Making informed decisions about home financing starts with knowing how to properly compare mortgage options. For homebuyers and homeowners in Seattle, Bellevue, and surrounding communities, understanding the nuances between different loan products, lenders, and rate structures can save tens of thousands of dollars over the life of a loan. In 2026's evolving real estate market, where tech professionals at companies like Amazon and Microsoft navigate complex compensation structures, the ability to evaluate mortgage offers becomes even more critical. This guide breaks down exactly what to compare, how to analyze offers side by side, and which factors matter most for your specific financial situation.

Understanding What to Compare When Shopping for a Mortgage

When you compare mortgage offers, you're evaluating far more than just the interest rate. Each loan estimate contains multiple components that directly impact your monthly payment, upfront costs, and long-term financial commitment.

The Consumer Financial Protection Bureau provides comprehensive guidance on reviewing loan estimates from multiple lenders. Their research shows that borrowers who obtain at least three quotes save an average of $3,000 over the life of their loan compared to those who only get one offer.

Key Components to Evaluate

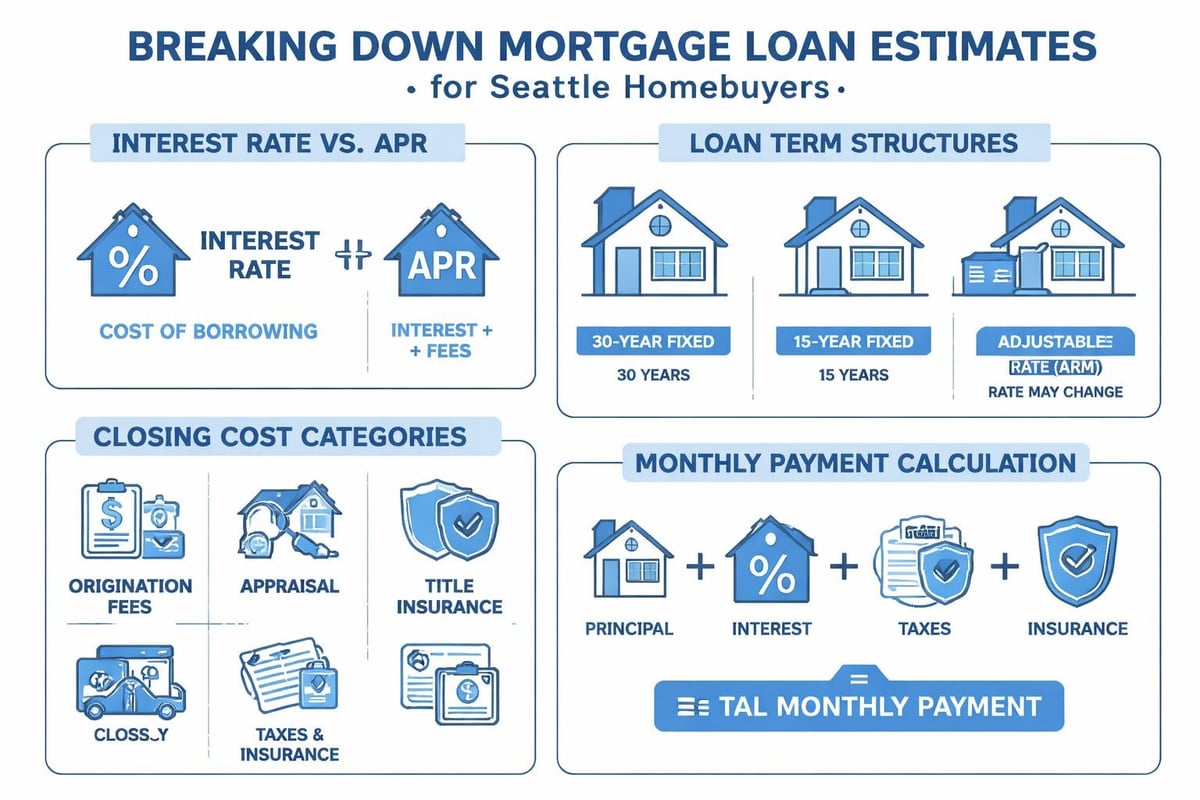

Interest Rate vs. APR: The interest rate determines your monthly principal and interest payment, while the Annual Percentage Rate (APR) includes the interest rate plus fees, giving you a more complete picture of borrowing costs. A lender might offer a lower rate but charge higher fees, resulting in a higher APR.

