Understanding how to apply for mortgage loan financing represents one of the most significant financial decisions you'll make as a Seattle-area homebuyer. Whether you're purchasing your first condo in Bellevue, upgrading to a larger home in Redmond, or investing in property across Kirkland, the mortgage application process requires careful preparation and strategic planning. With Seattle's competitive real estate market and the unique financial profiles of tech professionals working at Amazon, Microsoft, and Google, knowing exactly what to expect can streamline your path to homeownership and position you for success.

Understanding the Mortgage Application Foundation

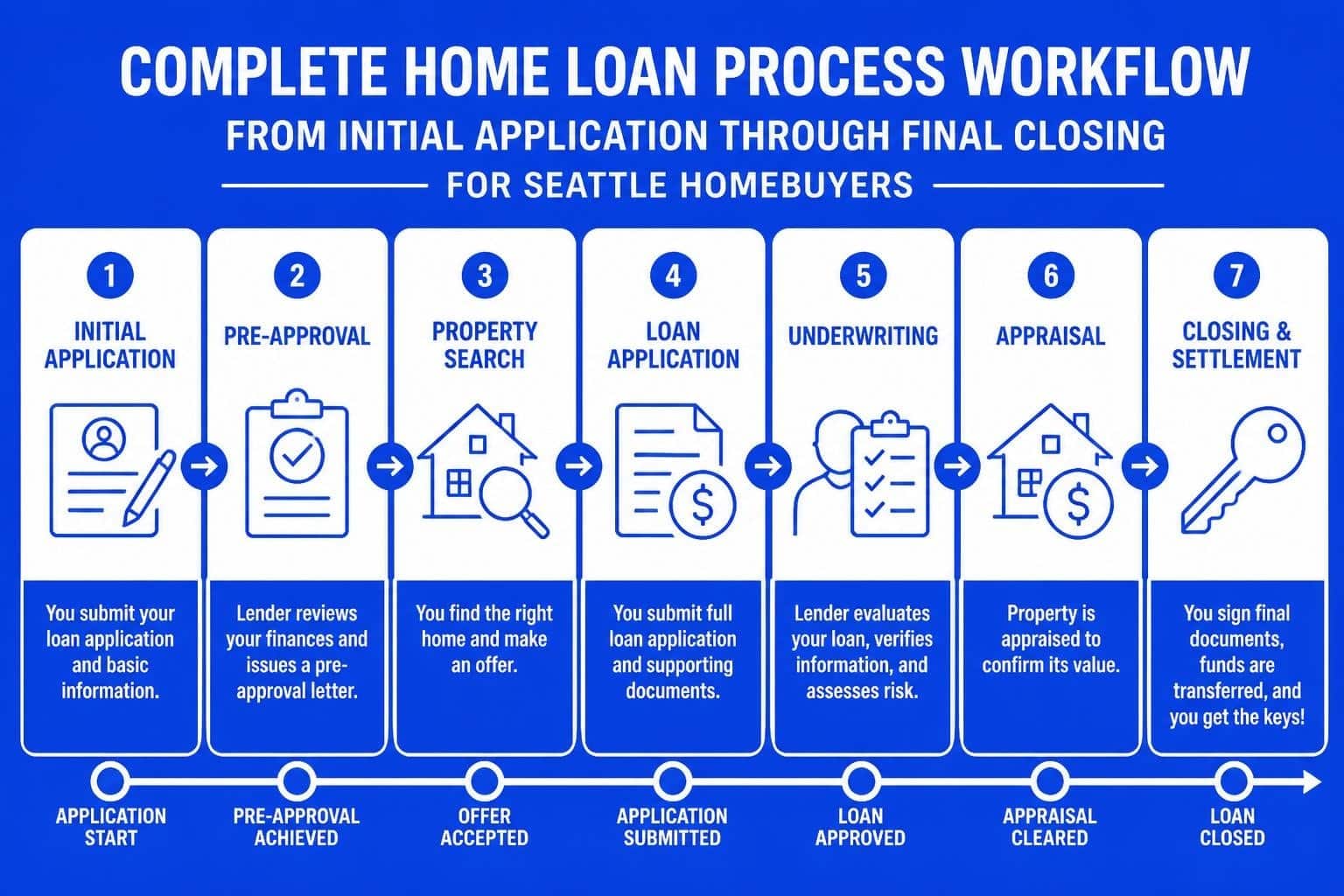

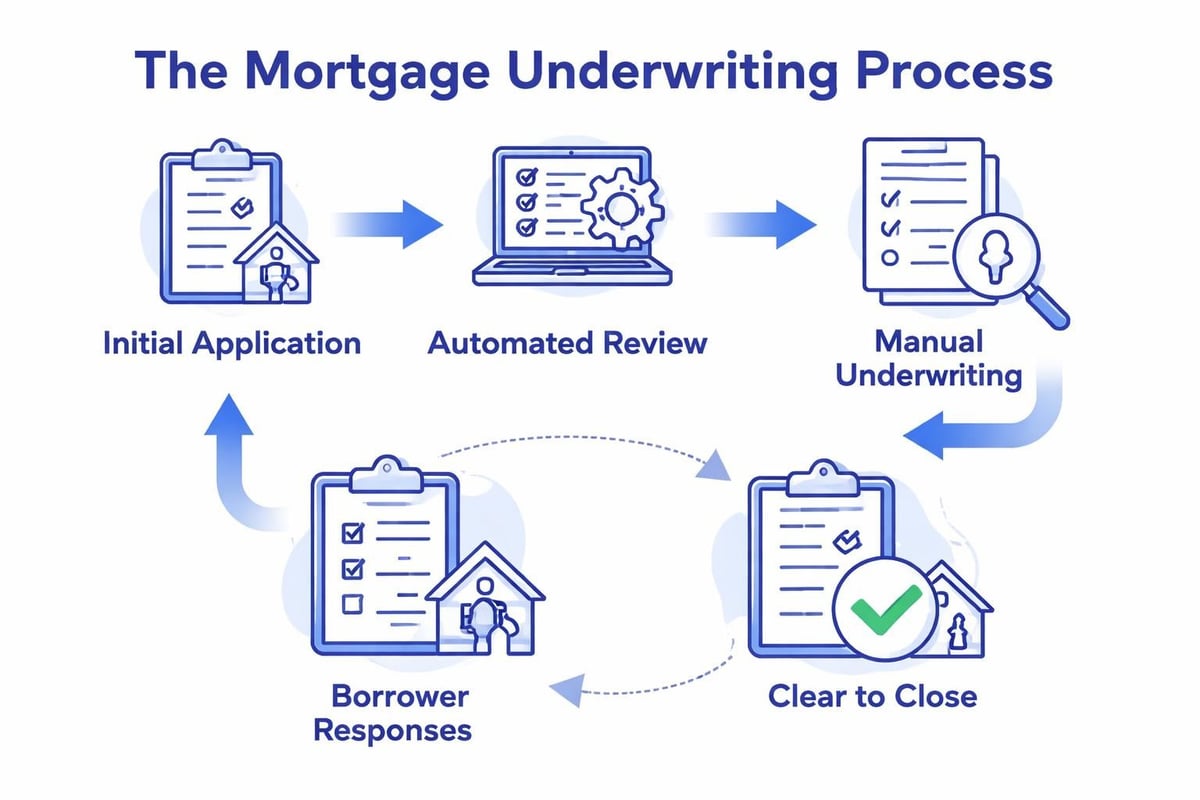

When you apply for mortgage loan financing, you're initiating a formal evaluation process where lenders assess your ability to repay borrowed funds over an extended period. This evaluation examines multiple aspects of your financial life, from employment history to credit worthiness, debt obligations, and asset reserves.

The application process typically involves three primary phases:

- Pre-application preparation and documentation gathering

- Formal application submission and initial review

- Underwriting, verification, and final approval

Each phase demands specific information and documentation. The Consumer Financial Protection Bureau outlines six essential pieces of information you'll need to provide when starting your mortgage application, including income verification, employment details, and asset documentation.

Why Seattle Borrowers Face Unique Considerations

Seattle's housing market presents distinct challenges that influence how you should approach your mortgage application. Property values in Seattle, Shoreline, and surrounding communities often exceed national averages, meaning many qualified buyers require jumbo loan financing beyond conventional conforming limits.

