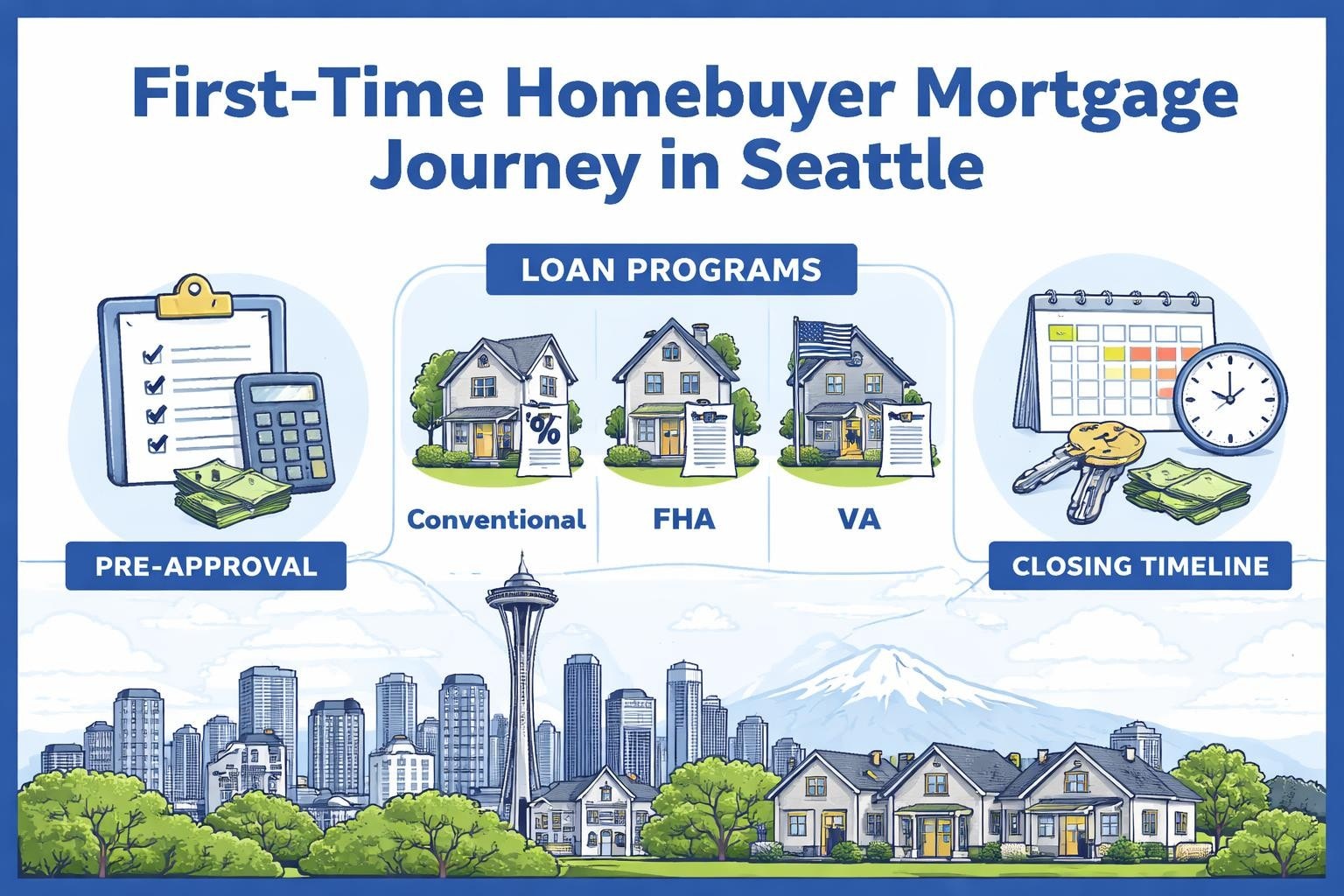

Buying a home in the Greater Seattle area demands more than just securing a loan. It requires strategic guidance through complex qualification criteria, competitive offers, and rapidly changing market conditions. A qualified mortgage advisor brings expertise that transforms the financing process from overwhelming to manageable, helping buyers in Seattle, Bellevue, Shoreline, and surrounding communities make confident decisions. Whether you're purchasing your first home in Lynnwood or refinancing investment property in Mill Creek, working with an experienced professional can mean the difference between securing your ideal property and missing the opportunity entirely.

