Finding the best loan rates mortgage options in Seattle's competitive housing market requires understanding how rates are determined, what factors influence your personal rate, and how to position yourself for the most favorable terms. As of March 2026, mortgage rates have shown volatility, recently rising to 6.11% according to recent Associated Press reporting, influenced by geopolitical tensions and bond market fluctuations. For Seattle-area homebuyers, particularly tech professionals in Bellevue, Redmond, and Kirkland, securing competitive rates often involves leveraging stock compensation and strategic timing. This guide breaks down everything you need to know about obtaining the best loan rates mortgage products available in 2026.

Understanding What Determines Your Mortgage Rate

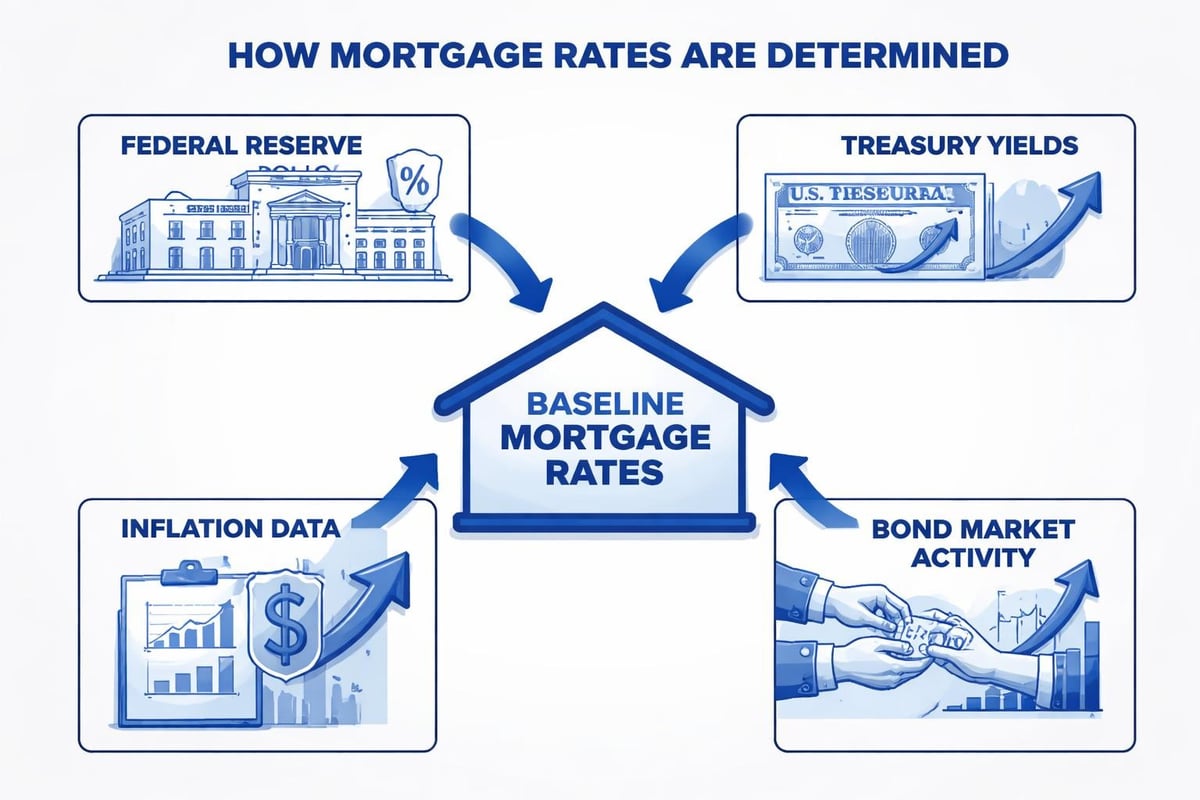

Mortgage rates aren't one-size-fits-all. The rate you receive depends on a complex interaction between national economic factors and your personal financial profile.

National Economic Factors

The broader economy significantly influences baseline mortgage rates. The relationship between 10-year Treasury yields and mortgage rates is particularly important, as lenders often price conventional mortgages based on these benchmarks. When Treasury yields rise, mortgage rates typically follow.

