Finding the best home lending solution requires understanding your financial profile, comparing loan products, and working with a knowledgeable partner who can navigate complex income scenarios and competitive markets. In Seattle's dynamic housing market, where median home prices frequently exceed conventional loan limits and tech professionals often rely on stock-based compensation, choosing the right mortgage program and lender can determine whether you secure your ideal property or lose out to better-prepared buyers. This comprehensive guide explores proven strategies for identifying the best home lending options, from traditional financing to specialized programs designed for high earners and first-time buyers across Seattle, Bellevue, Redmond, Kirkland, and surrounding communities.

Understanding Modern Home Lending Products

The best home lending approach starts with matching your financial situation to the right loan type. Today's mortgage landscape offers far more variety than the traditional 30-year fixed-rate loan many buyers assume is their only option.

Conventional Loans and Their Advantages

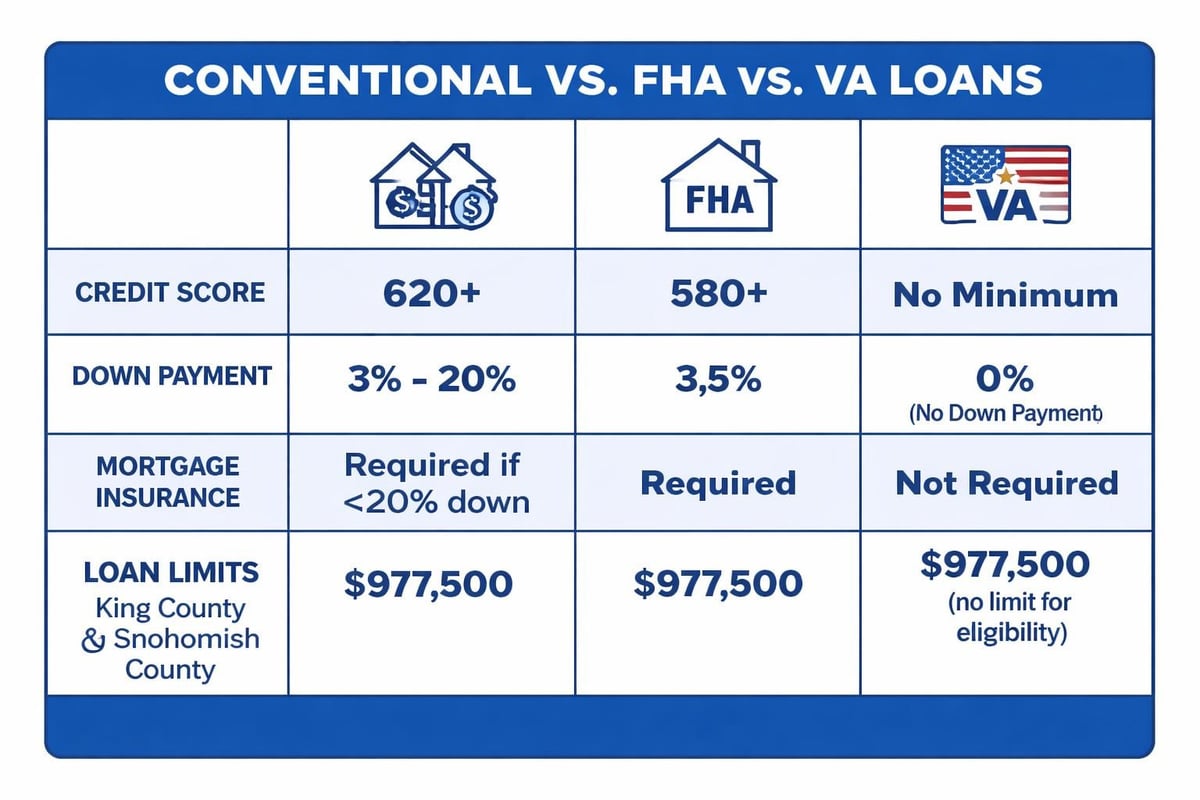

Conventional mortgages remain the most popular choice for qualified buyers, offering competitive rates and flexible terms. These loans typically require:

- Minimum credit scores of 620, though 740+ unlocks the best pricing

- Down payments as low as 3% for first-time buyers

- Private mortgage insurance (PMI) when putting down less than 20%

- Maximum loan amounts up to $806,500 in King County for 2026

One significant benefit: PMI can be removed once you reach 20% equity through payments or appreciation, unlike FHA mortgage insurance which lasts for the loan's life on most loans.

