Searching for "mortgage agents near me" starts with understanding what you actually need from a lending professional. Whether you're purchasing your first home in Seattle or refinancing in Shoreline, the right mortgage agent helps you navigate complex loan programs, qualify income sources accurately, and close on time. In 2026, homebuyers across the Greater Seattle area face unique challenges including elevated interest rates, competitive inventory in neighborhoods from Lynnwood to Everett, and evolving underwriting requirements for stock compensation. Finding a local mortgage professional who understands these regional dynamics and can structure loans around your specific financial profile makes the difference between a smooth transaction and a frustrating experience.

What Mortgage Agents Actually Do

Mortgage agents work as intermediaries between borrowers and lenders, accessing multiple loan products across various financial institutions. Unlike loan officers employed by a single bank, agents typically maintain relationships with numerous wholesale lenders, providing clients with broader options.

The Core Services You Should Expect

Professional mortgage agents perform several critical functions throughout your transaction. They analyze your financial profile including income documentation, credit history, and debt obligations to determine realistic loan amounts. They compare rate sheets from multiple lenders to identify competitive pricing. They manage the application process from pre-approval through closing, coordinating with underwriters, processors, title companies, and real estate agents.

Key responsibilities include:

- Pre-qualifying borrowers before house hunting begins

- Structuring loan scenarios around complex income sources

- Locking interest rates at optimal timing

- Troubleshooting underwriting conditions and documentation requests

- Delivering clear closing cost breakdowns with no hidden fees

For tech professionals in Seattle working at Amazon, Microsoft, or Google, specialized agents understand how to qualify RSUs, stock options, and variable bonus income. This expertise directly impacts your purchasing power in high-cost markets like Bellevue and Redmond.

Mortgage Brokers vs Direct Lenders: Understanding the Difference

When searching for mortgage agents near me, you'll encounter both brokers and direct lenders. The distinction affects your loan options, pricing transparency, and service experience.

Mortgage Brokers

Brokers access wholesale lending channels from multiple institutions. They don't fund loans themselves but originate applications and submit them to partner lenders. This model creates competition among lenders for your business, potentially lowering costs.

| Broker Advantages | Broker Considerations |

|---|---|

| Multiple lender options in one conversation | Must verify broker credentials and licensing |

| Wholesale pricing often beats retail rates | Service quality varies significantly by broker |

| Flexibility for complex income scenarios | Some lenders not available through broker channels |

| One application accesses many products | Broker compensation models vary |

Direct Lenders

Banks and mortgage companies that underwrite and fund loans in-house operate as direct lenders. You work with their employed loan officers who only offer that institution's products.

The Better Business Bureau provides guidance on choosing mortgage lenders versus brokers, emphasizing the importance of understanding compensation structures and comparing total costs.

Direct lenders control their underwriting timelines and may offer relationship benefits if you have existing accounts. However, you're limited to their specific loan programs and pricing.

How to Find Quality Mortgage Agents in Seattle

Location matters more than many borrowers realize. Mortgage agents familiar with Seattle's housing market understand local property tax structures, HOA dynamics in condominiums, and neighborhood valuation trends that affect appraisals.

Start with Referrals from Trusted Sources

Real estate agents who close numerous transactions annually develop working relationships with reliable mortgage professionals. They observe which loan officers communicate proactively, meet deadlines, and solve problems efficiently.

Ask your real estate agent these specific questions:

- Which mortgage agents do you trust in competitive multiple-offer situations?

- Who has successfully closed transactions with buyers in my price range?

- Which professionals communicate clearly with first-time buyers?

Friends, family members, and colleagues who recently purchased homes in Lynnwood, Lake Forest Park, or Mill Creek can provide candid feedback about their mortgage agent's performance under real conditions.

Verify Credentials and Standing

All mortgage loan originators must hold valid licenses through the Nationwide Multistate Licensing System (NMLS). You can verify any agent's license status, employment history, and disciplinary actions through the NMLS Consumer Access website.

The BBB’s directory of accredited mortgage brokers offers additional insights into business practices and customer complaint history.

Check online reviews across multiple platforms including Google, Zillow, and Redfin. Look for patterns in feedback rather than isolated comments. Consistent themes around communication quality, timeline adherence, and problem-solving capability indicate reliable service.

Interview Multiple Agents Before Committing

Schedule consultations with at least three mortgage agents. Prepare identical questions for each to enable direct comparison.