Loan Terms and Structure: Beyond the standard 30-year fixed mortgage, options include 15-year, 20-year, and adjustable-rate mortgages (ARMs). Each structure serves different financial goals and risk tolerances.

Closing Costs and Fees: These vary significantly between lenders and can include origination fees, appraisal costs, title insurance, and processing charges. In competitive markets like Shoreline and Lynnwood, understanding total closing costs helps you budget accurately.

How Different Mortgage Types Compare

The Greater Seattle housing market accommodates diverse buyer profiles, from first-time purchasers in Mill Creek to experienced investors in Bellevue. Each mortgage type offers distinct advantages depending on your situation.

| Mortgage Type | Typical Rate (2026) | Down Payment | Best For |

|---|---|---|---|

| Conventional | 6.50% – 7.00% | 3% – 20% | Strong credit, stable income |

| FHA | 6.25% – 6.75% | 3.5% | Lower credit scores, limited savings |

| VA | 6.00% – 6.50% | 0% | Military service members and veterans |

| Jumbo | 6.75% – 7.25% | 10% – 20% | High-balance loans in expensive markets |

Conventional Loans

Conventional mortgages remain the most common option for Seattle-area buyers with solid credit scores (typically 620 or higher) and stable employment. These loans conform to Fannie Mae and Freddie Mac guidelines, offering competitive rates and flexible term options. Freddie Mac’s mortgage comparison tools help borrowers understand how conventional loans stack up against other options.

When you compare mortgage rates for conventional products, you'll find that putting down 20% eliminates private mortgage insurance (PMI), reducing your monthly payment. However, lower down payment options exist for qualified buyers.

Government-Backed Programs

FHA loans serve buyers who may not qualify for conventional financing due to credit history or limited down payment funds. VA loans, available to eligible service members and veterans, often provide the most favorable terms with zero down payment and no ongoing mortgage insurance. For Seattle veterans looking to maximize these benefits, specialized VA loan programs offer strategic advantages.

Jumbo Loans for High-Balance Properties

In Seattle's expensive real estate market, where median home prices frequently exceed conventional loan limits ($1,063,750 in 2026 for King County), jumbo financing becomes necessary. These loans require stronger credit profiles and larger down payments but enable purchases of luxury properties in Kirkland, Medina, and downtown Seattle.

For tech employees with substantial RSU packages, 10% down jumbo programs provide access to higher-priced homes without depleting liquid savings needed for stock market opportunities.

Analyzing Interest Rates and Market Conditions

Interest rates fluctuate based on Federal Reserve policy, inflation expectations, and broader economic conditions. In early 2026, rates have stabilized compared to the volatility seen in previous years, but understanding rate trends remains essential when timing your mortgage application.

Current Rate Environment

As of March 2026, 30-year fixed mortgage rates hover between 6.50% and 7.00% for well-qualified borrowers. Shorter-term products like 15-year mortgages typically offer rates 0.50% to 0.75% lower. For buyers considering accelerated payoff strategies, 10-year mortgage rates provide even greater interest savings but require higher monthly payments.