What a Mortgage Advisor Does for Seattle Homebuyers

A mortgage advisor serves as your dedicated financing strategist throughout the homebuying process. Unlike automated online platforms that offer generic rate quotes, a professional advisor evaluates your complete financial picture to recommend loan programs that align with your specific goals.

Core Responsibilities and Services

Professional mortgage advisors provide comprehensive support that extends far beyond rate shopping. They analyze income documentation, review credit profiles, and identify opportunities to strengthen your qualification before you even start house hunting.

Key services include:

- Pre-qualification and pre-approval letter preparation for competitive Seattle markets

- Detailed analysis of conventional, FHA, VA, and jumbo loan options

- Strategic guidance on down payment requirements and reserve planning

- Coordination with underwriting teams to ensure smooth processing

- Rate lock timing recommendations based on market conditions

- Closing cost negotiation and lender credit strategies

For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, advisors specialize in qualifying complex compensation packages. This includes evaluating restricted stock units (RSUs), bonuses, and equity compensation that traditional lenders might overlook or undervalue.

Qualification Expertise for Complex Income

Many Seattle-area buyers work in technology, healthcare, or professional services with compensation structures that extend beyond base salary. A skilled mortgage advisor knows how to document and present this income to maximize your purchasing power.

Stock options typically require two years of history to count toward qualification, but experienced advisors understand which lenders accept shorter timeframes. For buyers in Redmond or Kirkland employed by major tech companies, this expertise directly impacts how much home you can afford.

| Income Type | Standard Requirement | Advanced Strategy |

|---|---|---|

| Base Salary | Current employment verification | Projected increases for job changes |

| RSUs/Stock | 2-year history | 1-year with specific underwriters |

| Bonuses | 2-year average | Current year if consistent pattern |

| Commission | 2-year tax return average | Year-to-date trending analysis |

According to industry trends for 2025, mortgage professionals increasingly focus on creative income qualification strategies as borrower profiles become more diverse.

Choosing the Right Mortgage Advisor in Greater Seattle

Not all mortgage advisors offer the same level of service or access to loan programs. The professional you choose directly impacts your interest rate, closing timeline, and overall experience.

Experience and Market Knowledge

Look for advisors with deep roots in the Seattle market who understand local property values, competitive offer dynamics, and neighborhood-specific considerations. Someone familiar with Everett market conditions brings different insights than an advisor who primarily works in downtown Seattle.

Critical qualifications to verify:

- Active NMLS license with clean regulatory history

- Minimum five years of experience in your target market

- Proven track record with your specific loan type (jumbo, FHA, VA)

- Relationships with local real estate agents and escrow companies

- Technology platform for real-time application updates

The mortgage advisor profession requires specific licensing, continuing education, and adherence to regulatory standards that protect consumers throughout the lending process.

Communication Style and Availability

Your mortgage advisor should provide clear explanations without industry jargon that confuses rather than clarifies. They should also be accessible when you have questions, especially during time-sensitive situations like multiple offer scenarios.

In competitive Seattle neighborhoods like Lake Forest Park or Shoreline, offers often require same-day responses. Your advisor needs the operational capacity to deliver updated pre-approval letters, adjust loan amounts, and communicate with listing agents on tight deadlines.

Understanding Loan Program Options Through Your Advisor

A primary value that mortgage advisors provide is translating complex loan program guidelines into actionable recommendations based on your situation.