Several macro-level elements shape the rate environment:

- Federal Reserve policy decisions on short-term interest rates

- Inflation expectations and current inflation data

- Employment statistics and economic growth indicators

- Global economic conditions including geopolitical events

- Bond market investor demand for mortgage-backed securities

According to First Community Mortgage’s analysis, these factors create the foundation upon which individual rates are built. In Seattle's market, where home prices remain elevated compared to national averages, understanding these influences helps buyers time their applications strategically.

Personal Financial Profile Impact

Your individual circumstances can cause your rate to vary significantly from advertised rates. Lenders assess risk through multiple lenses, and borrower-specific factors directly impact pricing.

Credit Score Influence

| Credit Score Range | Typical Rate Impact |

|---|---|

| 760+ | Best available rates |

| 700-759 | 0.25%-0.50% higher |

| 660-699 | 0.50%-1.00% higher |

| 620-659 | 1.00%-1.50% higher |

| Below 620 | Limited options, significantly higher |

Down Payment Considerations

The amount you put down affects both your rate and overall loan structure. Larger down payments reduce lender risk and often result in better pricing:

- 20% or more: Eliminates PMI, typically best rates

- 10%-19%: Competitive rates, PMI required on conventional loans

- 5%-9%: Slightly higher rates, higher PMI

- 3%-5%: Higher rates, maximum PMI on conventional products

For Seattle tech professionals with RSU compensation, strategic timing of stock vesting can significantly impact down payment capability and therefore access to the best loan rates mortgage products.

