Finding the best mortgage loan requires understanding your financial profile, property goals, and the current lending landscape. In Seattle's competitive housing market, where home prices remain elevated and tech professionals navigate complex compensation structures, choosing the right mortgage product can save tens of thousands of dollars over the life of your loan. This guide walks through the essential factors that define a superior mortgage loan, from interest rates and closing costs to lender responsiveness and underwriting flexibility, helping you make an informed decision whether you're purchasing in Shoreline, refinancing in Lynnwood, or upgrading in Mill Creek.

Understanding What Makes a Mortgage Loan the Best Choice

The best mortgage loan isn't necessarily the one with the lowest advertised rate. It's the loan that aligns with your financial situation, timeline, and long-term plans while offering competitive pricing and reliable execution.

Key Components That Define Loan Quality

When evaluating mortgage options, several factors work together to determine overall value:

- Annual Percentage Rate (APR) captures the true cost including fees and points

- Loan term flexibility allows you to balance monthly payment with total interest paid

- Closing cost transparency prevents surprises at the settlement table

- Lender responsiveness ensures smooth communication throughout the process

- Underwriting speed and accuracy particularly critical in competitive Seattle-area markets

Many borrowers focus exclusively on the interest rate, but the best mortgage loan considers your complete financial picture. A first-time buyer in Lake Forest Park might prioritize low down payment options, while a tech professional at Microsoft with substantial RSU compensation might seek jumbo loan expertise and quick closing timelines.

Conventional Loans Versus Government-Backed Programs

The mortgage landscape offers distinct product categories, each serving different borrower profiles:

| Loan Type | Minimum Down Payment | Credit Score Requirement | Best For |

|---|---|---|---|

| Conventional | 3% (first-time buyers) | 620+ | Strong credit, flexible terms |

| FHA | 3.5% | 580+ | Lower credit scores, smaller down payments |

| VA | 0% | No minimum | Eligible veterans and service members |

| USDA | 0% | 640+ | Rural and suburban properties |

Conventional loans dominate Seattle's housing market because they offer competitive rates, no upfront mortgage insurance for 20% down, and higher loan limits suitable for the region's property values. According to recent market analysis from Yahoo Finance, borrowers with strong credit profiles continue to benefit from conventional loan pricing advantages in 2026.

For properties in Everett or Mill Creek where prices may fall below Seattle's median, FHA loans provide accessible entry points with lower down payment requirements. However, the ongoing mortgage insurance premium often makes conventional financing more cost-effective for borrowers who can manage 5-10% down.

Rate Shopping and Lender Comparison Strategies

Securing the best mortgage loan requires proactive comparison across multiple lenders. The Consumer Financial Protection Bureau recommends obtaining at least three loan estimates to identify the most favorable terms.

How to Compare Loan Estimates Effectively

When you receive Loan Estimates from different lenders, focus on these sections:

- Page 1, Section A: Compare interest rates and monthly principal and interest payments

- Page 1, Section B: Review projected costs at closing including down payment and closing costs

- Page 2, Section A: Examine origination charges and points

- Page 2, Section B: Analyze services you cannot shop for versus those you can

- Page 3: Review total cash needed at closing

The variation between lenders can be substantial. In Seattle's market, differences in underwriting overlays, pricing adjustments, and fee structures often create opportunities to save $3,000-$8,000 in closing costs or secure a rate 0.125-0.25% lower than initial quotes.

Understanding Rate Lock Timing and Strategy

Interest rates fluctuate daily based on bond market activity. Recent AP News reporting highlighted how the 30-year mortgage rate climbed to 6.85% in late 2025, demonstrating the volatility borrowers face.

The best mortgage loan strategy includes:

- Rate lock timing coordinated with your purchase timeline

- Lock period selection typically 30, 45, or 60 days based on closing date

- Float-down options that protect against rate increases while allowing decreases

- Extension policies understanding costs if closing delays occur

For competitive Seattle-area purchases where sellers prefer quick closes, working with a lender who can lock rates and close efficiently becomes essential. A 9-business-day closing capability means you can confidently lock your rate closer to closing, reducing extension risk.

