Choosing the right mortgage can save you tens of thousands of dollars over the life of your loan. When you compare mortgage loans, you're not just looking at interest rates-you're evaluating total costs, monthly payments, loan terms, and how each option aligns with your financial goals. For homebuyers in Seattle and surrounding areas like Bellevue, Redmond, and Kirkland, understanding how to properly compare mortgage loans is essential in one of the nation's most competitive housing markets. This guide will walk you through the key factors, tools, and strategies you need to make an informed decision.

Understanding the Core Elements of Every Mortgage Loan

When you set out to compare mortgage loans, five fundamental components determine your total cost and monthly obligation. Each element plays a distinct role in shaping your financial commitment.

Interest rate represents the cost of borrowing money, expressed as a percentage. A lower rate means less interest paid over time, but the advertised rate doesn't tell the complete story. The annual percentage rate (APR) provides a more comprehensive view by including lender fees, discount points, and other closing costs, giving you a standardized way to compare mortgage loans from different lenders.

Loan term defines how long you'll make payments. Common terms include:

- 15-year fixed: Higher monthly payments, less total interest

- 30-year fixed: Lower monthly payments, more total interest

- Adjustable-rate mortgages (ARMs): Initial fixed period followed by rate adjustments

The loan amount you borrow directly impacts your monthly payment and total interest. Even small differences in principal can compound significantly over time. This is particularly relevant for Seattle tech professionals considering jumbo loans for higher-priced properties in neighborhoods like Capitol Hill or Queen Anne.

Down payment requirements vary by loan type. Conventional loans typically require 3-20%, while FHA loans accept as little as 3.5%. VA and USDA loans may offer zero-down options for qualified buyers. Your down payment percentage affects whether you'll pay private mortgage insurance (PMI), adding to your monthly costs.

How to Compare Different Mortgage Loan Types

Different loan programs serve different buyer profiles. Understanding these distinctions helps you compare mortgage loans more strategically.

Conventional Loans

Conventional loans aren't backed by government agencies. They offer flexibility and competitive rates for borrowers with strong credit (typically 620+) and sufficient down payment. For Seattle buyers in Shoreline or Lynnwood, conventional loans work well for standard home purchases within conforming loan limits.

Conforming loans follow limits set by Fannie Mae and Freddie Mac ($806,500 for single-family homes in most areas in 2026). Non-conforming or jumbo loans exceed these limits, common in high-cost areas like Seattle where median home prices regularly surpass $800,000.

Government-Backed Loans

FHA loans accommodate buyers with lower credit scores (as low as 580) and smaller down payments. They require mortgage insurance premiums both upfront and monthly, which increases total costs despite competitive interest rates.

VA loans serve eligible veterans, active-duty service members, and qualifying spouses. With no down payment requirement and no PMI, VA loans often provide exceptional value. Seattle has a significant veteran population, making this an important option for many buyers in Mill Creek and Lake Forest Park.

USDA loans support rural and suburban homebuyers with zero down payment in designated areas. While Seattle proper doesn't qualify, portions of Everett and surrounding regions may be eligible.

Adjustable-Rate Mortgages

ARMs offer lower initial rates than fixed mortgages, typically for 3, 5, 7, or 10 years before adjusting annually. When you compare mortgage loans, ARMs can make sense if you plan to sell or refinance before the adjustment period begins. Tech professionals on assignment in Seattle for limited timeframes often benefit from 5/1 or 7/1 ARM structures.

