Finding the best mortgage loan company requires more than comparing interest rates on a comparison website. Whether you're purchasing your first home in Shoreline or refinancing a property in Bellevue, the lender you choose directly impacts your closing timeline, out-of-pocket costs, and overall experience during one of the largest financial transactions of your life. In Seattle's competitive housing market, where multiple-offer scenarios and quick closings are standard, partnering with a responsive, experienced mortgage company becomes even more critical. This guide breaks down exactly what separates exceptional mortgage companies from average ones and how to identify the right fit for your specific financing needs.

What Defines the Best Mortgage Loan Company

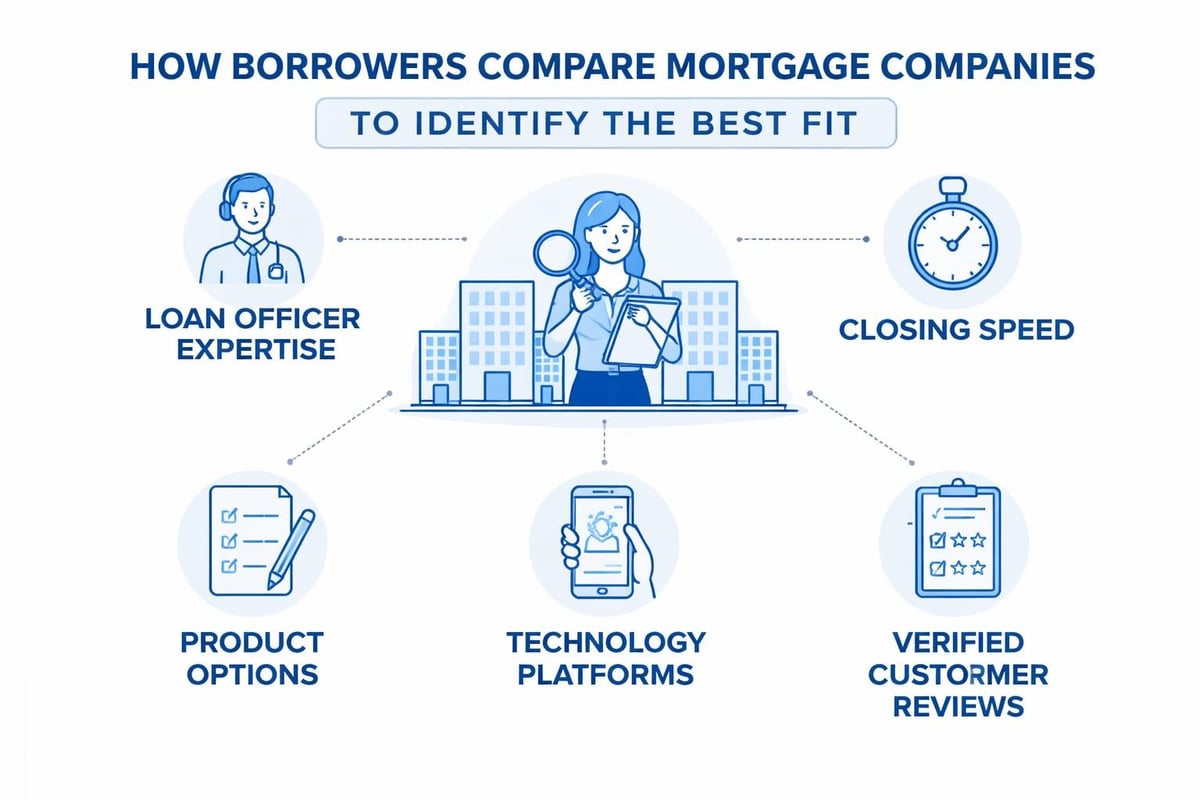

The best mortgage loan company delivers far beyond competitive rates. True excellence in mortgage lending combines expertise, operational efficiency, transparent communication, and product diversity to serve borrowers across different financial profiles and property types.