Specialized Loan Programs for Seattle-Area Borrowers

Seattle's unique economic landscape creates specific mortgage needs that standard loan products don't always address optimally.

Jumbo Loans for High-Value Properties

With median home prices exceeding conventional loan limits in many Seattle neighborhoods, jumbo financing becomes necessary. The 2026 conforming loan limit is $806,500 for single-family homes in King County, but many properties exceed this threshold.

Jumbo loan considerations include:

- Credit score requirements typically 700-720 minimum

- Down payment expectations usually 10-20%

- Debt-to-income ratio scrutiny with more conservative thresholds

- Asset reserve requirements often 6-12 months of payments

- Interest rate pricing relative to conventional loans

The best mortgage loan for a $1.5 million property in Bellevue or Redmond requires a lender with jumbo expertise, competitive portfolio pricing, and underwriters who understand tech compensation structures.

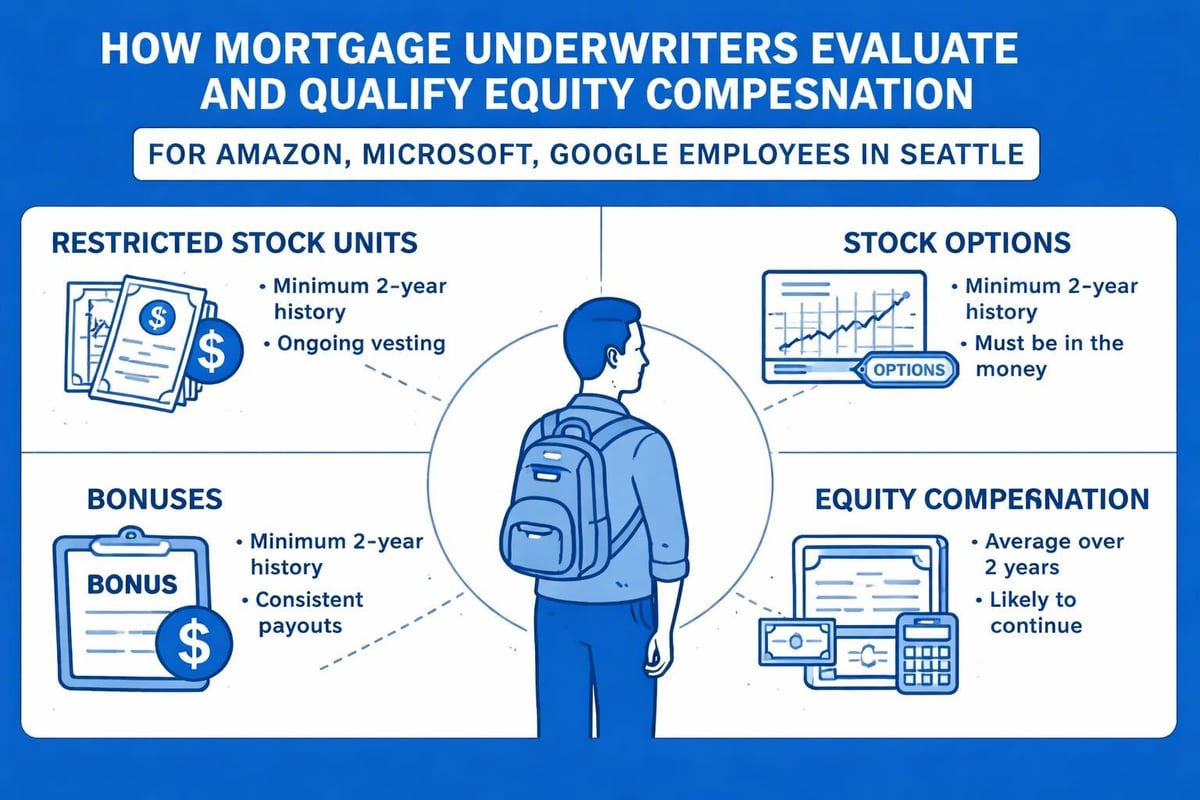

Qualifying RSUs and Stock Compensation

For the thousands of tech professionals working at Amazon, Microsoft, Google, and other Seattle-area employers, stock-based compensation represents a significant portion of income. Standard mortgage guidelines often struggle to properly credit this income.