Key Comparison Metrics Beyond the Interest Rate

The advertised rate grabs attention, but comprehensive comparison requires examining several cost factors simultaneously.

| Comparison Factor | What It Reveals | Why It Matters |

|---|---|---|

| APR | True borrowing cost including fees | Allows apples-to-apples comparison |

| Monthly Payment | Principal, interest, taxes, insurance | Determines affordability |

| Total Interest Paid | Cumulative interest over loan life | Shows long-term cost impact |

| Closing Costs | Upfront fees to obtain the loan | Affects cash needed at closing |

| Break-Even Point | When refinance costs are recovered | Helps decide if refinancing makes sense |

Discount Points and Lender Credits

Discount points let you pay upfront fees to reduce your interest rate. One point equals 1% of the loan amount. For a $600,000 mortgage common in Redmond, one point costs $6,000. When you compare mortgage loans, calculate whether the monthly savings justify the upfront expense based on how long you plan to keep the loan.

Lender credits work in reverse-you accept a higher rate in exchange for reduced closing costs. This strategy works well if you're short on cash for closing or plan to refinance within a few years as rates change.

The Consumer Financial Protection Bureau’s guide to comparing loan estimates provides standardized worksheets to help you evaluate these trade-offs systematically.

Using Mortgage Comparison Calculators Effectively

Digital tools simplify the process when you compare mortgage loans side by side. Mortgage comparison calculators let you input different scenarios and instantly see how payments and total costs differ.

What to Input for Accurate Comparisons

- Loan amount: Your expected purchase price minus down payment

- Interest rate: The actual rate quoted, not the APR

- Loan term: 15-year, 30-year, or custom term

- Property taxes: Seattle's average effective rate is approximately 0.92%

- Homeowners insurance: Typically $1,200-$1,800 annually in the Seattle area

- HOA fees: If applicable to your property

- PMI: If putting less than 20% down on conventional loans

Running multiple scenarios helps you understand how small rate differences compound over time. For example, on a $700,000 mortgage-typical for a single-family home in Kirkland-a 0.25% rate difference creates approximately $100 monthly variance and $36,000 over 30 years.

Zillow’s loan comparison calculator allows you to evaluate up to three loans simultaneously, particularly useful when weighing conventional, FHA, and ARM options against each other.

Evaluating Lenders and Loan Officers

The lender you choose matters as much as the loan type. When you compare mortgage loans, evaluate the professionals and institutions behind them.

Questions to Ask Every Lender

- What is your current interest rate for my loan type and credit profile?

- What is the APR, and what fees does it include?

- Are there any lender fees you can reduce or waive?

- How long does your rate lock guarantee last?

- What documentation do you need, and what's your typical timeline to close?

- Do you service loans in-house or sell them?

Comparing Lender Types

Banks offer the security of established institutions and may provide relationship discounts if you have existing accounts. However, they sometimes have less flexibility with unique income situations.

Credit unions typically offer competitive rates for members and personalized service. Seattle-area credit unions serve specific employee groups and communities.

Mortgage brokers access multiple lenders, providing broader options and the ability to shop rates on your behalf. This is particularly valuable for tech professionals with complex income involving RSUs, stock options, and bonus structures that require specialized underwriting.

Online lenders streamline the application process and often feature lower overhead costs, translating to competitive rates. However, they may offer less personalized guidance through complex transactions.

Qualifying Income for Seattle Tech Professionals

Seattle's concentration of major tech employers creates unique mortgage scenarios. When you compare mortgage loans as a Microsoft, Amazon, or Google employee, understanding how lenders qualify stock-based compensation is critical.

How Lenders Evaluate RSUs and Stock Options

Restricted Stock Units (RSUs) can be counted as qualifying income if documented through:

- Two years of vesting history shown on W-2s or pay stubs

- Employer documentation of vesting schedules

- Evidence of continuity (RSUs will continue in future years)

Lenders typically average the past two years of RSU income and may apply a haircut or discount depending on stock volatility. For jumbo loans common in Seattle's competitive market, maximizing qualifying income through stock compensation can significantly increase buying power.

Stock options require different documentation and may be treated more conservatively, especially if unvested or subject to company performance metrics.

Bonuses need consistent two-year history to be counted, with lenders averaging the amounts received. Sign-on bonuses typically don't qualify as ongoing income.