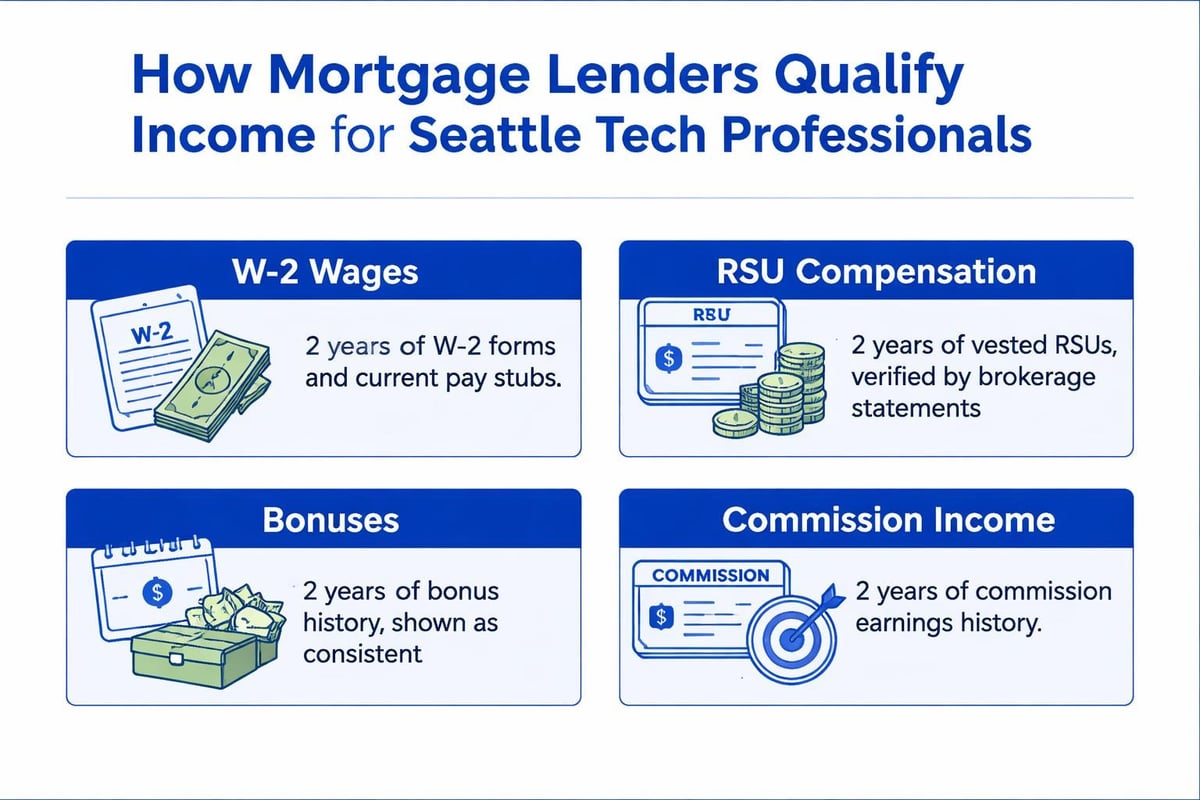

Tech professionals face additional complexity. Stock-based compensation including RSUs, ESPP shares, and annual bonuses can represent 30-50% of total income for Seattle-area technology workers. Properly documenting and qualifying this income requires specialized knowledge and strategic presentation during the application process.

Preparing to Apply for Mortgage Loan Financing

Preparation distinguishes successful applications from those that encounter delays, requests for additional documentation, or unexpected denials. Before you formally apply for mortgage loan approval, invest time in organizing your financial documentation and understanding your borrowing position.

Documentation Checklist for Seattle Borrowers

Gathering documents before starting your application accelerates the timeline and demonstrates preparedness to your loan officer and underwriter.

| Document Category | Required Items | Special Notes for Tech Professionals |

|---|---|---|

| Income Verification | Two years W-2s, recent pay stubs | Include RSU/equity award statements |

| Tax Returns | Complete returns with all schedules | Show stock income and capital gains |

| Asset Statements | 2-3 months bank/investment accounts | Document vested but unsold RSUs |

| Employment | Verification of employment letter | Startup equity requires special documentation |

| Credit | Lender will pull directly | Review your own report first |

| Property | Purchase agreement (if applicable) | Seattle market often requires quick closings |

For borrowers in Lynnwood or Mill Creek purchasing homes under $1.4 million, conventional conforming loans typically require less extensive documentation than jumbo products. However, thorough preparation benefits all applicants regardless of loan size.

