When you're ready to apply mortgage financing in the Greater Seattle area, understanding the complete process from start to finish can make the difference between a smooth transaction and a stressful experience. Whether you're purchasing your first condo in Lynnwood, upgrading to a larger home in Mill Creek, or refinancing investment property in Everett, the mortgage application process follows a structured path that requires preparation, documentation, and strategic decision-making. With Seattle's competitive real estate market and the prevalence of tech professionals with complex compensation structures, knowing exactly what to expect when you apply for a mortgage saves time, reduces anxiety, and positions you for approval.

Understanding Your Financial Position Before You Apply

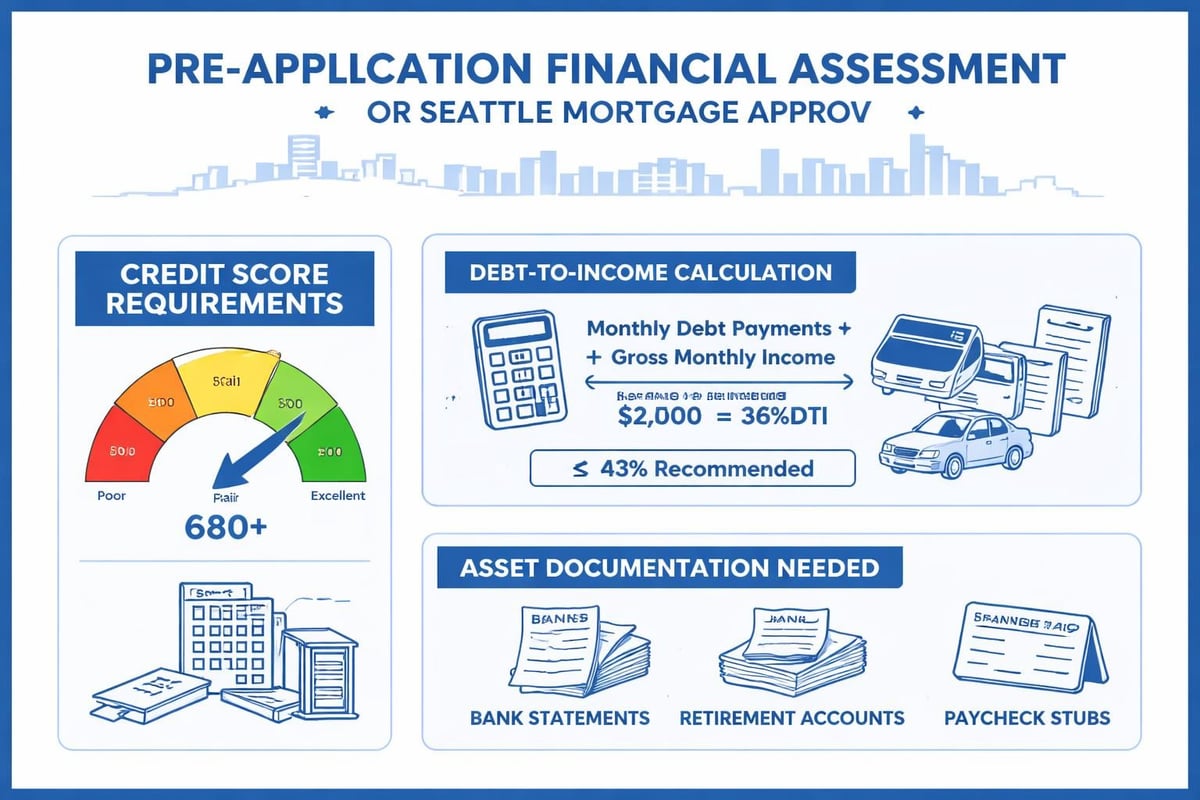

Before you formally apply mortgage financing, establishing a clear picture of your financial health sets the foundation for success. Lenders evaluate three primary factors: credit score, debt-to-income ratio, and available assets.