Essential interview questions:

- How many loans do you personally close each month?

- What percentage of your applications receive final approval?

- Which lenders do you work with regularly?

- How do you handle rate locks and timing strategy?

- Can you provide references from recent clients?

- What is your typical timeline from application to closing?

Pay attention to how agents explain complex topics. The best professionals translate mortgage terminology into understandable concepts without condescension.

Loan Programs Your Mortgage Agent Should Understand

Comprehensive mortgage agents near me offer access to diverse loan products suited to different financial situations and property types. Understanding available programs helps you evaluate whether an agent can truly serve your needs.

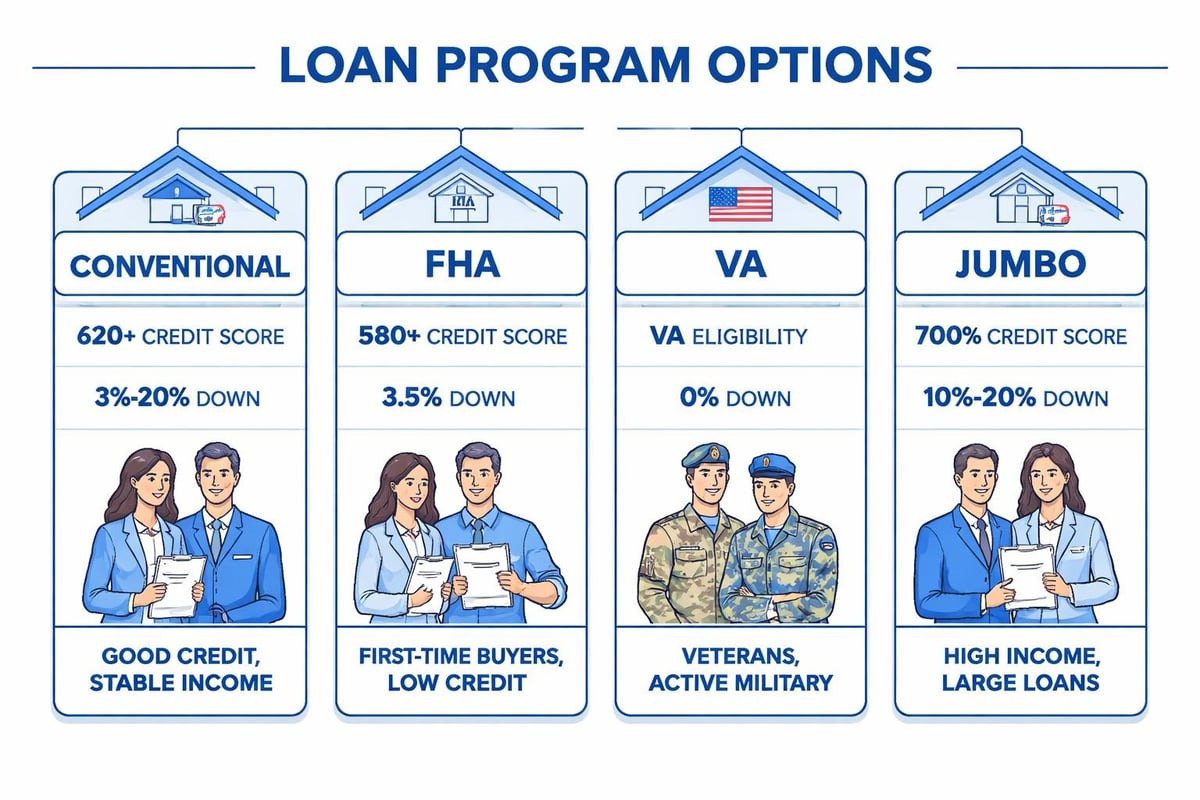

Conventional Loans

These conforming loans follow guidelines established by Fannie Mae and Freddie Mac. They require minimum credit scores typically above 620 and down payments as low as 3% for first-time buyers.

Conventional loans work well for borrowers with stable employment, documented income, and moderate debt-to-income ratios. In Seattle's high-cost market, conforming loan limits for 2026 allow borrowing up to $806,500 for single-family homes, though these limits adjust annually.