Credit Profile Optimization

Your credit score directly impacts both approval likelihood and the interest rate you'll receive. Most conventional loans require minimum FICO scores of 620, though competitive rates typically require scores above 700.

Strategic credit optimization steps include:

- Reviewing credit reports for errors 90 days before applying

- Reducing credit card balances below 30% of available limits

- Avoiding new credit applications during your home search

- Maintaining consistent payment history on all accounts

Seattle's competitive market often requires rapid response when you find the right property. Having your credit optimized months before you begin house hunting positions you to act quickly when opportunity arises.

The Formal Application Process

When you're ready to apply for mortgage loan approval, you'll work directly with your loan officer to complete a comprehensive application. This document, formally known as the Uniform Residential Loan Application (Form 1003), captures detailed information across multiple categories.

Application Components Explained

Modern mortgage applications request information that allows lenders to assess risk and comply with federal lending regulations. Understanding what lenders evaluate during the approval process helps you present your financial profile strategically.

Personal and Property Information:

The application begins with basic identifying information including Social Security number, date of birth, current address, and contact details. You'll also provide property information including address, purchase price, and intended occupancy status. For Seattle borrowers, clearly indicating whether you're purchasing a primary residence, second home, or investment property affects both rates and qualification requirements.

Employment and Income Details:

This section documents your employment history for the past two years, including employer names, positions, dates of employment, and income earned. Seattle tech professionals should be prepared to explain job transitions, especially moves between companies or promotions that significantly increased compensation.

Stock-based compensation requires special attention. Your loan officer will analyze RSU vesting schedules, historical stock sales, and company equity agreements to determine qualifying income. For employees at publicly traded companies like Amazon or Microsoft, this process is more straightforward than for startup employees with illiquid equity.

Assets and Liabilities Documentation

When you apply for mortgage loan financing, lenders evaluate both what you own and what you owe. Asset documentation proves you have sufficient funds for down payment, closing costs, and cash reserves.

Acceptable asset sources include:

- Checking and savings accounts

- Investment accounts (stocks, bonds, mutual funds)

- Retirement accounts (401k, IRA)

- Vested company stock and RSUs

- Gift funds from family members

For Everett or Lake Forest Park buyers using gift funds, proper documentation is critical. Lenders require gift letters confirming the funds are gifts, not loans, along with documentation showing the transfer from donor to recipient.

Liabilities encompass all recurring monthly debts including credit cards, student loans, auto loans, and other mortgages. Your debt-to-income ratio, calculated by dividing total monthly debts by gross monthly income, typically cannot exceed 43-50% depending on loan program and compensating factors.

