A VA loan home loan represents one of the most powerful benefits available to military service members, veterans, and eligible surviving spouses purchasing property in the Greater Seattle area. With zero down payment requirements, no private mortgage insurance, and competitive interest rates, this government-backed financing option opens doors to homeownership that conventional loans simply cannot match. For Seattle-area veterans working at Joint Base Lewis-McChord or transitioning tech professionals landing roles at Amazon or Microsoft, understanding how to leverage a VA loan home loan can mean the difference between renting indefinitely in expensive markets like Bellevue and Redmond or building long-term wealth through real estate.

Understanding VA Loan Home Loan Eligibility Requirements

The VA home loan program provides guaranteed financing to those who have served our country, but specific eligibility criteria determine who qualifies. Unlike conventional mortgages that rely solely on credit scores and income verification, VA loan home loan eligibility centers on your service record and discharge status.

Active Duty Service Members

Active duty personnel become eligible after 90 consecutive days of service during wartime or 181 days during peacetime. This timeline allows relatively new service members to access homeownership benefits earlier than most civilian financing options permit. For active duty members stationed at Naval Station Everett or Coast Guard facilities in Seattle, this means you could qualify for a VA loan home loan while still serving.

Veterans and Discharged Personnel

Veterans must meet minimum service requirements that vary based on when you served. Those who served during the Gulf War (August 2, 1990 to present) need 24 continuous months or the full period for which called to active duty. Service members with discharge statuses other than dishonorable maintain eligibility regardless of separation date.

National Guard and Reserve Members

Guard and Reserve members qualify after six years of service or if called to active duty for qualifying periods. For Washington State National Guard members training at Camp Murray near Lakewood, understanding these nuances helps determine when you can pursue a VA loan home loan for properties in Shoreline or Lake Forest Park.

Key Benefits That Set VA Loan Home Loans Apart

The competitive advantage of a VA loan home loan extends far beyond simple government backing. These benefits create real financial opportunities, particularly in high-cost markets like Seattle where median home prices exceeded $825,000 in 2026.

Zero Down Payment Advantage

Perhaps the most transformative benefit, eligible borrowers can finance 100% of a home's purchase price without any down payment. In Seattle's competitive market, this means a veteran purchasing a $700,000 home in Mill Creek saves $140,000 in upfront cash compared to a conventional loan requiring 20% down.

No Private Mortgage Insurance

Conventional loans require PMI when down payments fall below 20%, often adding $200 to $400 monthly to mortgage payments. A VA loan home loan eliminates this expense entirely, creating immediate monthly savings that compound over the life of the loan.

Competitive Interest Rates

VA loans consistently offer lower interest rates than conventional financing because the Department of Veterans Affairs guarantees a portion of each loan. This government backing reduces lender risk, translating directly into better rates for borrowers. Even a 0.25% rate difference on a $600,000 Lynnwood property saves approximately $90 monthly and over $32,000 across a 30-year term.

| Benefit Category | VA Loan Home Loan | Conventional Loan | Monthly Savings Example |

|---|---|---|---|

| Down Payment | 0% | 20% ($140,000) | N/A |

| PMI Requirement | None | $250-400/month | $325/month |

| Interest Rate | 6.25% (example) | 6.50% (example) | $90/month |

| Total Monthly Advantage | – | – | $415/month |

Lenient Credit Requirements

While VA loan guidelines don't specify minimum credit scores, most lenders work with borrowers starting around 580-620 FICO scores. This flexibility helps veterans with rebuilding credit histories access homeownership when conventional lenders might decline their applications.

VA Loan Home Loan Limits and Entitlement

Understanding entitlement determines how much you can borrow with a VA loan home loan without requiring a down payment. The VA changed its approach to loan limits in 2020, creating new opportunities for borrowers in expensive markets.

Basic Entitlement and Bonus Entitlement

Every eligible veteran receives basic entitlement of $36,000, which lenders multiply by four to determine the maximum zero-down loan amount in most markets. Combined with bonus entitlement, veterans with full entitlement can purchase homes at any price point without down payments, provided they qualify based on income and debt-to-income ratios.

For Seattle-area properties exceeding conforming loan limits, this becomes particularly valuable. A veteran purchasing a $900,000 home in Bellevue with full entitlement faces no down payment requirement despite the high price point, assuming income qualification supports the purchase.

Restoring and Reusing Entitlement

Veterans can use VA loan benefits multiple times throughout their lives. Entitlement restores automatically when you sell a property and pay off the VA loan. This reusability allows military families to relocate from Seattle to other duty stations and back again, using VA financing each time.