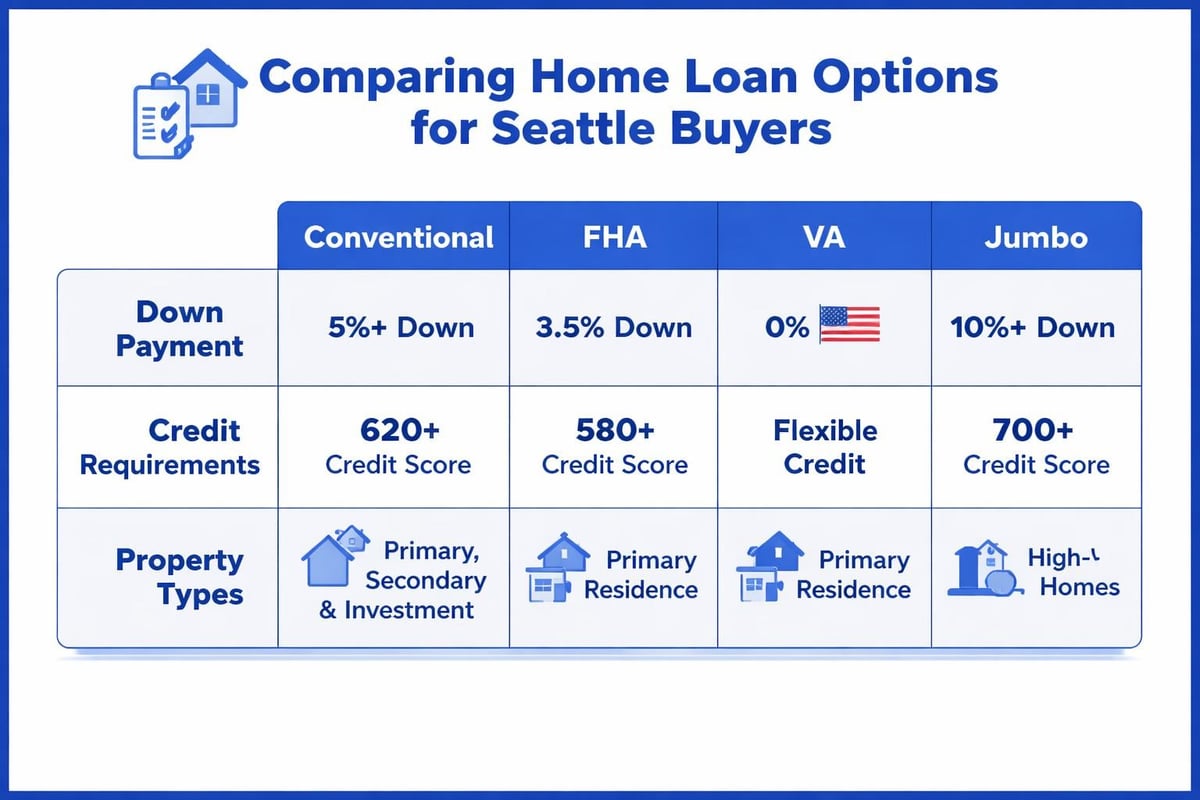

Conventional Loans for Strong Credit Profiles

Conventional financing dominates the Seattle market for buyers with credit scores above 700 and down payments of at least 5%. These loans offer flexibility in property types, loan amounts, and term options.

Conventional loan advantages:

- No upfront mortgage insurance premium

- PMI removal option once reaching 20% equity

- Higher loan limits for jumbo properties

- Flexibility for investment properties and second homes

For a $900,000 home in Bellevue, a conventional loan with 10% down provides competitive rates without the limitations of government-backed programs. Your mortgage advisor structures the transaction to minimize monthly costs while preserving cash reserves.

Government-Backed Programs for Qualified Buyers

FHA, VA, and USDA loans serve specific buyer segments with unique benefits. Veterans purchasing in Mill Creek qualify for zero-down VA financing with no monthly mortgage insurance. First-time buyers in eligible Everett neighborhoods might access USDA programs with minimal down payments.

A knowledgeable advisor identifies which programs align with your eligibility and property selection. They also navigate the additional requirements these loans impose, such as property condition standards and occupancy rules.

Jumbo Financing for Higher-Value Properties

Seattle's median home price frequently exceeds conforming loan limits, making jumbo financing essential for many buyers. These loans require more stringent qualification but offer competitive rates for well-qualified borrowers.

| Loan Type | 2026 Loan Limit (King County) | Minimum Credit | Typical Down Payment |

|---|---|---|---|

| Conforming | $806,500 | 620 | 3% – 5% |

| High-Balance | $806,500 – $1,209,750 | 680 | 5% – 10% |

| Jumbo | $1,209,750+ | 700 | 10% – 20% |

According to the 2025 mortgage industry outlook, jumbo lending continues expanding as more lenders enter the space with competitive programs.