Core Characteristics That Matter Most

Experienced loan officers make the difference between smooth closings and missed deadlines. A knowledgeable professional anticipates underwriting issues before they become problems, structures your application to highlight strengths, and communicates complex guidelines in plain language. In markets like Seattle, Redmond, and Kirkland, where tech compensation packages include RSUs and stock options, specialized expertise in qualifying non-traditional income becomes invaluable.

Speed and reliability separate top-tier companies from the rest. The ability to deliver pre-approvals within hours, not days, and close loans in under three weeks demonstrates operational excellence. For buyers competing in Lynnwood or Mill Creek, a lender who closes in 9 business days versus 30 can mean the difference between winning and losing a contract.

| Lender Quality Factor | What To Look For | Why It Matters |

|---|---|---|

| Loan Officer Experience | 10+ years, hundreds of closed transactions | Anticipates issues, structures applications strategically |

| Product Variety | Conventional, FHA, VA, USDA, jumbo, portfolio | Matches right program to your situation |

| Technology Integration | Online application, digital document upload, mobile updates | Speeds process, increases transparency |

| Direct Underwriting | In-house underwriters, not outsourced | Faster decisions, better communication |

| Customer Reviews | 4.8+ stars across multiple platforms | Validates consistent performance |

The Better Business Bureau recommends evaluating multiple lenders

Comparing at least three mortgage lenders allows you to identify differences in fees, service quality, and responsiveness. The comparison process reveals which companies treat your business as valuable versus those running automated, impersonal operations.

Types of Mortgage Companies and Their Strengths

Understanding different lender categories helps you target your search effectively. Each type operates under different business models with distinct advantages and limitations.

Direct Lenders vs. Mortgage Brokers

Direct lenders employ loan officers who originate loans funded directly by their institution. They control underwriting, processing, and funding but only offer their own loan products. Major banks, credit unions, and online lenders fall into this category.

Mortgage brokers work with multiple wholesale lenders, accessing dozens of loan programs and rate options. This model provides flexibility to match borrowers with the best-fit lender for their specific scenario. Brokers excel at complex situations like self-employment income, unique properties, or challenging credit profiles.

For Seattle-area tech professionals with stock compensation, brokers familiar with equity income guidelines across multiple lenders often secure better approvals than single-source direct lenders.

Banks, Credit Unions, and Independent Companies

- National banks offer brand recognition and extensive branch networks but often lack local market expertise and personalized service

- Credit unions provide competitive rates for members but typically have limited product menus and slower processing timelines

- Independent mortgage companies combine specialized expertise with operational flexibility, often delivering faster closings and more customized solutions

In competitive markets like Everett and Lake Forest Park, local independent companies with established relationships to area real estate agents and title companies frequently outperform large national institutions.

Key Factors in Selecting Your Best Mortgage Loan Company

Your ideal lender aligns with your financial profile, property type, and timeline requirements. Generic "best of" lists rarely account for individual circumstances that make certain lenders better fits than others.

Interest Rates and Annual Percentage Rates (APR)

Rate matters, but APR tells the complete story. While two lenders might advertise identical interest rates, their fees and closing costs can differ by thousands of dollars. APR incorporates these costs, providing an apples-to-apples comparison.

Rate locks protect you from market fluctuations between application and closing. The best mortgage loan company offers flexible lock periods (30, 45, or 60 days) and clear policies about extensions if closing delays occur beyond your control.

Fee Structures and Closing Cost Transparency

Origination charges, processing fees, underwriting fees, and administrative costs vary dramatically between lenders. Some advertise low rates but compensate through elevated fees. Others maintain straightforward pricing with minimal junk fees.

Request Loan Estimates from each lender you're considering. Federal law requires this standardized form within three business days of application, making direct comparisons simple and revealing which companies front-load costs versus those hiding fees until closing.

Loan Programs and Product Availability

The best mortgage loan company for a first-time buyer in Shoreline purchasing a $450,000 condo differs from the best option for an investor buying a $1.8 million property in Bellevue. Product specialization matters.