Some scenarios allow using entitlement on multiple properties simultaneously. Veterans with remaining entitlement after one VA loan can secure a second VA loan home loan, ideal for those purchasing rental properties or relocating while retaining their previous home.

The VA Loan Home Loan Application Process

Navigating the VA home-buying process requires systematic steps that begin before you ever tour properties. Understanding this sequence helps Seattle-area veterans move efficiently from eligibility verification through closing.

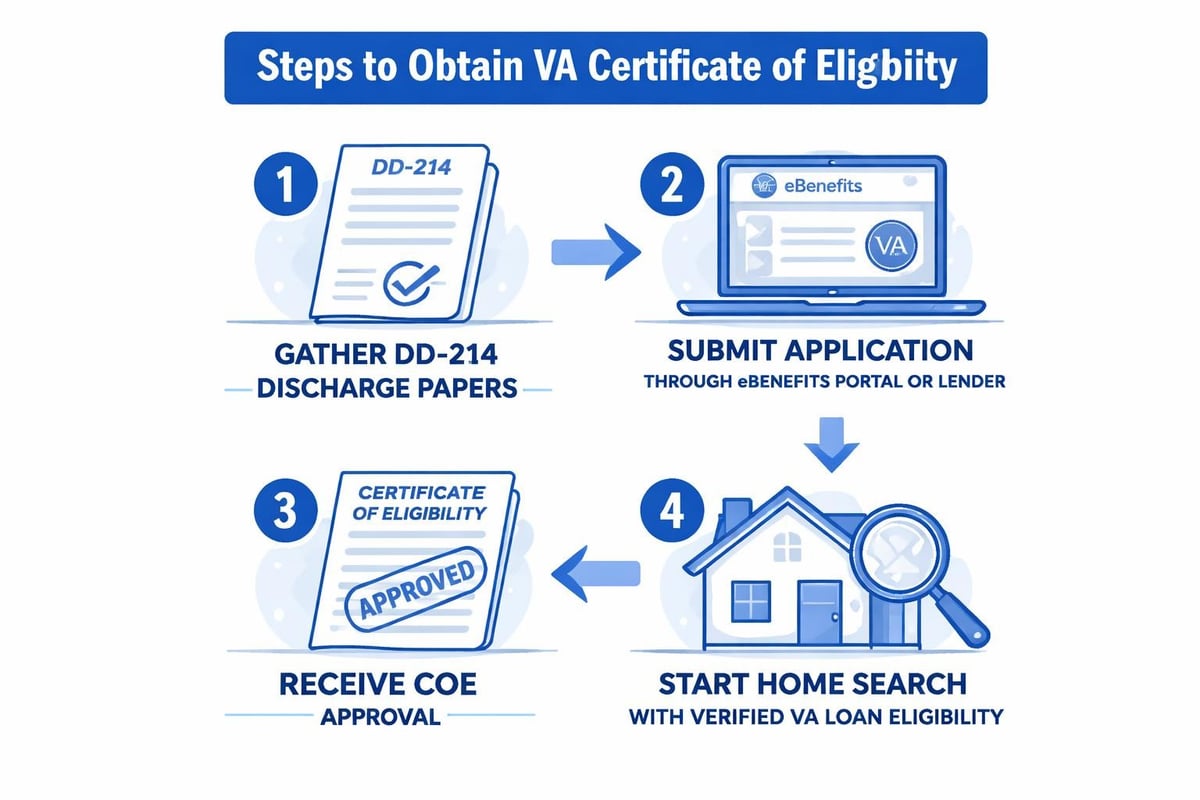

Step One: Obtain Your Certificate of Eligibility

The Certificate of Eligibility (COE) proves to lenders that you meet VA qualification standards. You can request your COE through three methods:

- eBenefits Portal: The fastest option for most veterans with DD-214 information already in the VA system

- Through Your Lender: Experienced VA lenders can pull COEs directly during pre-approval

- Mail Application: VA Form 26-1880 submitted with service documentation

For Seattle-area veterans, working with a licensed mortgage broker experienced in VA loans often streamlines this process, as they can obtain COEs while simultaneously evaluating your financial profile.

