Navigating the mortgage landscape in Seattle’s competitive housing market requires a clear understanding of your financing options. Conventional home loan programs remain the most popular choice for homebuyers across the Puget Sound region, representing the majority of purchase transactions in communities from downtown Seattle to Shoreline, Lynnwood, and beyond. Unlike government-backed loans such as FHA or VA mortgages, conventional loans are not insured or guaranteed by federal agencies, which creates both advantages and specific qualification requirements that borrowers should understand before beginning their home search.

What Defines Conventional Home Loan Programs

Conventional home loan programs are mortgage products offered by private lenders and backed by government-sponsored enterprises Fannie Mae and Freddie Mac. These loans follow standardized underwriting guidelines established by these entities, creating consistency across lenders while maintaining flexibility for various borrower profiles.

The Consumer Financial Protection Bureau provides comprehensive information about how these loans differ from government-insured options. The primary distinction lies in the risk assumption: with conventional financing, lenders rely on private mortgage insurance and borrower qualifications rather than government backing.

Conforming vs. Non-Conforming Conventional Loans

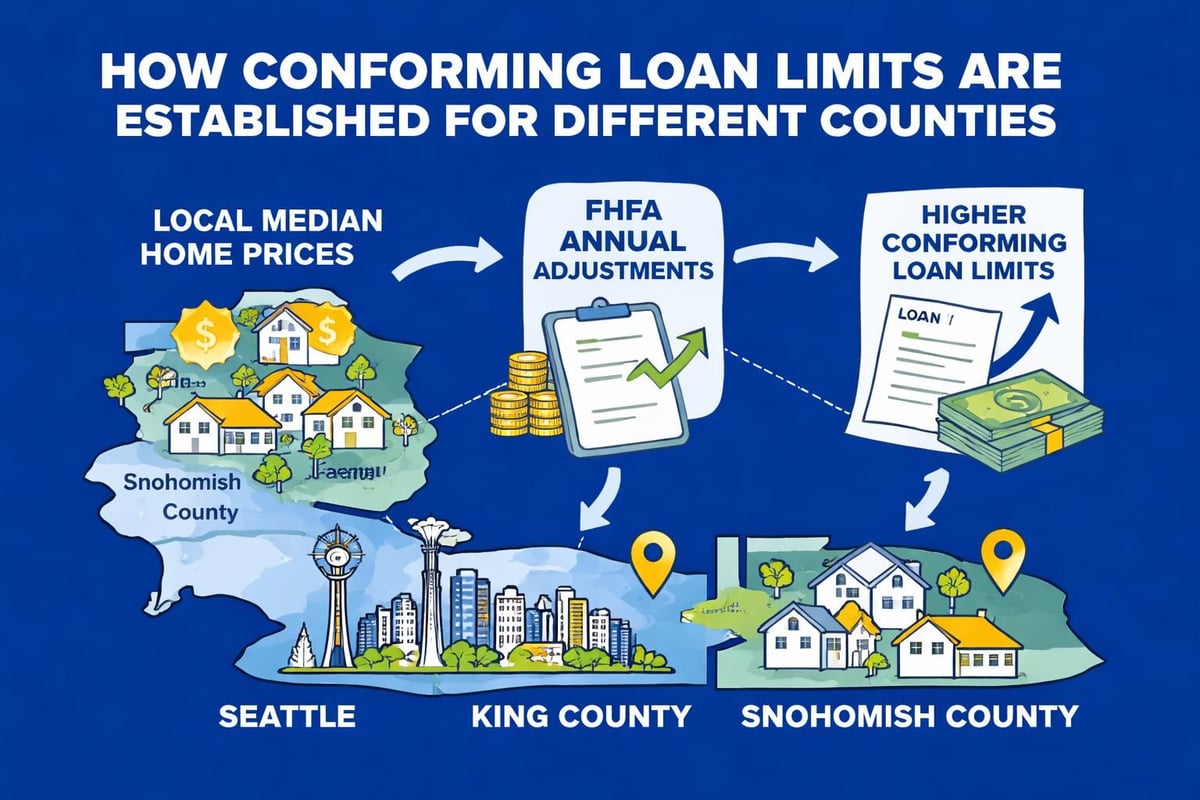

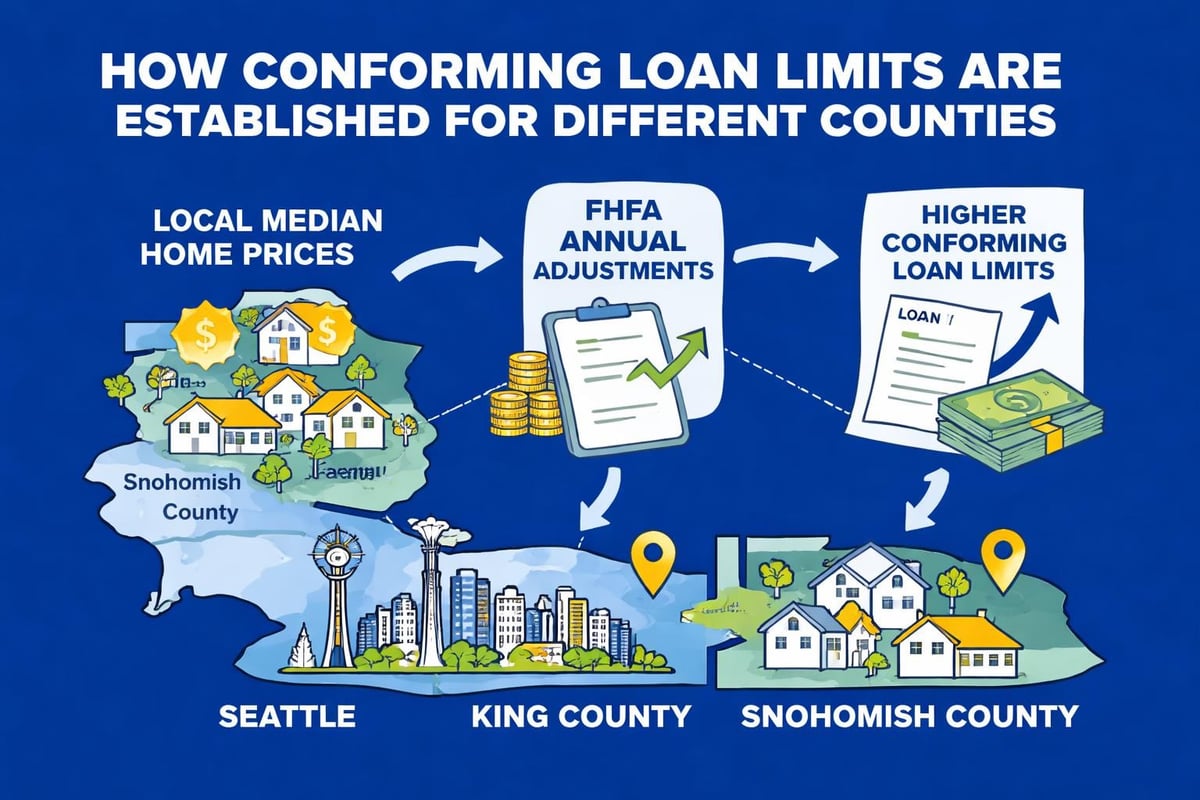

Conventional mortgages fall into two main categories based on loan amount. Conforming loans adhere to the limits established annually by the Federal Housing Finance Agency, which for 2026 stands at $806,500 for single-family homes in most counties. King County, Snohomish County, and other high-cost areas often receive higher limits due to elevated property values.

Non-conforming loans, commonly called jumbo loans, exceed these thresholds. In Seattle’s competitive neighborhoods like Capitol Hill, Queen Anne, or Medina, where median home prices frequently surpass conforming limits, jumbo financing becomes essential for many buyers. These loans typically require stronger credit profiles and larger down payments but offer the purchasing power needed in premium markets.

Credit Score Requirements and Qualification Standards

Credit standards for conventional home loan programs are more stringent than government-backed alternatives, but they also offer better pricing for well-qualified borrowers. Most lenders establish a minimum credit score of 620 for conventional financing, though some portfolio products may accept scores as low as 580 with compensating factors.