The best mortgage loan approach for tech employees includes:

- Two-year vesting history to establish income continuity

- Proper documentation including vesting schedules and grant letters

- Underwriter experience with Fannie Mae and Freddie Mac guidelines for equity compensation

- Bonus and RSU calculation methods that maximize qualifying income

- Jumbo loan expertise since higher incomes often correlate with higher purchase prices

A loan officer experienced with tech compensation can often qualify $50,000-$150,000 more in income than lenders unfamiliar with these guidelines, directly impacting purchasing power in Seattle's expensive market.

Fixed-Rate Versus Adjustable-Rate Mortgages

Choosing between fixed and adjustable rates represents one of the most significant decisions in selecting the best mortgage loan for your situation.

When Fixed-Rate Mortgages Make Sense

Fixed-rate mortgages provide payment stability and predictability, ideal for:

- Long-term homeownership plans exceeding 7-10 years

- Budget certainty requirements where payment fluctuations create hardship

- Rising rate environments where locking current rates prevents future increases

- Primary residences where stability enhances quality of life

The 30-year fixed-rate mortgage remains the most popular choice in Seattle, offering manageable payments while building equity steadily. For borrowers prioritizing faster payoff and lower total interest, 15 and 20-year terms provide alternatives with significantly reduced interest costs.

Adjustable-Rate Mortgage Advantages

ARMs offer lower initial rates in exchange for potential future adjustments, creating opportunities for specific scenarios:

| ARM Feature | 5/1 ARM | 7/1 ARM | 10/1 ARM |

|---|---|---|---|

| Fixed period | 5 years | 7 years | 10 years |

| Typical rate advantage | 0.50-0.75% | 0.40-0.60% | 0.25-0.40% |

| Best for | Short-term ownership | Medium-term plans | Long-term with rate bet |

In Lynnwood or Shoreline, where buyers might plan to relocate within 5-7 years for career advancement, a 7/1 ARM could save $15,000-$25,000 compared to a 30-year fixed rate, with no exposure to rate adjustments during ownership.

Closing Speed and Lender Reliability Factors

The best mortgage loan combines competitive pricing with exceptional execution. In Seattle's competitive market, where multiple-offer scenarios remain common, lender performance directly impacts offer strength.

Why Closing Timeline Matters in Competitive Markets

When sellers receive multiple offers, they evaluate not just price but likelihood of successful closing. Key differentiators include:

- Pre-approval strength backed by underwriter review and documentation

- Lender reputation known to listing agents and sellers

- Typical closing timeline demonstrating ability to meet contract deadlines

- Communication standards ensuring smooth transaction coordination

A 9-business-day closing capability allows buyers to present offers with 14-day close terms, significantly strengthening competitiveness compared to conventional 30-45 day timelines. This speed requires advanced underwriting processes, efficient appraisal ordering, and experienced processing teams.

Evaluating Lender Reviews and Performance History

Research potential lenders through multiple channels:

- Google reviews for overall satisfaction and communication quality

- Zillow lender profiles showing transaction volume and ratings

- Redfin partner metrics if applicable to your search platform

- Real estate agent referrals based on past transaction experience

- Better Business Bureau ratings for complaint history and resolution

According to CNBC’s evaluation of top mortgage lenders, borrowers should prioritize lenders with consistent five-star ratings, transparent fee structures, and documented customer service excellence. Look for loan officers with hundreds of verified reviews across platforms, indicating sustained performance rather than isolated positive experiences.