Your credit score directly impacts both your approval odds and the interest rate you'll receive. For conventional loans in 2026, most lenders require a minimum score of 620, though conventional loan requirements specify that scores above 740 typically unlock the most favorable pricing. Review your credit reports from all three bureaus at least 60 days before you plan to apply for a mortgage, giving yourself time to dispute errors or pay down balances strategically.

Key financial metrics lenders examine:

- Credit score across all three bureaus (Experian, TransUnion, Equifax)

- Total monthly debt obligations versus gross monthly income

- Cash reserves for down payment, closing costs, and reserves

- Employment history and income stability

- Recent large deposits or unusual financial activity

For Seattle-area tech professionals working at Amazon, Microsoft, or Google, your compensation package likely includes RSUs, stock options, and performance bonuses. These income sources require special documentation and calculation methods that differ from traditional W-2 salary verification.

Gathering Required Documentation

The documentation phase determines how quickly you can apply mortgage financing and move through underwriting. Most lenders require similar core documents, though specific requirements vary based on your employment type, property location, and loan program.

Standard Employment Documentation

Traditional W-2 employees need to provide two years of W-2 forms, recent pay stubs covering the most recent 30-day period, and written verification of employment. However, in Shoreline and throughout the Seattle metro, many borrowers have income structures that require additional documentation.

| Document Type | Traditional Employee | Tech Professional with RSUs | Self-Employed |

|---|---|---|---|

| Income Verification | 2 years W-2s + pay stubs | W-2s + RSU vesting schedule | 2 years tax returns |

| Employment Confirmation | VOE from employer | VOE + stock compensation letter | Business license + 1099s |

| Asset Verification | 2 months bank statements | Brokerage statements + bank statements | Business and personal accounts |

| Additional Items | None typically | Equity award documents | P&L statements, balance sheet |

Self-employed borrowers in Lake Forest Park or Mill Creek need two years of personal and business tax returns, a current profit and loss statement, and a year-to-date balance sheet. The mortgage application paperwork requirements have become more standardized, but complex income situations always require closer scrutiny.

Asset and Reserve Documentation

When you apply for a mortgage, lenders verify you have sufficient funds for your down payment, closing costs, and reserves. This means providing complete bank statements showing the previous two months of activity for all accounts.

Large deposits exceeding 50% of your gross monthly income trigger documentation requirements. If you received a bonus, gift funds from family, or sold stock, you'll need to provide paper trails explaining the source. For Seattle buyers using RSU proceeds as part of their down payment, maintain clear records of stock sales and transfers.

Choosing the Right Loan Program

The loan program you select when you apply mortgage financing affects your down payment requirement, interest rate, mortgage insurance obligations, and long-term costs. Seattle's higher home prices mean many borrowers need jumbo financing for purchases above the conforming loan limit.

Conventional Loans

Conventional loans dominate the Seattle market, offering flexibility for borrowers with strong credit and stable income. These loans require as little as 3% down for first-time buyers, though 5-20% down payments are more common in competitive markets like Bellevue and Redmond.

Benefits of conventional financing:

- Lower overall costs with 20% or more down payment

- No upfront mortgage insurance premium

- Ability to cancel PMI once you reach 20% equity

- Faster closing timelines in competitive markets

- More flexible property type eligibility

Jumbo Loans for Higher-Priced Properties

Seattle's median home prices frequently exceed conforming loan limits, making jumbo financing essential for many buyers. When you apply for a jumbo mortgage, expect stricter credit requirements (typically 700+ score), larger down payments (often 10-20%), and more thorough documentation of income and assets.

Tech professionals in the Seattle area benefit from specialized jumbo programs that properly calculate RSU and stock compensation income, maximizing purchasing power without requiring artificially conservative income calculations.

Government-Backed Options

FHA loans allow down payments as low as 3.5% with credit scores down to 580, making them attractive for first-time buyers in Everett or Lynnwood. However, mandatory mortgage insurance for the life of the loan (on most FHA loans) increases long-term costs compared to conventional options.

VA loans offer zero-down financing for eligible veterans and service members, with no mortgage insurance requirement. USDA loans provide another zero-down option for properties in designated rural areas, though few locations within the core Seattle metro qualify.