Step Two: Get Pre-Approved

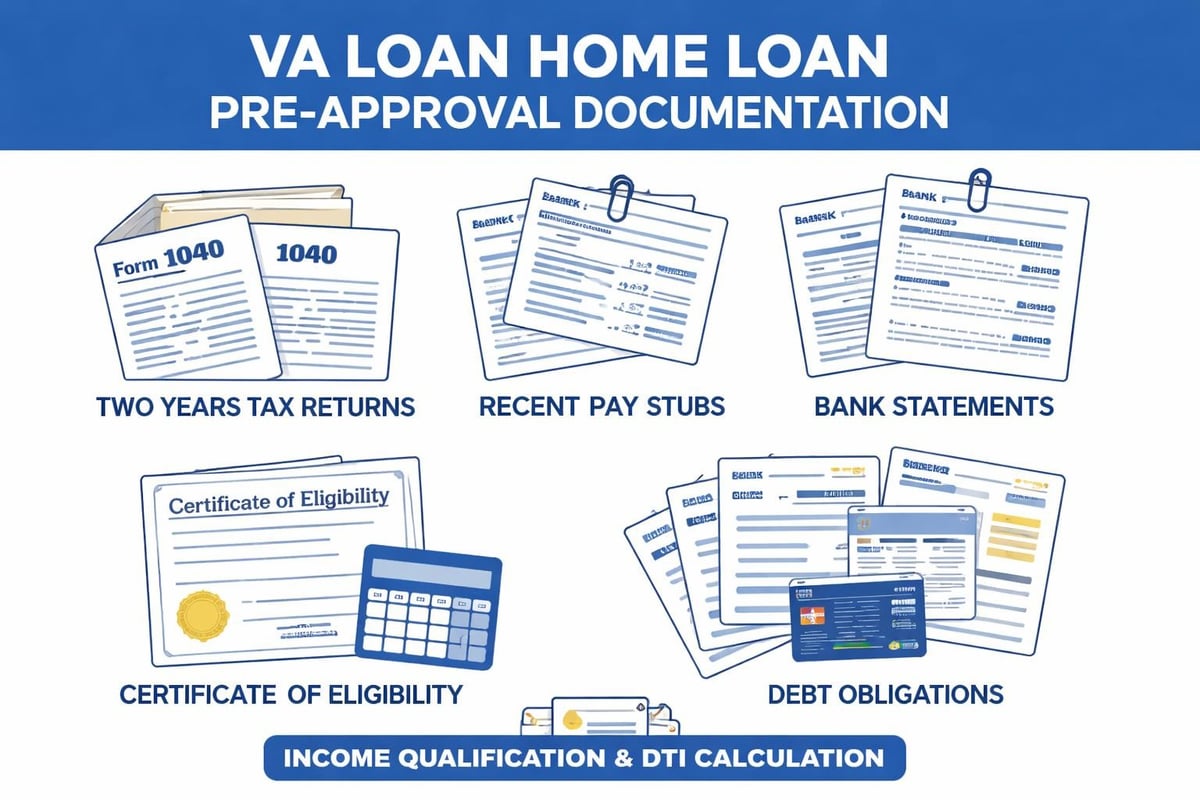

Pre-approval with a knowledgeable lender establishes your budget and strengthens offers in competitive markets. This step involves comprehensive income verification, credit review, and debt analysis to determine your maximum purchase price.

Tech professionals in Seattle with RSU compensation or stock options should work with lenders experienced in qualifying these income types. Understanding how to qualify complex compensation maximizes buying power when Amazon or Microsoft equity represents significant earning potential.

Step Three: Home Search and Offer

Armed with pre-approval, you can confidently tour properties knowing your financing is secured. VA loan home loan requirements mandate properties meet minimum property standards, ensuring homes are safe, sound, and sanitary.

Working with real estate agents familiar with VA transactions helps navigate Seattle's competitive market. These professionals understand VA appraisal requirements and can identify potential issues before you submit offers.

Step Four: VA Appraisal

The VA appraisal serves dual purposes: establishing fair market value and ensuring the property meets VA minimum property requirements. This protects veterans from overpaying or purchasing homes with significant defects.

Appraisers evaluate structural integrity, roofing condition, heating systems, and water quality. Properties in older Seattle neighborhoods like Shoreline may require repairs before VA approval, which sellers can address or buyers can negotiate.

Step Five: Underwriting and Closing

Once the appraisal clears, your loan moves to underwriting where lenders verify all documentation and ensure guideline compliance. Clear communication with your lender during this phase prevents delays from missing documents or clarification requests.

Closing on a VA loan home loan involves signing final documents, paying closing costs, and receiving your keys. While VA loans limit certain fees lenders can charge veterans, budgeting 1-3% of the purchase price for closing costs remains prudent.

