Navigating the mortgage landscape in Seattle requires more than just comparing interest rates online. A qualified mortgage financial advisor brings expertise, market knowledge, and strategic guidance to help homebuyers and homeowners make informed financing decisions. Whether you’re purchasing your first condo in Shoreline or refinancing a jumbo loan in Bellevue, working with an experienced advisor can mean the difference between a stressful transaction and a smooth, confidence-building experience. Understanding what a mortgage financial advisor does and how they can serve your specific financial situation is essential for anyone entering the competitive Seattle-area housing market.

What Is a Mortgage Financial Advisor?

A mortgage financial advisor is a licensed professional who specializes in helping clients navigate the complexities of home financing. Unlike traditional loan officers who may focus solely on originating loans, a comprehensive advisor takes a holistic approach to your financial picture.

Core Responsibilities and Expertise

These professionals evaluate your income, assets, credit profile, and long-term financial goals to recommend appropriate loan products and strategies. They analyze conventional loans, FHA, VA, jumbo financing, and specialized programs to find the best fit for your situation.

Key functions include:

- Assessing your complete financial profile including W-2 income, self-employment earnings, and investment income

- Explaining loan program guidelines, underwriting requirements, and qualification criteria

- Calculating debt-to-income ratios and maximum borrowing capacity

- Structuring loan scenarios to optimize approval odds and monthly payments

- Coordinating with underwriters, processors, and closing teams throughout the transaction

For tech professionals in Seattle working at companies like Amazon or Microsoft, a mortgage financial advisor provides specialized expertise in qualifying RSUs, stock options, bonuses, and other non-traditional compensation. This knowledge becomes critical when maximizing purchasing power in high-cost markets like Redmond or Kirkland.

Why Seattle Homebuyers Need Specialized Mortgage Guidance

The Greater Seattle housing market presents unique challenges that require expert navigation. Median home prices consistently exceed national averages, competitive multiple-offer scenarios are common, and many buyers rely on complex compensation structures.

Market Complexity Demands Professional Insight

In neighborhoods from Mill Creek to Lynnwood, buyers face fast-moving inventory and sophisticated sellers. A mortgage financial advisor helps you understand how much home you can truly afford, not just what a generic online calculator suggests.

They factor in property taxes, homeowners insurance, HOA fees, and potential mortgage insurance to calculate realistic monthly obligations. This prevents overextension and ensures you maintain financial flexibility after closing.

| Challenge | How Advisors Help |

|---|---|

| Stock-based compensation | Qualify RSUs, options, and vesting schedules per guidelines |

| Jumbo loan requirements | Navigate higher credit and reserve standards |

| Fast closings | Structure documentation and underwriting for 9-15 day timelines |

| Multiple properties | Strategize debt ratios across investment and primary homes |

Building a network of trusted advisors, as recommended by the Consumer Financial Protection Bureau, strengthens your entire homebuying team and decision-making process.

The Mortgage Advisor Qualification Process

Professional mortgage advisors must meet strict licensing, education, and continuing education requirements. In Washington State, this means completing federal NMLS registration, background checks, and ongoing training.

Certification and Professional Standards

Many advisors pursue advanced designations to demonstrate expertise and commitment to ethical practices. The Certified Mortgage Advisor™ designation represents rigorous training focused on client education, financial security analysis, and comprehensive advisory services beyond basic loan origination.

Experience matters significantly in this field. An advisor with 25+ years of market cycles has navigated interest rate fluctuations, guideline changes, housing downturns, and boom periods. This historical perspective informs better recommendations during uncertain times.

What to verify when selecting an advisor:

- Active NMLS license and clean disciplinary record

- Years of experience in your local market

- Client reviews and testimonials across multiple platforms

- Lender partnerships and product access

- Communication style and availability during transactions

The Seattle market’s sophistication demands advisors who understand local appraisal practices, title requirements, and inspection timelines. An advisor serving Lake Forest Park should know how waterfront properties are valued differently than standard single-family homes.

Loan Product Selection and Strategy

One of the most valuable services a mortgage financial advisor provides is matching you with the right loan structure for both your current situation and future plans.

