Purchasing your first home represents one of the most significant financial decisions you'll make, and securing the right first home buyers loan can determine whether your dream becomes reality. As a Seattle mortgage broker with 25+ years of experience, I've guided hundreds of first-time buyers through the complex landscape of loan programs, qualification requirements, and strategic financing decisions. The Greater Seattle housing market presents unique challenges, from competitive pricing in Bellevue and Redmond to emerging opportunities in Shoreline and Lynnwood. Understanding your loan options is the foundation of a successful purchase strategy.

Understanding First Home Buyers Loan Programs

A first home buyers loan isn't a single product but rather a category of mortgage programs designed with favorable terms for those entering homeownership for the first time. These programs typically feature lower down payment requirements, flexible credit guidelines, and sometimes reduced interest rates or assistance with closing costs.

Federal Loan Programs for First-Time Buyers

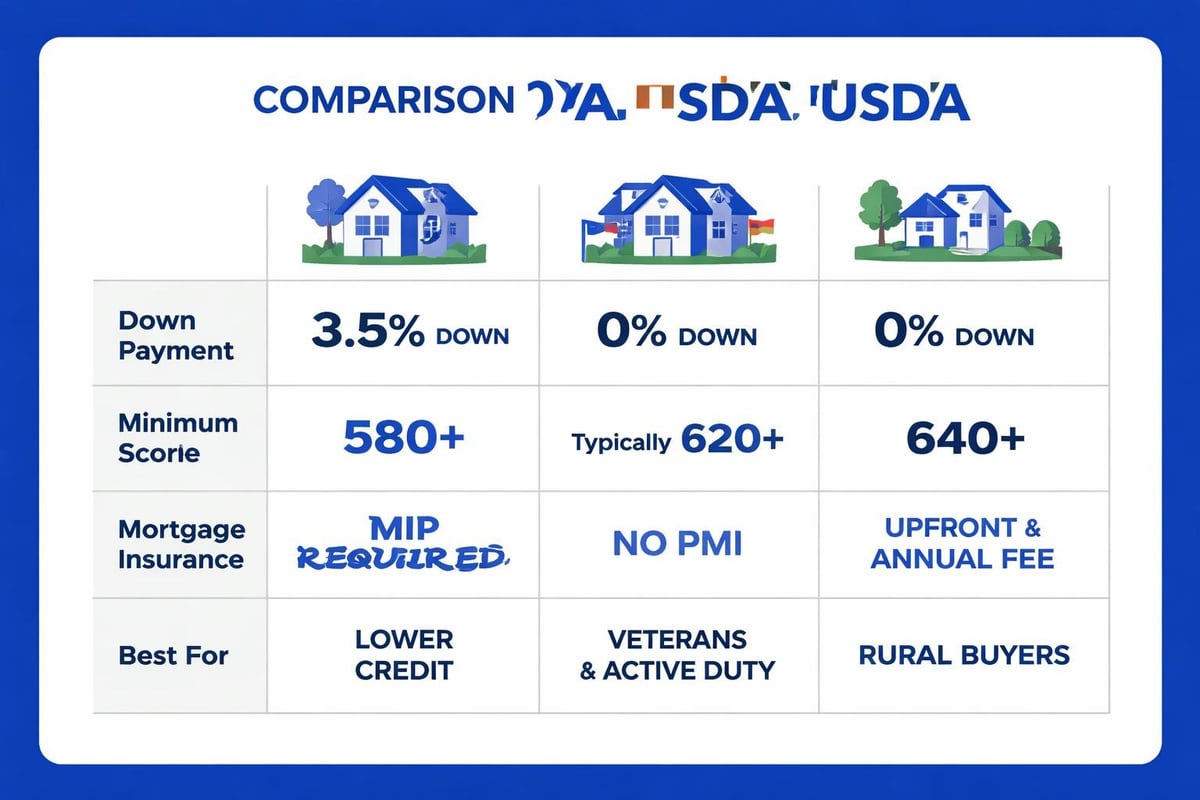

The federal government backs several mortgage programs specifically structured to help first-time buyers overcome traditional barriers to homeownership. FHA-insured loans remain the most popular choice, requiring as little as 3.5% down with credit scores as low as 580. These loans carry mortgage insurance throughout the loan's life if you put down less than 10%, but they provide accessible entry points for buyers with limited savings.