Timing Your Rate Lock and Application

Interest rates fluctuate daily based on economic indicators, Federal Reserve policy, and market conditions. Recent mortgage rate trends show the importance of monitoring rate movements when you compare mortgage loans.

Rate Lock Strategies

A rate lock guarantees your quoted rate for a specified period, typically 30-60 days. Extended locks (90+ days) usually cost extra through higher rates or fees. In Seattle's fast-moving market, coordination between rate locks and closing timelines requires careful planning.

Float-down options let you lock a rate but capture a lower rate if the market improves before closing. These provisions come with specific requirements-often the rate must drop by at least 0.25% and you must be within a certain timeframe before closing.

Consider locking when:

- You've found your home and have an accepted offer

- Rates are at or near historical lows for your timeframe

- Economic indicators suggest rates may rise

- You're risk-averse and value payment certainty

Consider floating when:

- You're still house hunting without a contract

- Economic trends suggest rates may decrease

- You're comfortable with some uncertainty

- Your lender offers favorable float-down terms

Understanding Closing Costs and Cash to Close

When you compare mortgage loans, closing costs often represent the differentiator between seemingly similar offers. Total costs typically range from 2-5% of the loan amount.

Typical Closing Cost Categories

Lender fees include:

- Origination or underwriting fees

- Application fees

- Processing fees

- Rate lock fees

Third-party fees cover:

- Appraisal ($500-$800 in Seattle)

- Title insurance and title search

- Escrow and settlement fees

- Survey costs (if required)

- Credit report fees

Prepaid items and reserves include:

- Prepaid interest from closing to month-end

- Property tax reserves for escrow account

- Homeowners insurance reserves

- Initial escrow deposit

Government fees consist of:

- Recording fees

- Transfer taxes (varies by location)

Seattle buyers should be aware that Washington state doesn't have state income tax but does impose real estate excise tax on sellers, which doesn't directly affect your closing costs as a buyer but impacts overall transaction expenses.