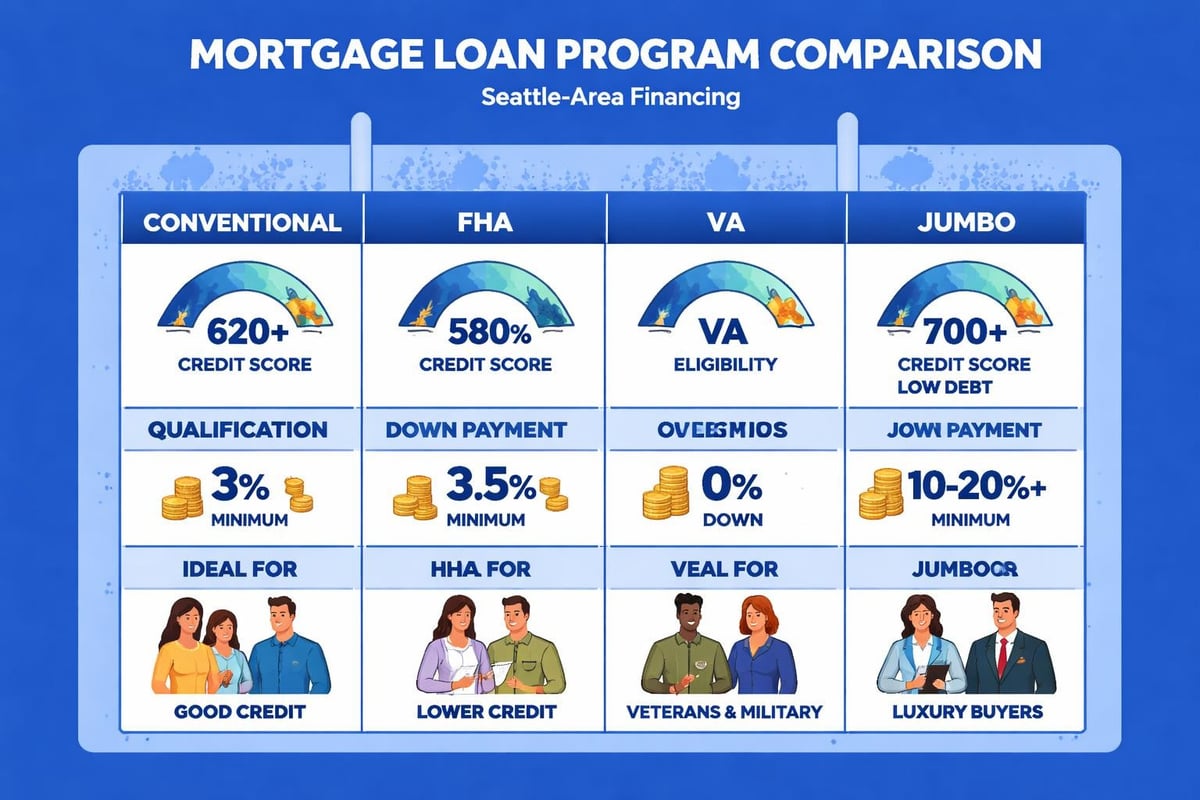

Conventional Financing Options

For borrowers with strong credit (typically 680+) and sufficient down payment funds, conventional loans offer competitive rates and flexible terms. These loans conform to Fannie Mae and Freddie Mac guidelines, with loan limits adjusted annually for high-cost areas.

In 2026, Seattle-area conventional loan limits allow borrowing up to $806,500 for single-family homes in King County before entering jumbo territory. A skilled advisor explains how 5%, 10%, or 20% down payment affects your rate, monthly payment, and private mortgage insurance requirements.

Jumbo Loan Expertise for High-Value Properties

Properties above conforming limits require jumbo financing with different underwriting standards. These loans typically demand:

- Credit scores of 700 or higher

- Lower debt-to-income ratios (often 43% or below)

- Larger cash reserves (6-12 months of payments)

- More comprehensive income documentation

A mortgage financial advisor structures your application to meet these stricter requirements while maximizing your approval amount. For Everett buyers purchasing luxury homes or Seattle professionals buying in competitive neighborhoods, jumbo expertise becomes essential.

Government-Backed Loan Programs

FHA loans serve first-time buyers and those with smaller down payments or credit challenges. VA loans provide exceptional benefits for eligible military service members and veterans, including zero down payment options and no mortgage insurance.