VA loans serve eligible veterans, active-duty service members, and qualifying spouses with zero down payment requirements and no mortgage insurance. For Seattle-area military families stationed at Joint Base Lewis-McChord or Naval Station Everett, this program delivers substantial savings over conventional financing.

USDA loans offer another zero-down option for properties in eligible rural and suburban areas. While Seattle proper doesn't qualify, portions of Mill Creek and areas beyond the immediate metro region may be eligible, making this worth exploring for buyers willing to commute.

Conventional First Home Buyers Loan Options

Conventional mortgages backed by Fannie Mae and Freddie Mac offer competitive alternatives with as little as 3% down through programs like HomeReady and Home Possible. These programs target low-to-moderate income buyers and include flexible underwriting for non-traditional income sources.

Why Choose Conventional Over Government Loans

Conventional loans provide several advantages that make them attractive despite slightly stricter qualification requirements:

- Lower total costs when you have good credit (typically 680+)

- Cancellable mortgage insurance once you reach 20% equity

- Higher loan limits ($806,500 for single-family homes in King County for 2026)

- Faster processing in competitive markets where speed matters

For tech professionals in Seattle, Bellevue, or Redmond earning strong base salaries plus RSUs or stock compensation, conventional financing often delivers better long-term value than FHA loans. I regularly help Amazon and Microsoft employees maximize their buying power by properly documenting equity compensation according to underwriting guidelines.

| Loan Type | Minimum Down Payment | Credit Score Minimum | Mortgage Insurance | Best For |

|---|---|---|---|---|

| FHA | 3.5% | 580 | Required (permanent if under 10% down) | Lower credit, smaller down payment |

| Conventional 3% | 3% | 620 | Cancellable at 20% equity | Good credit, limited savings |