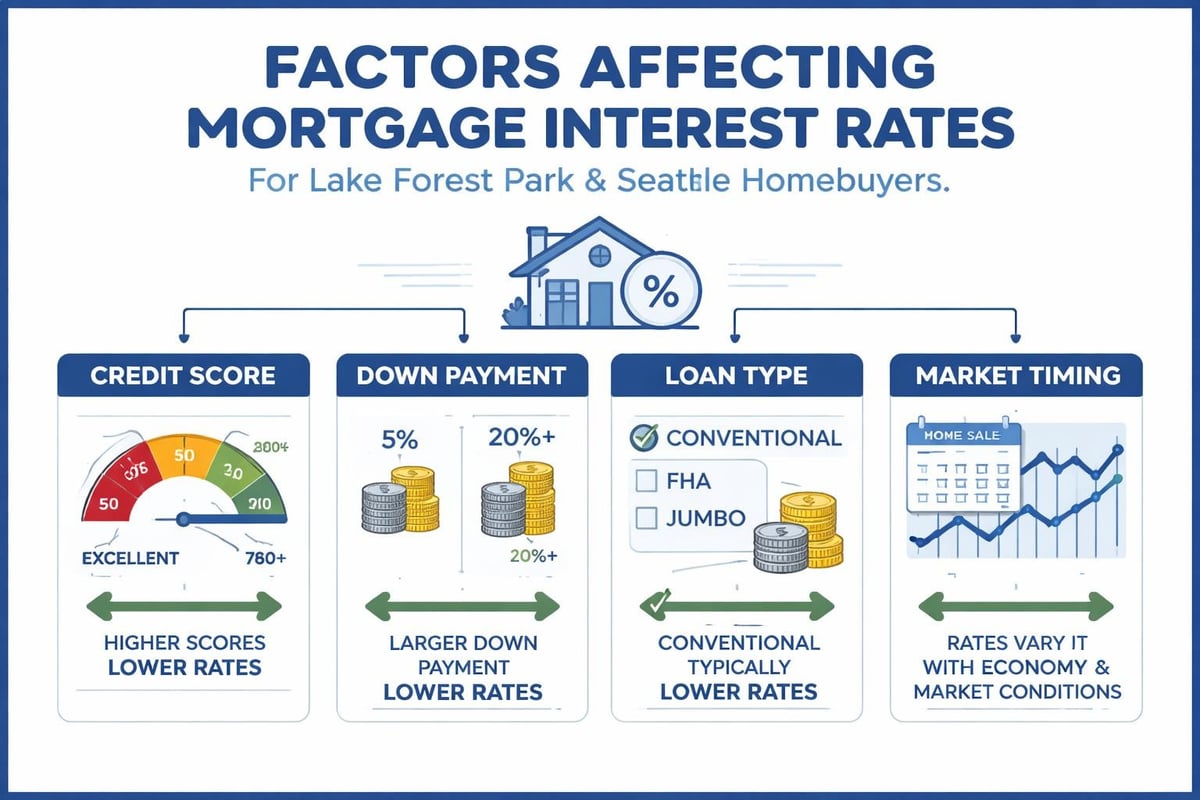

Factors Affecting Your Personal Rate:

- Credit score (higher scores unlock better rates)

- Loan-to-value ratio (more equity means lower rates)

- Property type (single-family homes vs. condos vs. investment properties)

- Loan amount (jumbo loans may carry rate premiums)

- Geographic location (local market conditions in Everett differ from Seattle proper)

Rate Lock Strategies

When you compare mortgage offers, pay attention to rate lock periods. A rate lock guarantees your quoted rate for a specified timeframe, typically 30 to 60 days. In competitive Seattle neighborhoods where purchase agreements move quickly, longer lock periods (45-60 days) provide security but may cost slightly more upfront.

Evaluating Lender Options and Service Quality

The lender you choose matters as much as the loan terms you receive. Response time, underwriting flexibility, and closing speed directly impact your ability to compete for homes in fast-moving markets like Bellevue and Redmond.

Big Banks vs. Mortgage Brokers vs. Credit Unions

Each lender type offers different advantages. Large national banks provide stability and extensive product menus but may lack personalized service. Credit unions often offer competitive rates to members but may have limited hours and slower processing times. Mortgage brokers access multiple wholesale lenders, providing broader options and potentially better rates through increased competition.

When Underwriting Flexibility Matters:

Tech professionals with complex income structures benefit from lenders experienced in qualifying stock-based compensation. Standard automated underwriting systems may not properly evaluate RSUs, options, or performance bonuses. Specialized brokers understand how to document and maximize these income sources for qualification purposes.

Communication and Responsiveness

In Seattle's competitive market, where multiple-offer scenarios are common, lender speed and availability can determine whether your offer gets accepted. Sellers and listing agents prefer buyers with pre-approvals from responsive lenders who can close quickly and navigate contingencies smoothly.

Look for lenders who:

- Return calls and emails within a few hours

- Provide clear timelines and expectations

- Proactively communicate about needed documentation

- Have underwriting authority to make decisions quickly

Comparing Costs Beyond the Interest Rate

When you compare mortgage options, total costs extend far beyond monthly payments. Understanding the full financial picture prevents surprises and helps you budget appropriately.