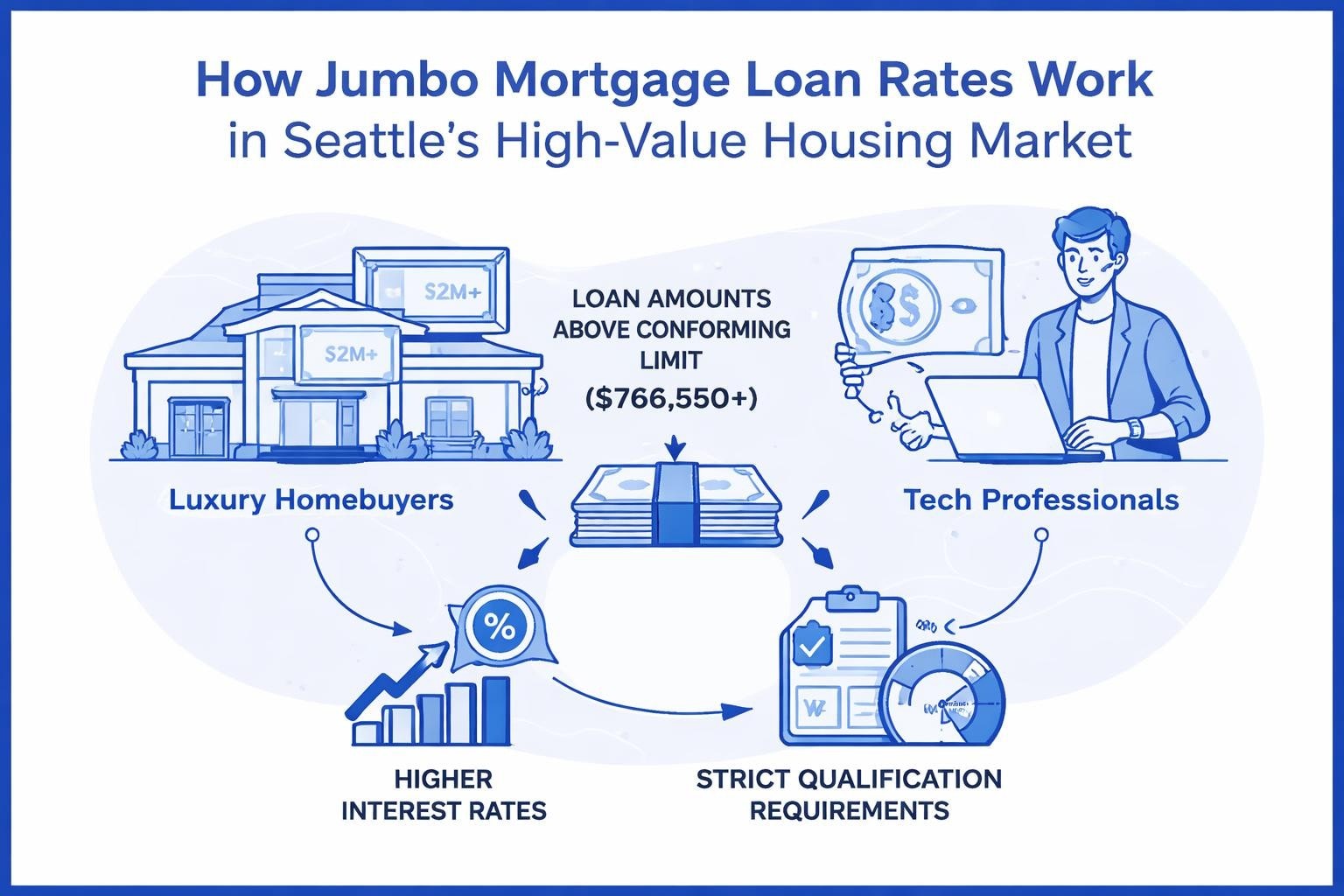

Jumbo Loans for Seattle's Premium Markets

Properties exceeding conforming loan limits require jumbo financing. In neighborhoods throughout Seattle, Bellevue, and Redmond where median home prices frequently surpass $1 million, jumbo loan expertise becomes essential.

Jumbo loans demand stronger financial profiles including higher credit scores (typically 700+), larger down payments (often 10-20%), and substantial cash reserves. Experienced agents structure these applications to highlight borrower strengths and mitigate perceived risks.

For professionals with significant stock compensation, agents must understand how underwriters evaluate RSUs, stock options, and variable bonuses when calculating qualifying income for jumbo loans.

