Purchasing your first home represents one of the most significant financial decisions you'll ever make, and in Seattle's competitive housing market, having the right strategy and guidance is essential. Whether you're a tech professional at Amazon or Microsoft looking to leverage stock compensation, or a growing family searching in neighborhoods from Shoreline to Everett, understanding the complete homebuying process will help you make confident decisions. This comprehensive guide covers everything from financial preparation and mortgage options to navigating Seattle-area markets and closing your transaction successfully.

Understanding Your Financial Position Before Purchasing Your First Home

Before you begin touring properties or scrolling through listings, establishing a clear picture of your financial health is critical. Your credit score, debt-to-income ratio, and savings will determine not only which homes you can afford but also the mortgage rates and terms you'll qualify for.

Credit Score Requirements and Impact

Your credit score directly affects your mortgage interest rate and loan approval. Conventional loans typically require a minimum score of 620, though higher scores unlock better rates and terms. FHA loans may accept scores as low as 580 with a 3.5% down payment, or even 500 with 10% down.

Key credit considerations include:

- Review your credit reports from all three bureaus for errors

- Pay down credit card balances to below 30% of limits

- Avoid opening new credit accounts during the homebuying process

- Maintain consistent payment history on all existing obligations

For tech professionals in Seattle with strong incomes but limited credit history, establishing multiple credit types and maintaining low utilization ratios becomes especially important. Even a 20-point score difference can impact your rate by 0.25% or more, translating to thousands of dollars over the loan term.

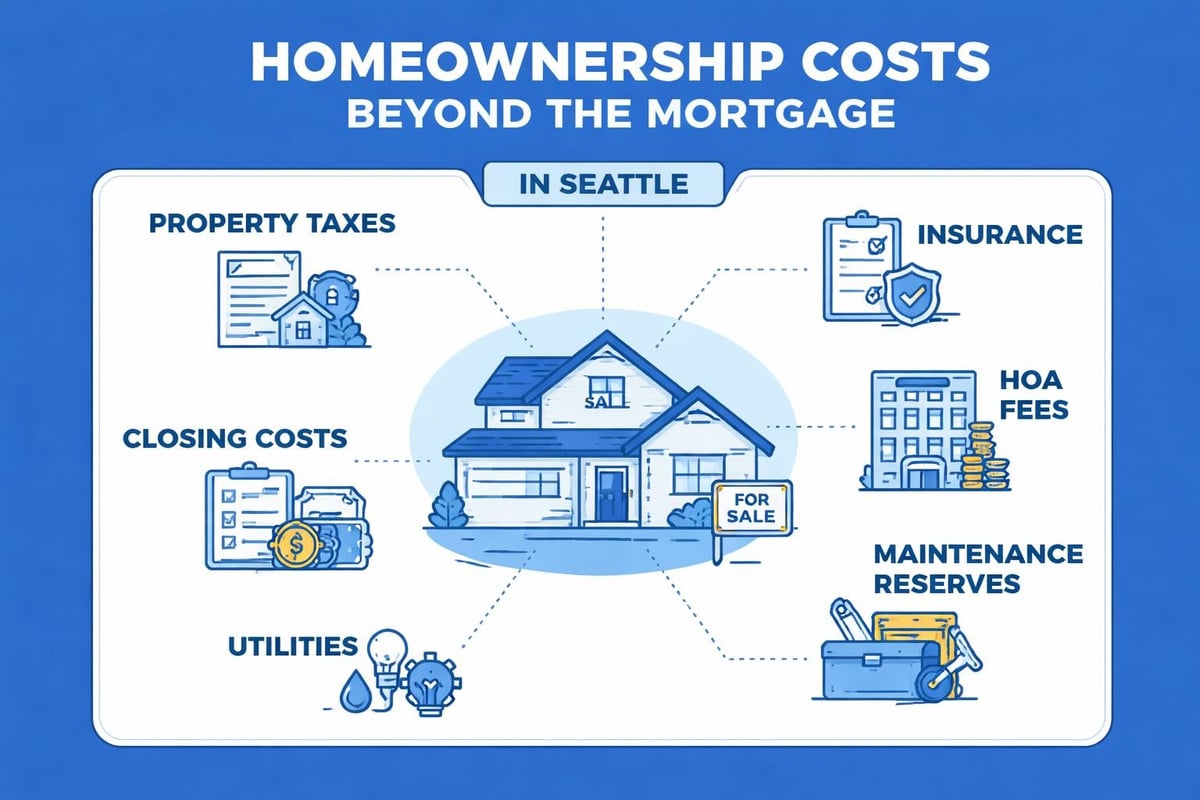

Calculating Your True Budget

Many first-time buyers focus solely on the purchase price without considering the full cost of homeownership. Understanding all housing costs ensures you select a home that fits comfortably within your long-term budget.