Upfront Costs and Closing Fees

Closing costs typically range from 2% to 5% of the loan amount. On a $900,000 home in Seattle with 20% down ($180,000), you might finance $720,000 and pay $14,400 to $36,000 in closing costs.

| Fee Category | Typical Range | Negotiable? |

|---|---|---|

| Origination Fee | 0% – 1% of loan | Yes |

| Appraisal | $600 – $1,200 | Limited |

| Title Insurance | $1,500 – $3,500 | Yes (shop around) |

| Escrow/Attorney | $800 – $1,500 | Limited |

| Recording Fees | $200 – $400 | No |

The CFPB’s rate exploration tool helps you understand how different factors affect not just rates but overall costs.

Points and Rate Buydowns

Discount points allow you to pay upfront fees to reduce your interest rate. One point equals 1% of the loan amount and typically reduces your rate by 0.25%. Whether points make sense depends on how long you plan to keep the loan.

Example: On a $720,000 loan, one point costs $7,200 and might reduce your rate from 6.75% to 6.50%. The monthly savings would be approximately $110, meaning you'd break even after 65 months (about 5.5 years). If you plan to stay in the home longer, points could save money long-term.

Ongoing Costs

Don't forget to factor in property taxes (approximately 1% of home value annually in King County), homeowners insurance ($1,200-$2,500 annually), HOA fees (common in Seattle condos), and potential PMI if putting down less than 20%.

Using Comparison Tools and Calculators Effectively

Technology simplifies the process when you compare mortgage options. Several sophisticated calculators help you model different scenarios and understand long-term implications.

Recommended Calculation Approaches

TDECU’s mortgage comparison calculator allows side-by-side evaluation of up to three different mortgage options, showing monthly payments, total interest paid, and overall cost differences.

Key Metrics to Calculate:

- Monthly principal and interest payment

- Total monthly housing payment (including taxes, insurance, HOA)

- Total interest paid over loan life

- Break-even point for points or rate buydowns

- Equity build-up timeline

Scenario Modeling

Run multiple scenarios to understand how different choices affect outcomes. Compare a 30-year fixed at 6.75% against a 15-year at 6.00%. Model 5% down versus 10% down on a jumbo purchase. Test how extra principal payments affect payoff timelines.

For buyers in Lynnwood or Everett considering different property price ranges, modeling helps determine comfortable budget limits based on actual payment obligations.