Credit Score Impact on Rates and Terms:

- 780+ scores: Access to best available rates and lowest fees

- 720-779 scores: Competitive pricing with minimal adjustments

- 680-719 scores: Moderate rate adjustments and possible additional requirements

- 620-679 scores: Higher rates and stricter documentation standards

For Seattle-area tech professionals at Amazon, Microsoft, and Google, strong credit profiles combined with substantial income often position them favorably for optimal pricing. However, recent graduates or those rebuilding credit should expect additional scrutiny and potentially higher costs.

Debt-to-Income Ratio Considerations

Conventional underwriting examines your debt-to-income ratio (DTI) carefully, typically capping total monthly obligations at 43-50% of gross income. This calculation includes your proposed mortgage payment, property taxes, homeowners insurance, HOA fees, and all recurring debts like student loans, auto payments, and credit cards.

Seattle’s high property taxes and homeowners insurance premiums can significantly impact DTI calculations. A $750,000 home in Lake Forest Park might carry monthly property taxes exceeding $900 and insurance costs approaching $200, which reduces available borrowing capacity compared to markets with lower housing costs.

Down Payment Options and Private Mortgage Insurance

One of the most significant advantages of conventional home loan programs is the flexibility in down payment requirements. While the traditional 20% down payment eliminates the need for mortgage insurance, conventional loans accept down payments as low as 3% for qualified first-time buyers and 5% for repeat purchasers.

| Down Payment | PMI Required | Loan-to-Value Ratio | Best For |

|---|---|---|---|

| 3-4.99% | Yes | 95-97% LTV | First-time buyers with limited savings |

| 5-9.99% | Yes | 90-95% LTV | Repeat buyers, moderate equity available |

| 10-19.99% | Yes | 80-90% LTV | Buyers seeking balance of liquidity and cost |

| 20%+ | No | 80% LTV or lower | Those prioritizing lowest monthly payment |

Private mortgage insurance (PMI) protects the lender if you default on the loan. Unlike FHA mortgage insurance, which remains for the loan’s life on purchases with less than 10% down, conventional PMI automatically terminates once you reach 22% equity through payments and appreciation. Seattle’s strong property value growth has helped many homeowners eliminate PMI ahead of schedule.

However, putting less down and accepting PMI may prove strategically sound when investment returns exceed borrowing costs or when preserving liquid reserves provides financial security. This decision requires careful analysis of individual circumstances, opportunity costs, and risk tolerance.