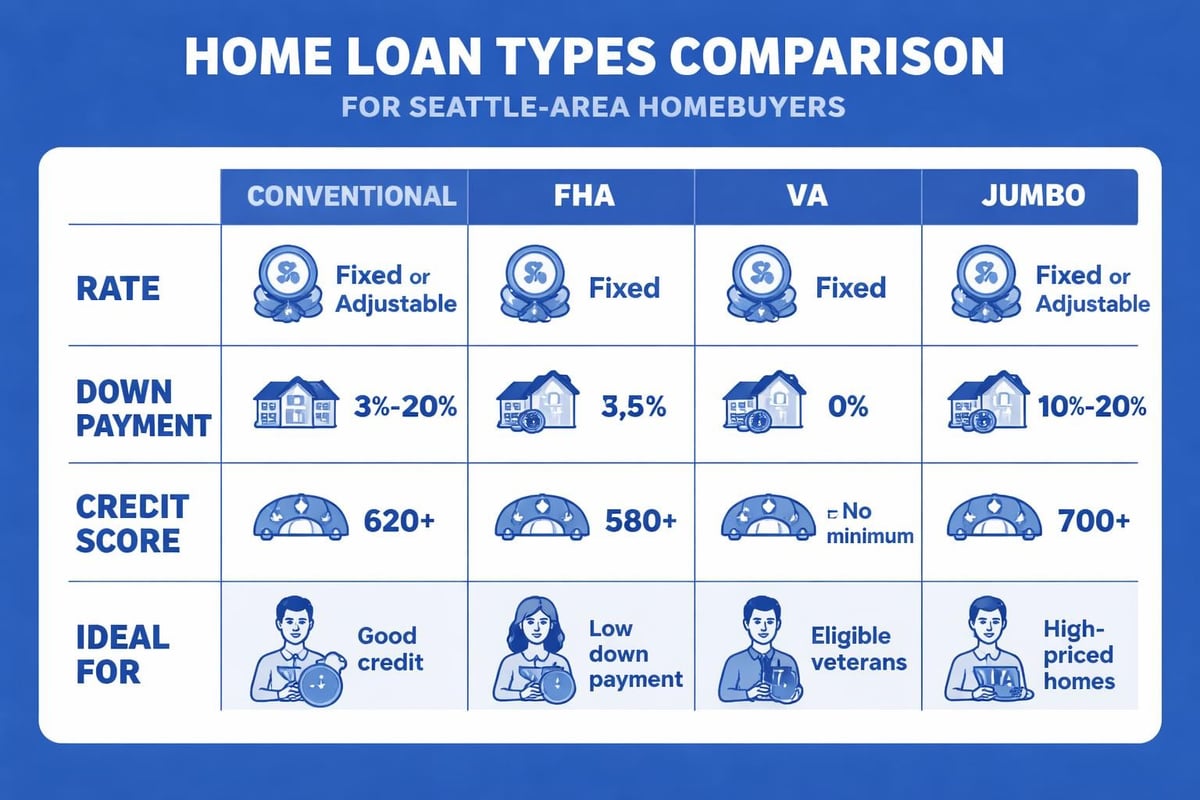

Loan Type Comparison for Seattle Buyers

Different mortgage products carry different rate structures. Understanding these distinctions is essential when searching for the best loan rates mortgage options.

Conventional vs. Government-Backed Loans

Conventional Loans typically offer the best rates for borrowers with strong credit (720+) and significant down payments. In markets like Shoreline and Lynnwood, where home prices often exceed conforming loan limits, these products remain popular.

FHA Loans feature competitive rates for borrowers with lower credit scores or smaller down payments. The 3.5% down payment requirement makes these attractive for first-time buyers in Mill Creek and Lake Forest Park.

VA Loans often provide the absolute best rates for eligible veterans and service members, with no down payment required and no PMI.

Jumbo Loans are necessary for Seattle-area properties exceeding $1,209,750 (2026 conforming limit). While historically carrying higher rates, competitive jumbo products now exist for well-qualified borrowers.

Fixed-Rate vs. Adjustable-Rate Mortgages

The choice between fixed and adjustable rates significantly impacts your long-term costs.

30-Year Fixed Mortgages

- Predictable payments for entire loan term

- Protection against future rate increases

- Currently averaging 6.11% nationally

- Ideal for long-term homeowners

15-Year Fixed Mortgages

- Substantially lower total interest paid

- Rates typically 0.50%-0.75% below 30-year products

- Higher monthly payments

- Excellent for refinancing or buyers with strong income

Adjustable-Rate Mortgages (ARMs)

ARMs offer lower initial rates, making them attractive for certain situations:

- 5/1 ARM: Fixed for five years, then adjusts annually

- 7/1 ARM: Fixed for seven years, then adjusts annually

- 10/1 ARM: Fixed for ten years, then adjusts annually

Initial ARM rates currently sit approximately 0.75%-1.25% below comparable fixed products. For Everett buyers planning to relocate within 5-7 years, ARMs can provide significant savings.

Strategic Approaches to Securing Best Rates

Getting approved is one thing. Securing the best loan rates mortgage products require deliberate preparation and timing.

Credit Optimization Timeline

6-12 Months Before Applying

Start with a comprehensive credit review. Obtain reports from all three bureaus and dispute any inaccuracies. Pay down credit card balances to below 30% utilization, ideally below 10%. Avoid opening new credit accounts during this period.

3-6 Months Before Applying

Focus on payment consistency. Set up automatic payments to ensure nothing is missed. If you have collections or charge-offs, consider negotiating pay-for-delete arrangements. Build your savings to demonstrate reserves beyond your down payment.

1-3 Months Before Applying

Avoid major purchases that would appear as new debt. Don't co-sign loans for others. Maintain stable employment, as job changes can complicate approval. Gather documentation including pay stubs, tax returns, and bank statements.

Income Documentation for Tech Professionals

Seattle's concentration of tech employers creates unique opportunities for mortgage qualification. RSUs, stock options, and bonuses can significantly increase buying power when properly documented.

Equity Compensation Guidelines

- Vested RSUs: Typically counted at 100% of value for qualifying income

- Unvested RSUs with history: May be averaged over 24 months

- Stock options: Generally not counted until exercised and sold

- Performance bonuses: Averaged over two years with continuance verification

Working with a broker experienced in tech compensation is critical. Many Seattle homebuyers in Bellevue and Redmond find that proper RSU documentation increases their qualifying amount by 25%-50%.