| VA | 0% | No minimum (typically 620+) | None | Veterans and military |

| USDA | 0% | 640 | Required | Eligible rural/suburban areas |

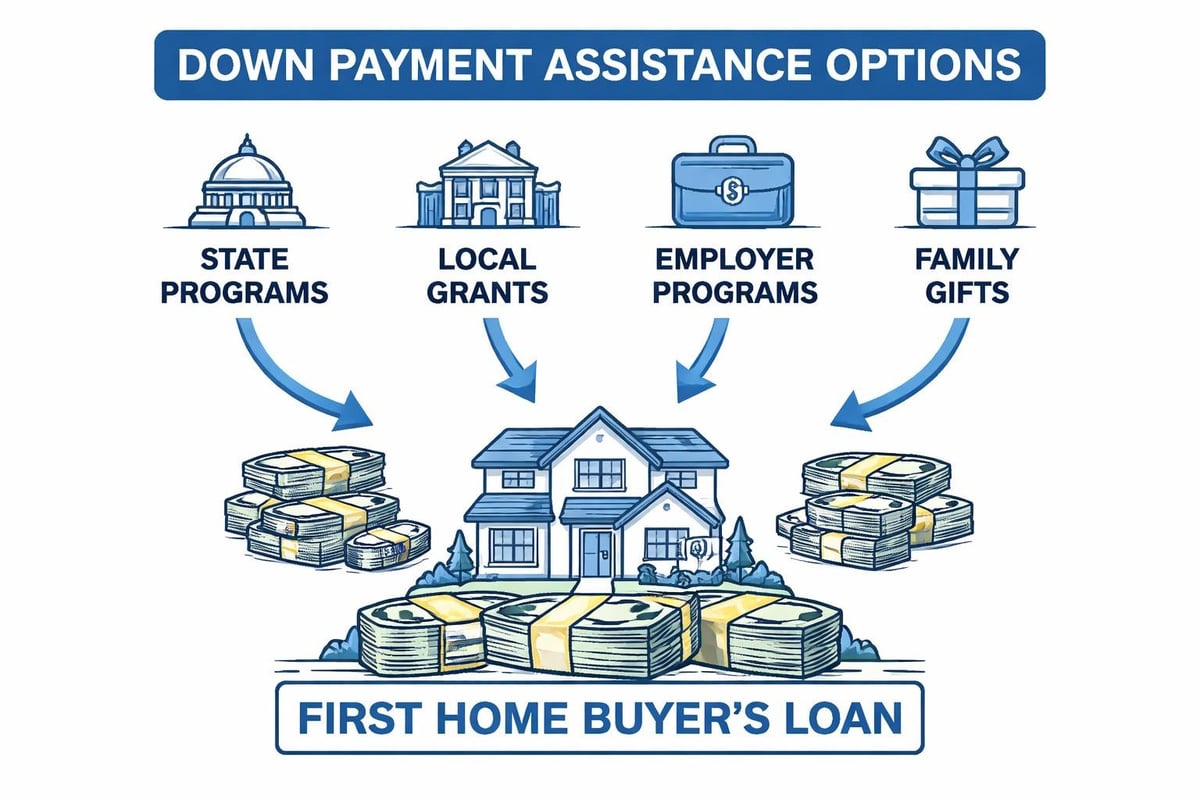

Down Payment Assistance for First Home Buyers

The down payment remains the largest obstacle for most first-time buyers. In the Seattle metro area, where median home prices exceed $650,000, even a 3% down payment represents nearly $20,000 before accounting for closing costs.

Washington State Housing Finance Commission Programs

Washington State offers robust down payment assistance through the Housing Finance Commission. Their House Key program provides competitive interest rates combined with down payment assistance options. In 2026, eligible buyers can access:

- Down payment assistance up to 5% of the purchase price

- Competitive fixed-rate mortgages

- Reduced mortgage insurance costs

- Homebuyer education resources

These programs carry income limits that vary by county. King County limits differ from Snohomish County, so buyers shopping in Lynnwood or Everett may find more flexibility than those focused exclusively on Seattle neighborhoods.

City and County Assistance Programs

Seattle's Office of Housing periodically offers down payment assistance to qualified buyers purchasing in specific neighborhoods. These programs often prioritize workforce housing and may require buyers to work in Seattle or meet income thresholds tied to Area Median Income (AMI).

Various first-time homebuyer programs throughout Washington provide grants, forgivable loans, and deferred-payment second mortgages that dramatically reduce the cash needed at closing.

Qualifying for Your First Home Buyers Loan

Understanding qualification requirements helps you position yourself as a strong borrower and avoid surprises during the application process. Lenders evaluate four primary factors when reviewing your first home buyers loan application.

Credit Requirements Across Programs

Credit scores determine both loan eligibility and your interest rate. While FHA loans accept scores as low as 580 for 3.5% down (or 500-579 for 10% down), conventional loans typically require 620 minimum. For the best rates on any program, aim for 740 or higher.

I recommend pulling your credit report at least six months before starting your home search. This timeline allows you to dispute errors, pay down balances, and avoid new credit inquiries that could lower your score. Even small improvements in credit score can save thousands over the life of your loan.

Debt-to-Income Ratio Calculations

Lenders calculate your debt-to-income (DTI) ratio by dividing total monthly debt payments by gross monthly income. Most programs allow DTI ratios up to 43-50%, though lower ratios strengthen your application and may qualify you for better terms.

Front-end ratio includes only housing costs (principal, interest, taxes, insurance, HOA fees). Back-end ratio adds all monthly debt obligations including student loans, car payments, and minimum credit card payments.

For Lake Forest Park buyers earning $120,000 annually with $800 in monthly debt, a $2,800 mortgage payment would create a back-end DTI of 36% ($3,600 total debt / $10,000 monthly income), well within acceptable limits.

Income Documentation Standards

Traditional W-2 employment requires two years of job history in the same field, recent pay stubs, and tax returns. Self-employed buyers need two years of tax returns showing consistent or increasing income, though some programs allow one-year documentation for established businesses.

Tech employees with RSUs, stock options, or performance bonuses require special attention to income calculation. Underwriters typically average two years of variable compensation and may discount or exclude certain components. Properly documenting and presenting this compensation determines whether you qualify for a $700,000 home versus $900,000 in competitive Seattle neighborhoods.