Each program has specific use cases where it excels:

| Program Type | Best For | Key Advantage |

|---|---|---|

| Conventional | Strong credit, 5%+ down | Lowest rates, flexible terms |

| FHA | Lower credit, 3.5% down | Accessible approval standards |

| VA | Military/veterans | Zero down, no PMI |

| Jumbo | High-value properties | Large loan amounts available |

Your advisor analyzes which program delivers the lowest total cost over your expected ownership period, not just the lowest rate advertised today.

Stock Compensation and Complex Income Qualification

Seattle’s concentration of major tech employers creates unique mortgage challenges. Many professionals receive significant portions of compensation through RSUs, stock options, bonuses, and equity grants rather than base salary alone.

How Advisors Qualify Non-Traditional Income

Underwriting guidelines for stock-based compensation have evolved considerably. A knowledgeable mortgage financial advisor understands how to document and verify these income sources according to current standards.

RSU qualification typically requires:

- Two-year history of receiving and vesting equity compensation

- Consistent pattern showing income is likely to continue

- Proper documentation through pay stubs, W-2s, and vesting schedules

- Calculation methods that average income over time

For Amazon employees in Seattle or Microsoft workers in Redmond, this expertise directly impacts buying power. The difference between an advisor who can effectively qualify your total compensation versus one who only considers base salary can mean hundreds of thousands of dollars in purchasing capacity.

Bonuses require similar documentation and history. An advisor skilled in complex income structures knows which documentation satisfies underwriters and how to present your financial profile for maximum approval strength.

The Pre-Approval Process and Timeline

Serious homebuyers in competitive markets like Bellevue or Kirkland need strong pre-approval letters that sellers and listing agents take seriously. A mortgage financial advisor provides this credibility through thorough upfront underwriting.

What Comprehensive Pre-Approval Includes

True pre-approval goes far beyond a soft credit pull and income estimate. It involves submitting full documentation for underwriter review before you even find a property.

- Complete credit report review and analysis

- Income verification through recent pay stubs, W-2s, and tax returns

- Asset documentation showing down payment and reserve funds

- Initial underwriter evaluation of your file

- Commitment letter stating specific approval terms

This process typically takes 3-5 business days when you provide documents promptly. The result is a pre-approval letter that gives you confidence during house hunting and demonstrates to sellers that your financing is reliable.

In multiple-offer situations common throughout the Seattle area, this distinction matters. Sellers choose buyers they trust will close, and a thoroughly underwritten pre-approval signals that reliability.

Working Through the Application and Underwriting Process

Once you have an accepted offer, your mortgage financial advisor coordinates the formal application, appraisal, title work, and underwriting review.

Documentation and Communication

Expect to provide detailed financial documentation including:

- 30 days of pay stubs covering current year

- 2 years of W-2s and tax returns

- 2 months of bank statements for all accounts

- Retirement account statements if using for reserves

- Purchase agreement and property details

Your advisor reviews these documents before submission to catch potential issues. They explain any conditions the underwriter requests and guide you through providing satisfactory responses.

Common underwriting conditions:

- Explanation letters for large deposits or credit inquiries

- Verification of employment closer to closing

- Updated pay stubs showing continued employment

- Gift letter documentation if receiving down payment assistance

Clear, proactive communication throughout this 30-45 day period prevents last-minute surprises. An experienced advisor anticipates potential concerns and addresses them before they become problems.

Interest Rate Strategy and Lock Timing

Interest rates fluctuate daily based on economic factors, Federal Reserve policy, and bond market movements. A mortgage financial advisor helps you understand rate trends and make strategic lock decisions.

When to Lock Your Rate

Rate locks guarantee a specific interest rate for a defined period, typically 30-60 days. Locking too early risks missing lower rates, while waiting too long exposes you to potential increases.

Your advisor monitors market conditions and recommends lock timing based on:

- Current rate trends and economic indicators

- Your timeline to closing

- Your risk tolerance for rate volatility

- Specific loan program and property type

For construction loans or delayed closings in Shoreline or Lynnwood, extended locks or float-down options might make sense. Your advisor explains these strategies and associated costs clearly.

Rate is important, but it’s not the only factor. Annual percentage rate (APR) captures total loan costs including fees, providing a more complete comparison metric when evaluating lender options.