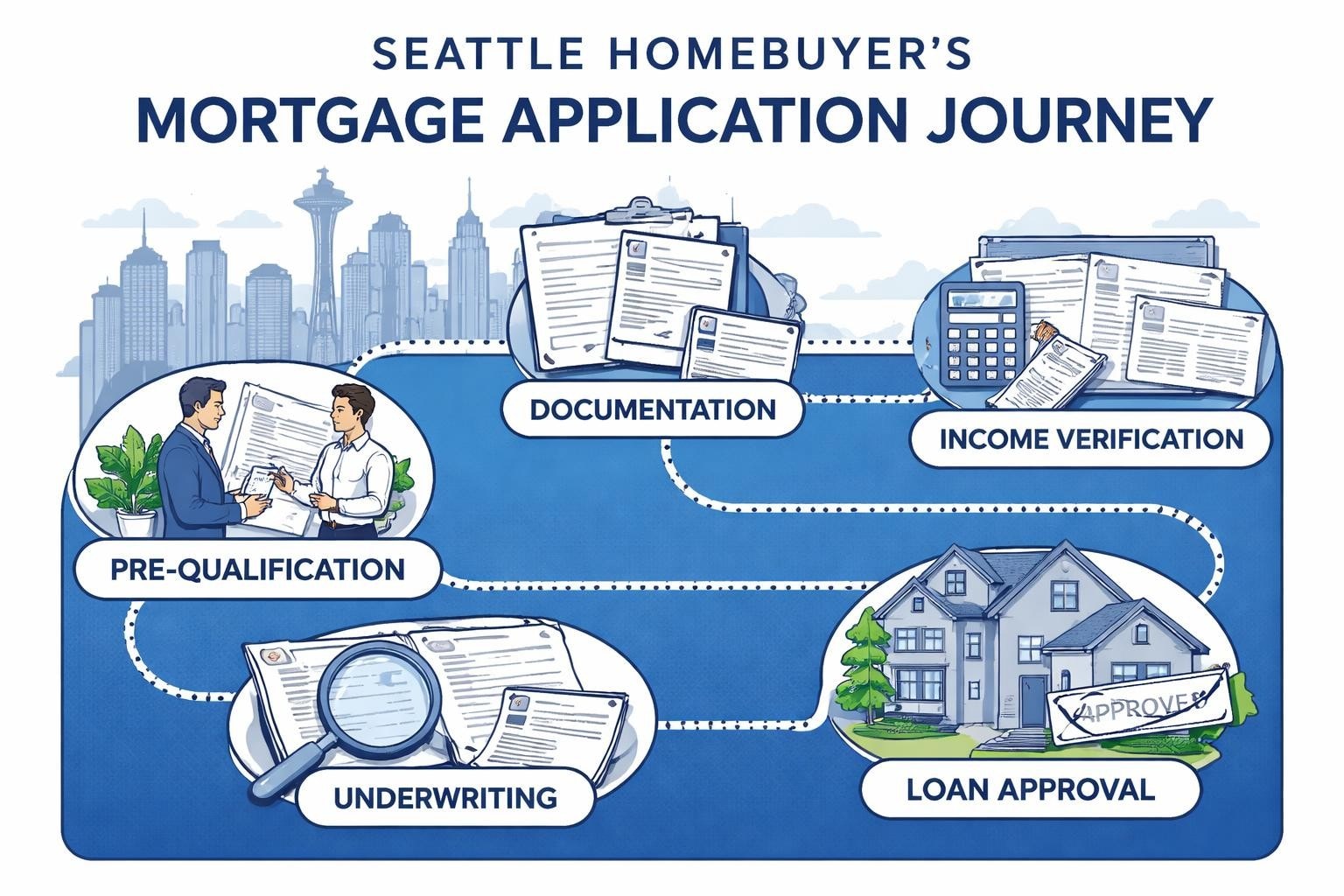

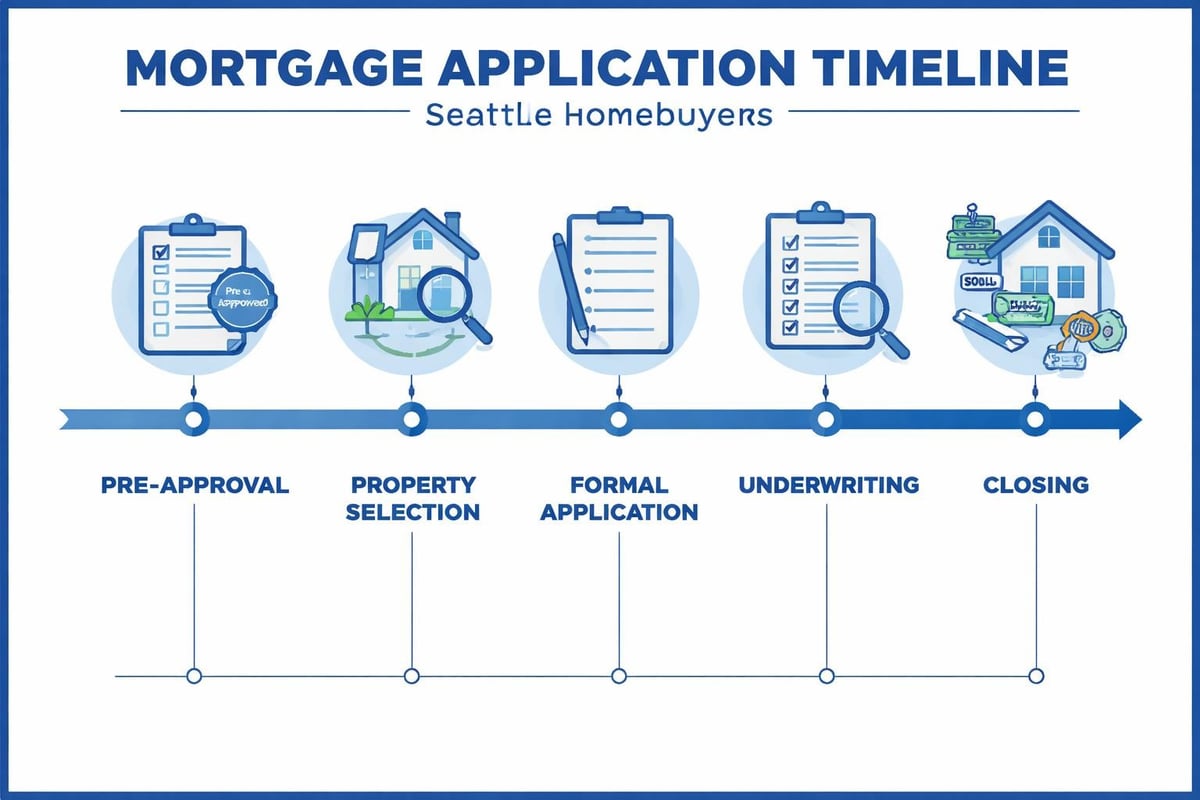

The Pre-Approval Process

Obtaining pre-approval before you actively shop for homes provides critical advantages in Seattle's competitive market. Pre-approval differs significantly from pre-qualification-it involves a complete credit review, income verification, and conditional loan commitment.

When you apply for mortgage pre-approval, the lender pulls your credit, reviews submitted documentation, and issues a commitment letter specifying the loan amount, program, and conditions. This letter demonstrates to sellers in Seattle, Mill Creek, or Shoreline that you're a serious, qualified buyer.

Understanding the mortgage application process from a pre-approval perspective helps you move quickly when you find the right property. Pre-approvals typically remain valid for 60-90 days, though you can refresh them by providing updated documentation.

Pre-Approval Timeline

- Initial consultation and loan program discussion (1 hour)

- Document submission and review (1-2 days)

- Credit pull and automated underwriting (same day)

- Manual review and conditional approval (1-3 days)

- Pre-approval letter issuance (same day as approval)

Strong pre-approvals can close in as few as 9 business days when you find a property and remove contingencies, a significant competitive advantage in multiple-offer situations common throughout Seattle and Bellevue.