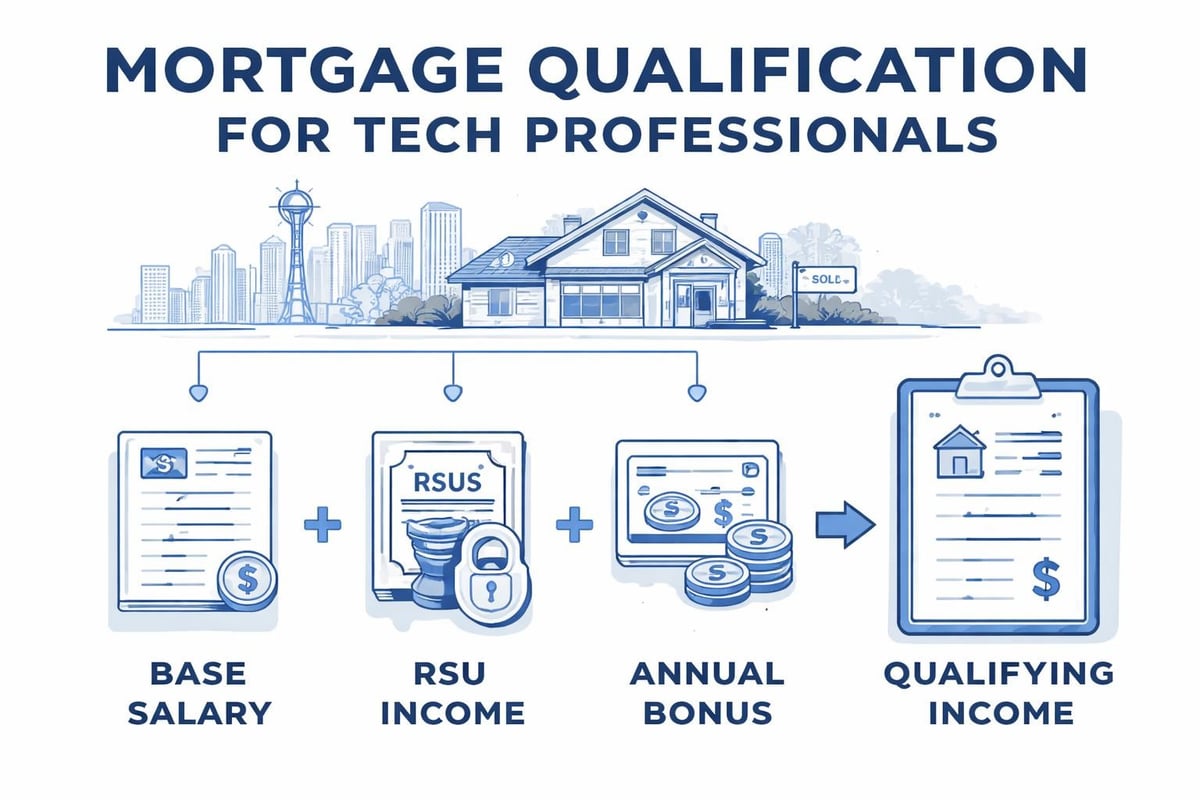

Special Considerations for Seattle-Area Tech Professionals

The concentration of technology employers in the Greater Seattle area creates unique mortgage considerations. Understanding how to properly document and utilize stock-based compensation maximizes buying power.

Qualifying Income from RSUs and Stock Options

Restricted Stock Units (RSUs) can be included as qualifying income once they vest and convert to cash. Lenders typically require two years of RSU history and average the amounts received. For Microsoft or Amazon employees with substantial RSU packages, this can add $50,000 to $200,000+ in qualifying income.

Documentation Requirements:

- Two years of W-2s showing RSU income

- Recent pay stubs reflecting vesting schedule

- Letter from employer confirming ongoing grants

- Stock award statements showing future vesting

Jumbo Loan Strategies

When comparing jumbo mortgage options, focus on lenders experienced with high-earning professionals. Understanding jumbo loan structures helps you leverage equity and income effectively while maintaining liquidity for investments and emergencies.

Some jumbo programs offer:

- Down payments as low as 10%

- No PMI even with less than 20% down

- Higher debt-to-income ratio allowances

- Portfolio lending flexibility for unique situations

Questions to Ask When You Compare Mortgage Lenders

Armed with the right questions, you can quickly identify which lenders deserve serious consideration and which ones to eliminate from your search.

Essential Lender Questions

About Rates and Terms:

- What is your interest rate and APR for my specific situation?

- How long is the rate lock period?

- What are your total closing costs itemized?

- Do you charge origination fees or broker fees?

- Are there prepayment penalties?

About Process and Timeline:

- What is your typical closing timeline?

- How quickly can you provide pre-approval?

- Who will be my main point of contact?

- What underwriting overlays do you have beyond standard guidelines?

- Can you close in 14-21 days if needed for a competitive offer?

About Experience:

- How many loans did you close in the Seattle area last year?

- Do you have experience with my employment type or income structure?

- Can you provide references from recent clients?

- What percentage of your loans close on time?

Leveraging Multiple Offers for Better Terms

Obtaining multiple loan estimates gives you negotiating power. Most lenders will match or beat competitor offers when presented with documented alternatives.

Effective Negotiation Tactics

Request loan estimates from at least three lenders within a short timeframe (7-14 days). Multiple mortgage inquiries within a focused period count as a single credit pull for scoring purposes, protecting your credit score.

Once you receive estimates, compare them using a standard format. The CFPB’s comparison guide provides a clear framework for evaluation.

What You Can Negotiate:

- Origination fees or broker compensation

- Rate (especially if you have competing offers)

- Closing cost credits

- Rate lock extensions

- Appraisal or inspection fee waivers

Timing Your Rate Shop

Market rates change daily. When you compare mortgage rates, do so when you're genuinely ready to move forward within 30-60 days. Rate shopping too early means quotes become outdated before you need them.

In Seattle's market, spring and summer typically see increased competition and potentially higher rates due to demand, while winter months may offer slight advantages.