Evaluate whether lenders offer:

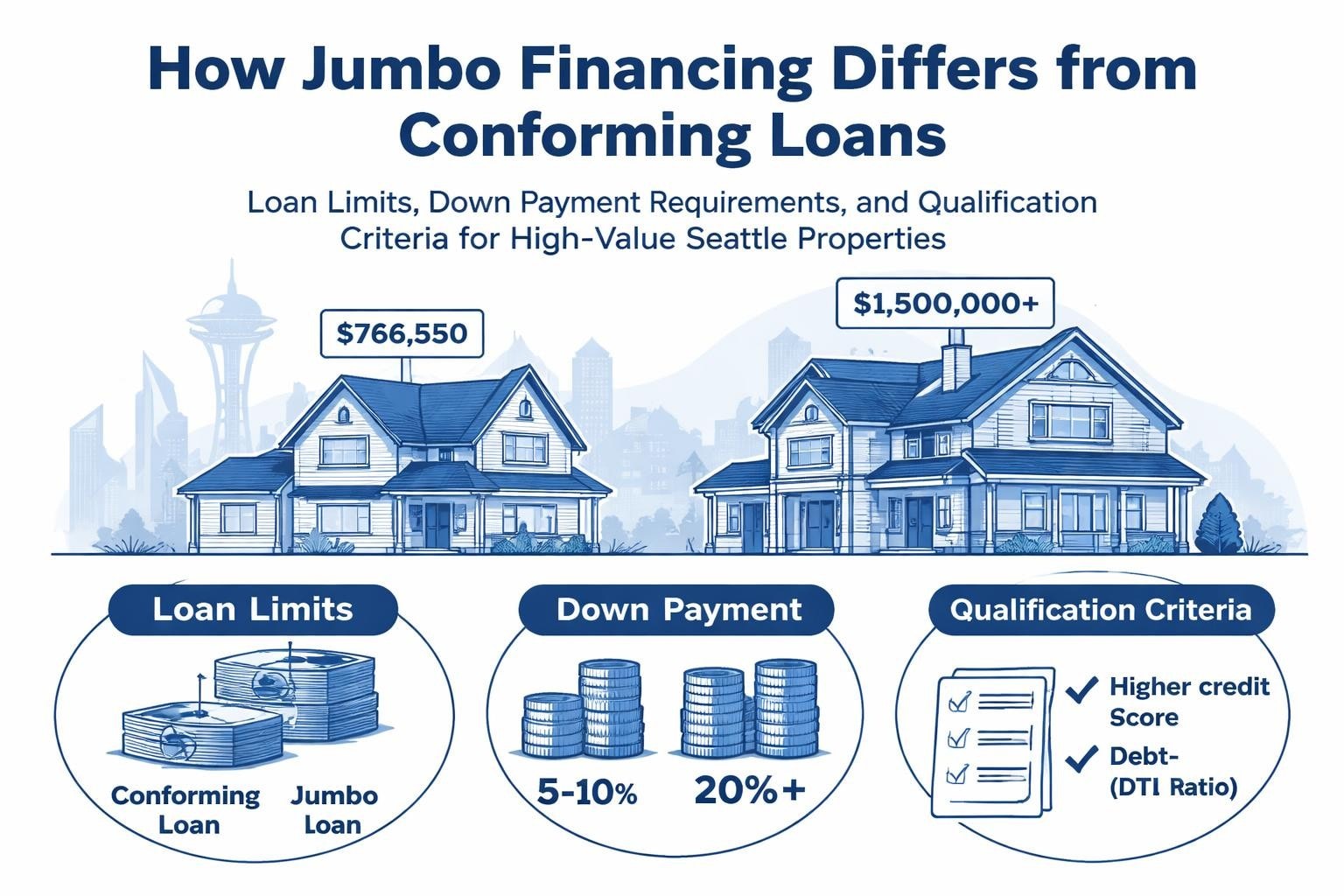

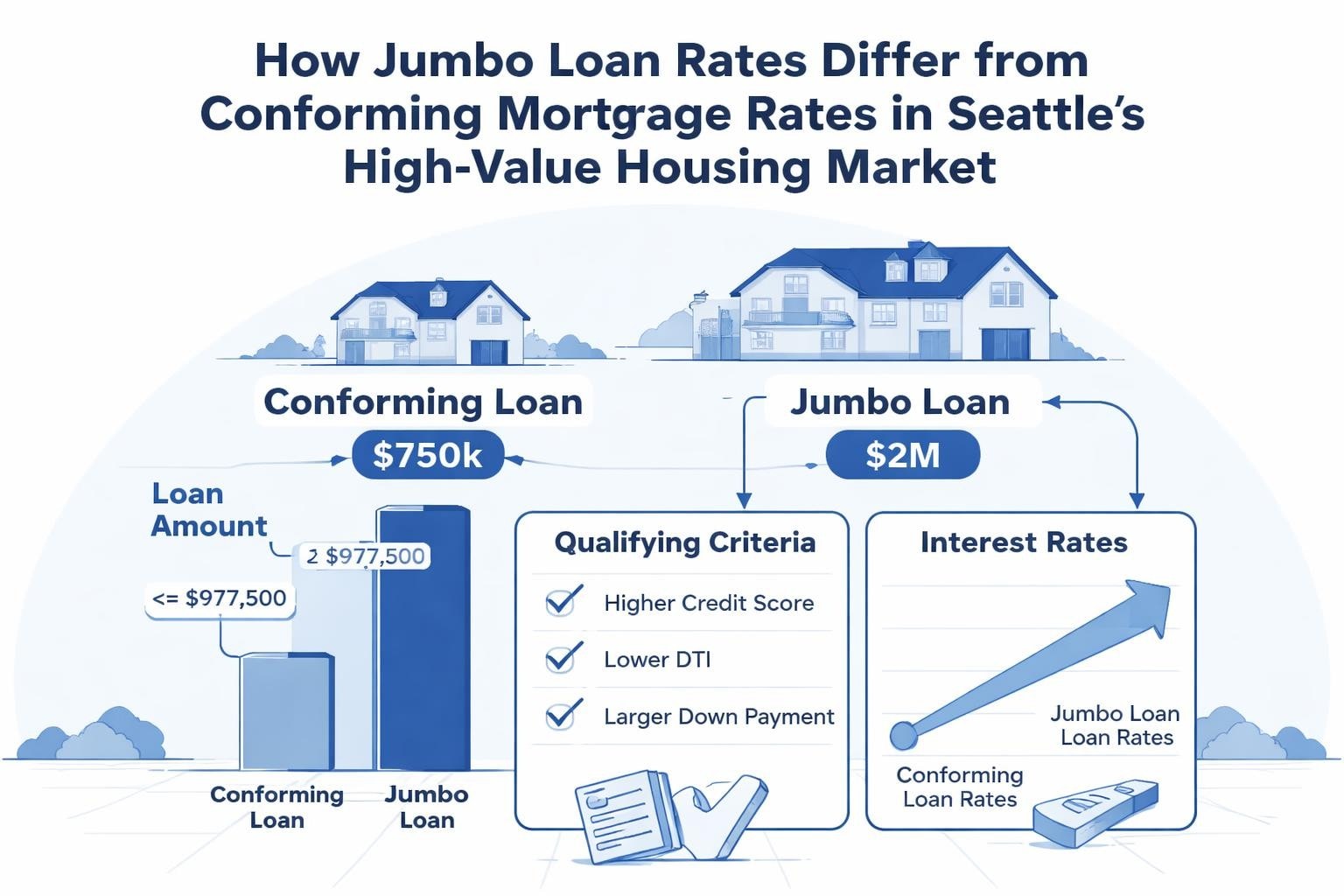

- Conventional conforming loans (Fannie Mae/Freddie Mac up to $806,500 in 2026)

- Jumbo loans for Seattle-area purchases exceeding conforming limits

- FHA loans with 3.5% down payment options

- VA loans for eligible veterans and service members with zero down payment

- Portfolio programs for unique scenarios outside agency guidelines

Tech professionals frequently need jumbo financing with specialized income documentation. Working with a company experienced in qualifying RSUs, stock options, and retention bonuses prevents application denials or unnecessary delays.