Strategic Considerations for Seattle-Area Buyers

The Greater Seattle real estate market requires specific strategies that differ from national averages. Our median prices, competitive offer situations, and rapid appreciation create unique opportunities and challenges for first-time buyers.

Pre-Approval Strength in Multiple Offer Situations

In markets like Redmond or Bellevue where quality listings regularly receive 5-10 offers, your financing strength directly impacts seller decisions. A pre-approval letter from a local lender with quick closing capabilities often outweighs offers with slightly higher prices but uncertain financing.

I work extensively with Seattle-area buyers to structure pre-approvals that stand out:

- Full underwriting review beyond basic qualification

- Verified documentation rather than stated income

- Lender reputation known to local agents and sellers

- Accelerated closing timelines as fast as 9 business days

Choosing the Right First Home Buyers Loan for Your Timeline

Your purchase timeline should influence loan program selection. FHA loans typically take 30-45 days to close due to appraisal requirements and property condition standards. Conventional loans often close faster, particularly when underwriting is complete before offer acceptance.

Buyers targeting competitive neighborhoods in Shoreline or Mill Creek benefit from conventional financing when possible. The ability to waive financing contingencies or offer shorter contingency periods provides significant competitive advantage.

Understanding Total Cost Beyond Monthly Payment

Many first-time buyers focus exclusively on monthly payment affordability while overlooking total ownership costs. Your first home buyers loan structures these costs differently depending on program choice.

Compare two scenarios for a $600,000 purchase in Everett:

FHA Scenario: 3.5% down ($21,000), 6.5% rate, $3,578 monthly payment including upfront and monthly mortgage insurance

Conventional Scenario: 5% down ($30,000), 6.375% rate, $3,512 monthly payment including mortgage insurance

The conventional loan requires $9,000 more upfront but costs $66 less monthly. After 24 months at 20% equity, you can cancel PMI, reducing the payment to approximately $3,100. The FHA mortgage insurance remains for the loan's life unless you refinance.

Common First Home Buyers Loan Mistakes to Avoid

Experience shows certain mistakes appear repeatedly among first-time buyers, often derailing purchases or creating financial stress after closing.

Mistake 1: Maxing Out Your Qualification

Just because you qualify for a $4,000 monthly payment doesn't mean you should commit to that amount. Life circumstances change, and maintaining financial flexibility protects against job changes, family expansion, or unexpected expenses. I generally recommend keeping housing costs below 30% of gross income when possible.

Mistake 2: Ignoring Property Type Restrictions

Not all loan programs finance all property types equally. Condos require specific certifications for FHA and conventional financing. Properties needing significant repairs may not qualify for traditional programs, forcing you toward renovation loans with different requirements.

Mistake 3: Making Large Purchases Before Closing

Opening new credit cards, financing furniture, or buying vehicles between pre-approval and closing changes your debt-to-income ratio and credit profile. I've seen transactions collapse days before closing because buyers purchased cars or furniture on credit, pushing DTI beyond acceptable limits.

Mistake 4: Skipping Professional Guidance

First-time homebuyer resources provide valuable information, but generic advice can't replace personalized strategy based on your specific income, credit, and goals. Working with experienced local professionals who understand Seattle-area market dynamics protects your interests and streamlines the process.