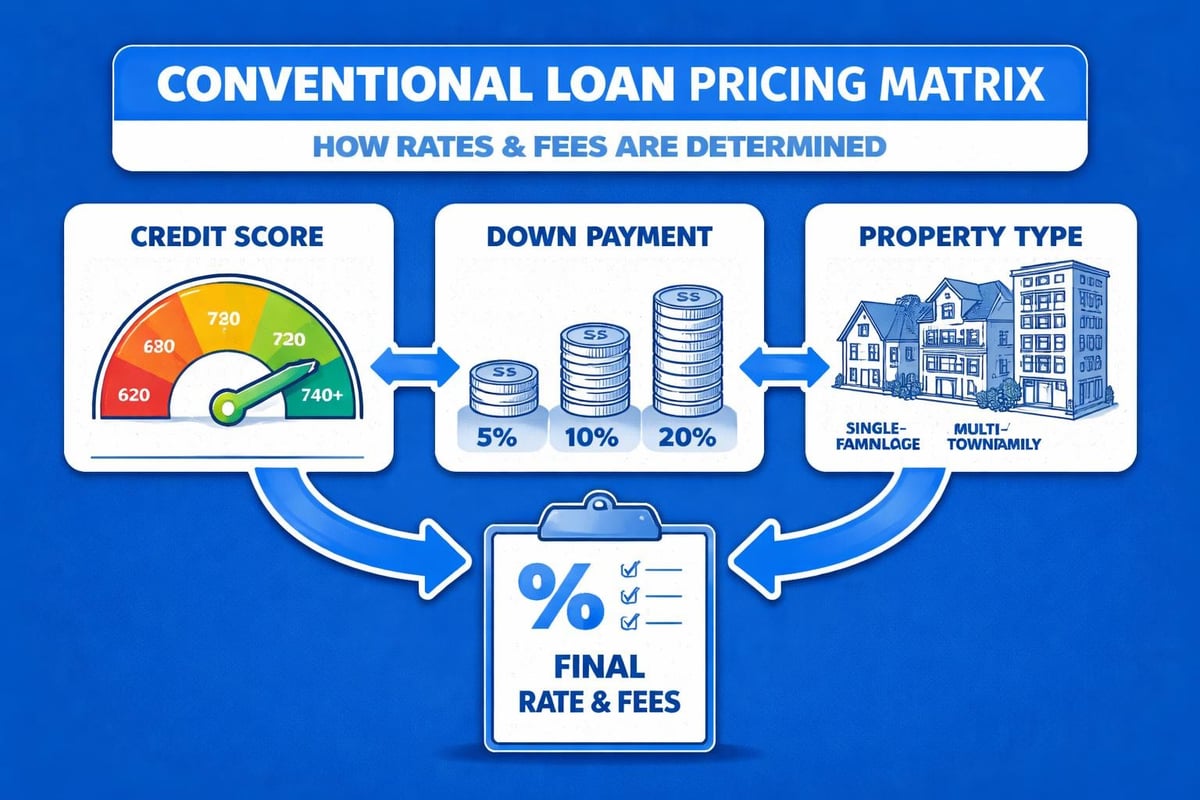

Interest Rates and Pricing Adjustments

Conventional home loan programs offer competitive interest rates that fluctuate based on market conditions, borrower qualifications, and property characteristics. In 2026, rates have stabilized compared to the volatility experienced in 2022-2024, though they remain sensitive to Federal Reserve policy and economic indicators.

Factors Influencing Your Rate:

- Credit score and profile strength

- Loan-to-value ratio and down payment size

- Property type (single-family, condo, multi-unit)

- Occupancy status (primary residence, second home, investment)

- Loan term (15-year, 20-year, 30-year)

- Points and closing cost credits selected

Lenders apply loan-level price adjustments (LLPAs) based on these factors, which can increase or decrease your rate by meaningful amounts. A borrower with a 680 credit score putting 5% down might pay 1.5-2% more in rate or upfront fees compared to a borrower with a 760 score putting 20% down on an identical property.

Fixed-Rate vs. Adjustable-Rate Options

Conventional loans are available in both fixed-rate and adjustable-rate formats. Fixed-rate mortgages maintain the same interest rate for the entire loan term, providing payment stability that many Seattle buyers prefer given the region’s high property costs.

Adjustable-rate mortgages (ARMs) offer lower initial rates that adjust periodically after a fixed period. Common structures include 5, 7, and 10 ARMs, where the first number indicates years of fixed rates before annual adjustments begin. These products appeal to buyers who anticipate moving, refinancing, or significantly increasing income within the fixed period.

Tech professionals in Redmond with substantial stock compensation often use ARMs strategically, planning to pay down principal aggressively or refinance once RSUs vest and provide additional liquidity.

Documentation and Income Verification

Conventional home loan programs require comprehensive documentation of income, assets, and employment. Standard salaried employees provide recent pay stubs, W-2 forms, and employment verification. Self-employed borrowers need two years of personal and business tax returns along with year-to-date profit and loss statements.

Qualifying Stock Compensation and Bonuses

Seattle’s concentration of technology employers creates unique documentation scenarios. Restricted stock units (RSUs), stock options, and performance bonuses represent significant income sources that require specific treatment under conventional guidelines.

RSU and Stock Income Documentation:

- Provide vesting schedules showing future grant dates and amounts

- Submit tax returns demonstrating history of stock income receipt

- Calculate average income over two years for qualification purposes

- Document current stock value and potential tax implications

- Verify employer continuation of compensation structure

Lenders typically average two years of stock income, though some allow current-year projections with strong vesting documentation. For a Microsoft employee with $150,000 base salary and $100,000 annual RSU vesting, qualifying income might reach $225,000-$250,000 depending on vesting history and documentation strength.

Property Type and Condition Requirements

Conventional home loan programs maintain specific property standards that influence eligibility. Single-family homes, condominiums, townhomes, and multi-unit properties (up to four units) all qualify, though requirements vary by property type.