VA Funding Fee and Closing Costs

The VA funding fee helps sustain the loan program for future generations of veterans. This one-time charge varies based on service type, down payment amount, and whether you're a first-time or subsequent VA loan user.

Understanding Funding Fee Rates

| Service Category | First-Time Use | Subsequent Use | With 5% Down | With 10% Down |

|---|---|---|---|---|

| Regular Military | 2.15% | 3.30% | 1.50% | 1.25% |

| Reserves/Guard | 2.15% | 3.30% | 1.50% | 1.25% |

| Veterans with disability compensation receive complete exemptions from funding fees, creating additional savings for those with service-connected conditions. |

The funding fee can be rolled into your loan amount rather than paid upfront. On a $650,000 Everett property, the $13,975 funding fee adds approximately $84 to your monthly payment when financed over 30 years-a manageable increase that preserves cash for moving expenses and home improvements.

VA Loan Closing Cost Protections

VA regulations limit which closing costs veterans can pay, protecting borrowers from excessive fees. Sellers can pay all closing costs, and it's common in veteran-friendly markets for negotiated seller concessions to cover these expenses entirely.

Prohibited veteran-paid costs include:

- Lender attorney fees

- Buyer's real estate agent commission

- Document preparation fees charged by lenders

- Application or processing fees beyond 1% of loan amount

Refinancing Options With VA Loan Home Loans

The various VA loan types extend beyond purchase financing to include powerful refinancing tools that help veterans lower rates or access home equity.

Interest Rate Reduction Refinance Loan (IRRRL)

The IRRRL, commonly called a "VA streamline refinance," allows veterans to refinance existing VA loans into lower rates with minimal documentation. This option requires no appraisal, limited income verification, and can close in as few as two weeks.

When Seattle mortgage rates drop significantly below your current rate, an IRRRL can reduce monthly payments substantially. For a veteran with a $500,000 remaining balance at 7.0%, refinancing to 6.25% saves approximately $250 monthly or $90,000 over the remaining loan term.

Cash-Out Refinance

VA cash-out refinancing converts home equity into cash while refinancing into a new VA loan. Unlike the IRRRL, this option requires full income qualification and a VA appraisal but allows borrowing up to 100% of your home's current value.

Veterans in appreciating markets like Mill Creek or Lake Forest Park who purchased several years ago often have substantial equity. A homeowner who bought at $450,000 and now owns a property worth $650,000 could access up to $200,000 in equity through VA cash-out refinancing for debt consolidation, home improvements, or investment opportunities.

Common VA Loan Home Loan Misconceptions

Several myths surrounding VA loans persist despite decades of successful program operation. Correcting these misunderstandings helps veterans make informed decisions.

Myth: VA Loans Take Longer to Close

Modern VA loan processing matches conventional timelines when working with experienced lenders. Efficient underwriting and appraisal ordering can close VA loans in 21-30 days, with some specialized lenders achieving nine-business-day closings in optimal conditions.

Myth: Sellers Won't Accept VA Offers

While some sellers harbor concerns about VA appraisal requirements, educated real estate professionals recognize VA loans close reliably. In veteran-friendly markets like those near Joint Base Lewis-McChord, VA offers receive equal consideration. Including strong pre-approval letters and offering competitive terms overcomes most seller hesitations.

Myth: You Can Only Use VA Benefits Once

Veterans can use VA loan benefits repeatedly throughout their lives. Whether relocating from Seattle to other duty stations or upgrading to larger properties as families grow, the ability to restore and reuse entitlement creates lifetime flexibility.