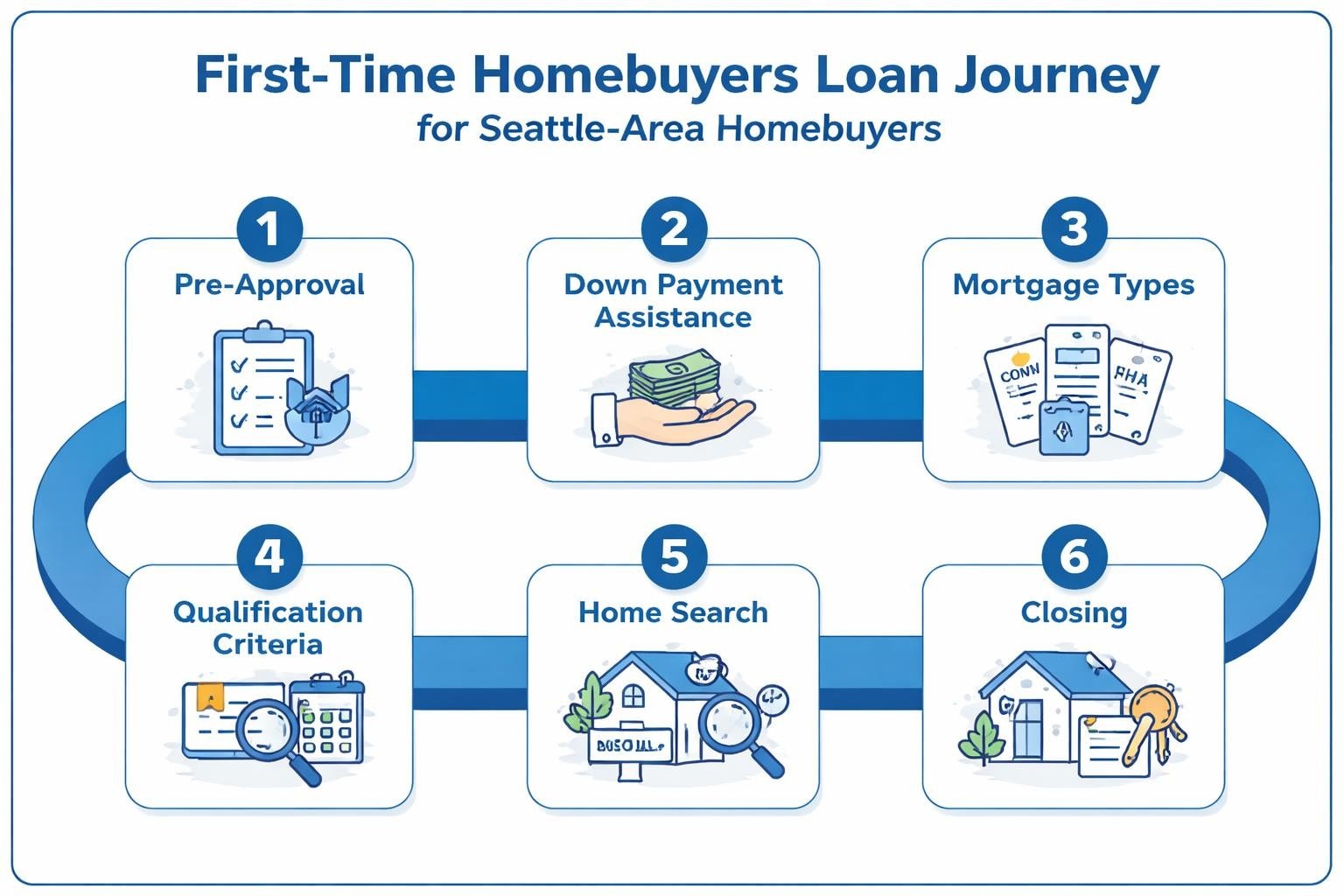

How to Start Your First Home Buyers Loan Process

Beginning your homeownership journey with proper preparation increases success rates and reduces stress throughout the transaction.

Step 1: Assess Your Financial Position

Review your complete financial picture including credit scores, savings, income stability, and existing debts. Calculate realistic monthly payments you can afford long-term, accounting for property taxes, insurance, and maintenance costs that accompany homeownership.

For Seattle-area buyers, remember that King County property taxes average 0.93% of assessed value annually. A $650,000 home generates roughly $6,045 in annual property taxes, or approximately $504 monthly on top of your mortgage payment.

Step 2: Get Pre-Approved Early

Connect with a mortgage broker 3-6 months before you plan to make offers. This timeline allows you to address any credit issues, understand exactly how much home you can afford, and position yourself as a serious buyer when you find the right property.