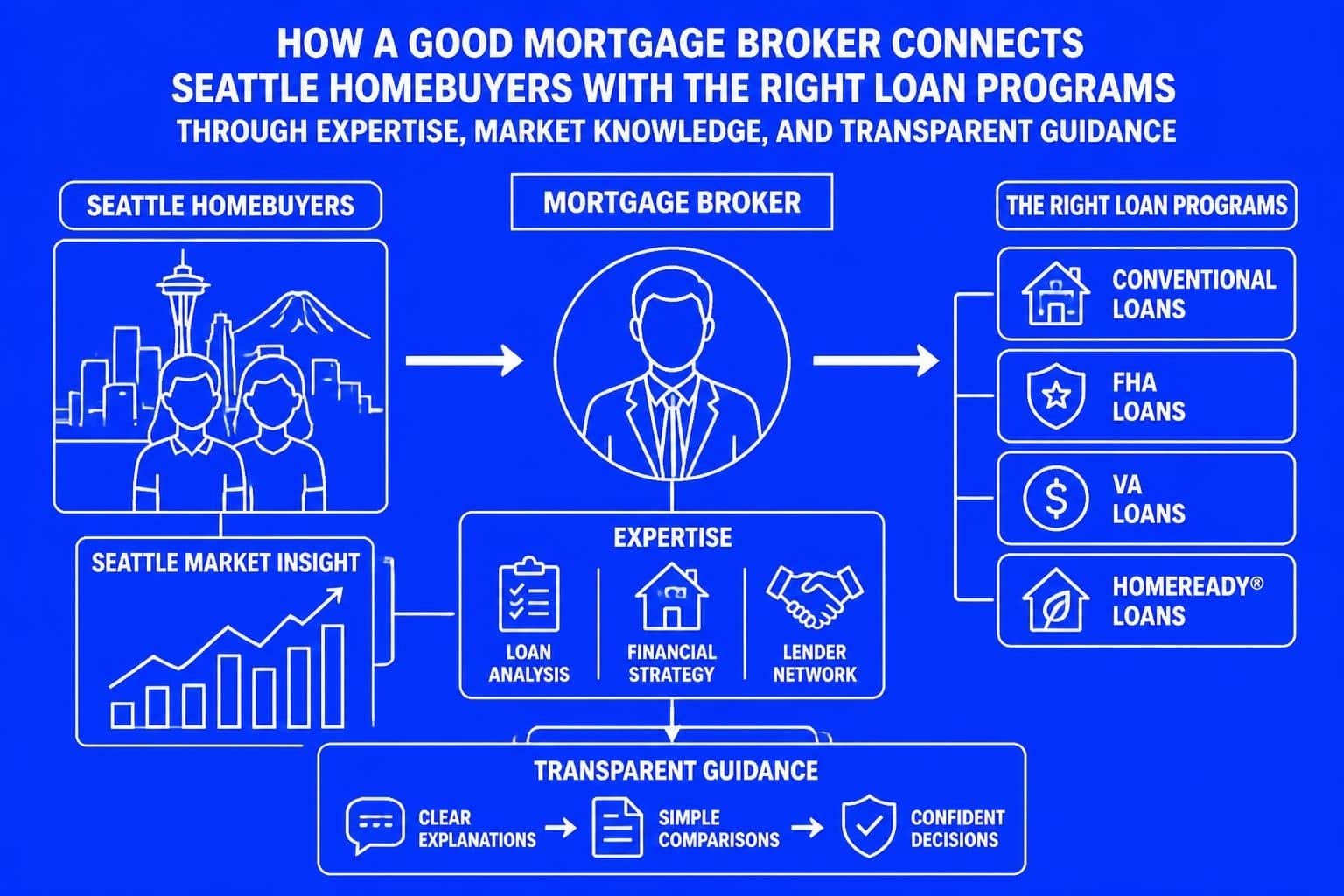

Loan Program Selection and Strategy

Before you formally apply for mortgage loan approval, you should understand which loan programs align with your financial situation and homeownership goals. Different programs offer distinct advantages depending on down payment capacity, property type, and borrower qualifications.

Conventional Loans for Seattle Buyers

Conventional conforming loans follow guidelines established by Fannie Mae and Freddie Mac. In 2026, the conforming loan limit for King County is $1,063,750 for single-family homes, though these limits adjust annually based on housing price trends.

Conventional loan advantages include:

- Down payments as low as 3% for qualified first-time buyers

- Competitive interest rates for borrowers with strong credit

- Private mortgage insurance that can be removed once you reach 20% equity

- Flexible property type approval including condos and multi-unit properties

For properties exceeding conforming limits, common throughout Seattle's core neighborhoods, jumbo loans provide financing without maximum loan amounts. These non-conforming loans typically require stronger financial profiles but offer solutions for high-value properties.

Government-Backed Loan Options

FHA, VA, and USDA loans serve specific borrower segments with unique qualification criteria and benefits.

| Loan Type | Minimum Down Payment | Credit Score | Best For |

|---|---|---|---|

| FHA | 3.5% | 580+ | Lower credit scores, smaller down payments |

| VA | 0% | No minimum | Military service members and veterans |

| USDA | 0% | 640+ | Rural/suburban properties in eligible areas |

| Conventional | 3-5% | 620+ | Strong credit, competitive rates |

While Seattle proper doesn't qualify for USDA financing, portions of Snohomish County including some areas near Mill Creek may be eligible. Researching government loan programs helps first-time buyers understand all available options.

Navigating Underwriting and Approval

After you apply for mortgage loan financing and submit your complete application, your file moves to underwriting. This phase involves detailed verification of all information provided and assessment of lending risk.

The Underwriting Timeline

Standard underwriting typically requires 3-7 business days for initial review, though complex files involving multiple income sources or unique property types may require additional time. With Fairway's advanced underwriting capabilities, qualified Seattle borrowers can potentially close in as few as 9 business days when all documentation is complete and property appraisal is timely.

Underwriters verify information through multiple channels. Employment verification contacts your employer directly to confirm position, salary, and continued employment. Income verification examines tax returns, W-2s, and pay stubs for consistency. Asset verification requires original bank statements showing sufficient funds for closing.