Submitting Your Formal Application

Once you've identified a property and have an accepted purchase agreement, you'll formally apply for mortgage financing tied to that specific address. This triggers several concurrent processes: title review, appraisal ordering, homeowners insurance coordination, and formal underwriting.

The Uniform Residential Loan Application (URLA), also known as Form 1003, captures detailed information about you, the property, and the proposed transaction. When you apply mortgage financing, accuracy in this application is essential-inconsistencies between your application and supporting documentation can delay approval or trigger additional conditions.

Information Required on Your Application

Your formal application requires comprehensive details across multiple categories. Property information includes the complete address, purchase price, property type, and intended use (primary residence, second home, or investment). Borrower information extends beyond basic contact details to include two years of residence history, employment details, and declarations about your financial situation.

Critical application sections:

- Borrower and co-borrower identifying information

- Current and previous addresses with dates

- Employment and income details for all sources

- Asset and liability listing with account numbers

- Property information and transaction details

- Declarations regarding citizenship, occupancy, and financial obligations

For Lake Forest Park or Lynnwood buyers purchasing their first home, the declarations section includes questions about outstanding judgments, foreclosures, bankruptcies, and loan obligations. Answer these questions accurately-misrepresentations can result in loan denial even after initial approval.

Navigating the Underwriting Process

After you apply for a mortgage, your file moves to underwriting where a licensed professional reviews all documentation against program guidelines. Automated underwriting systems provide initial recommendations, but human underwriters make final approval decisions.

Underwriters verify every aspect of your application. They confirm employment directly with your employer, validate bank statements match application data, review credit report details, and ensure the property meets program requirements. This process typically takes 3-7 days for straightforward scenarios, though complex income documentation or property issues can extend timelines.

Common Underwriting Conditions

Almost every mortgage approval includes conditions-specific items the underwriter needs to verify or clarify. These might include updated pay stubs if your most recent one is more than 30 days old, explanations for credit inquiries, or verification that you've maintained sufficient funds for closing.

When you apply mortgage financing with stock compensation as a significant income component, expect conditions requesting RSU vesting schedules, historical stock award documentation, and verification of current holdings. Underwriters need to establish a stable, predictable income stream from equity compensation, which requires looking at multiple years of vesting patterns.

| Condition Type | Example Request | Typical Resolution Time |

|---|---|---|

| Income Verification | Updated pay stub or VOE | 1-2 days |

| Asset Sourcing | Explanation for large deposit | 1-3 days |

| Credit Inquiry | Letter explaining recent credit pull | Same day |

| Property Documentation | HOA documents or condo questionnaire | 3-5 days |

| Title Issues | Lien payoff or ownership clarification | 5-10 days |

Responding to conditions quickly and completely keeps your closing timeline on track. In Seattle's fast-paced market, delays can jeopardize transactions, particularly when you're competing against cash buyers or working within tight contingency periods.