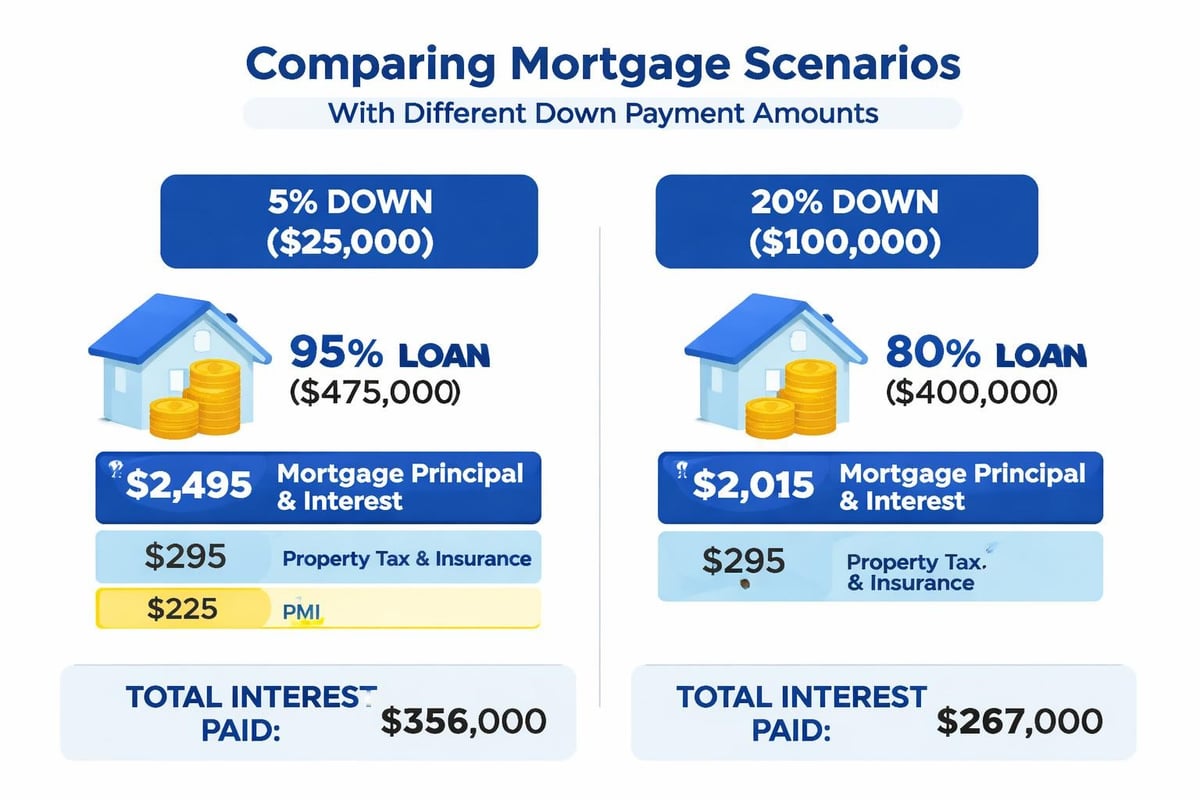

Down Payment Options and Private Mortgage Insurance

Down payment requirements significantly impact both immediate affordability and long-term loan costs, making this a critical component of identifying the best mortgage loan.

Minimum Down Payment Requirements by Loan Type

Modern mortgage programs offer various down payment thresholds:

- 3% conventional for qualified first-time buyers

- 5% conventional for repeat buyers with standard credit

- 10% conventional for strong positioning and reduced PMI costs

- 20% conventional eliminating private mortgage insurance entirely

- 0% VA for eligible veterans in Seattle and surrounding areas

For a $750,000 home in Mill Creek, the difference between 3% and 20% down represents $127,500 in upfront cash. However, the lower down payment creates ongoing PMI costs of approximately $400-$600 monthly until reaching 20% equity.

Private Mortgage Insurance Cost-Benefit Analysis

PMI makes homeownership accessible with smaller down payments but adds to monthly costs. Consider these factors:

- PMI rates typically range 0.5-1.5% of loan amount annually

- Cancellation timing automatically at 78% loan-to-value, requestable at 80%

- Tax deductibility limited based on income levels under current law

- Alternative strategies such as lender-paid PMI or piggyback loans

Calculate break-even points between saving for 20% down versus purchasing sooner with PMI. In appreciating markets like Seattle, home price increases often offset PMI costs, particularly when prices rise 5-8% annually.

Refinancing Considerations for Existing Homeowners

The best mortgage loan for current homeowners might involve refinancing to improve terms, access equity, or adjust loan structure.