Responding to Conditions and Documentation Requests

Even well-prepared applications typically receive conditional approval requiring additional documentation or explanations. Responding promptly to lender requests keeps your timeline on track and demonstrates cooperation.

Common condition requests include:

- Updated pay stubs dated within 30 days of closing

- Explanation letters for large deposits or credit inquiries

- Verification of specific assets or income sources

- Additional documentation for self-employment income

- Condo project approval for properties in HOA communities

For Seattle condo buyers, project approval can add several days to your timeline. Lenders review HOA financial statements, insurance coverage, and occupancy ratios to ensure the project meets lending guidelines.

Special Considerations for Tech Professionals

Seattle's concentration of technology employers creates unique mortgage scenarios requiring specialized knowledge when you apply for mortgage loan financing. Stock compensation, job mobility, and high income-to-home-price ratios demand strategic application approaches.

Qualifying RSU and Stock Compensation

Restricted Stock Units represent deferred compensation that vests over time according to company-specific schedules. Most lenders require two-year history of RSU income to use it for qualification, though some flexibility exists for borrowers with strong compensating factors.

RSU qualification typically requires:

- Two years of tax returns showing consistent stock income

- Current vesting schedule from your employer

- Documentation of vested but unsold shares

- Evidence of stock value and liquidity

For employees who recently joined Amazon, Microsoft, or other major employers, initial RSU vesting may not provide sufficient history for full qualification. However, experienced mortgage brokers can structure applications to maximize qualifying income even with limited RSU history by emphasizing base salary, bonuses, and other documented compensation.

Jumbo Loan Strategies for High-Value Properties

Seattle's median home price consistently exceeds $800,000, pushing many qualified buyers into jumbo loan territory. These loans require stronger financial profiles but enable purchases throughout Bellevue, Redmond, and Seattle's most desirable neighborhoods.

Jumbo loans typically require:

- Minimum credit scores of 700+

- Debt-to-income ratios below 43%

- Cash reserves covering 6-12 months of mortgage payments

- Down payments of 10-20% depending on loan size

Tech professionals with substantial stock portfolios can often meet reserve requirements through investment accounts, even if liquid cash holdings are modest. Proper documentation and strategic asset presentation maximize approval likelihood.

Location-Specific Market Dynamics

Where you purchase influences both your application strategy and lender requirements when you apply for mortgage loan approval. Different communities within the Greater Seattle area present distinct considerations.

Seattle and Core Eastside Markets

Properties in Seattle, Bellevue, and Redmond typically command premium prices reflecting strong employment centers, excellent schools, and limited housing inventory. Buyers in these markets should expect:

- Higher likelihood of needing jumbo financing

- Competitive offer situations requiring proof of funds and pre-approval strength

- Condo projects requiring lender project approval

- Potentially higher property taxes and HOA fees affecting debt ratios

Emerging North End Communities

Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett offer relatively more affordable entry points while maintaining proximity to Seattle employment centers. Buyers targeting these markets may find:

- Greater inventory of homes within conforming loan limits

- More single-family options versus condos

- Slightly more negotiating leverage in purchase agreements

- Different property tax structures affecting overall housing costs

Understanding these dynamics helps you and your loan officer structure your application to highlight strengths relevant to your target market. For guidance specific to Greater Seattle neighborhoods, visit Mortgage Reel for localized expertise and market insights.

Pre-Approval Versus Pre-Qualification

Before you apply for mortgage loan financing, understanding the distinction between pre-qualification and pre-approval protects your interests and strengthens your negotiating position.

Pre-Qualification: Initial Assessment

Pre-qualification provides a preliminary estimate of borrowing capacity based on self-reported information. This informal process doesn't involve credit checks or documentation verification. While helpful for initial planning, pre-qualification letters carry limited weight in competitive Seattle markets.

Pre-Approval: Verified Commitment

Pre-approval involves submitting a complete application, providing documentation, and receiving underwriter review of your financial profile. This process results in a conditional commitment from the lender, subject only to property approval and final verification before closing.

Pre-approval advantages include:

- Demonstrated seriousness to sellers and listing agents

- Clear understanding of borrowing capacity and monthly payment

- Identification of potential issues before finding your ideal property

- Faster closing timeline once purchase agreement is signed

In Seattle's competitive market, sellers often receive multiple offers and favor buyers with strong pre-approval letters from reputable lenders. Completing this step before house hunting positions you to act decisively when you find the right property.