For buyers in Shoreline or Lynnwood considering properties in the $600,000 to $800,000 range, conventional financing often provides the cleanest path forward with minimal documentation requirements compared to government-backed alternatives.

Government-Backed Loan Programs

FHA, VA, and USDA loans serve specific buyer segments with distinct advantages. FHA loans accept credit scores as low as 580 with 3.5% down, making them accessible for buyers still building credit or recovering from past financial challenges. Veterans and active military personnel should always explore VA loans first, as they offer:

- Zero down payment requirement

- No monthly mortgage insurance

- Competitive interest rates regardless of down payment size

- Flexible credit guidelines

In Lake Forest Park and Mill Creek, where many military families transition to civilian careers at Boeing or tech companies, VA loans represent some of the best home lending opportunities available, particularly for higher-priced properties where the zero-down benefit creates substantial savings.

| Loan Type | Min. Credit Score | Min. Down Payment | Mortgage Insurance | 2026 Loan Limit (King County) |

|---|---|---|---|---|

| Conventional | 620 | 3% | PMI (removable) | $806,500 |

| FHA | 580 | 3.5% | MIP (lifetime) | $644,000 |

| VA | No minimum | 0% | None | $806,500 |

| Jumbo | 700+ | 10-20% | None | No limit |

Jumbo Loans for Seattle's Premium Market

When Seattle home prices exceed conventional loan limits, jumbo financing becomes necessary. The best home lending partners provide jumbo programs with competitive rates and creative qualifying approaches.

Jumbo loans typically require stronger financial profiles but offer flexibility for high earners. Expect minimum requirements including:

- Credit scores of 700 or higher (740+ for optimal pricing)

- Down payments between 10% and 20% depending on loan amount

- Debt-to-income ratios under 43% (though exceptions exist)

- Significant cash reserves, often 6-12 months of payments

For Amazon and Microsoft employees in Redmond and Bellevue, jumbo loans paired with stock compensation analysis can unlock purchasing power well beyond what base salary alone would support.

Qualifying Strategies for Seattle Tech Professionals

Seattle's concentration of technology employers creates unique lending considerations. Understanding how lenders evaluate stock-based compensation separates successful buyers from those who underestimate their borrowing capacity.