Understanding the Full Loan Estimate Document

The standardized Loan Estimate form, required within three business days of application, contains all essential information needed to compare mortgage offers accurately.

Page-by-Page Breakdown

Page 1 shows loan amount, interest rate, monthly payment, and estimated cash to close. This summary provides quick comparison points.

Page 2 details closing costs broken into categories: origination charges, services you can shop for, services you cannot shop for, taxes and government fees, and prepaids. This granularity reveals where costs accumulate.

Page 3 presents final calculations and additional information about escrow accounts, payment adjustments (for ARMs), penalties, and assumptions about property costs.

Red Flags to Watch For

Certain elements in loan estimates should prompt additional questions or reconsideration:

- Origination fees exceeding 1% of the loan amount

- Unusually high processing or underwriting fees

- Significant differences between interest rate and APR (indicating high fees)

- Prepayment penalties on fixed-rate loans

- Escrow shortfalls or large monthly escrow payments

Local Market Factors in Seattle and Surrounding Areas

Geographic differences within the Greater Seattle area affect mortgage decisions. Understanding neighborhood-specific factors helps you compare mortgage options more effectively.

Property Type Considerations

Seattle's dense urban core features numerous condominiums, which may require larger down payments (typically 20-25%) and face stricter lending requirements than single-family homes in Lake Forest Park or Mill Creek. Warrantability issues with condo buildings can limit financing options.

