions and neighborhoods, with particularly strong support for workforce housing in areas seeing rapid appreciation. According to state-by-state assistance resources, Washington ranks among the top states for first-time buyer support.

Federal Tax Benefits and Credits

First time home buyers should understand available tax benefits including:

- Mortgage interest deduction on loans up to $750,000

- Property tax deduction (though often limited by SALT cap)

- Potential energy efficiency credits for improvements

- Capital gains exclusion when eventually selling (up to $250,000 single, $500,000 married)

Consult a tax professional to understand how homeownership affects your specific tax situation, particularly if you have complex income sources or investment properties.

Building Your Home Buying Team

Success as a first time home buyer depends partly on assembling the right professional team to guide your transaction. Each role serves a specific purpose in protecting your interests and ensuring smooth execution.

Choosing the Right Mortgage Broker

Your mortgage broker serves as your advocate through the financing process, explaining options, securing competitive rates, and managing the application through closing. For first time home buyers, experience with your specific situation matters tremendously.

Look for brokers who:

- Maintain strong reviews across multiple platforms

- Specialize in your employment type (W-2, self-employed, tech compensation)

- Have deep knowledge of your target neighborhoods

- Communicate proactively with clear explanations

- Close loans on schedule consistently

Interview 2-3 mortgage professionals before committing, asking about their process, timeline expectations, and how they handle complications. First time home buyers benefit from educational approaches rather than transactional relationships.

Real Estate Agent Selection

Your buyer's agent should know your target neighborhoods intimately, understand multiple offer strategies, and have strong negotiation skills. For first time home buyers, patience and education matter as much as transaction experience.

Agent qualities to prioritize include:

- Full-time professional status with consistent production

- Specific neighborhood expertise in your search areas

- Experience representing buyers in competitive situations

- Strong communication habits and technology adoption

- Professional network including inspectors, contractors, and title companies

Washington is a buyer agency state, meaning your agent works exclusively for your interests once you establish a relationship. Take advantage of this fiduciary relationship by being completely honest about your needs, concerns, and financial boundaries.

Inspector and Attorney Considerations

Home inspectors provide crucial property condition information, helping first time home buyers understand maintenance needs and potential repair costs. Hire inspectors based on referrals from trusted sources, not just the lowest bid.

While Washington doesn't require attorney involvement in residential real estate transactions, complex situations sometimes benefit from legal review. Condominiums with unusual HOA structures, probate sales, or properties with easement issues may warrant legal consultation.

Long-Term Financial Planning After Purchase

Homeownership introduces new financial planning considerations that first time home buyers should address proactively. Building equity and maintaining your investment requires strategic thinking beyond the initial purchase.

Building Equity Through Strategic Payments

Your mortgage payment includes principal and interest, with early payments weighted heavily toward interest. Understanding this amortization schedule helps first time home buyers decide whether extra principal payments make sense for their situation.

Making one extra payment annually reduces a 30-year mortgage to approximately 25 years and saves significant interest over the loan's life. However, this strategy only makes sense if you've already:

- Maxed employer retirement matching (highest guaranteed return)

- Maintained 3-6 months emergency reserves

- Paid off high-interest debt (credit cards, personal loans)

- Funded other short-term savings goals

For first time home buyers with low mortgage rates (below 4%), investing excess cash in retirement accounts often produces better long-term returns than accelerated mortgage payoff.

Refinancing Considerations and Timing

Monitor market conditions and your financial profile for refinancing opportunities. Rate improvement of 0.75-1% typically justifies refinancing costs, though this threshold varies based on loan size and how long you plan to remain in the property.

First time home buyers should also consider refinancing to remove PMI once reaching 20% equity, even if rates haven't dropped significantly. The monthly savings from PMI elimination often exceeds the value of slightly lower rates.

Market Trends Affecting Seattle First Time Home Buyers in 2026

Understanding current market dynamics helps first time home buyers set realistic expectations and plan effective strategies. The Greater Seattle market has evolved significantly in recent years, creating both challenges and opportunities.

Inventory Levels and Seasonal Patterns

Seattle traditionally sees inventory increase in spring and summer, with March through June representing peak buying season. First time home buyers shopping during winter months often face less competition but also fewer available properties.

Current inventory remains below historical averages in most Seattle neighborhoods, though outer areas like Everett and Mill Creek show improving selection. This supply constraint keeps upward pressure on prices, particularly for well-maintained homes in desirable school districts.

Interest Rate Environment

The Federal Reserve's monetary policy significantly influences mortgage rates, though the relationship isn't perfectly direct. First time home buyers in 2026 navigate an environment where rates fluctuate based on inflation data, employment reports, and geopolitical events.

Rather than trying to time the market perfectly, focus on what you can control: your credit profile, down payment amount, and documentation quality. These factors influence your individual rate more than market timing strategies.

According to Opendoor’s first-time buying tips, focusing on long-term affordability rather than short-term rate movements leads to better outcomes for most buyers.

Technology Industry Impact on Housing Demand

Seattle's housing market remains closely tied to the technology sector's health. Strong hiring at major employers increases demand, while layoffs or hiring freezes create temporary softening. First time home buyers who work in tech should consider employment stability when determining comfortable purchase prices.

Remote work policies also continue reshaping demand patterns, with some buyers prioritizing space over commute convenience. This trend particularly benefits areas like Mill Creek and Lake Forest Park, where larger homes at lower prices per square foot attract families willing to commute occasionally.

Navigating the path to homeownership requires preparation, patience, and partnership with experienced professionals who understand both the Seattle market and the unique needs of first time home buyers. From understanding mortgage qualification with complex tech compensation to competing effectively in multiple offer situations, success comes from education and strategic execution. Keith Akada and the team at Mortgage Reel bring 25+ years of expertise helping first time home buyers across Seattle, Bellevue, Redmond, and Kirkland achieve their homeownership goals with clarity, transparency, and proven results. Whether you're exploring your options or ready to get pre-approved, Mortgage Reel provides the guidance and execution you need to buy confidently in 2026's competitive market.