Condominiums require additional review of the homeowners association, including financial health, insurance coverage, owner-occupancy ratios, and litigation status. Seattle’s abundant condo inventory means buyers should verify project eligibility early in the transaction.

Appraisal and Property Condition Standards

Properties must meet basic safety, soundness, and security standards. While conventional loans are more lenient than FHA regarding property condition, significant health or safety issues identified during appraisal may require resolution before closing.

The appraisal determines property value and ensures the purchase price aligns with market conditions. According to National Association of Realtors data, appraisal gaps have become less common as 2026 market conditions have stabilized, but competitive Seattle neighborhoods occasionally still experience valuation challenges.

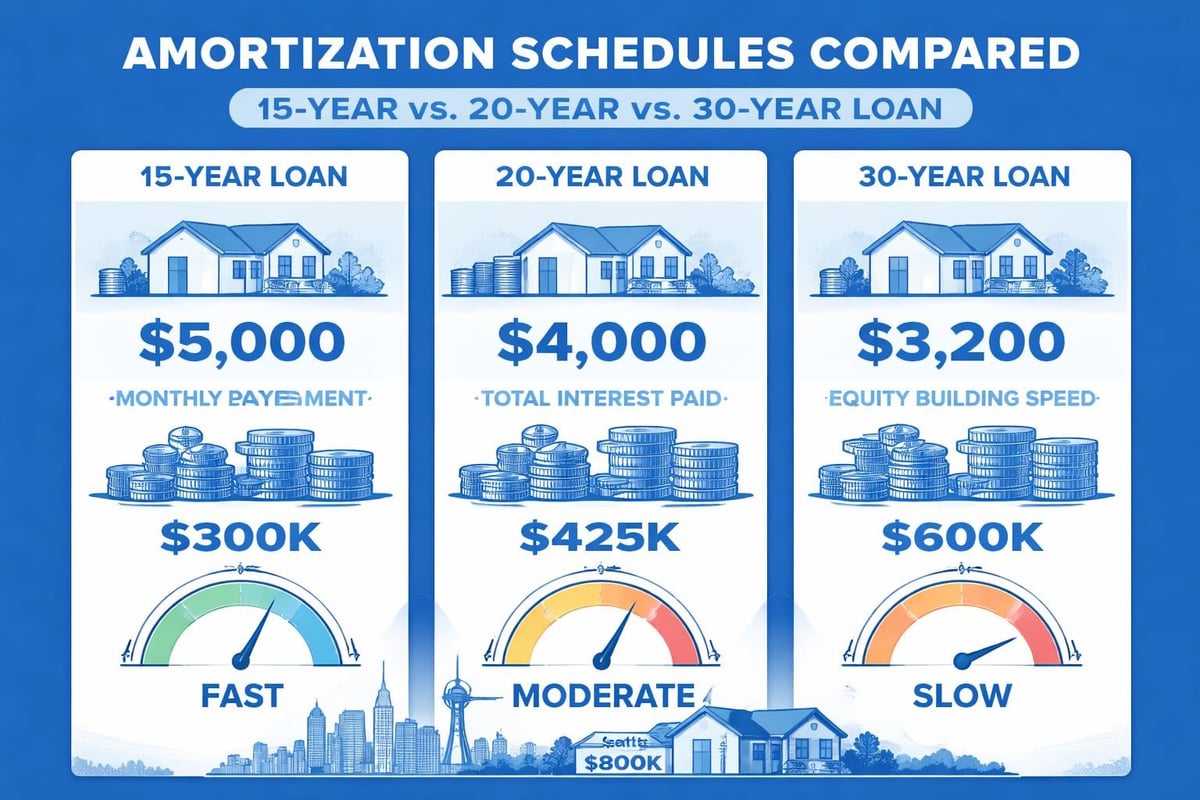

Loan Terms and Repayment Structures

The most common conventional loan term spans 30 years, providing the lowest monthly payment through extended amortization. However, conventional home loan programs offer flexibility in term selection based on financial goals and circumstances.

| Loan Term | Monthly Payment | Total Interest | Best For |

|---|---|---|---|

| 15-year | Highest | Lowest | Strong income, equity building priority |

| 20-year | Moderate-high | Moderate-low | Balance of payment and payoff speed |

| 30-year | Lowest | Highest | Cash flow optimization, investment opportunities |

Shorter terms carry lower interest rates but higher monthly payments. A $600,000 loan at 6.5% costs approximately $3,790 monthly on a 30-year term versus $5,230 on a 15-year term. However, the 15-year borrower saves over $260,000 in interest and builds equity much faster.