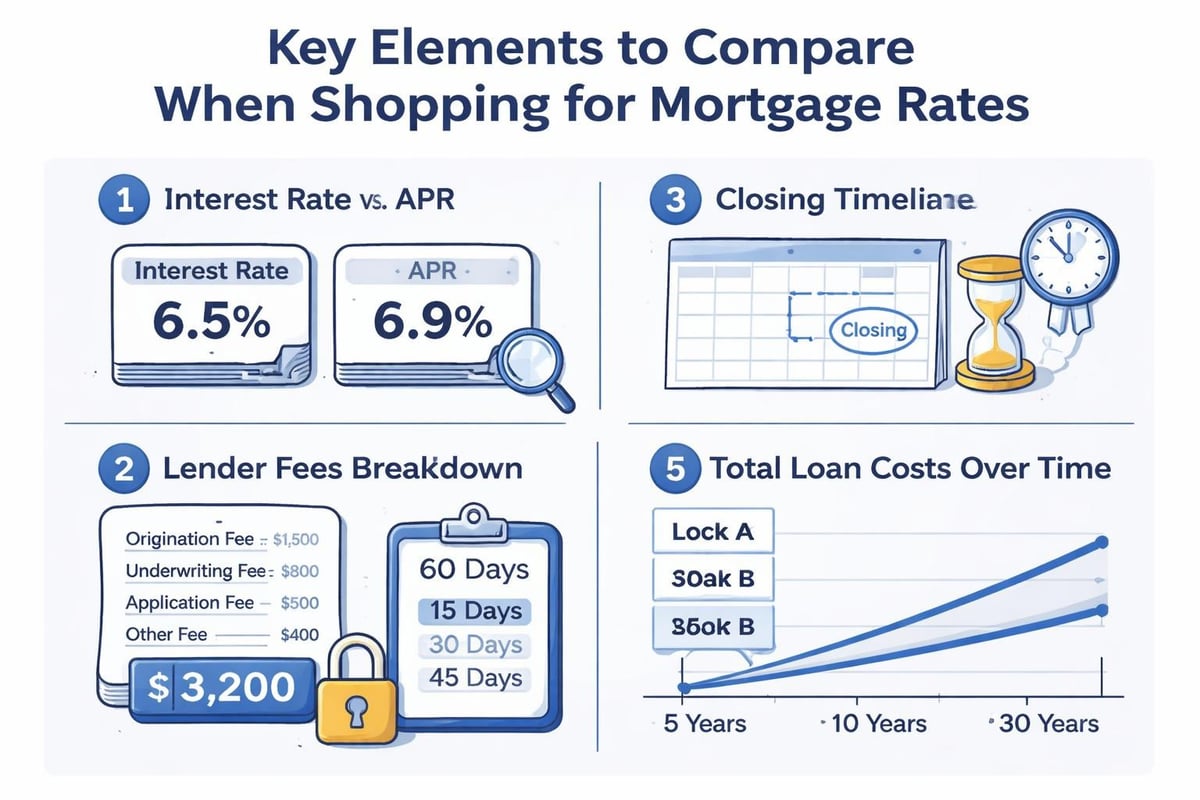

Rate Lock Strategy

Timing your rate lock requires balancing market conditions with your closing timeline.

| Lock Period | Typical Cost | Best For |

|---|---|---|

| 30 days | Standard (no cost) | Purchase with clear close date |

| 45 days | 0.125% rate or fee | Most purchase transactions |

| 60 days | 0.25% rate or fee | New construction, complex purchases |

| 90 days | 0.375%-0.50% rate or fee | Extended closings, construction loans |

Some lenders offer float-down provisions, allowing you to capture lower rates if they drop before closing. These typically cost 0.125%-0.25% upfront but provide downside protection.

Shopping and Comparing Mortgage Lenders

Securing the best loan rates mortgage products requires comparing multiple lenders effectively.

What to Compare Beyond Rate

Annual Percentage Rate (APR) provides a more complete picture than the interest rate alone, incorporating fees and costs into a single percentage. A loan with a slightly higher rate but lower fees might have a better APR.