| Expense Category | Monthly Cost Range (Seattle Area) | Annual Impact |

|---|---|---|

| Property Taxes | $400 – $1,200 | $4,800 – $14,400 |

| Homeowners Insurance | $100 – $250 | $1,200 – $3,000 |

| HOA Fees (if applicable) | $200 – $800 | $2,400 – $9,600 |

| Maintenance/Repairs | $200 – $500 | $2,400 – $6,000 |

| Utilities | $150 – $300 | $1,800 – $3,600 |

Beyond monthly costs, purchasing your first home requires substantial upfront cash. Down payment requirements vary by loan type, but you'll also need funds for closing costs (typically 2-5% of the purchase price), earnest money deposits, inspection fees, and appraisal costs.

Exploring Mortgage Options for First-Time Buyers

The mortgage landscape offers numerous programs designed specifically for those purchasing your first home. Understanding the differences between loan types helps you select the option that best aligns with your financial situation and homeownership goals.

Conventional Loans

Conventional mortgages, not backed by government agencies, remain the most common choice for buyers with strong credit and stable income. These loans offer flexibility in property type and price range, making them ideal for Seattle's diverse housing market.

Conventional loan advantages:

- Down payments as low as 3% for first-time buyers

- Ability to cancel PMI once you reach 20% equity

- Higher loan limits suitable for Seattle's median home prices

- Competitive rates for well-qualified borrowers

For 2026, the conventional conforming loan limit in King County is $806,500 for single-family homes, with higher limits for multi-unit properties. This accommodates most purchases in neighborhoods like Lake Forest Park and Mill Creek without requiring jumbo financing.

Government-Backed Loan Programs

FHA, VA, and USDA loans provide alternatives with more flexible qualification standards. FHA loans accept lower credit scores and offer 3.5% down payments, though they require mortgage insurance for the loan's life. VA loans, available to eligible service members and veterans, offer 100% financing with no PMI requirement.

Comparison of government loan programs:

| Loan Type | Min. Down Payment | Credit Score | PMI Requirement | Property Location |

|---|---|---|---|---|

| FHA | 3.5% | 580+ | Required (lifetime) | No restrictions |

| VA | 0% | No minimum | None | No restrictions |

| USDA | 0% | 640+ | Required | Rural areas only |

| Conventional | 3% | 620+ | Removable at 20% | No restrictions |

Jumbo Loans for Seattle's Market

Seattle's robust real estate market frequently pushes buyers above conforming loan limits, particularly in neighborhoods like Bellevue and Redmond. Jumbo loans accommodate higher purchase prices but typically require larger down payments (10-20%) and stronger credit profiles.

For tech professionals with substantial RSU compensation, qualifying stock income properly becomes essential for jumbo loan approval. Lenders can count RSUs and stock options as qualifying income when documented correctly, significantly increasing purchasing power for Microsoft and Amazon employees.

Navigating Seattle's Competitive Housing Market

Understanding local market dynamics helps you make strategic decisions when purchasing your first home in the Greater Seattle area. Each neighborhood presents unique characteristics, price points, and competition levels.

Neighborhood Selection Strategy

Seattle-area communities range from urban high-rises to suburban single-family neighborhoods, each offering distinct lifestyle benefits. Shoreline provides excellent schools and parks with more affordable pricing than central Seattle. Lynnwood offers strong transportation connections and newer construction options. Everett presents the most budget-friendly entry point while maintaining access to major employers.

Researching neighborhoods thoroughly includes evaluating school ratings, commute times, planned development, and property appreciation trends. Consider not just current needs but how your requirements might evolve over the next 5-10 years.

Key neighborhood evaluation factors:

- Commute time to primary workplace

- School district quality and boundaries

- Walkability and public transportation access

- Local amenities and shopping options

- Future development plans and zoning changes

- Historical appreciation rates and market stability

Making Competitive Offers

Seattle's housing market remains competitive in 2026, particularly for well-priced homes in desirable neighborhoods. Multiple offer situations require strategic positioning to succeed without overpaying.

Working with your lender to secure pre-approval (not just pre-qualification) demonstrates financial readiness to sellers. A pre-approval letter from a reputable local lender carries significantly more weight than online pre-qualifications. Consider including an escalation clause that automatically increases your offer up to a maximum price if competing offers emerge.

The Pre-Approval Process Explained

Getting pre-approved before house hunting provides clarity on your budget and strengthens your position with sellers. The pre-approval process involves comprehensive documentation review and preliminary underwriting.