Questions to Ask Before Choosing a Lender

Strategic questions reveal lender capabilities and help you assess fit before committing to an application.

Qualification and Pre-Approval Questions

-

How do you calculate my maximum purchase price? This reveals whether the lender considers your complete financial picture or applies generic debt-to-income formulas.

-

What documentation will you need for my income type? Self-employed borrowers, commissioned sales professionals, and tech workers with equity compensation need lenders who understand complex income documentation.

-

How quickly can you deliver a pre-approval letter? In competitive markets, same-day pre-approvals demonstrate operational capability.

-

Do your pre-approvals include credit and income verification, or are they pre-qualifications? Verified pre-approvals carry significantly more weight with sellers and listing agents.

Process and Timeline Questions

Understanding the lender's typical workflow helps set realistic expectations and identifies potential bottlenecks.

- What's your average time from application to clear-to-close?

- Do you have in-house processing and underwriting?

- How will you communicate status updates throughout the process?

- What happens if issues arise during underwriting?

The best mortgage loan company maintains proactive communication, reaching out with updates rather than waiting for you to inquire about progress. NerdWallet’s guide on choosing a mortgage lender emphasizes the importance of understanding the complete borrowing process before committing to a lender.

Service and Support Questions

Post-closing support matters more than many borrowers realize. Questions about ongoing service reveal whether you're valued beyond the initial transaction.

-

Who services my loan after closing? Some lenders sell servicing rights immediately, transferring your payment processing to unfamiliar companies.

-

What happens if I want to refinance in the future? Established relationships with your original loan officer often result in faster, less expensive refinancing.

-

How do you handle rate lock extensions if closing delays occur? Fair policies protect you from market movements caused by circumstances beyond your control.

How Customer Reviews Reveal Lender Quality

Online reviews provide unfiltered insights into actual customer experiences. The best mortgage loan company consistently earns high ratings across multiple platforms over extended periods.

Where to Find Credible Reviews

- Google Reviews: Local business ratings with verified Google accounts

- Zillow Lender Directory: Mortgage-specific platform with detailed borrower feedback

- Yelp: Consumer review platform with fraud detection algorithms

- Better Business Bureau: Complaint tracking and resolution records

Look for patterns across hundreds of reviews rather than focusing on individual five-star or one-star outliers. Companies with 750+ reviews maintaining 4.9+ average ratings demonstrate exceptional, consistent performance.

Red Flags in Reviews and Responses

Watch for recurring complaints about:

- Missed closing deadlines and delayed rate locks

- Lack of communication during critical decision points

- Unexpected fees appearing at closing

- Loan officers who disappear after application submission

- Pushy sales tactics or pressure to lock rates prematurely

Equally important: evaluate how companies respond to negative reviews. Professional, constructive responses that acknowledge issues and explain resolutions indicate accountability and customer-focused operations.

Technology and Digital Experience

Modern mortgage lending requires robust technology platforms that streamline documentation, accelerate underwriting, and provide transparency throughout the loan process.

Digital Application and Document Management

The best mortgage loan company offers secure online portals for application submission, document upload, and real-time status tracking. Mobile-friendly platforms allow you to submit pay stubs, bank statements, and tax returns from your phone rather than scanning and emailing files.

Advanced systems integrate with employment verification services, instantly confirming income and reducing documentation requirements. For W-2 employees, this often eliminates the need for manual pay stub submission entirely.

Communication Technology and Responsiveness

Expect multiple communication channels including text messaging, email, and phone access. Loan officers who respond within hours, not days, keep transactions moving forward and prevent last-minute surprises.

Video consultation capabilities became standard during recent years and now represent baseline expectations. Initial consultations, document reviews, and closing questions handled via video call save time while maintaining personal connection.

Specialized Expertise for Complex Scenarios

Standard residential purchase and refinance transactions represent only a portion of mortgage lending. Complex scenarios require lenders with specialized knowledge and underwriting relationships.