Maximizing RSU and Stock Option Income

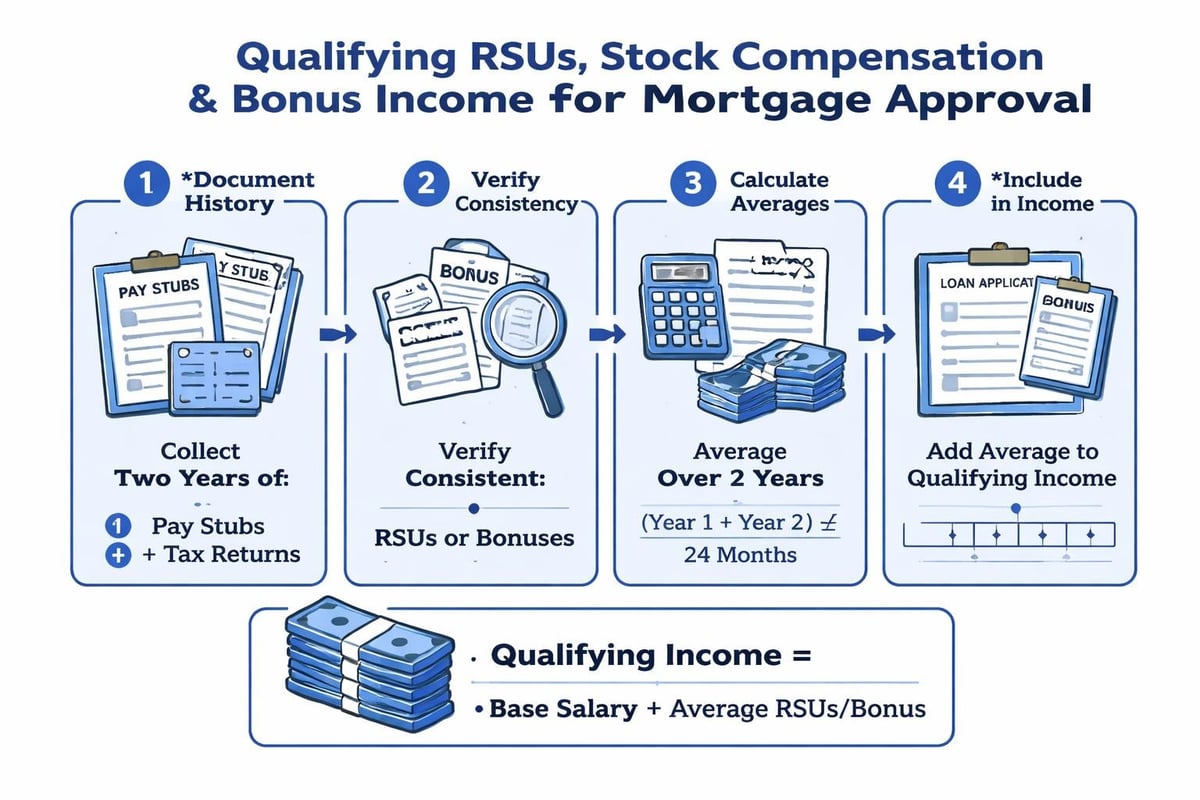

Restricted stock units (RSUs), employee stock purchase plans (ESPPs), and stock options can be used to qualify for mortgages, but guidelines vary significantly between lenders. The best home lending partners understand how to document and verify equity compensation properly.

For RSUs, lenders typically require:

- Two-year history of stock grants showing on W-2s or tax returns

- Proof of vesting schedule for continuity

- Documentation of company stock value and volatility

- Calculation using conservative averaging methods

Some advanced underwriting platforms can qualify unvested RSUs expected to vest within 12 months, substantially increasing buying power for recent hires at major tech firms. This approach works particularly well in Everett, where buyers can find excellent value while commuting to Seattle campuses.

Bonus and Commission Income Documentation

Annual bonuses and performance-based compensation follow similar verification requirements. Underwriters generally need:

- Two years of consistent bonus history

- Year-to-date paystubs showing current-year bonus

- Employment verification confirming bonus structure will continue

- Averaging calculation to determine monthly qualifying income

A software engineer in Seattle earning $200,000 in base salary plus $80,000 in annual RSUs might qualify based on $280,000 total income, dramatically expanding their home search parameters compared to salary-only calculations.

Rate Shopping and Timing Strategies

Securing the best home lending terms requires strategic timing and thorough rate comparison. Many buyers focus exclusively on interest rates while overlooking total cost factors that matter more over typical ownership periods.

Understanding APR vs. Interest Rate

The Annual Percentage Rate (APR) provides a more complete picture than the advertised interest rate alone. APR includes:

- The note rate you'll pay monthly

- Origination fees and points

- Mortgage insurance premiums

- Other mandatory costs distributed over the loan term

Two lenders might quote 6.5% interest rates, but one charging 2% in fees will have a significantly higher APR than one charging 0.5%. For buyers planning to stay in their home 5-7 years or longer, paying points to reduce the rate often makes financial sense. Shorter ownership timelines favor minimal upfront costs despite slightly higher rates.

Timing Your Lock Strategy

Interest rate locks protect you from increases between application and closing, but timing them incorrectly can cost money. Consider these approaches:

- Extended locks (45-60 days) provide security but cost more upfront

- Standard locks (30 days) work well for strong purchase contracts

- Float-down options allow one-time rate reduction if markets improve

- Lock extensions add cost when closings delay unexpectedly

In competitive Seattle neighborhoods, where inspection contingencies might extend timelines, discussing lock strategies with your loan officer prevents unnecessary rate risk.

Choosing the Right Lending Partner

The institution and individual handling your mortgage matters as much as the loan product itself. Evaluating mortgage lenders involves examining their capabilities across multiple dimensions.

Response Time and Communication Standards

In markets where sellers receive multiple offers within 24 hours of listing, loan officer responsiveness directly impacts your competitive position. The best home lending professionals provide:

- Pre-approval letters within hours, not days

- Direct cell phone and email access outside business hours

- Proactive status updates throughout the process

- Quick answers to agent and seller questions

Buyers in Kirkland competing against all-cash offers need every advantage, including a lender reputation for reliable closings and clear communication.

Underwriting Flexibility and Problem-Solving

Cookie-cutter underwriting fails complex financial situations. Experienced loan officers know how to structure files to highlight strengths while addressing potential concerns before they become denial issues.