Required Documentation

Lenders review your complete financial profile to determine loan eligibility and maximum purchase price. Gathering documentation upfront accelerates the pre-approval timeline and helps identify potential issues early.

Standard documentation requirements:

- Two years of W-2 forms and tax returns

- Recent pay stubs (30 days)

- Two months of bank statements for all accounts

- Employment verification

- Documentation of additional income sources (bonuses, RSUs, commissions)

- Explanation letters for credit inquiries or recent deposits

For tech professionals with stock compensation, additional documentation proves RSU value and vesting schedules. Lenders typically average restricted stock income over two years, so consistent grant history strengthens qualification.

Understanding Debt-to-Income Ratios

Your debt-to-income (DTI) ratio compares monthly debt obligations to gross monthly income. Most conventional loans require DTI below 43-50%, though some programs accept higher ratios with compensating factors like strong credit or significant reserves.

Front-end DTI considers only housing expenses (principal, interest, taxes, insurance, HOA fees), while back-end DTI includes all monthly debt payments. Reducing DTI before purchasing your first home might involve paying down installment loans, reducing credit card balances, or increasing income through bonuses or side work.

Working with Real Estate Professionals

Assembling a knowledgeable team makes purchasing your first home smoother and less stressful. Your mortgage broker, real estate agent, and home inspector each play critical roles in successful transactions.

Selecting a Real Estate Agent

Choosing an experienced buyer’s agent familiar with Seattle-area markets provides invaluable guidance through negotiations, inspections, and closing. Look for agents who specialize in first-time buyers and demonstrate strong communication skills.

Interview multiple agents before committing. Ask about their experience in your target neighborhoods, average response time, negotiation approach, and recent transactions. The right agent educates rather than pressures, helps you understand market conditions, and advocates for your interests throughout the process.

The Role of Your Mortgage Broker

Your mortgage broker structures financing to maximize purchasing power while ensuring loan terms align with long-term goals. Unlike loan officers who work for a single lender, brokers access multiple lending sources to find optimal programs and rates.

Beyond securing financing, experienced brokers provide market insight, timeline guidance, and problem-solving when issues arise. They coordinate with your real estate agent, title company, and appraiser to maintain transaction momentum and meet closing deadlines.

Understanding Closing Costs and Down Payments

The cash required to close on your home extends beyond the down payment. Preparing for all closing costs prevents last-minute surprises and ensures smooth transaction completion.

Breaking Down Closing Costs

Closing costs typically range from 2-5% of the purchase price and cover services required to complete your transaction. Some costs are lender fees while others are third-party charges.

| Cost Category | Typical Range | Negotiable |

|---|---|---|

| Loan origination fee | 0-1% of loan | Sometimes |

| Appraisal | $500-800 | No |

| Title insurance | $1,000-3,000 | Sometimes |

| Escrow/settlement fee | $500-1,500 | Sometimes |

| Recording fees | $200-500 | No |

| Prepaid taxes/insurance | Varies | No |

| Home inspection | $400-700 | No |

Planning for these costs early prevents budget strain. Some sellers offer closing cost credits as part of negotiations, particularly if homes have been on market longer than average.