Cost Analysis and Fee Transparency

Understanding the complete cost structure of your mortgage prevents surprises at closing. A trustworthy mortgage financial advisor provides detailed fee breakdowns early in the process.

Typical Mortgage Costs

Borrowers pay both lender fees and third-party costs. Lender fees include origination charges, underwriting fees, and processing costs. Third-party costs cover appraisal, title insurance, escrow, recording, and other services.

Common fee categories:

- Origination/broker fees: 0.5-1% of loan amount

- Appraisal: $500-800 for standard homes, more for complex properties

- Title insurance: Based on purchase price, roughly $1,000-2,000

- Escrow/closing fees: $500-1,500

- Prepaid items: Property taxes, homeowners insurance, interest

In Washington State, buyers typically pay their own closing costs unless negotiated otherwise. Your advisor helps you understand which fees are negotiable and where you might find savings without compromising service quality.

Comparing loan estimates across lenders requires careful analysis of fees, rates, and terms. An ethical advisor explains exactly what you’re paying for and why, never hiding costs in fine print.

Refinance Strategy and Timing

Homeowners in Seattle and surrounding areas regularly evaluate refinance opportunities to lower payments, access equity, or adjust loan terms. A mortgage financial advisor helps determine when refinancing makes financial sense.

Rate-and-Term Refinancing

This strategy involves replacing your current mortgage with a new loan at better terms, ideally a lower rate or shorter term. The breakeven analysis is critical: how long will it take for monthly savings to offset closing costs?

If you plan to stay in your Everett home for five more years and can break even in 18 months through refinancing, the decision is straightforward. If you might relocate sooner, the math becomes less favorable.

Cash-Out Refinancing Considerations

Accessing home equity through cash-out refinancing allows you to fund renovations, consolidate debt, or make investments. Your advisor structures this carefully to maintain strong loan-to-value ratios and avoid unnecessary risk.

Lenders typically limit cash-out refinances to 80% loan-to-value on primary residences, though requirements vary by program and property type. Understanding these constraints helps you plan appropriately.

Choosing the Right Mortgage Financial Advisor

Not all mortgage professionals offer the same level of expertise, service, or results. Selecting an advisor requires evaluating multiple factors beyond advertised rates.

Key Selection Criteria

Look for advisors with extensive local market experience, strong client reviews across multiple platforms, and transparent communication practices. The number of five-star reviews and consistency across Google, Zillow, Redfin, and other sites indicates reliable service delivery.

Questions to ask potential advisors:

- How many years have you worked in the Seattle market specifically?

- What percentage of your clients are tech professionals with stock compensation?

- What is your typical timeline from application to closing?

- How do you communicate throughout the transaction?

- Can you provide recent client references?

An advisor with 750+ verified five-star reviews demonstrates a long track record of satisfied clients. This social proof matters more than self-promotional marketing claims.

Availability and responsiveness also matter significantly. In competitive markets where offers require quick responses, you need an advisor who answers calls, responds to emails promptly, and proactively updates you on progress.

Advanced Strategies for Investment Properties

Real estate investors in the Seattle area face different qualification standards and strategic considerations. A sophisticated mortgage financial advisor helps you build a multi-property portfolio effectively.

Investment Property Financing Requirements

Lenders view investment properties as higher risk, requiring larger down payments (typically 15-25%), higher credit scores, and more substantial reserves. Debt-to-income calculations include the new property’s projected payment, not just rental income.

Your advisor helps you structure acquisitions to maintain qualification capacity for future purchases. This might involve:

- Timing purchases to maximize reported rental income

- Structuring LLCs appropriately for lending purposes

- Maintaining adequate liquidity across properties

- Understanding how each acquisition affects future borrowing power

For investors in Lake Forest Park or Mill Creek building portfolios, this strategic guidance becomes invaluable as you scale beyond your first rental property.

Common Mistakes a Mortgage Financial Advisor Helps You Avoid

Even financially sophisticated buyers make errors during the mortgage process that cost money or jeopardize approval. Professional guidance prevents these pitfalls.

Documentation and Timing Errors

Changing jobs during the mortgage process can complicate approval, as can making large purchases on credit or moving money between accounts without explanation. Your advisor warns you about these actions upfront.