Consider these factors when evaluating offers:

- Origination fees and points

- Third-party fees (appraisal, title, escrow)

- Lender responsiveness and communication quality

- Closing timeline capabilities

- Lock period and float-down options

- Reputation and reviews from local borrowers

Current Market Rate Landscape

As analyzed by Yahoo Finance in early March 2026, rising oil prices and geopolitical factors have created upward pressure on rates. The best loan rates mortgage offerings currently cluster in these ranges for well-qualified borrowers:

Conventional 30-Year Fixed: 5.875%-6.375%

Conventional 15-Year Fixed: 5.125%-5.625%

FHA 30-Year Fixed: 5.750%-6.250%

VA 30-Year Fixed: 5.625%-6.125%

Jumbo 30-Year Fixed: 6.125%-6.750%

These ranges assume excellent credit (740+), 20% down on conventional products, and competitive Seattle-area lenders. Your actual rate will depend on your specific situation.

Refinancing Considerations in 2026

Current homeowners may find refinancing opportunities despite elevated rates compared to 2020-2021 lows.

When Refinancing Makes Sense

Rate-and-Term Refinance

If you purchased when rates exceeded 7%, as they did in late 2023, recent declines toward 6% may justify refinancing. Calculate your break-even point by dividing closing costs by monthly savings.

Cash-Out Refinance

Seattle-area homeowners have built substantial equity as prices appreciated. Cash-out refinancing allows accessing this equity for renovations, debt consolidation, or investment property down payments. Current rates make this viable when the alternative (HELOC, personal loan) carries higher costs.

Mortgage Insurance Elimination

If your home in Lynnwood or Mill Creek has appreciated to where you now have 20% equity, refinancing to eliminate PMI can provide immediate monthly savings that offset a slightly higher rate environment.

Break-Even Analysis Framework

Calculate whether refinancing makes financial sense:

- Determine total closing costs (typically 2%-5% of loan amount)

- Calculate monthly payment reduction

- Divide total costs by monthly savings

- Compare break-even timeline to how long you plan to keep the home

Example: $500,000 loan, $10,000 closing costs, $200/month savings = 50-month break-even. If you plan to stay beyond four years, refinancing makes sense.

Rate Improvement Tactics for Different Borrower Profiles

Different situations call for different strategies to secure the best loan rates mortgage products available.

First-Time Homebuyers

Challenges: Limited down payment, shorter credit history, less real estate knowledge

Strategies:

- Explore first-time buyer programs with competitive rates

- Consider FHA loans if credit score is below 720

- Use gift funds from family to increase down payment

- Focus on smaller starter homes in Mill Creek or Everett

- Build reserves to strengthen application beyond minimum requirements

Move-Up Buyers

Advantages: Equity from current home, established credit, income growth

Strategies:

- Time sale of current home to maximize down payment

- Consider bridge financing if timing doesn't align perfectly

- Leverage improved credit score since first purchase

- Explore conventional products with 10%-15% down

- Use equity to buy down rate through points if planning long-term ownership

Real Estate Investors

Unique Considerations: Multiple properties affect debt-to-income ratios, different down payment requirements

Strategies:

- Maintain strong reserves (6+ months per property)

- Document rental income properly through tax returns and leases

- Consider portfolio loans for multiple properties

- Build relationships with investor-friendly lenders

- Structure acquisitions to maintain optimal debt-to-income ratios

Tech Professionals with Equity Compensation

Opportunities: High income, substantial assets in stock, strong employment

Strategies:

- Work with lenders experienced in RSU/stock option qualification

- Time closings around vesting schedules when possible

- Maintain documentation of compensation structure and vesting schedule

- Consider jumbo products designed for high-income borrowers

- Leverage signing bonuses and relocation packages for down payments

Market-Specific Considerations for Greater Seattle

Local market dynamics influence which mortgage products and strategies work best.

Competitive Offer Environments

Seattle, Bellevue, and Redmond markets remain competitive despite rate increases. Strong pre-approval letters are essential, and working with lenders who can close quickly (9-15 business days) provides significant advantages.