Common Application Mistakes to Avoid

Even experienced buyers sometimes make errors that delay approval or create complications when they apply for mortgage loan financing. Awareness of common pitfalls helps you navigate the process smoothly.

Financial Changes During Application

Your financial situation should remain stable from application through closing. Avoid these common mistakes:

- Changing jobs or accepting new employment

- Making large purchases or opening new credit accounts

- Moving money between accounts without documentation

- Depleting savings for non-housing expenses

Lenders verify employment and assets immediately before closing. Unexpected changes can delay or even derail approved loans.

Documentation Gaps

Incomplete documentation represents the leading cause of application delays. NerdWallet’s mortgage application guide emphasizes the importance of providing complete, accurate documentation from the outset.

Ensure all documents are:

- Complete (every page of tax returns, all schedules included)

- Current (dated within required timeframes)

- Readable (clear scans or photos, not blurry or cut off)

- Consistent (information matches across documents)

Unrealistic Expectations

Understanding realistic timelines and requirements prevents frustration. Standard purchase transactions typically require 30-45 days from accepted offer to closing, though experienced lenders with streamlined processes can sometimes accommodate shorter timelines for qualified buyers.

Technology and Application Efficiency

Modern mortgage applications leverage technology to streamline processes and improve borrower experience. When you apply for mortgage loan financing in 2026, you'll likely encounter digital tools that simplify documentation and communication.

Digital Application Platforms

Many lenders now offer online application portals where you can complete forms, upload documents, and track application progress in real time. These platforms provide:

- Secure document storage accessible 24/7

- Automated reminders for pending requirements

- Direct messaging with your loan officer

- Mobile-friendly interfaces for on-the-go access

Electronic Verification Services

Lenders increasingly use automated verification systems that connect directly to employers, financial institutions, and tax authorities. These services can:

- Verify employment without manual VOE forms

- Access bank statements electronically with your permission

- Retrieve tax transcripts directly from the IRS

- Reduce documentation requirements and processing time

While technology improves efficiency, complex applications involving self-employment, multiple income sources, or unique property types still benefit from experienced human guidance to ensure all elements are properly documented and presented.