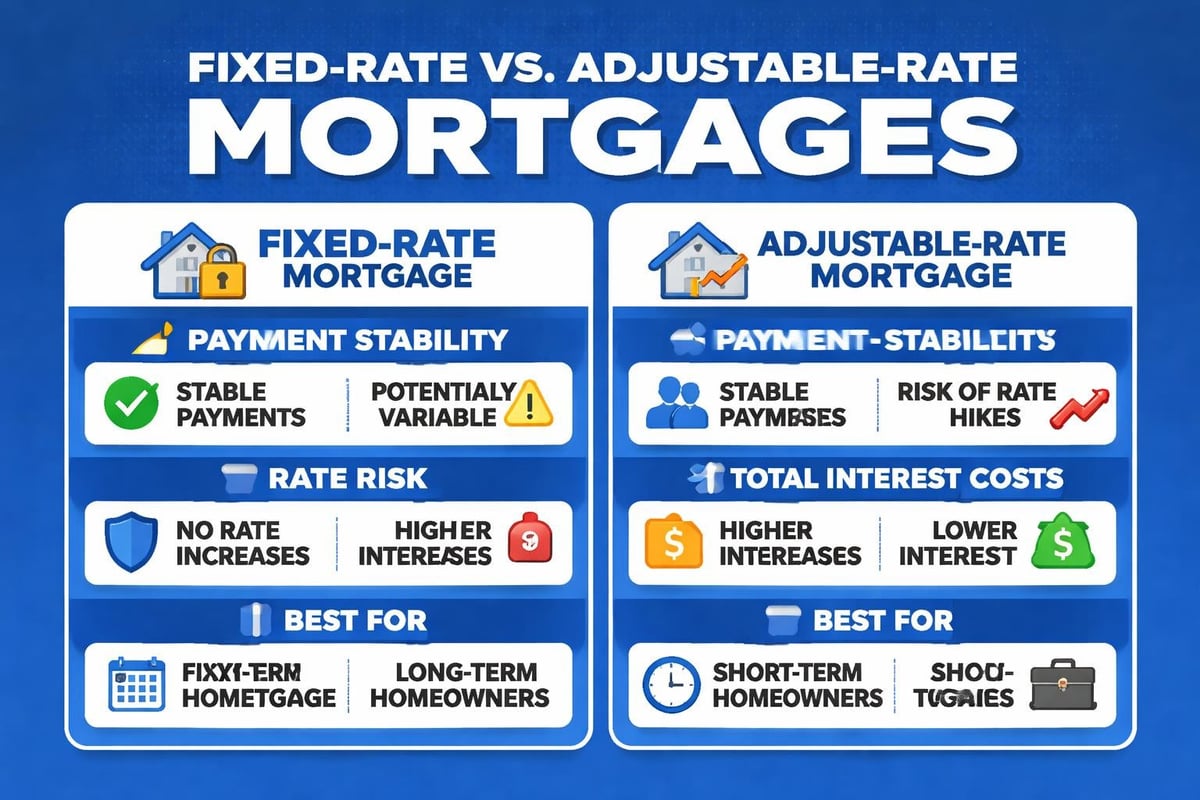

Comparing Fixed-Rate vs. Adjustable-Rate Mortgages

This decision significantly impacts your long-term financial planning. The right choice depends on your timeline, risk tolerance, and market outlook.

| Feature | 30-Year Fixed | 15-Year Fixed | 5/1 ARM | 7/1 ARM |

|---|---|---|---|---|

| Initial Rate | Higher | Lowest | Very Low | Low |

| Rate Stability | Lifetime | Lifetime | 5 years | 7 years |

| Monthly Payment | Lowest | Highest | Very Low Initially | Low Initially |

| Total Interest | Highest | Lowest | Variable | Variable |

| Best For | Long-term stability | Equity building | Short ownership | Medium-term plans |

When ARMs Make Sense

For Seattle professionals on temporary assignments or those planning to upgrade within 5-7 years, ARMs can provide significant savings. The initial rate discount (often 0.5-1.0% below fixed rates) translates to meaningful monthly savings.

Calculate your break-even point: if you'll sell or refinance before the ARM adjusts, you benefit from lower payments without exposure to rate increases. For a $750,000 loan in Bellevue, a 0.75% rate advantage saves approximately $400 monthly during the fixed period.

When Fixed Rates Provide Better Value

Fixed rates offer predictability in budgeting and protection against rising rates. If you plan to stay in your home for 10+ years or rates are historically low, locking in a fixed rate provides long-term security. Seattle's strong job market and quality of life encourage longer homeownership periods, making fixed rates popular among established residents in areas like Shoreline and Lake Forest Park.

Refinancing Considerations When Comparing Loans

Existing homeowners should periodically compare mortgage loans to determine if refinancing makes financial sense. The calculus involves current rates, closing costs, remaining loan term, and your future plans.

When to Consider Refinancing

- Rate reduction: General guideline suggests refinancing when you can reduce your rate by 0.75-1.0%, though smaller reductions may work depending on loan size and remaining term

- Loan term change: Switching from 30-year to 15-year to build equity faster

- Cash-out needs: Tapping equity for home improvements, debt consolidation, or investment opportunities

- PMI removal: Refinancing conventional loans after reaching 20% equity to eliminate mortgage insurance

Break-Even Analysis

Calculate how many months you need to recoup closing costs through monthly savings. If you're paying $3,000 in closing costs to save $150 monthly, your break-even point is 20 months. Plan to stay beyond that timeline to benefit from refinancing.

Tools like Freddie Mac’s loan comparison calculator help you model different refinancing scenarios to determine optimal timing and structure.

Common Mistakes When Comparing Mortgage Loans

Avoiding these pitfalls ensures you make decisions based on complete information rather than incomplete assumptions.