Tech Industry Compensation and Jumbo Financing

Amazon, Microsoft, Google, and other Seattle-area tech employers compensate through base salary plus significant equity components. Traditional lenders often struggle to qualify RSUs, stock options, and retention bonuses, leaving substantial purchasing power on the table.

The best mortgage loan company for tech professionals understands how to:

- Document vesting schedules and calculate sustainable income from equity compensation

- Average bonus history to establish qualifying income patterns

- Structure debt-to-income ratios to maximize approval amounts while maintaining comfortable payment levels

- Coordinate jumbo loan underwriting for purchases exceeding conforming loan limits

In Bellevue and Redmond, where median home prices frequently require jumbo financing, this expertise becomes essential rather than optional.

Self-Employment and Non-Traditional Income

Business owners, commissioned sales professionals, and freelancers face additional documentation requirements. Lenders experienced with self-employed borrowers know how to:

- Analyze tax returns to identify qualifying income versus total revenue

- Add back legitimate business deductions that reduce taxable income but don't affect cash flow

- Use bank statement programs for borrowers who maximize tax deductions

- Structure applications to highlight business stability and future income predictability

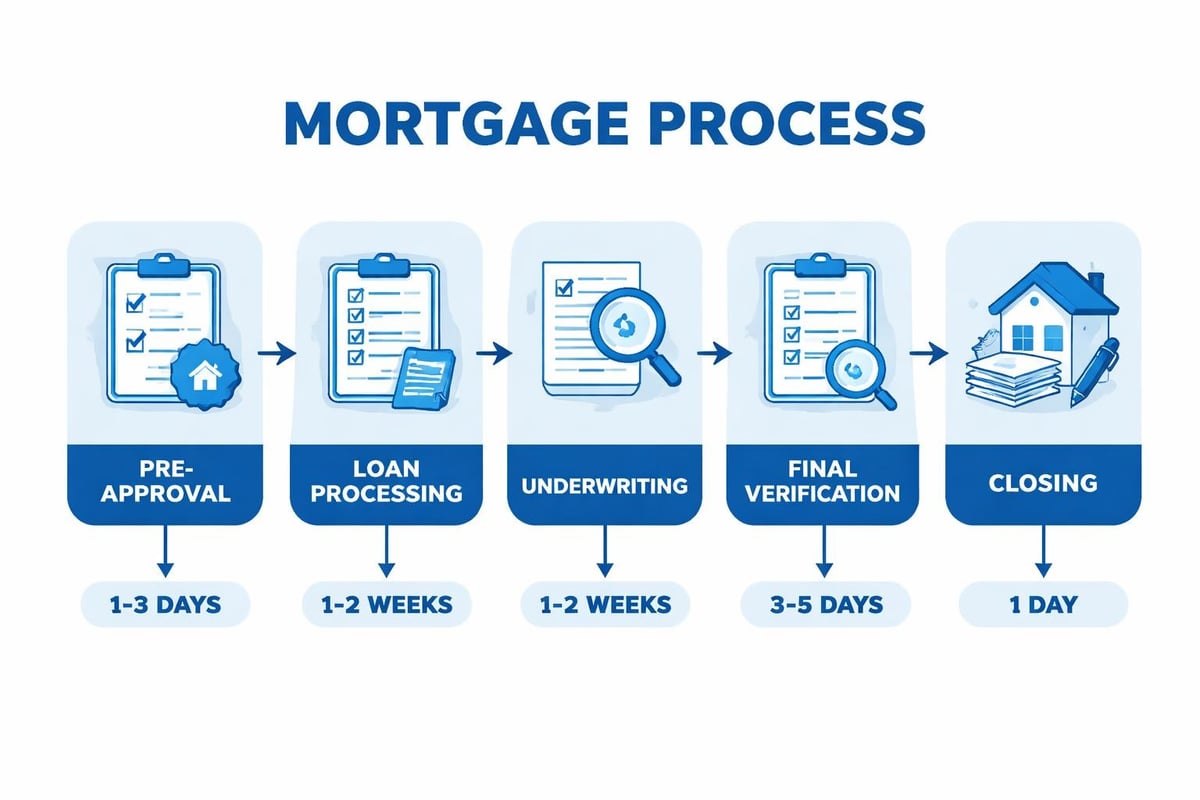

The Application and Approval Process

Understanding typical workflows helps you prepare documentation, ask informed questions, and identify when your transaction falls behind schedule.