Other common mistakes include:

- Shopping for furniture or cars before closing

- Accepting new credit card offers

- Making unexplained large deposits

- Switching bank accounts during underwriting

- Failing to respond promptly to conditions

A proactive advisor educates you on what to avoid from contract to closing, preventing delays or worse, loan denials just days before scheduled closing.

Overlooking Total Cost of Ownership

First-time buyers especially often focus exclusively on monthly principal and interest payments, forgetting property taxes, insurance, HOA fees, and maintenance costs. Your advisor helps you model complete ownership expenses.

For a $800,000 home in Bellevue, monthly obligations might include $3,500 for principal and interest, $900 for property taxes, $150 for insurance, and $300 for HOA fees. Understanding this $4,850 total payment prevents budget strain after closing.

Working with an experienced mortgage financial advisor transforms the homebuying or refinancing process from overwhelming to manageable. The right advisor brings market expertise, strategic guidance, and proven execution to help you achieve your homeownership goals confidently. Whether you’re a first-time buyer in Shoreline, a tech professional navigating complex compensation in Seattle, or an investor building a portfolio across King County, Keith Akada and Mortgage Reel provide the education, transparency, and strategic approach you need to make sound financing decisions backed by 25+ years of experience and 750+ five-star client reviews.

Frequently Asked Questions

1. What should I look for when choosing a mortgage financial advisor?

When selecting a mortgage financial advisor, consider their local market experience, client reviews, and communication style. Look for advisors with a strong track record, ideally with numerous five-star reviews across platforms like Google and Zillow. It’s also important to ask about their experience with clients who have similar financial situations, such as tech professionals with stock compensation. Additionally, inquire about their typical timeline from application to closing and how they keep clients informed throughout the process.

2. How can a mortgage financial advisor help with refinancing?

A mortgage financial advisor can provide valuable insights into whether refinancing is a smart financial move for you. They analyze your current mortgage terms, interest rates, and your long-term financial goals. By conducting a breakeven analysis, they help you understand how long it will take for the savings from a lower rate to offset the closing costs. They can also guide you on cash-out refinancing options if you want to access your home equity for renovations or other investments.

3. What are the common mistakes to avoid during the mortgage process?

Common mistakes during the mortgage process include changing jobs, making large purchases on credit, or moving money between accounts without proper documentation. These actions can complicate your approval. Additionally, first-time buyers often overlook the total cost of ownership, focusing only on monthly payments. A mortgage financial advisor helps you avoid these pitfalls by educating you on what to avoid and ensuring you understand all financial obligations associated with homeownership.

4. How does stock-based compensation affect mortgage qualification?

Stock-based compensation, such as RSUs and stock options, can complicate mortgage qualification. Lenders require a consistent history of receiving and vesting equity compensation to consider it as income. A knowledgeable mortgage financial advisor understands the documentation needed, such as pay stubs and vesting schedules, to effectively present your financial profile. This expertise can significantly impact your purchasing power, especially for tech professionals in high-cost markets like Seattle.

5. What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal assessment of your financial situation, often based on self-reported information, while pre-approval involves a thorough review of your financial documents by a lender. A mortgage financial advisor can help you obtain a comprehensive pre-approval, which includes a complete credit report review, income verification, and an initial underwriter evaluation. This process provides a stronger position in competitive markets, as it demonstrates to sellers that you are a serious and reliable buyer.

6. How can I ensure transparency in mortgage costs?

To ensure transparency in mortgage costs, work with a mortgage financial advisor who provides a detailed breakdown of all fees early in the process. This includes lender fees, third-party costs, and any potential negotiable items. Understanding the complete cost structure helps you avoid surprises at closing. A trustworthy advisor will explain each fee clearly, ensuring you know what you are paying for and why, allowing for better comparisons across different lenders.

7. What role does a mortgage financial advisor play in the application process?

A mortgage financial advisor plays a crucial role in the application process by coordinating all aspects, including documentation, appraisal, and underwriting. They help you gather necessary financial documents, review them for accuracy, and submit them to the lender. Throughout the 30-45 day underwriting period, your advisor maintains clear communication, addressing any conditions or requests from the underwriter promptly. Their proactive approach helps prevent last-minute surprises and ensures a smoother closing experience.