Quality pre-approval includes:

- Credit report review and score verification

- Income and employment confirmation

- Asset documentation for down payment and reserves

- Debt obligation verification

- Property type and location discussion

Step 3: Understand Your Loan Options

Meet with your loan officer to review available first home buyers loan programs based on your specific situation. Compare FHA, conventional, VA (if eligible), and state assistance programs. Understand the trade-offs between down payment size, interest rates, and ongoing costs like mortgage insurance.

Step 4: Determine Your Down Payment Strategy

Decide whether to maximize down payment size or preserve cash reserves for post-closing needs. Consider combining your savings with down payment assistance programs, family gifts, or employer homebuying benefits available to many Seattle tech workers.

Step 5: Budget for Additional Costs

Beyond down payment and monthly mortgage payments, budget for closing costs (2-5% of purchase price), moving expenses, immediate home improvements, and emergency reserves for unexpected repairs. First-time buyers often underestimate these costs, creating financial stress immediately after purchase.

Navigating Seattle's Unique Market Conditions

The Greater Seattle housing market presents specific considerations that influence first home buyers loan strategy and property selection.

Price Ranges Across Metro Submarkets

Understanding realistic price points helps focus your search and financing approach. As of 2026, median home prices vary significantly across the region:

- Seattle proper: $780,000-$850,000 depending on neighborhood

- Bellevue/Redmond: $950,000-$1,100,000 for single-family homes

- Shoreline/Lake Forest Park: $690,000-$780,000

- Lynnwood/Mill Creek: $620,000-$710,000

- Everett: $550,000-$640,000

These price points directly impact the type of first home buyers loan that makes sense. Bellevue buyers often need jumbo financing above conforming limits, while Everett buyers can maximize conventional or FHA programs with standard limits.

Condominium Considerations for Urban Buyers

Seattle's urban core offers numerous condominium options at lower price points than single-family homes. Condos require additional financing scrutiny including homeowners association certification, project approval, and reserve fund requirements.

FHA maintains strict condo certification requirements that many Seattle buildings don't meet. Conventional financing offers more flexibility with condo purchases, though rates may be slightly higher and down payment requirements can increase for smaller units or buildings with significant renter occupancy.

Maximizing Tech Compensation for Qualification

Seattle's concentration of major technology employers creates unique income documentation opportunities that many lenders don't fully understand or utilize.

RSU and Stock Compensation Treatment

Restricted stock units (RSUs) from employers like Amazon, Microsoft, or Google can substantially increase your purchasing power when properly documented. Underwriters typically require two years of RSU income and calculate qualifying income using either the average or the lowest year, depending on trends.

For a Microsoft employee earning $150,000 base salary plus $80,000 in annual RSU vesting, proper documentation might qualify them based on $220,000-$230,000 total income rather than just base salary. This difference translates to roughly $100,000-$150,000 additional purchasing power.

Bonus and Commission Income

Regular performance bonuses, sales commissions, and profit-sharing require two-year history and demonstrated continuity. Some underwriters discount bonuses by 25-50% if they're discretionary, while others average them fully if they're consistent and contractually outlined.

Navigating Job Changes in Tech

Technology sector professionals frequently change employers for career advancement. Recent job changes don't automatically disqualify you if you remain in the same field with comparable or increased compensation. Documentation requirements increase, but experienced underwriting teams can structure approvals for recently-transitioned professionals.

Interest Rate Strategies for First-Time Buyers

Interest rates significantly impact both monthly affordability and total loan cost over time. Understanding rate fundamentals helps you make informed decisions about timing and loan structure.

Fixed vs. Adjustable Rate Mortgages

Most first home buyers loan applications utilize fixed-rate mortgages for payment stability and predictability. Thirty-year fixed rates remain the standard, though 15-year and 20-year options exist for buyers prioritizing equity building and total interest savings.

Adjustable-rate mortgages (ARMs) offer lower initial rates, typically fixed for 5, 7, or 10 years before annual adjustments. In early 2026, 7-year ARMs might price 0.50-0.75% below 30-year fixed rates. For buyers confident they'll move or refinance within the fixed period, ARMs can reduce costs substantially.

Rate Lock Timing and Market Monitoring

Rate locks guarantee your interest rate for a specific period (typically 30-60 days). In stable or rising rate environments, lock immediately upon application. In declining markets, consider shorter locks or float strategies with your loan officer.