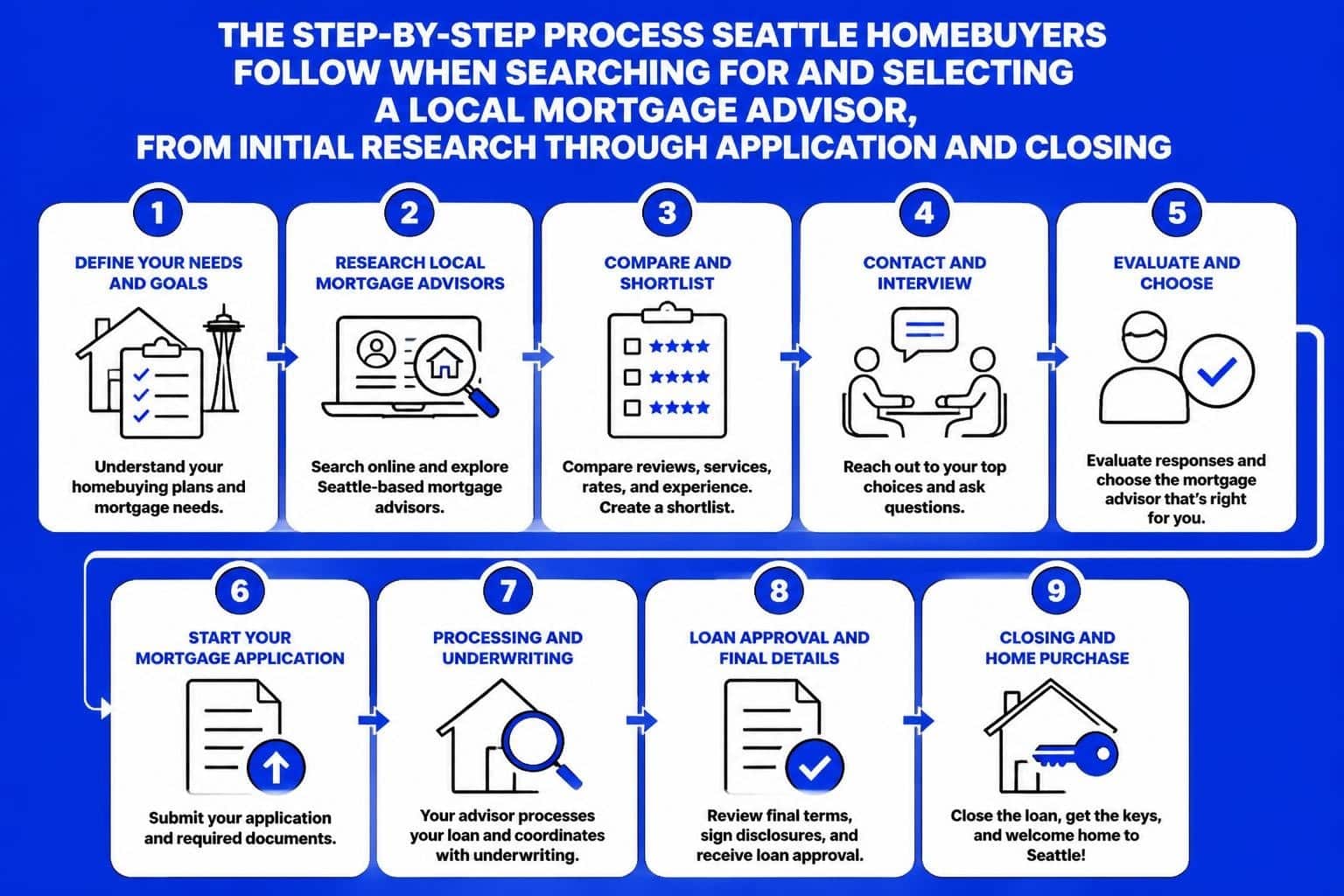

Working with the Right Mortgage Professional

Who guides you through the application process significantly impacts your experience and outcome. When you apply for mortgage loan financing, choosing a knowledgeable, responsive loan officer provides distinct advantages.

Questions to Ask Potential Loan Officers

Interviewing loan officers before committing helps ensure alignment with your needs and communication preferences.

Consider asking:

- How many years of experience do you have in the Seattle market?

- What percentage of your clients are tech professionals with stock compensation?

- What is your average time from application to closing?

- How do you communicate throughout the process?

- What are your current interest rates and fees?

The Value of Local Expertise

Seattle's unique market characteristics reward working with professionals who understand regional dynamics. Local loan officers know:

- Which condo projects meet lending guidelines

- How to structure applications for competitive offer situations

- Strategies for qualifying various forms of tech compensation

- Realistic timelines and potential challenges in different neighborhoods

With 25+ years of experience and 750+ five-star reviews, proven performance in Seattle's market provides confidence throughout the application journey.

Rate Locks and Timing Strategies

Interest rates fluctuate based on economic conditions, Federal Reserve policy, and market factors. When you apply for mortgage loan approval, understanding rate locks protects you from unfavorable rate movements during your transaction.

Rate Lock Fundamentals

A rate lock guarantees a specific interest rate for a defined period, typically 30-60 days. Once locked, your rate won't increase even if market rates rise, though you also won't benefit if rates decrease.

Rate lock considerations include:

- Lock period must exceed your expected closing timeline

- Extension fees apply if closing delays beyond lock period

- Float-down options may be available for a fee if rates decrease significantly

- Lock timing should align with contract dates and appraisal schedules

Strategic Lock Timing

Some borrowers prefer locking rates immediately upon application, while others monitor market trends and lock closer to closing. Your strategy should reflect:

- Current rate environment (rising, falling, or stable)

- Your risk tolerance for rate fluctuation

- Transaction timeline and confidence in closing date

- Market conditions and economic indicators

For Seattle buyers in competitive situations, securing a rate lock early in the process provides certainty for financial planning and removes one variable from an already complex transaction.

Successfully navigating the mortgage application process requires preparation, documentation, and strategic guidance tailored to Seattle's competitive market. Whether you're a first-time buyer in Everett or a tech professional purchasing a jumbo-priced home in Bellevue, understanding each phase of the application journey positions you for success. Keith Akada and the team at Mortgage Reel bring 25+ years of experience serving Seattle-area homebuyers with transparent guidance, specialized expertise in stock compensation qualification, and the ability to close loans in as few as 9 business days, helping you move from application to homeownership with confidence.