Rate-and-Term Refinance Opportunities

When market rates drop significantly below your current rate, refinancing can reduce payments or shorten loan terms. Evaluate these factors:

- Rate improvement threshold typically 0.75-1.00% to justify closing costs

- Remaining loan term refinancing 7 years into a 30-year loan resets the clock

- Closing cost recovery calculating months to recoup expenses through savings

- Break-even analysis ensuring ownership timeline exceeds recovery period

For a $600,000 mortgage at 7.00%, refinancing to 6.25% saves approximately $280 monthly or $3,360 annually. With closing costs around $6,000-$8,000, break-even occurs in 21-28 months, making refinancing attractive for homeowners planning to stay beyond that timeframe.

Cash-Out Refinancing for Home Equity Access

Seattle-area homeowners have accumulated substantial equity through appreciation. Cash-out refinancing allows accessing this equity while potentially improving loan terms.

Common cash-out refinance uses include:

- Home renovations and improvements

- Debt consolidation at lower interest rates

- Investment property down payments

- Education funding or business capital

Conventional cash-out refinancing typically requires maintaining 20% equity after the transaction, meaning 80% maximum loan-to-value. For a home valued at $900,000 with a $400,000 existing mortgage, you could access up to $320,000 while maintaining 80% LTV.

Working with Experienced Local Mortgage Professionals

While online lenders and large national banks offer mortgage products, working with experienced local professionals provides distinct advantages in Seattle's unique market.

Benefits of Seattle-Area Mortgage Expertise

Local loan officers bring market-specific knowledge that enhances the mortgage experience:

- Property value understanding based on neighborhood trends and comparable sales

- Appraisal coordination with relationships to local appraisers familiar with specific areas

- Title and escrow partnerships ensuring smooth closing coordination

- Real estate agent relationships that strengthen your offers through reputation

- Local economic knowledge understanding tech industry cycles and employment patterns

For properties in Lake Forest Park or Everett, local expertise helps navigate unique challenges like septic systems, well water, or rural property classifications that can complicate financing.

The Value of Proven Track Records

Experience matters significantly in mortgage lending. A loan officer with 25+ years in the Seattle market has guided clients through multiple economic cycles, rate environments, and guideline changes.

Look for professionals who demonstrate:

- Extensive verified reviews across Google, Zillow, Redfin, and industry platforms

- Transparent communication explaining complex concepts clearly

- Proactive guidance anticipating challenges before they become problems

- Educational approach empowering informed decisions rather than pushing products

- Consistent availability responding to questions throughout the process

The Motley Fool’s 2025 Mortgage Lender Awards emphasized customer service and transparency as key differentiators among top-performing lenders, attributes best assessed through direct interaction and review analysis.

Technology and Modern Mortgage Platforms

The best mortgage loan experience in 2026 combines personal expertise with technological efficiency.

Digital Application and Documentation Systems

Modern mortgage platforms streamline the borrowing process through:

- Online applications completed in 15-20 minutes from any device

- Document upload portals eliminating fax and mail delays

- Electronic signature capabilities for disclosures and closing documents

- Real-time status tracking showing exactly where your loan stands

- Automated verification of income, assets, and employment

These technologies reduce processing time from weeks to days while maintaining accuracy and compliance. For busy tech professionals working at Amazon or Microsoft campuses in Seattle and Redmond, digital-first processes align with expectations for efficient, transparent transactions.

The Human Element in Complex Scenarios

While technology handles routine aspects efficiently, complex scenarios require experienced human judgment:

- Non-traditional income sources like RSU compensation or self-employment

- Credit challenges requiring strategic approaches and exception handling

- Property complications such as unique construction or mixed-use zoning

- Timing pressures in competitive offer situations requiring creative solutions

The ideal combination pairs technological efficiency for standard processes with accessible expertise for complex questions and unique situations.

Selecting the best mortgage loan requires balancing rate competitiveness, lender reliability, product flexibility, and expert guidance tailored to your specific situation. Whether you're purchasing your first home in Shoreline, upgrading to a larger property in Seattle, or refinancing in Mill Creek, the right mortgage partner makes a measurable difference in both immediate costs and long-term financial outcomes. Keith Akada at Mortgage Reel brings over 25 years of Seattle-area experience, 750+ five-star reviews, and specialized expertise in tech compensation and jumbo loans to help you navigate every aspect of the mortgage process with confidence and clarity.