Pre-Approval Through Closing Timeline

| Stage | Typical Timeline | Key Activities |

|---|---|---|

| Pre-Approval | Same day to 3 days | Credit check, income verification, initial underwriting review |

| Full Application | 1-2 days | Complete file submission with all required documentation |

| Processing | 3-7 days | Document verification, title work, appraisal ordering |

| Underwriting | 5-10 days | Comprehensive file review, condition requests, final approval |

| Clear to Close | 2-3 days | Final verification, closing disclosure review, funding preparation |

| Closing | 1 day | Document signing, fund disbursement, ownership transfer |

Exceptional lenders compress this timeline through efficient operations and experienced underwriting teams. The ability to close in 9-12 business days versus 30-45 days provides significant competitive advantage in markets like Seattle, Kirkland, and Mill Creek.

Common Delays and How to Avoid Them

Most closing delays stem from preventable documentation issues or poor communication:

- Incomplete employment verification: Self-employed borrowers and those with recent job changes need extra documentation prepared upfront

- Appraisal complications: Properties requiring repairs or in declining markets may need additional review

- Title issues: Existing liens, boundary disputes, or ownership questions require resolution before closing

- Last-minute financial changes: New credit inquiries, job changes, or large deposits trigger re-underwriting

Working with a proactive loan officer who requests comprehensive documentation upfront prevents most delays. The American Bankers Association’s guidance on choosing lenders emphasizes the value of borrower preparation in accelerating approvals.

Local Market Expertise Makes a Difference

Seattle-area real estate presents unique challenges that national lenders often misunderstand. Local expertise translates to smoother transactions and better outcomes.

Why Seattle Market Knowledge Matters

The Greater Seattle housing market operates differently than national averages:

- Competitive multiple-offer scenarios require strong pre-approvals and quick responses to counteroffers

- Appraisal challenges in rapidly appreciating neighborhoods need experienced negotiation

- Condo financing in Seattle high-rises involves additional review requirements

- Property tax considerations impact debt-to-income calculations differently than other markets

Lenders serving Shoreline, Lynnwood, Everett, and Lake Forest Park understand local property values, common inspection issues, and preferred title companies. These relationships accelerate closings and prevent complications that derail transactions with out-of-area lenders.

Agent Relationships and Reputation

Local real estate agents develop preferences for lenders who consistently deliver on promises. Strong professional relationships often mean:

- Your offers receive favorable consideration when sellers compare multiple bids

- Listing agents recommend lenders to their buyer clients based on proven performance

- Transaction coordinators prioritize your file because they trust the lender's reliability

Ask potential lenders for references from local real estate professionals. Top performers maintain relationships with dozens of agents who vouch for their expertise and execution.

Refinancing Considerations and Future Flexibility

Your relationship with your mortgage company shouldn't end at closing. The best mortgage loan company supports long-term financial goals through refinancing opportunities and ongoing guidance.

When Refinancing Makes Sense

Rate-and-term refinancing becomes attractive when:

- Current market rates fall at least 0.75% below your existing rate

- Your credit score has improved significantly since original financing

- You want to eliminate mortgage insurance by reaching 20% equity

- Adjustable-rate mortgages approach first adjustment dates

Cash-out refinancing allows you to access home equity for debt consolidation, home improvements, or investment opportunities. Seattle-area homeowners often leverage accumulated equity to fund renovations that increase property value beyond the loan amount.

Lender Loyalty Benefits and Considerations

Returning to your original lender for refinancing often streamlines the process. Many companies offer:

- Reduced documentation since they originated your current loan

- Waived application or processing fees for existing customers

- Faster closing timelines with established relationships

- Retained servicing to avoid payment processing changes

However, loyalty shouldn't override rate shopping. Compare refinance offers from multiple lenders to ensure competitive pricing, then give your current lender opportunity to match or beat outside offers.