Real-world examples include:

- Structuring gift funds from family members to meet seasoning requirements

- Explaining one-time income drops without triggering declining-income concerns

- Sourcing large deposits from stock sales or bonuses properly

- Navigating self-employment income with creative documentation

Tech professionals often carry complex finances including side consulting income, rental properties, or international work history. Finding a lending partner experienced with these scenarios prevents frustrating delays or outright denials.

Technology and Speed Capabilities

Modern lending platforms enable faster closings without sacrificing quality. Advanced underwriting systems can deliver:

- Automated income and employment verification

- Digital asset verification linking directly to bank accounts

- Electronic appraisal options reducing timeline bottlenecks

- Online portals for real-time status tracking

Some lenders now close purchases in 9-12 business days versus the industry standard of 30-45 days. In competitive situations, this speed allows buyers to waive financing contingencies confidently or negotiate shorter closing periods that appeal to sellers.

Portfolio Diversification and Investment Property Financing

Beyond primary residences, the best home lending strategies often include investment property acquisition for wealth building. Seattle's strong rental market and consistent appreciation make real estate investment attractive for qualified buyers.

Conventional Investment Property Loans

Financing rental properties requires larger down payments and stronger reserves than primary residences. Typical requirements include:

- 15-25% down payment depending on property count

- Six months reserves (PITI payments) for each financed property

- Maximum debt-to-income ratios around 45%

- Expected rental income can offset mortgage payments

Conventional financing allows up to 10 financed properties, providing substantial portfolio-building capacity for disciplined investors.

DSCR Loans for Streamlined Qualification

Debt Service Coverage Ratio (DSCR) loans qualify borrowers based on property cash flow rather than personal income. These programs work exceptionally well for:

- Self-employed buyers with complex tax returns

- High-net-worth individuals who minimize reported income

- Investors expanding beyond conventional property limits

- Buyers with recent credit events but strong assets

Mill Creek and Everett offer attractive investment opportunities where positive cash flow supports DSCR qualification, even when traditional income verification would limit borrowing capacity.

Refinancing Strategies and Equity Access

Homeownership unlocks ongoing financial opportunities through refinancing and equity borrowing. Understanding when to refinance and which product to use maximizes long-term wealth building.

Rate-and-Term Refinancing Decision Points

Refinancing to lower your rate makes sense when:

- Current rates sit at least 0.75% below your existing rate

- You plan to keep the home long enough to recoup closing costs

- Your credit score has improved significantly since original financing

- You want to eliminate mortgage insurance after reaching 20% equity

For Seattle homeowners who purchased in 2023-2024 at higher rates, monitoring refinance opportunities as rates decline can save hundreds monthly.

Cash-Out Refinancing for Strategic Goals

Extracting equity through cash-out refinancing funds various objectives including:

- Home improvements that increase property value

- Debt consolidation at lower interest rates

- Investment property down payments

- Education expenses or business investments

Cash-out refinances typically require 20% remaining equity post-closing and follow conventional or jumbo guidelines depending on loan size.

Home Equity Lines of Credit (HELOCs)

HELOCs provide flexible credit lines secured by home equity, offering several advantages over cash-out refinancing:

- No impact on your existing first mortgage rate

- Interest-only payment options during draw periods

- Access funds as needed rather than taking lump sums

- Potentially tax-deductible interest when used for home improvements

Shoreline and Lake Forest Park homeowners who've built substantial equity since purchase can establish HELOCs as financial safety nets or opportunistic investment funding without disturbing favorable first mortgage terms.

| Product Type | Best For | Rate Type | Closing Costs | Access Speed |

|---|---|---|---|---|

| Cash-Out Refi | Large lump sum needs | Fixed | $3,000-$6,000 | 30-45 days |

| HELOC | Flexible ongoing access | Variable | $500-$1,500 | 2-4 weeks |

| Home Equity Loan | Fixed payment preference | Fixed | $2,000-$4,000 | 2-3 weeks |

Working With Real Estate Professionals

Your lending experience improves dramatically when your loan officer collaborates effectively with your real estate agent and other transaction participants.

Pre-Approval Strength and Credibility

Sellers and listing agents evaluate offer strength partially based on financing quality. Strong pre-approvals include:

- Full credit report review, not just soft pulls

- Comprehensive income and asset documentation

- Specific property type and price range parameters

- Direct lender contact information for verification

Generic online pre-qualifications carry little weight compared to detailed letters from established local lenders with proven closing track records.