Biweekly Payment Strategies

Many Seattle homeowners implement biweekly payment strategies, making half their monthly payment every two weeks rather than one full payment monthly. This results in 26 half-payments (13 full payments) annually instead of 12, accelerating principal reduction and shortening the loan term by 4-6 years on a 30-year mortgage.

This approach requires discipline but costs nothing to implement independently, unlike formal biweekly programs that charge setup and transaction fees. The strategy works particularly well for borrowers paid biweekly who can align mortgage payments with paycheck receipt.

Reserve Requirements and Asset Verification

Lenders evaluate your financial reserves to ensure you can withstand unexpected expenses or income disruptions. Reserve requirements vary based on loan amount, occupancy type, and credit profile, typically ranging from zero to six months of principal, interest, taxes, and insurance (PITI).

Investment properties and multi-unit homes require the highest reserves, often six months of PITI for each financed property. Primary residence purchases in Shoreline or Lynnwood might require only two months of reserves, while no reserves may be needed for exceptionally strong borrowers on lower-balance loans.

Acceptable Reserve Assets:

- Checking and savings account balances

- Stocks, bonds, and mutual fund investments (70-90% value counted)

- Retirement accounts like 401(k) and IRA (60-70% value counted for age restrictions)

- Cash value of life insurance policies

- Proceeds from pending asset sales with documented contracts

Borrowed funds, including gifts that require repayment, do not qualify as reserves. Documentation requirements include two months of bank statements showing consistent balances without unexplained large deposits.

Secondary Residence and Investment Property Financing

Conventional home loan programs extend beyond primary residences to include second homes and investment properties, though qualification standards tighten considerably. Second homes require occupancy for some portion of the year and cannot generate rental income, making them suitable for vacation properties in locations like the San Juan Islands or Cascade foothills.

Investment properties are purchased explicitly for rental income and require minimum 15-20% down payments depending on unit count and borrower profile. Lenders incorporate expected rental income into qualification calculations, typically counting 75% of market rent to offset the additional housing payment.

Multi-Unit Property Considerations

Purchasing a duplex, triplex, or fourplex as a primary residence represents a strategic approach for many Seattle buyers. Living in one unit while renting others allows rental income to offset mortgage costs while building equity and real estate investment experience.

Conventional programs count 75% of expected rental income from non-occupied units toward qualifying income after subtracting the full PITI payment. This structure can dramatically increase purchasing power for buyers comfortable with landlord responsibilities and property management.

Refinancing with Conventional Programs

Existing homeowners utilize conventional home loan programs not just for purchases but also for refinancing existing mortgages. Rate-and-term refinancing replaces your current loan with new terms, ideally reducing interest rates, shortening loan terms, or eliminating mortgage insurance.

Cash-out refinancing allows you to borrow against home equity, accessing funds for renovations, debt consolidation, or investment opportunities. Conventional programs permit cash-out refinancing up to 80% of current home value, though some lenders offer 85-90% LTV options with strong credit and compensating factors.

Seattle’s substantial home appreciation since 2020 has created significant equity for many homeowners, making cash-out refinancing an attractive option for those seeking liquidity without selling. A homeowner who purchased in Mill Creek for $450,000 in 2021 might now own a property worth $580,000, potentially accessing $100,000+ in equity while maintaining 20% ownership stake.

Working with Experienced Mortgage Professionals

Understanding conventional home loan programs requires expertise in current guidelines, market conditions, and strategic financing approaches. The complexity of qualification standards, pricing matrices, and property requirements makes professional guidance essential for optimal outcomes.