Making Your Final Decision

After researching options, reading reviews, and conducting interviews, synthesizing information into a clear decision requires structured evaluation.

Creating Your Comparison Matrix

Build a simple spreadsheet comparing your top three candidates across critical factors:

- Interest rate and APR for your specific scenario

- Total estimated closing costs

- Loan officer experience and responsiveness

- Average closing timeline

- Customer review ratings across multiple platforms

- Product availability for your needs

- Technology platform quality

Weight factors according to your priorities. First-time buyers might prioritize educational support and patience, while experienced investors focus on speed and jumbo loan expertise.

Trust Your Instincts on Communication

Beyond quantitative comparisons, assess how each loan officer makes you feel. The best mortgage loan company assigns professionals who:

- Listen more than they talk during initial consultations

- Explain concepts clearly without condescending language

- Proactively identify potential challenges rather than overselling approval certainty

- Return calls and emails within reasonable timeframes

- Demonstrate genuine interest in your long-term success

If something feels off during early interactions, trust that instinct. You'll communicate extensively throughout the mortgage process, making rapport and trust essential components of successful partnerships.

Resources for Continued Learning

Mortgage financing involves complex regulations, programs, and strategies. Ongoing education helps you make confident decisions throughout the homeownership journey.

Banks.com’s comprehensive guide on choosing mortgage lenders offers additional perspectives on lender evaluation and selection criteria. Educational resources from trusted sources supplement individual lender consultations and help you ask informed questions.

Industry changes occur regularly. Following reliable mortgage education sources keeps you updated on program changes, rate movements, and emerging loan products that might benefit your situation.

Common Mistakes to Avoid

Even informed borrowers make preventable errors when selecting mortgage companies. Awareness of common pitfalls helps you navigate the selection process successfully.

Choosing Based Solely on Rate

The lowest advertised rate rarely translates to the lowest actual cost. Lenders compensate for rate discounts through:

- Elevated closing costs that exceed rate savings over typical ownership periods

- Discount points that require upfront cash to buy down rates

- Reduced service quality that causes delays, frustration, and potential deal failures

Calculate total costs over your expected ownership timeline rather than focusing exclusively on monthly payment differences.

Failing to Get Pre-Approved Before House Hunting

Pre-qualification letters based on self-reported information carry minimal weight with sellers. Verified pre-approvals demonstrating creditworthiness and income validation position you as serious buyers in competitive markets.

In Seattle, Bellevue, Redmond, and Kirkland, where desirable properties receive multiple offers within days, unverified pre-qualifications often disqualify buyers from consideration entirely.

Switching Lenders Mid-Process

Changing lenders after starting the application process resets timelines, potentially missing rate lock expirations and purchase contract deadlines. Unless serious problems emerge, commit to your chosen lender and work through challenges collaboratively.

Legitimate reasons to switch include:

- Discovering undisclosed fees not mentioned during initial conversations

- Consistent failure to meet promised timelines or return communications

- Bait-and-switch tactics where promised rates become unavailable

- Unprofessional behavior or pressure tactics

Neglecting to Lock Your Rate Appropriately

Rate locks protect against market increases but expire if closings extend beyond lock periods. Understand:

- Lock periods should exceed your expected closing timeline by at least one week

- Extension policies and associated costs if delays occur

- Float-down options that allow rate reductions if markets improve during your lock period

Selecting the best mortgage loan company requires evaluating expertise, operational efficiency, product offerings, and personal compatibility alongside rate competitiveness. The right lender becomes a long-term partner who supports your homeownership journey through purchase, refinance, and strategic financial decisions. Keith Akada at Mortgage Reel brings 25+ years of experience serving Seattle-area homebuyers with transparent guidance, specialized tech industry income expertise, and proven execution reflected in 750+ five-star reviews across major platforms. Whether you're purchasing in Shoreline, refinancing in Everett, or need jumbo financing in Bellevue, working with a trusted local mortgage broker ensures you receive personalized service matched to Seattle's competitive real estate market.