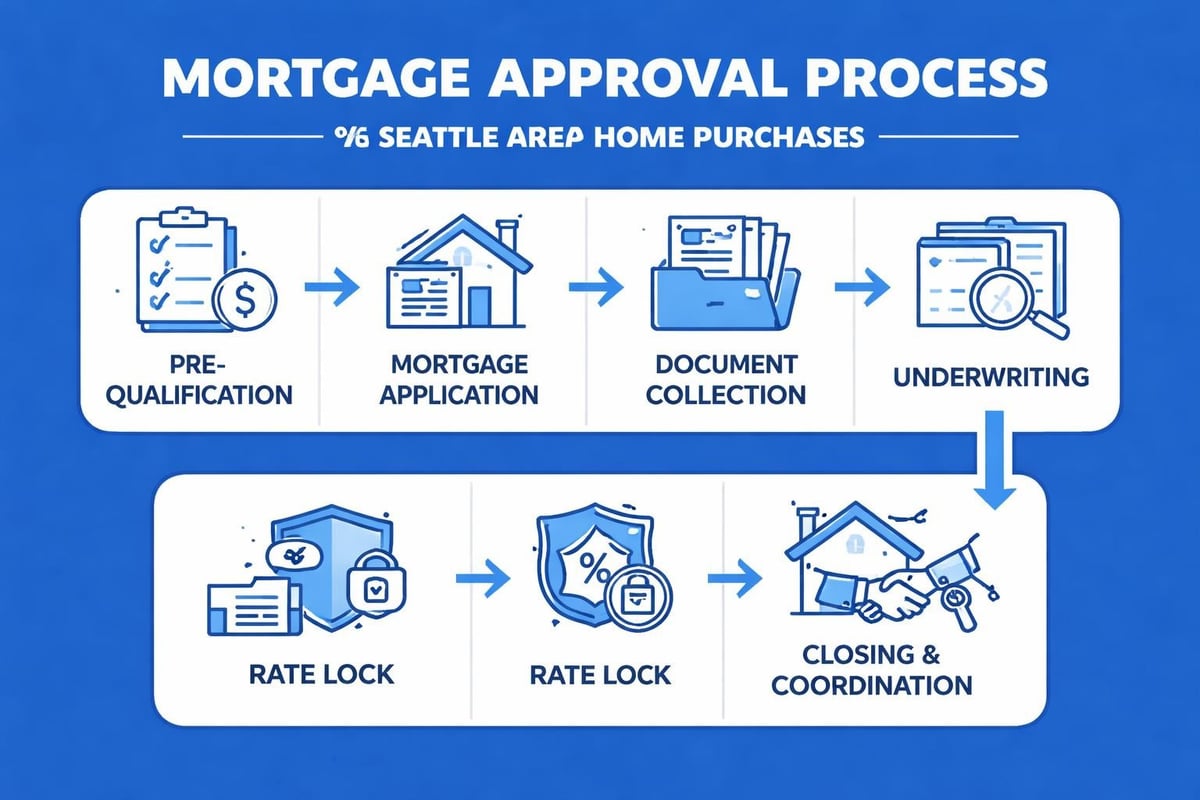

The Application and Approval Process

Working with a mortgage advisor streamlines the path from initial consultation to closing day. Understanding each phase helps you prepare documentation and manage expectations.

Initial Consultation and Strategy Session

Your first meeting establishes the foundation for your entire transaction. A thorough advisor asks detailed questions about your financial goals, timeline, and property preferences before recommending specific loan structures.

Topics covered in initial consultations:

- Current income, assets, and debt obligations

- Credit history review and improvement opportunities

- Down payment source and seasoning requirements

- Property type preferences and location priorities

- Timeline for purchase and any contingencies

For buyers in Lynnwood or Shoreline considering new construction, timing strategies differ significantly from resale purchases. Your advisor coordinates construction loan details with your builder's timeline and permanent financing conversion.

Documentation and Underwriting Coordination

Modern mortgage applications require extensive documentation, but experienced advisors know exactly what underwriters need. They request specific items upfront rather than creating frustrating back-and-forth requests during processing.

Standard documentation requirements:

- Two years of W-2 forms and tax returns

- Recent pay stubs covering 30-day period

- Two months of bank statements for all accounts

- Explanations for any large deposits or withdrawals

- Credit authorization and disclosure signatures

Tech professionals with equity compensation should gather RSU vesting schedules, stock award agreements, and year-to-date statements showing consistent income patterns. Your mortgage advisor packages this information to meet specific underwriter requirements for alternative income sources.

The mortgage market trends entering 2025 show increased scrutiny on income verification and asset sourcing, making proper documentation more critical than ever.

Rate Lock Strategy and Closing Coordination

Interest rates fluctuate daily, and timing your rate lock requires market knowledge and strategic thinking. Some buyers lock immediately upon contract acceptance, while others float for better pricing in declining rate environments.