Government-Backed Programs

FHA loans serve buyers with lower credit scores or smaller down payments. VA loans provide exceptional benefits for eligible service members and veterans including zero down payment options and no mortgage insurance requirements.

USDA loans support rural property purchases, though they have limited applicability in metropolitan Seattle. Some outer areas of Mill Creek or Everett might qualify depending on specific location definitions.

Specialized Programs for Unique Situations

Bank Statement Loans accommodate self-employed borrowers or business owners who show significant tax write-offs that reduce documented income. Rather than tax returns, these programs analyze bank deposits to determine cash flow.

Non-QM (Non-Qualified Mortgage) loans provide flexibility for borrowers with recent credit events, alternative income documentation, or investment property portfolios exceeding conventional guidelines.

Key Factors When Comparing Mortgage Agents

Beyond basic licensing and product access, several differentiating factors separate exceptional mortgage agents from average ones. Understanding these distinctions helps you select the right professional.

Communication Standards and Responsiveness

Mortgage transactions involve tight timelines, especially in competitive markets. Agents who respond to calls and emails within hours rather than days prevent delays that could jeopardize your contract.

Ask how agents prefer to communicate and what response times you should expect. Clarify who handles your file when your primary agent is unavailable.

Technology and Process Efficiency

Modern mortgage platforms enable digital document uploads, electronic signatures, and real-time application status tracking. Agents utilizing current technology streamline your experience and reduce closing timelines.

Some brokers can close loans in as few as 9 business days when borrowers provide documentation promptly and properties appraise without complications. This speed matters significantly when competing against cash offers or working with sellers who need quick closings.

Fee Transparency and Cost Structures

Request detailed Loan Estimates from each agent during your comparison process. These standardized forms break down all costs including origination fees, third-party services, prepaid items, and lender credits.

| Fee Category | What to Compare |

|---|---|

| Origination Charges | Percentage of loan amount or flat fees |

| Discount Points | Optional upfront costs to reduce rate |

| Third-Party Services | Appraisal, title, escrow fees |

| Prepaid Items | Property taxes, insurance, interest |

| Lender Credits | Rate adjustments that offset costs |

The Consumer Financial Protection Bureau provides resources explaining how to evaluate costs and understand your rights during the mortgage process.

Some agents quote attractively low rates but add excessive origination fees or junk charges. Others offer genuine competitive pricing across all cost categories. Total cost comparison over your expected holding period matters more than initial rate alone.

What Seattle Homebuyers Should Ask Mortgage Agents

Regional market knowledge separates local experts from generic loan officers. Mortgage agents serving the Greater Seattle area should understand specific challenges affecting transactions here.

Questions About Local Market Expertise

- How do you help buyers compete in multiple-offer situations common in Shoreline and Lake Forest Park?

- What appraisal challenges have you seen in Seattle neighborhoods recently?

- How do you structure pre-approvals to strengthen offers without over-committing buyers?

- Which inspection contingency timeframes work best with current seller expectations?

Agents familiar with Seattle's market dynamics provide strategic guidance that extends beyond simple loan qualification.

Questions for Tech Industry Professionals

If you work in Seattle's technology sector, your compensation likely includes equity components requiring specialized understanding.

Ask potential agents:

- How do you calculate qualifying income from RSUs that vest over multiple years?

- Which underwriters accept stock compensation most favorably?

- How do you document bonus income for employees with limited employment history at current companies?

- What cash reserve requirements apply when stock assets comprise significant net worth?

Mortgage Reel’s expertise in qualifying complex compensation packages for Amazon, Microsoft, and Google employees demonstrates this specialized knowledge.

Questions About Rate Lock Strategy

Interest rates fluctuate daily. Your agent's approach to rate locks affects your final cost significantly.

Understand how long lock periods last, whether extensions are available, and what happens if rates drop after locking. Some lenders offer float-down options providing protection against rate increases while preserving the ability to capture decreases.

Red Flags When Evaluating Mortgage Agents

Certain warning signs indicate you should continue your search rather than commit to a particular agent.

Avoid agents who:

- Guarantee loan approval before reviewing your complete financial profile

- Pressure you to lock rates immediately without explanation

- Refuse to provide written fee estimates

- Cannot explain how they're compensated

- Promise unrealistic closing timelines

- Discourage you from comparison shopping

- Use high-pressure sales tactics

Professional mortgage agents welcome questions, provide transparent answers, and encourage informed decision-making. They succeed through referrals and repeat business, not through manipulating uninformed borrowers.