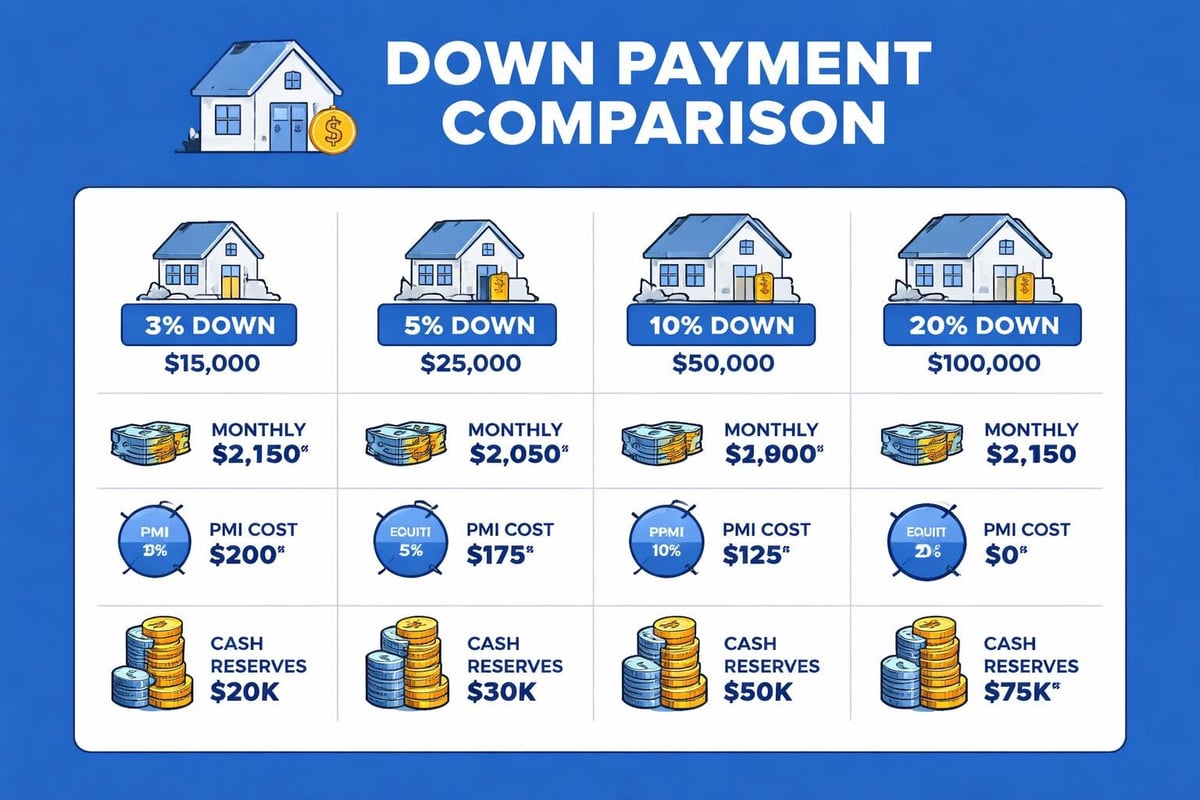

Down Payment Strategies

While 20% down payments eliminate PMI and reduce monthly payments, numerous programs allow much smaller down payments when purchasing your first home. The optimal down payment balances monthly affordability, long-term interest costs, and maintaining emergency reserves.

Down payment considerations:

- 20% down eliminates PMI and provides best rates

- 10-15% down balances affordability with equity building

- 5% down increases monthly costs but preserves cash reserves

- 3-3.5% down maximizes purchasing power for qualified buyers

For Seattle buyers facing high property values, smaller down payments might be strategic if it means buying sooner in an appreciating market. Running scenarios with your mortgage broker reveals the true cost difference between down payment options.

Home Inspection and Due Diligence

The inspection period allows you to thoroughly evaluate the property's condition before finalizing your purchase. This contingency period protects buyers from unknown defects and provides negotiation leverage for needed repairs.

Professional Home Inspections

Hiring qualified home inspectors reveals issues invisible during showings. Comprehensive inspections cover structural elements, electrical systems, plumbing, HVAC, roofing, and foundation. In Seattle's older housing stock, particularly in neighborhoods like Shoreline and Lake Forest Park, inspections often uncover needed updates to electrical panels, water heaters, or drainage systems.

Attend the inspection whenever possible. Inspectors explain findings in detail and answer questions about maintenance, repair urgency, and cost estimates. This knowledge informs negotiation strategy and helps prioritize future home improvement projects.

Addressing Inspection Findings

Inspection reports rarely show perfect properties. The key is distinguishing between minor maintenance items and significant defects affecting safety, functionality, or value. Material issues might warrant repair requests, price reductions, or in severe cases, contract termination.

Common inspection negotiation approaches:

- Request seller repairs before closing

- Ask for closing cost credits to fund future repairs

- Negotiate purchase price reduction

- Accept property as-is with full knowledge of conditions

- Terminate contract if issues exceed acceptable risk

Your real estate agent guides negotiation strategy based on market conditions, inspection severity, and seller motivation. In competitive Seattle markets, buyers sometimes waive inspection contingencies, though this significantly increases risk when purchasing your first home.

Special Considerations for Tech Professionals

Seattle's concentration of major technology employers creates unique opportunities and challenges for homebuyers. Understanding how lenders evaluate stock compensation and bonuses maximizes your purchasing power.

Qualifying RSUs and Stock Options

Restricted stock units and stock options represent substantial income for Microsoft, Amazon, and Google employees. However, lenders apply specific guidelines when counting this compensation toward mortgage qualification.

Generally, lenders average RSU income over the most recent two years, requiring documentation of vesting schedules and grant history. The more consistent your RSU grants, the more income lenders will count. Some programs allow using current year projections if you can demonstrate increasing grant patterns.