Coordinating Timeline Expectations

Real estate agents structure offers based on realistic financing timelines. When your lender commits to specific closing dates, meeting those commitments protects your earnest money and purchase contract. Delays can trigger:

- Contract extension negotiations with stressed sellers

- Rate lock expirations requiring costly extensions

- Lost opportunities if sellers cancel contracts

Choosing the best home lending partner means selecting someone whose timeline promises you can trust completely.

Market-Specific Considerations for Greater Seattle

Seattle's housing market presents unique challenges requiring specialized knowledge and strategic approaches.

Competitive Offer Environments

Low inventory relative to demand creates multiple-offer scenarios where financing strength matters. Competitive buyers should:

- Obtain pre-approvals from lenders respected by local agents

- Consider larger earnest money deposits showing commitment

- Work with loan officers who respond quickly to agent inquiries

- Explore financing structures that appeal to seller priorities

In Bellevue's luxury market, where homes regularly receive 5-10 offers, these details separate successful buyers from perpetually disappointed shoppers.

Condo Financing Complexities

Seattle's condo market involves additional lending requirements. Lenders must verify:

- HOA financial health and reserve funding levels

- Owner-occupancy ratios meeting agency guidelines

- Absence of significant pending litigation against associations

- Commercial space percentages within acceptable limits

Some buildings lose financing eligibility due to deferred maintenance or financial mismanagement, making lender experience with condo financing essential for buyers targeting high-rises in downtown Seattle or waterfront developments.

New Construction Timing Challenges

Builder timelines rarely match original projections. The best home lending approach for new construction includes:

- Rate lock strategies accounting for probable delays

- Communication protocols with builder sales teams

- Backup plans if completion extends beyond lock periods

- Understanding builder incentives and captive lender requirements

Lynnwood and Everett continue seeing significant new construction activity, creating opportunities for buyers willing to navigate the unique financing considerations these purchases require.

Credit Optimization Before Applying

Your credit profile directly impacts rate pricing and program eligibility. Strategic credit management in the months before applying can save thousands over your loan's life.

Score Improvement Strategies

Borrowers hovering near pricing thresholds (typically 680, 700, 720, and 740) should focus on:

- Paying down credit card balances below 30% utilization

- Avoiding new credit inquiries in the 3-6 months before applying

- Correcting reporting errors through formal disputes

- Becoming authorized users on established accounts with perfect payment history

A 20-point score increase from 698 to 718 might reduce your rate by 0.25%, saving $50-$75 monthly on a $600,000 loan.

What to Avoid During the Process

Once you've applied for a mortgage, protect your approval by avoiding:

- Large purchases on credit cards or new auto loans

- Changing jobs, especially to different industries or commission-based roles

- Making large unexplained bank deposits

- Closing credit card accounts (reduces available credit)

Even small credit decisions during underwriting can derail approvals or delay closings when they trigger additional verification requirements.

Comparing Total Cost of Ownership

The best home lending decision considers costs beyond monthly payments. Comprehensive ownership cost analysis includes:

- Principal and interest payments

- Property taxes (varies significantly by city and school district)

- Homeowners insurance premiums

- HOA or condo fees where applicable

- Maintenance and repair reserves

- PMI or mortgage insurance when required

A $700,000 home in Redmond might carry monthly costs of $4,800 ($3,500 payment, $900 taxes, $200 insurance, $200 HOA), requiring gross income around $13,700 monthly or $164,000 annually to meet standard 35% housing ratio guidelines.

Understanding these projections prevents buyers from stretching into uncomfortable payment territory that limits financial flexibility.

Selecting the best home lending approach requires matching your financial profile to appropriate loan products, partnering with experienced professionals who understand complex income scenarios, and executing strategic timing throughout the process. Whether you're purchasing your first home in Seattle, refinancing to access equity in Kirkland, or building an investment portfolio across King and Snohomish Counties, working with a knowledgeable mortgage broker makes the difference between frustrating dead ends and smooth closings. Keith Akada brings 25+ years of mortgage expertise and specializes in qualifying stock compensation, RSUs, and bonus income for Seattle-area tech professionals, with proven ability to close purchases in as few as 9 business days through advanced underwriting platforms. Mortgage Reel provides the education, transparency, and strategic guidance you need to make confident home financing decisions backed by 750+ five-star reviews across major platforms.