Property Type Impact on Rates

Single-Family Homes: Best rates available

Condominiums: Rates typically 0.125%-0.375% higher, depending on building's financial health and FHA/VA approval status

Multi-Family (2-4 units): Rates 0.25%-0.50% higher, but rental income can offset

Manufactured Homes: Limited options, significantly higher rates

Shoreline and Lake Forest Park have diverse housing stock, making property type a crucial consideration when comparing the best loan rates mortgage options.

New Construction Timelines

Seattle-area new construction often involves extended closing timelines. Builder relationships with preferred lenders can sometimes secure competitive rates, but always compare these against independent lender offerings. Extended rate locks (60-90 days) may be necessary, affecting overall costs.

Understanding Points and Rate Buydowns

Discount points allow you to pay upfront fees to reduce your interest rate. Each point typically costs 1% of the loan amount and reduces your rate by approximately 0.25%.

When Points Make Sense

Calculate the Break-Even:

- $500,000 loan amount

- 1 point = $5,000 cost

- Rate reduction: 6.25% to 6.00%

- Monthly savings: approximately $75

- Break-even: 67 months (5.6 years)

Points are advantageous when you plan to stay in the home beyond the break-even period and have cash available that won't deplete your emergency reserves.

Temporary Buydowns

2-1 Buydown: Rate reduced by 2% in year one, 1% in year two, then normal rate

1-0 Buydown: Rate reduced by 1% in year one, then normal rate

These structures, sometimes offered by builders or sellers in softer markets, can ease payment shock while you adjust to homeownership costs. Everett occasionally sees seller concessions funding these arrangements.

Monitoring Rate Trends and Timing Applications

While timing the market perfectly is impossible, understanding trends helps make informed decisions.

Rate Movement Indicators

Watch these signals for potential rate changes:

- Federal Reserve meeting announcements and policy statements

- Monthly employment and inflation data releases

- 10-year Treasury yield movements

- Geopolitical developments affecting bond markets

- Housing market data (sales, inventory, prices)

CBS News identifies three major factors influencing rates and suggests proactive monitoring rather than passive waiting.

Application Timing Strategy

Peak Seasons: Spring and summer traditionally see higher purchase activity. Lender capacity can affect service quality and potentially pricing during these periods.

Off-Peak Advantages: Late fall and winter often bring less competition, potentially better service, and occasionally promotional rates.

Individual Timing: Apply when your financial profile is strongest-after receiving bonuses, when credit scores peak, or after vesting events for tech professionals in Kirkland and Redmond.

Common Mistakes That Cost Borrowers Better Rates

Avoiding these errors can improve your rate by 0.25%-0.50% or more.

Application Timing Errors

Mistake: Applying before credit optimization is complete

Impact: Lower credit score means higher rate for the entire loan term

Mistake: Major purchases between pre-approval and closing

Impact: Changed debt-to-income ratio can force rate renegotiation or denial

Mistake: Job changes during the mortgage process

Impact: Lenders require income stability; job changes can derail approval

Documentation Failures

Incomplete or disorganized documentation slows the process and can cause rate lock expirations. Gather these materials before starting:

- Two years of federal tax returns with all schedules

- Two months of bank statements for all accounts

- Most recent pay stubs covering 30 days

- W-2s from the past two years

- Complete employment history for two years

- Documentation of all income sources (RSUs, bonuses, rental income)

Shopping Too Narrowly

Comparing only one or two lenders limits your ability to find the best loan rates mortgage products. Apply with 3-5 lenders within a 14-day window-credit bureaus count these as a single inquiry, minimizing score impact.

Securing the best loan rates mortgage options in 2026 requires preparation, market knowledge, and strategic decision-making across multiple dimensions from credit optimization to lender selection. Whether you're a first-time buyer in Mill Creek, a tech professional relocating to Bellevue, or an investor expanding your Seattle portfolio, understanding how rates are determined and what factors you can control puts you in the strongest position to negotiate favorable terms. With over 25 years of experience helping Seattle-area clients navigate complex mortgage scenarios, including RSU qualification and rapid closings, Mortgage Reel provides the expertise and transparent guidance you need to secure competitive rates and close with confidence.