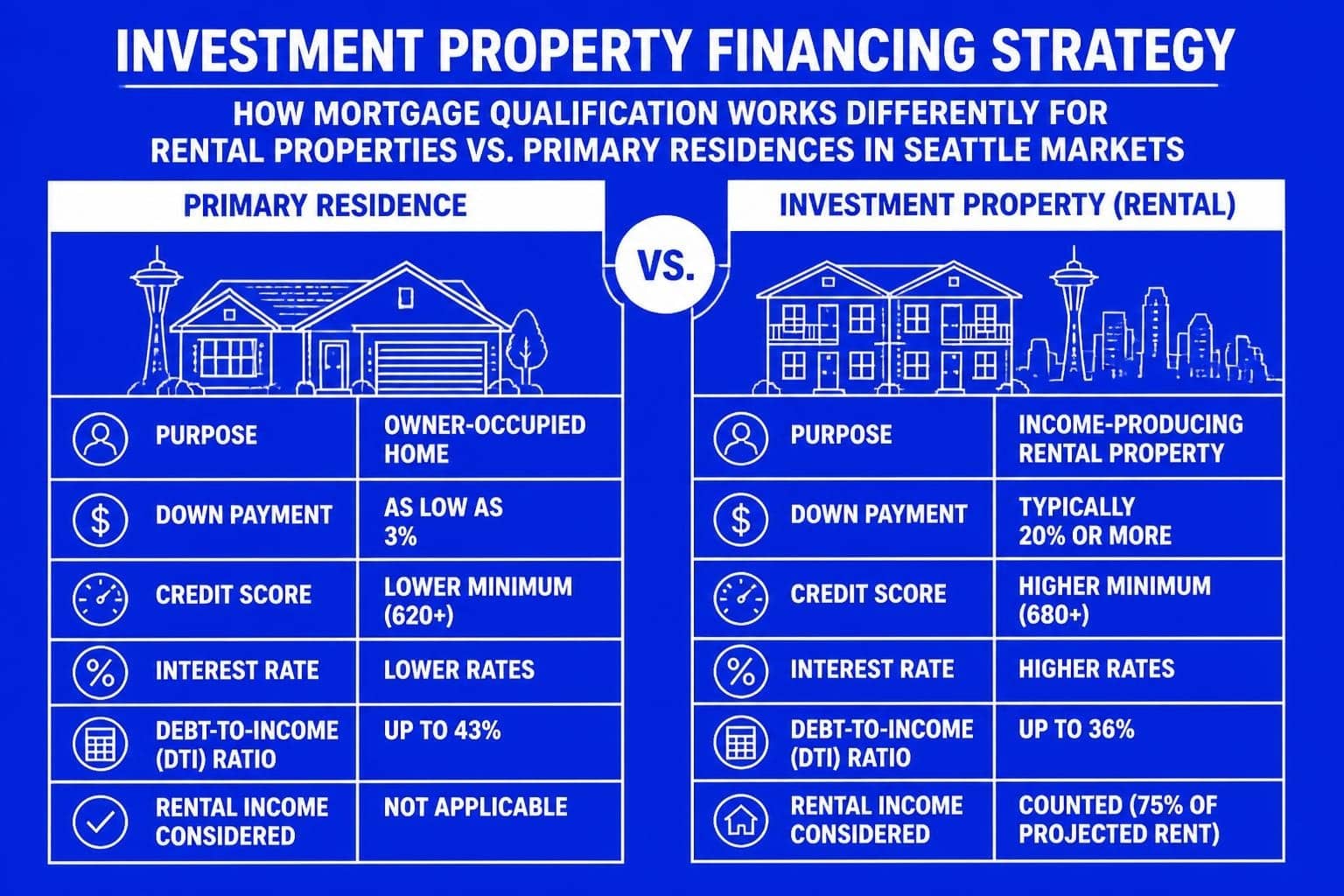

Investment properties and second homes face different rate structures, typically 0.50% to 1.00% higher than primary residences, with larger down payment requirements.

Competitive Offer Environments

In neighborhoods with low inventory and high demand, buyers who compare mortgage lenders for closing speed gain significant advantages. The ability to close in 14-21 days versus 45 days can make your offer more attractive to sellers, sometimes worth more than a slightly higher purchase price.

Pre-approval strength matters. Detailed pre-approvals with complete underwriting review demonstrate seriousness and capability compared to basic pre-qualification letters.

Refinance Considerations: When to Compare New Options

Existing homeowners should periodically compare mortgage options even after closing. Refinancing opportunities arise when rates drop, home values increase, or financial situations change.

Strategic Refinance Timing

Rate-and-Term Refinance: Worth considering when you can reduce your rate by at least 0.50% to 0.75%, depending on closing costs and break-even timeline. Current refinance rate trends help you gauge whether market conditions favor refinancing.

Cash-Out Refinance: Allows you to tap home equity for home improvements, debt consolidation, or investment purposes. In appreciating markets like Bellevue and Redmond, homeowners accumulate substantial equity that can be leveraged strategically.

Break-Even Analysis

Calculate how long it takes for monthly savings to offset refinancing costs. If closing costs total $8,000 and you save $200 monthly, your break-even point is 40 months. If you plan to stay in the home longer, refinancing makes financial sense.

Advanced Strategies for Optimizing Your Mortgage Selection

Beyond basic comparison, sophisticated approaches help you maximize value and minimize long-term costs.

Hybrid ARM Strategies

Adjustable-rate mortgages (ARMs) with initial fixed periods (5/1, 7/1, or 10/1) offer lower starting rates than 30-year fixed mortgages. For buyers who plan to relocate within the fixed period-common among tech professionals who may transfer to other offices-ARMs provide significant savings without rate risk.

Example: A 7/1 ARM might offer 6.00% versus 6.75% on a 30-year fixed. On a $720,000 loan, that's $300 monthly savings ($3,600 annually). Over seven years, you save $25,200 before the rate adjusts.

Bi-Weekly Payment Programs

While some lenders charge fees for bi-weekly payment programs, you can create the same effect independently by making one extra monthly payment annually. This reduces a 30-year mortgage to approximately 25 years and saves significant interest.

Portfolio Diversification

For high-income borrowers with substantial assets, maintaining mortgage debt while investing excess cash may yield better long-term returns. When you compare mortgage options, consider opportunity costs. If you can earn 8% annually in investments while paying 6.75% on a mortgage, leveraging the loan while investing cash could build more wealth than paying off the home quickly.

Choosing the right mortgage requires thorough comparison of rates, terms, costs, and lender capabilities-especially in competitive markets throughout the Seattle area. Understanding how to evaluate loan estimates, negotiate terms, and align mortgage structure with your financial goals positions you for both immediate and long-term success. Whether you're purchasing in Shoreline, refinancing in Everett, or navigating complex compensation as a tech professional, working with an experienced broker who understands local market dynamics makes all the difference. Mortgage Reel brings 25+ years of expertise and hundreds of five-star reviews to help Seattle-area homebuyers and homeowners make confident, informed mortgage decisions with transparent guidance and reliable execution.