Seattle's strong economy and steady housing demand creates relative rate stability compared to markets with higher volatility. Still, Federal Reserve policy changes, inflation trends, and broader economic conditions can shift rates meaningfully within weeks.

Points and Rate Buydown Strategies

Paying discount points (prepaid interest equal to 1% of loan amount per point) reduces your interest rate by approximately 0.25% per point. Calculate your break-even timeline by dividing the point cost by monthly payment savings.

For buyers planning to stay long-term in their first home, points can deliver substantial savings. For those likely to move or refinance within 3-5 years, paying points rarely makes financial sense.

Building Wealth Through Strategic First Home Purchases

Your first home purchase establishes the foundation for long-term wealth building through equity accumulation, forced savings discipline, and potential appreciation in strong markets like Greater Seattle.

Equity Building Through Principal Reduction

Each mortgage payment includes both interest and principal. Early payments are interest-heavy, but over time, principal portions increase. A $500,000 loan at 6.5% builds approximately $60,000 in principal equity over the first five years through scheduled payments alone.

Appreciation Potential in Seattle Submarkets

Historical appreciation varies by location, but Seattle-area homes have generally appreciated 4-7% annually over the past decade. Emerging neighborhoods in Shoreline or Mill Creek sometimes outpace established areas during growth cycles, while premium locations like Bellevue show steadier but consistent appreciation.

Your first home buyers loan doesn't just provide shelter-it creates a leveraged investment where modest appreciation on a large asset value generates substantial wealth. A $600,000 home appreciating 5% annually gains $30,000 in value that first year, representing a 100%+ return on a $21,000 FHA down payment.

Tax Benefits of Homeownership

The tax code provides several benefits to homeowners that effectively reduce ownership costs compared to renting.

Mortgage Interest Deduction

You can deduct mortgage interest on loans up to $750,000 for married couples filing jointly ($375,000 single). For a $600,000 mortgage at 6.5%, first-year interest approximates $38,700. At a 24% marginal tax rate, this deduction saves roughly $9,288 annually in federal taxes.

State income tax deductions (Washington has no state income tax) and property tax deductions (capped at $10,000 total for state and local taxes) provide additional benefits depending on your situation.

Long-Term Capital Gains Exclusion

When you eventually sell your home, single filers can exclude $250,000 in capital gains from taxation ($500,000 for married couples filing jointly), provided you've lived in the home as your primary residence for at least two of the previous five years. This exclusion represents one of the most powerful tax benefits in the code for building tax-free wealth.

Taking Action on Your First Home Purchase

Success in Seattle's competitive market requires preparation, professional guidance, and clear strategy. Understanding first home buyers loan options provides the foundation, but execution determines results.

Start by assessing your complete financial picture and connecting with experienced local professionals who understand both mortgage products and Greater Seattle market dynamics. Get pre-approved before shopping to strengthen your negotiating position and identify any issues requiring attention.

Research neighborhoods across the metro area to find the right balance of affordability, lifestyle fit, and long-term value. Consider expanding your search to areas like Lynnwood, Mill Creek, or Everett where your first home buyers loan dollars stretch further while maintaining access to Seattle employment centers.

Most importantly, view your first home purchase as a long-term wealth-building strategy rather than a perfect forever home. Many buyers outgrow their first property within 5-10 years, using accumulated equity as a springboard to their next home. Starting somewhere beats waiting for perfect conditions that may never materialize.

Securing the right first home buyers loan sets the foundation for successful homeownership and long-term wealth building in the Greater Seattle area. Whether you're targeting Seattle neighborhoods, exploring opportunities in Shoreline, or maximizing value in emerging markets like Lynnwood and Everett, having experienced guidance makes the difference between stress and confidence throughout your purchase journey. Keith Akada has helped hundreds of first-time buyers navigate these decisions with 25+ years of proven expertise in complex income documentation, competitive offer strategies, and program selection tailored to individual circumstances. If you're ready to explore your options and develop a customized strategy for your first home purchase, connect with Mortgage Reel to get started with a trusted Seattle mortgage broker who prioritizes education, transparency, and results.