Focusing Exclusively on Interest Rate

While important, the interest rate alone doesn't capture total cost. A loan with a 6.5% rate and $2,000 in fees may cost less than a 6.375% loan with $5,000 in fees, depending on your timeframe. Always compare mortgage loans using APR as the equalizer.

Ignoring Your Actual Timeline

A 15-year mortgage saves tremendous interest compared to a 30-year loan, but only if you can afford the higher payments and plan to stay long enough to benefit. Similarly, paying points to reduce your rate only makes sense if you'll keep the loan past the break-even point.

Not Getting Multiple Quotes

Rate and fee structures vary significantly between lenders. Shopping with at least three lenders provides negotiating leverage and ensures you're getting competitive terms. Seattle's competitive lending market rewards borrowers who compare mortgage loans from multiple sources.

Overlooking Total Cash Requirements

Focus on both monthly affordability and cash needed at closing. A low-down-payment FHA loan may have higher long-term costs through mortgage insurance, but it gets you into homeownership sooner with less cash required upfront.

Neglecting Your Credit Score Impact

Your credit score dramatically affects your rate and available programs. Before you formally compare mortgage loans, check your credit and address any issues. Even small score improvements can translate to better terms. Generally:

- 760+: Best rates available

- 700-759: Excellent rates

- 660-699: Good rates

- 620-659: Higher rates, limited options

- Below 620: Difficult to qualify for conventional loans

Documentation and Preparation Strategies

Having your financial documentation organized accelerates the process when you're ready to compare mortgage loans and make formal applications.

Essential Documents to Gather

Income verification:

- Two years of W-2s

- Two years of tax returns (especially if self-employed)

- Recent pay stubs covering 30 days

- RSU vesting schedules and documentation

- Bonus and commission history

Asset documentation:

- Two months of bank statements for all accounts

- Investment account statements

- Retirement account balances (if using for down payment)

- Gift letters (if receiving down payment assistance from family)

Property and debt information:

- Purchase contract (once you have an accepted offer)

- HOA documents (if applicable)

- Current mortgage statement (for refinances)

- Student loan statements and payment verification

- Auto loan and credit card account information

For tech professionals in Seattle with complex compensation, additional documentation around equity compensation helps lenders accurately qualify your income and maximize your purchasing power.

Making Your Final Decision

After you thoroughly compare mortgage loans across multiple lenders, synthesize your findings into a comprehensive decision matrix.

Create a Comparison Spreadsheet

Track these elements for each loan option:

- Lender name and loan officer contact

- Loan type and term

- Interest rate and APR

- Monthly principal and interest payment

- Total monthly payment (including taxes, insurance, PMI)

- Closing costs itemized

- Cash needed at closing

- Total interest over loan life

- Break-even point (if applicable)

- Rate lock period

- Estimated closing timeline

Trust Your Analysis, Not Pressure

Quality loan officers educate and guide rather than pressure. If you feel rushed or confused, that's a red flag. The decision to commit to a 15-30 year financial obligation deserves careful consideration. Take time to review loan estimates, ask questions, and ensure you understand every term before proceeding.

Consider the Relationship, Not Just the Numbers

While rates and costs matter enormously, the loan officer's expertise, responsiveness, and ability to navigate challenges also creates value. In Seattle's competitive market where timing matters, having a professional who can close efficiently and communicate clearly with all parties can mean the difference between securing your dream home and losing it to another buyer.

Choosing the right mortgage requires evaluating multiple loan options, understanding how different terms affect your total costs, and working with experienced professionals who can guide you through the complexities. When you're ready to compare mortgage loans with expert guidance tailored to Seattle's unique market and tech industry compensation structures, Mortgage Reel offers the expertise, transparency, and proven track record to help you make confident decisions. Keith Akada brings over 25 years of experience and 750+ five-star reviews to every client relationship, specializing in qualifying complex income scenarios and closing loans quickly in competitive situations.