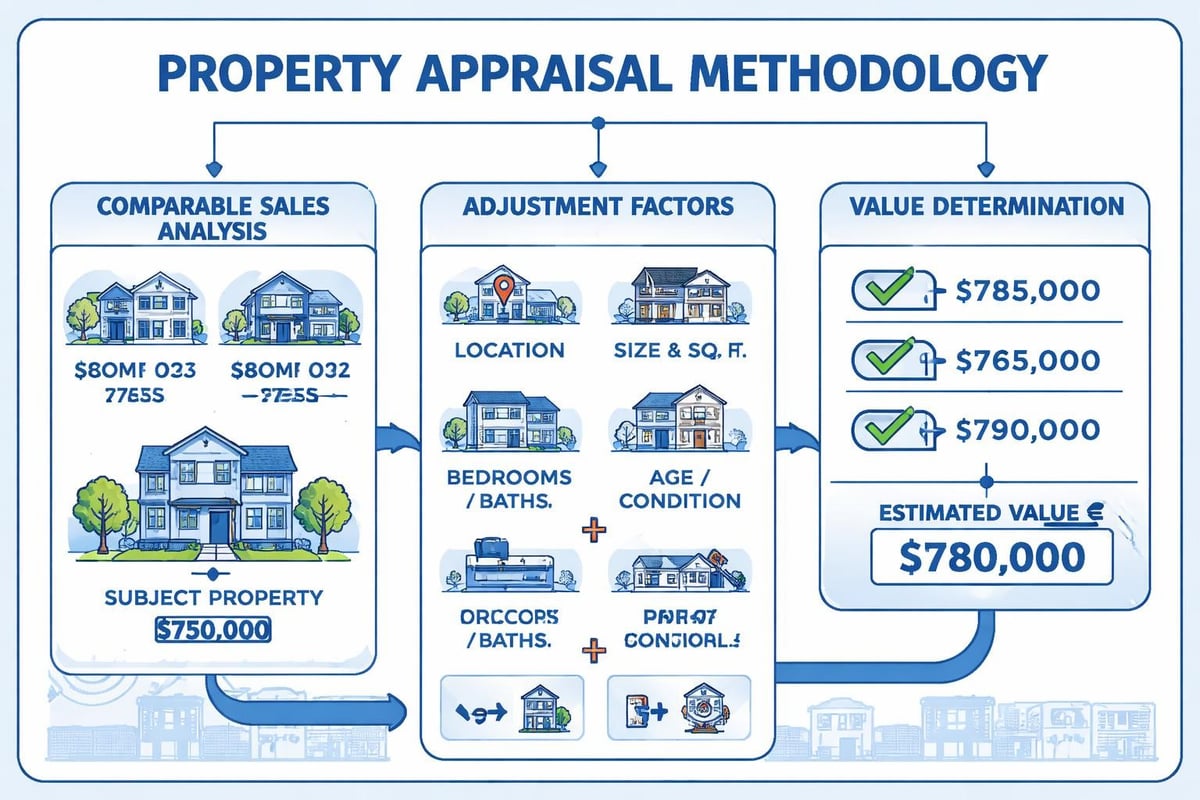

The Appraisal Requirement

Every mortgage requires an independent appraisal to verify the property's value supports the loan amount. When you apply for a mortgage on a Seattle home, the lender orders the appraisal shortly after application, and the appraiser typically completes their inspection within 7-10 days.

The 2026 appraisal threshold for higher-priced mortgage loans is set at $34,200, meaning certain lower-balance transactions may qualify for alternative valuation methods. However, most Seattle-area purchases well exceed this threshold and require full appraisals.

Appraisers evaluate the property's condition, square footage, bedroom/bathroom count, lot size, and location. They identify comparable sales from the previous 3-6 months, making adjustments for differences in features, condition, and location. In rapidly appreciating markets like Mill Creek or Shoreline, appraisers may give more weight to recent sales to capture current value trends.

What Happens If the Appraisal Comes In Low

If the appraised value falls below the purchase price, you have several options. You can renegotiate the purchase price with the seller, bring additional cash to closing to cover the difference, or cancel the transaction if your contract includes an appraisal contingency.

For Seattle buyers facing multiple-offer situations, waiving appraisal contingencies has become more common. If you choose this strategy, ensure you have sufficient cash reserves to cover potential gaps between contract price and appraised value.

Final Steps Before Closing

As you approach closing, several final verifications occur. Lenders re-verify employment within days of closing to confirm you're still employed. They conduct a final credit check to ensure you haven't taken on new debt. You'll receive a Closing Disclosure at least three business days before closing, detailing all loan terms, monthly payments, and closing costs.

Review your Closing Disclosure carefully against your Loan Estimate to identify any changes. Steps to apply for a mortgage include this critical review period, giving you time to question discrepancies or unexpected fees before you're at the closing table.

Preparing for Closing Day

Closing typically occurs at a title company office in the Seattle area. You'll need government-issued photo identification and certified funds for your down payment and closing costs. Personal checks aren't accepted-arrange a wire transfer or cashier's check several days in advance.

The closing appointment involves signing loan documents, the deed, and various disclosures. For Everett or Lynnwood closings, plan for 1-2 hours to complete all paperwork. You'll receive keys once the transaction funds and records with the county, typically the same day for purchases.