Combining VA Loans With Seattle Market Strategies

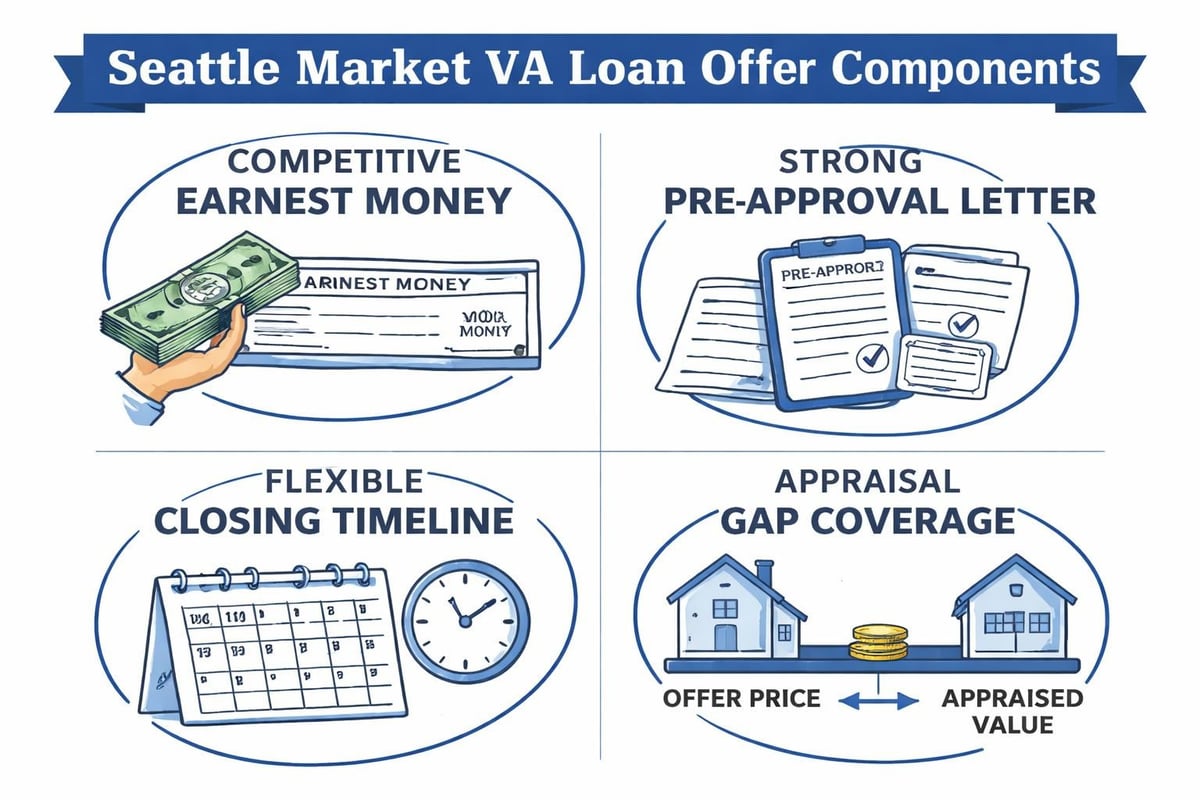

Seattle's competitive real estate market requires strategic approaches that maximize your VA loan home loan advantages while positioning offers competitively against conventional buyers.

Waiving Appraisal Contingencies Strategically

In multiple-offer scenarios, some buyers waive appraisal contingencies to strengthen offers. Veterans should approach this carefully, as VA appraisals protect against overpaying. Consider this strategy only when:

- You have cash reserves to cover potential appraisal gaps

- Recent comparable sales support the offer price

- Your agent confirms the property likely meets VA minimum standards

Offering Competitive Earnest Money

Substantial earnest money deposits demonstrate commitment without requiring down payments. Veterans purchasing in Redmond or Kirkland can offer 2-3% earnest money deposits, showing sellers their serious intent while preserving the zero-down VA benefit.

Pre-Inspections

Ordering pre-listing inspections before submitting offers identifies potential VA appraisal issues early. This proactive approach allows you to address concerns with sellers upfront or adjust offers accordingly, preventing surprises during the formal VA appraisal process.

Working With VA-Experienced Lenders

Selecting the right lender dramatically impacts your VA loan home loan experience. Not all lenders maintain equal expertise with VA guidelines, and this knowledge gap can create frustration during critical transaction phases.

Questions to Ask Potential Lenders

When evaluating mortgage brokers or lenders for your VA loan, consider these essential questions:

- What percentage of your annual loan volume consists of VA loans?

- Can you close VA loans in 30 days or less consistently?

- How do you handle VA appraisal issues when they arise?

- Do you have experience qualifying military allowances and benefits as income?

- What's your average response time for application questions?

Lenders processing substantial VA loan volumes understand nuanced guidelines and navigate challenges efficiently. For Seattle-area tech veterans, finding lenders who understand both VA requirements and complex compensation structures ensures smooth transactions when RSUs or stock options comprise significant income.

Local Market Knowledge Matters

VA loan regulations remain consistent nationally, but local market conditions vary dramatically. A lender operating primarily in low-cost markets may lack experience with Seattle's price points, competitive offer environments, and specific King County property considerations.

Choosing Seattle-based mortgage professionals provides advantages beyond VA expertise. Local lenders understand neighborhood dynamics from Lynnwood to Everett, maintain relationships with area appraisers, and can provide realistic timelines based on current local market conditions.