Working Effectively with Your Mortgage Agent

Once you select a mortgage agent, your collaboration determines transaction success. Understanding your role and responsibilities helps the process flow smoothly.

Documentation Requirements and Organization

Gather financial documents before formally applying. Standard requirements include:

- Two years of W-2 forms and tax returns

- Recent paystubs covering 30 days

- Two months of bank statements for all accounts

- Retirement account statements if using for down payment

- Documentation for additional income sources

- Explanation letters for credit inquiries or unusual deposits

For self-employed borrowers or those with rental properties, expect additional documentation including business tax returns, profit and loss statements, and lease agreements.

Maintaining Financial Stability During Processing

Avoid major financial changes between application and closing. Don't change jobs, open new credit accounts, make large purchases, or transfer money between accounts without informing your agent.

Underwriters verify employment and review credit immediately before closing. Changes can delay or derail your loan even after initial approval.

Asking Questions Throughout the Process

Mortgage professionals expect questions. Ask whenever you encounter unfamiliar terms, unexpected requirements, or concerning developments.

Understanding each step reduces anxiety and enables better decision-making. Your agent should explain underwriting conditions clearly and outline exactly what actions you need to take to satisfy requirements.

The Value of Long-Term Mortgage Relationships

Your relationship with a mortgage agent shouldn't end at closing. Market conditions change, financial situations evolve, and refinancing opportunities emerge periodically.

Maintaining contact with a trusted agent provides ongoing value. They monitor rate trends relevant to your situation, notify you when refinancing makes financial sense, and serve as a resource for home equity loans or investment property financing.

When circumstances change including income increases, improved credit scores, or falling interest rates, having an established relationship eliminates the need to restart your search for mortgage agents near me. Your agent already understands your financial profile and can quickly evaluate new opportunities.

Geographic Considerations in the Greater Seattle Area

Different cities within the region present unique characteristics affecting your mortgage process.

Seattle Proper

The city's diverse neighborhoods range from affordable areas to luxury markets. Condominium purchases involve additional documentation and lender approval of HOA financial health. Agents familiar with specific Seattle neighborhoods understand typical appraisal values and can identify properties likely to present valuation challenges.

Eastside Communities: Bellevue, Redmond, Kirkland

These cities feature premium housing markets with high median prices frequently requiring jumbo loans. Tech industry concentration means many buyers have stock-heavy compensation requiring specialized income qualification.

North Seattle Suburbs: Shoreline, Lynnwood, Mill Creek

These communities offer more moderate pricing while maintaining proximity to Seattle employment centers. First-time buyers often focus here, requiring agents skilled in down payment assistance programs and affordable loan structuring.

Everett and Outlying Areas

Northern communities provide entry points for buyers priced out of closer-in neighborhoods. Commute times to Seattle require consideration, but property values offer better affordability. Some properties in outer areas might qualify for specific loan programs not available in urban cores.

Current Market Conditions Affecting Seattle Mortgages in 2026

Interest rate environments significantly impact buying power and refinancing decisions. Throughout 2026, rates remain elevated compared to the historic lows of 2020-2021, though considerable volatility creates both challenges and opportunities.

Inventory levels across the Greater Seattle area remain tight in desirable neighborhoods, creating competitive conditions where pre-approval strength and closing speed matter. Multiple-offer situations favor buyers working with mortgage agents who communicate quickly with listing agents and can demonstrate reliable track records.

Home price appreciation has moderated from peak growth rates but continues in most submarkets. Appraisal gaps between contract prices and valuations create financing challenges requiring experienced agents to structure solutions or renegotiate terms.

Understanding these dynamics helps you work more effectively with your mortgage agent and set realistic expectations about timelines, costs, and probable outcomes.

Finding the right mortgage agent transforms a complex, stressful process into a manageable journey toward homeownership. The best professionals combine deep product knowledge, local market expertise, transparent communication, and proven execution. Keith Akada brings over 25 years of mortgage experience serving Seattle, Bellevue, Redmond, and surrounding communities with a client-first approach that has earned 750+ five-star reviews. Whether you're buying your first home or structuring a jumbo loan with complex tech compensation, Mortgage Reel provides the clarity, strategy, and reliability you need to close confidently.