Special Considerations for Seattle-Area Buyers

Seattle's unique housing market and employment landscape create specific scenarios when you apply mortgage financing. Condominium purchases require additional documentation, including HOA financials, reserves, and owner-occupancy ratios. Lenders scrutinize condo projects to ensure they meet Fannie Mae or Freddie Mac approval standards.

New construction purchases involve different timelines and processes. You'll apply for mortgage approval before the home is complete, then update documentation as construction progresses. Final approval and funding occur only after a certificate of occupancy is issued and a final inspection confirms the property matches plans.

Maximizing Tech Compensation for Loan Qualification

For Microsoft, Amazon, or Google employees, properly documenting stock compensation can significantly increase your qualified income. Most programs require a two-year history of RSU vesting to include this income, calculated based on the average of the previous two years or the most recent year if it's lower.

Signing bonuses typically can't be included unless your offer letter shows they'll continue. Annual performance bonuses qualify when you demonstrate a two-year history, calculated conservatively using the average or most recent year. Recent policy changes have made it easier to access mortgage credit for borrowers with non-traditional income structures, though documentation requirements remain thorough.

RSU income calculation example:

- 2024 RSU income: $85,000

- 2025 RSU income: $95,000

- Average: $90,000

- Qualifying monthly income from RSUs: $7,500

This additional income significantly impacts your purchasing power, especially for jumbo loans in Seattle's higher-priced neighborhoods.

Common Mistakes to Avoid

When you apply for a mortgage, certain actions can derail your approval even after initial clearance. Avoid making large purchases on credit, changing jobs, or moving money between accounts without documentation during your loan process.

Don't close credit card accounts to try improving your credit score-this can actually lower your score by reducing available credit. Avoid co-signing loans for others, as those obligations count against your debt-to-income ratio. Don't make undocumented deposits to your bank accounts, as these trigger sourcing requirements that can delay closing.

Critical don'ts during your mortgage process:

- Applying for new credit cards or loans

- Making large purchases (cars, furniture, appliances)

- Changing jobs or employment structure

- Moving money without clear documentation

- Missing any payments on existing obligations

- Making large cash deposits

For self-employed borrowers in Shoreline or Lake Forest Park, maintaining consistent income documentation through year-end is essential. If you apply for a mortgage late in the year, be prepared to provide year-to-date profit and loss statements and potentially delay closing until after tax returns are filed if income verification is marginal.

Timeline Expectations for Seattle Buyers

Standard purchase timelines from application to closing run 30-45 days, though accelerated programs can close in as few as 9 business days for well-qualified borrowers with straightforward income documentation. Refinance transactions typically move faster since no purchase contract drives the timeline.

Breaking down the typical timeline helps you plan effectively:

- Days 1-3: Application submission and initial document review

- Days 4-7: Credit review, income calculation, and automated underwriting

- Days 8-10: Appraisal ordered and scheduled

- Days 11-17: Appraisal completed and reviewed

- Days 18-22: Full underwriting review and initial conditions issued

- Days 23-27: Borrower provides condition responses

- Days 28-30: Final underwriting review and clear to close

- Days 31-35: Closing documents prepared and reviewed

- Days 36-40: Three-day waiting period after Closing Disclosure

- Day 40-45: Closing and funding

Your specific timeline depends on documentation complexity, property type, and how quickly you respond to conditions. Working with an experienced Seattle mortgage broker can accelerate each phase through proactive communication and efficient process management.

Successfully navigating the mortgage application process requires preparation, accurate documentation, and strategic guidance tailored to your unique financial situation. Whether you're purchasing in Seattle's competitive core neighborhoods or exploring opportunities in Mill Creek, Lynnwood, or Everett, understanding each step positions you for approval and confident decision-making. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area buyers and homeowners navigate complex loan scenarios, with specialized expertise in tech compensation and jumbo financing. With 750+ five-star reviews and the ability to close in as few as 9 business days, his team provides the education, transparency, and execution you need to achieve your homeownership goals.