VA Loan Home Loan Property Requirements

The VA establishes minimum property requirements ensuring homes purchased with VA financing are safe, structurally sound, and sanitary. Understanding these standards helps veterans identify suitable properties and avoid problematic listings.

Structural and Safety Standards

VA appraisers examine:

- Roof condition: Remaining life expectancy of at least two years

- Foundation integrity: No significant cracks or structural concerns

- Heating systems: Adequate heating for Seattle's climate throughout the home

- Electrical and plumbing: Safe, functional systems meeting local codes

- Water quality: Approved water source meeting health standards

Properties failing to meet these standards require repairs before VA loan approval. Sellers can complete repairs, buyers can negotiate credits, or transactions can terminate if issues prove too extensive.

Property Type Restrictions

VA loans can finance single-family homes, condominiums in VA-approved projects, townhomes, and multi-family properties up to four units if you'll occupy one unit. This flexibility allows veterans to house-hack, living in one unit while renting others to offset mortgage costs-a popular strategy in Seattle's rental-friendly market.

Condominiums Require Special Approval

Purchasing condominiums with VA financing requires the complex be VA-approved. This approval process examines the homeowners association's financial health, insurance coverage, and ownership distribution. Many Seattle-area condominiums maintain VA approval, but veterans should verify status before writing offers.

Special Considerations for Seattle-Area Tech Veterans

Veterans transitioning from military service to technology careers at Amazon, Microsoft, or Google face unique financial situations when pursuing VA loan home loans. Understanding how lenders evaluate tech compensation maximizes buying power.

Qualifying RSU and Stock Compensation

Restricted stock units and stock options often comprise significant portions of tech compensation packages. While some lenders hesitate to count unvested RSUs, experienced VA lenders can include this income using documented vesting schedules and historical grant patterns.

For a veteran earning $120,000 base salary plus $80,000 annually in vesting RSUs, proper income qualification could support purchasing power of $650,000-750,000 rather than limiting calculations to base salary alone.

Timing Considerations for Recent Transitions

Veterans recently hired in tech roles may have limited employment history with their civilian employer. VA guidelines allow using military income history combined with new civilian employment when careers are related or when sufficient reserves demonstrate financial stability.

Bonus Income and Variable Compensation

Annual bonuses, on-call pay, and performance incentives require two-year histories before most lenders include them in qualifying income. Veterans with consistent military special pay transitioning to civilian bonus structures should document this continuity to maximize qualification amounts.

Navigating Seattle's Competitive Neighborhoods

Different Seattle-area communities offer varying opportunities for veterans pursuing VA loan home loans. Understanding neighborhood characteristics helps target searches effectively.

Seattle Proper

Seattle's core neighborhoods present the highest price points, with median homes often exceeding $850,000. Veterans with strong income qualification or those purchasing condominiums find opportunities in areas like Northgate or Lake City, where prices moderate slightly compared to Capitol Hill or Queen Anne.

Shoreline and Lake Forest Park

These north Seattle suburbs offer excellent value for VA buyers, with single-family homes frequently priced $100,000-200,000 below Seattle proper. Strong schools, established neighborhoods, and convenient freeway access make these communities attractive for families, while prices remain accessible to military income levels.

Lynnwood and Mill Creek

Moving further north into Snohomish County creates additional affordability. Lynnwood's median home prices in 2026 hover around $650,000-$700,000, bringing them within reach for veterans earning typical military or early-career tech salaries. Mill Creek offers newer construction and master-planned communities appealing to families prioritizing modern amenities.

Everett

As the furthest north major city in the Greater Seattle metro area, Everett provides the most affordable entry points for VA loan home loans. With median prices around $550,000-$600,000, veterans can access single-family homes with yards while maintaining commute accessibility to Seattle employment centers via I-5 or transit options.

Understanding VA loan home loan benefits and requirements empowers Seattle-area veterans to make confident homebuying decisions in one of the nation's most competitive real estate markets. Whether you're an active duty service member stationed locally, a veteran working in tech, or a retired military professional ready to establish roots, VA financing provides unmatched advantages that make homeownership accessible and affordable. Keith Akada at Mortgage Reel brings 25+ years of mortgage expertise specifically serving Seattle-area veterans, combining deep VA loan knowledge with local market insights to help military homebuyers navigate complex transactions confidently. With the ability to close loans quickly and proven experience maximizing buying power for tech professionals with complex compensation, Keith provides the strategic guidance veterans deserve when leveraging their hard-earned benefits.