Your mortgage advisor monitors market conditions and recommends optimal lock timing based on your specific transaction. For purchase contracts with 30-day close deadlines common in Seattle's competitive market, early locks provide certainty even if rates decrease slightly.

Working With Mortgage Advisors in Competitive Markets

Seattle's housing market demands financing expertise that goes beyond standard lending practices. Buyers face multiple offer situations, escalation clauses, and aggressive timelines that test even experienced professionals.

Pre-Approval Strength and Offer Competitiveness

Listing agents in desirable Bellevue or Redmond neighborhoods receive dozens of offers on well-priced properties. Your pre-approval letter's strength influences which offers sellers seriously consider.

Elements that strengthen pre-approval credibility:

- Detailed property address and specific loan amount

- Clear verification of funds and income documentation

- Direct contact information for the mortgage advisor

- Lender name recognition in the local market

- Minimal or no financing contingency language

Some mortgage advisors offer verified approval programs that include complete underwriting before you even find a property. This positions your offer as essentially cash-equivalent in seller perception.

Appraisal Gap Coverage and Financing Contingencies

When you offer above asking price in competitive situations, appraisal gaps create financing challenges. If a $850,000 offer on a Kirkland home appraises at $820,000, you need to cover the $30,000 difference or renegotiate.

A strategic mortgage advisor discusses appraisal gap scenarios before you write offers, ensuring you understand cash requirements if comparable sales don't support your offer price. They also coordinate with appraisers to provide relevant comparable data that supports accurate valuations.

Ongoing Support Beyond Closing

The relationship with your mortgage advisor shouldn't end at closing. Market conditions change, refinancing opportunities emerge, and life circumstances evolve in ways that impact your mortgage strategy.

Portfolio Review and Refinance Analysis

Interest rate decreases of just 0.5% can justify refinancing for many homeowners. Your mortgage advisor monitors market conditions and proactively reaches out when refinancing makes financial sense for your specific situation.

For homeowners in Mill Creek or Everett who purchased during higher rate periods, refinancing in 2026's potentially lower rate environment could reduce monthly payments by hundreds of dollars. Your advisor calculates break-even periods and compares closing costs against long-term savings.

According to key industry insights for 2025, refinancing activity remains subdued but opportunities exist for strategic homeowners who purchased in recent high-rate periods.

Future Purchase Planning and Investment Strategy

Many Seattle-area homeowners eventually purchase investment properties, upgrade to larger homes, or downsize as life circumstances change. Your mortgage advisor helps you plan these transitions by analyzing qualification capacity and strategic timing.

Buying a second home in Everett while maintaining your Seattle primary residence requires careful debt-to-income management. Advisors calculate whether rental income from your current home offsets its payment for qualification purposes, expanding your purchasing power for the next property.

Common Mistakes to Avoid When Working With Advisors

Even experienced homebuyers make errors that complicate their mortgage transactions. Understanding these pitfalls helps you navigate the process more smoothly.

Making Major Financial Changes During Processing

Opening new credit cards, changing jobs, or making large purchases during your mortgage process can derail your approval. Underwriters verify employment and credit immediately before closing, and any changes trigger additional review.

Financial moves to avoid during mortgage processing:

- Applying for new credit cards or auto loans

- Making large cash deposits without documentation

- Changing employers or job titles

- Co-signing loans for family members

- Moving money between accounts without explanations

Your mortgage advisor provides clear guidance on maintaining financial stability from application through closing day. For buyers in Shoreline or Lake Forest Park with 45-day close timelines, this discipline becomes especially critical.

Focusing Solely on Interest Rate

While interest rates matter, they represent just one component of your total mortgage cost. Closing costs, lender fees, and loan structure often impact your long-term expense more than a 0.125% rate difference.

Some lenders advertise exceptionally low rates but charge thousands in origination fees or discount points. Your mortgage advisor breaks down the complete cost comparison, showing true APR and break-even analysis for different loan options.

Navigating Seattle's competitive real estate market requires more than just finding the lowest rate-it demands strategic guidance from a mortgage professional who understands your unique financial situation and goals. Whether you're purchasing in Bellevue, refinancing in Everett, or maximizing stock compensation for a jumbo loan, the right advisor transforms complexity into clarity. Mortgage Reel serves Greater Seattle homebuyers with transparent education, proactive communication, and 25+ years of proven expertise that helps clients make confident financing decisions from pre-approval through closing.