Experienced mortgage brokers maintain relationships with multiple lenders, creating competition for your business and access to diverse product offerings. This contrasts with retail bank loan officers limited to their employer’s programs and pricing. In Seattle’s competitive market, where timing and certainty matter tremendously, having an expert who can structure loans strategically and close efficiently provides meaningful advantages.

For professionals with complex compensation including stock grants, bonuses, and variable income, specialized expertise in documenting and qualifying non-traditional income sources becomes critical. The difference between qualifying at $250,000 versus $200,000 in annual income can represent $100,000+ in additional purchasing power.

Conventional home loan programs offer the flexibility, competitive pricing, and qualification pathways that make homeownership achievable for diverse borrower profiles across the Greater Seattle area. Understanding the nuances of credit requirements, down payment options, income documentation, and strategic structuring empowers you to make informed decisions aligned with your financial goals. Whether you’re purchasing your first home in Lynnwood, upgrading to a larger property in Seattle, or investing in rental real estate in Everett, working with a knowledgeable mortgage professional ensures you access the best conventional financing solutions available. Keith Akada at Mortgage Reel brings over 25 years of experience helping Seattle-area buyers and homeowners navigate conventional and jumbo loan programs with clarity, strategy, and execution that consistently earns five-star reviews from clients across the region.

Frequently Asked Questions

What are the benefits of using a mortgage broker over a bank loan officer?

Using a mortgage broker offers several advantages over a bank loan officer. Brokers have access to a wide range of lenders and mortgage products, allowing them to find the best rates and terms tailored to your specific needs. They can also negotiate on your behalf, creating competition among lenders. Additionally, brokers are often more knowledgeable about the nuances of various loan programs, which is especially beneficial for borrowers with complex financial situations, such as those with stock compensation or variable income.

How does the property type affect my mortgage options?

The type of property you intend to purchase significantly influences your mortgage options. Conventional loans can be used for single-family homes, condos, townhomes, and multi-unit properties (up to four units). However, each property type has specific eligibility criteria and appraisal standards. For instance, condos require additional scrutiny of the homeowners association’s financial health, while multi-unit properties may allow rental income to be counted toward qualifying income, enhancing your purchasing power.

What is the impact of a down payment on my mortgage?

Your down payment plays a crucial role in determining your mortgage terms, including interest rates and the requirement for private mortgage insurance (PMI). A larger down payment (20% or more) typically eliminates PMI, reducing your monthly payment. Conversely, smaller down payments (as low as 3% for first-time buyers) may require PMI, which adds to your costs. Additionally, a higher down payment can improve your loan-to-value ratio, potentially leading to better interest rates and terms.

What are the common pitfalls to avoid when applying for a conventional loan?

When applying for a conventional loan, it’s essential to avoid several common pitfalls. First, ensure your credit score is in good shape, as lower scores can lead to higher rates. Additionally, avoid making large purchases or taking on new debt before closing, as this can affect your debt-to-income ratio. Lastly, be thorough in documenting your income and assets, especially if you have non-traditional income sources, to prevent delays or complications in the approval process.

How can I improve my chances of getting approved for a conventional loan?

To improve your chances of approval for a conventional loan, focus on enhancing your credit score by paying down debts and making timely payments. Maintain a low debt-to-income ratio by managing your existing obligations and avoiding new debts. Additionally, save for a larger down payment to demonstrate financial stability and reduce lender risk. Finally, work with an experienced mortgage professional who can guide you through the process and help you present a strong application.

What should I know about refinancing a conventional loan?

Refinancing a conventional loan can be a strategic move to lower your interest rate, shorten your loan term, or access home equity. It’s essential to evaluate your current financial situation and market conditions to determine if refinancing is beneficial. Consider the costs associated with refinancing, such as closing costs and fees, and ensure that the potential savings outweigh these expenses. Additionally, be aware of the eligibility requirements and documentation needed for a successful refinance application.

What are the implications of using a cash-out refinance?

A cash-out refinance allows homeowners to borrow against their home equity, providing funds for various purposes like home improvements or debt consolidation. While this can be a useful financial tool, it’s important to understand the implications. You will be increasing your mortgage balance, which may lead to higher monthly payments. Additionally, if property values decline, you could owe more than your home is worth. Always assess your financial goals and consult with a mortgage professional before proceeding with a cash-out refinance.