RSU qualification requirements:

- Minimum two-year history of receiving stock compensation

- Documentation of all vesting schedules

- Brokerage statements showing deposits and sales

- Tax returns reflecting stock income

- Employment verification confirming continued grants

Working with a mortgage broker experienced in stock compensation ensures proper documentation and maximizes income calculation. This expertise often means the difference between qualifying for your target price range or settling for less.

Jumbo Loan Strategies

Many Seattle-area homes exceed conforming loan limits, requiring jumbo financing. While these loans demand stronger qualifications, they enable purchases in premium neighborhoods without enormous down payments.

Jumbo loan approval typically requires credit scores above 700, DTI ratios below 43%, and reserves covering 6-12 months of housing payments. For tech professionals with strong income but limited savings history, demonstrating 401(k) balances and stock portfolios helps meet reserve requirements.

Timing Your Purchase in Seattle's Market

Understanding seasonal patterns and market cycles helps you time your purchase advantageously. While you can buy any time of year, certain periods offer strategic benefits.

Seasonal Market Patterns

Seattle's housing market shows distinct seasonal variation. Spring and early summer bring peak inventory and competition as families target moves before the school year. Fall and winter typically offer less competition and more negotiating leverage, though inventory decreases.

For buyers prioritizing selection over price, spring shopping makes sense. Those willing to accept limited options for better negotiation position often succeed in November through February. Mill Creek and Everett markets show particularly strong seasonal variation compared to central Seattle condos.

Interest Rate Considerations

Mortgage rates fluctuate based on economic conditions, Federal Reserve policy, and market factors. While timing rates perfectly is impossible, understanding trends helps with purchase decisions.

Working with your lender to monitor rates and lock at opportune times protects your budget. Rate locks typically extend 30-60 days, so coordinate lock timing with your expected closing date. Some lenders offer float-down options if rates decrease after locking, though these may carry additional fees.

Final Steps to Closing

The period between offer acceptance and closing involves numerous tasks, deadlines, and coordination among multiple parties. Staying organized and responsive keeps your transaction on track.

The Underwriting Process

After initial approval, your loan file goes to underwriting for comprehensive review. Underwriters verify all documentation, order appraisals, review title reports, and ensure you meet program guidelines. They may request additional documentation or explanations for credit inquiries, employment changes, or large deposits.

Respond to underwriter requests promptly to avoid closing delays. Avoid major financial changes during this period-don't change jobs, open new credit, make large purchases, or move money between accounts without discussing with your lender first.

Final Walkthrough and Closing

Your final walkthrough typically occurs 24-48 hours before closing. This inspection confirms the property's condition matches your agreement and that any negotiated repairs were completed satisfactorily. Test appliances, run faucets, check windows and doors, and ensure nothing has changed since your last visit.

Closing day involves signing numerous documents and transferring funds. Review the Closing Disclosure at least three days before closing to verify all numbers match expectations. Bring valid identification and certified funds for your down payment and closing costs.

Closing day checklist:

- Government-issued photo ID

- Certified check or wire transfer confirmation

- Proof of homeowners insurance

- Final walkthrough notes

- Questions for title company

- Celebratory plans for becoming a homeowner

First-Time Buyer Programs and Assistance

Numerous programs help reduce barriers when purchasing your first home. Federal, state, and local initiatives offer down payment assistance, reduced rates, and educational resources.

Washington State Programs

The Washington State Housing Finance Commission offers several programs for first-time buyers, including down payment assistance loans and competitive interest rates. These programs include income limits and purchase price caps that accommodate most buyers in Lynnwood, Shoreline, and surrounding communities.

HomeChoice and House Key programs provide down payment assistance as secondary loans with deferred payments. Combined with 3% conventional financing, these programs enable homeownership with minimal cash investment.

Tax Benefits and Credits

Homeownership provides several tax advantages. Mortgage interest and property taxes are often deductible (subject to current tax law limits), reducing your effective housing cost. Some first-time buyers may qualify for Mortgage Credit Certificates, which convert a portion of mortgage interest into a direct tax credit.

Consult with tax professionals to understand specific benefits and maintain proper documentation. The tax advantages of homeownership contribute meaningfully to long-term wealth building compared to renting.

Purchasing your first home in the Seattle area requires careful planning, strategic financing, and expert guidance through each step of the process. From understanding your budget and securing optimal mortgage terms to navigating competitive markets and closing successfully, having an experienced partner makes all the difference. Keith Akada and the team at Mortgage Reel bring over 25 years of experience helping Seattle-area buyers achieve homeownership with confidence, offering specialized expertise in stock compensation qualification, jumbo loans, and rapid closing timelines. Whether you're searching in Seattle, Bellevue, or surrounding communities, our focus on education and transparency ensures you make informed decisions aligned with your long-term financial goals.