Conventional house loans remain the most popular financing choice for homebuyers across the Seattle metro area, offering flexibility and competitive terms that appeal to a wide range of borrowers. Unlike government-backed mortgages such as FHA or VA loans, conventional house loans are not insured by federal agencies, which means they follow guidelines set by private entities like Fannie Mae and Freddie Mac. For buyers in Seattle, Bellevue, Redmond, and surrounding communities, understanding how these loans work is essential to making informed decisions in one of the nation's most competitive housing markets. Whether you're a first-time buyer in Lake Forest Park or a tech professional in Kirkland looking to leverage stock compensation for a larger purchase, conventional financing offers distinct advantages worth exploring.

What Defines Conventional House Loans

Conventional house loans are mortgages that conform to the lending standards established by Fannie Mae and Freddie Mac, the government-sponsored enterprises that purchase and guarantee these loans on the secondary market. The Consumer Financial Protection Bureau provides comprehensive guidance on how these loans differ from government-insured options.

These loans fall into two primary categories: conforming and non-conforming. Conforming loans meet the maximum loan limits set annually by the Federal Housing Finance Agency, while non-conforming loans exceed these limits and are commonly referred to as jumbo loans. In King County and Snohomish County for 2026, the conforming loan limit stands at $806,500 for single-family homes, though this threshold gets adjusted based on median home prices.

Key Characteristics That Set Conventional Loans Apart

Several distinguishing features make conventional house loans unique in the mortgage landscape:

- No government insurance: Lenders assume more risk, which translates to stricter qualification requirements

- Flexible loan amounts: Available for purchases ranging from modest condos to multimillion-dollar estates

- Varied down payment options: Minimum requirements start as low as 3% for qualified borrowers

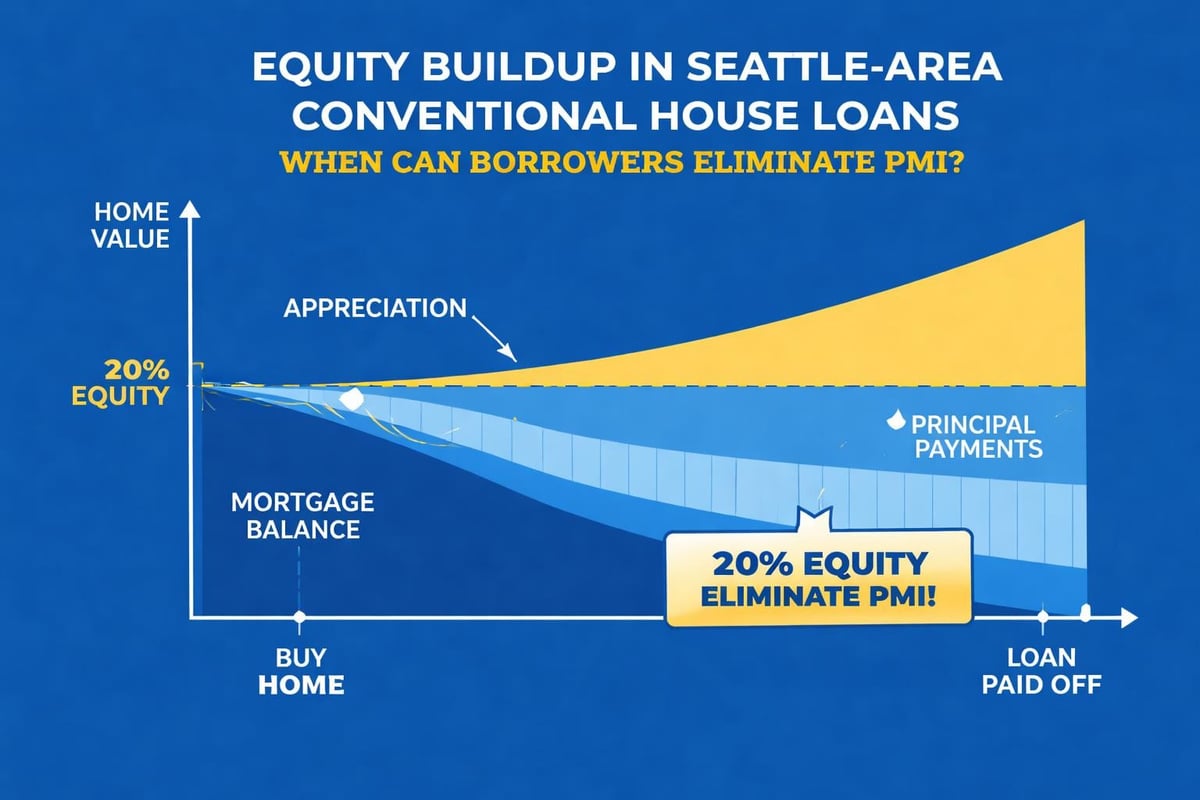

- Private mortgage insurance (PMI): Required when down payments fall below 20%, but can be removed once equity reaches that threshold

- Competitive interest rates: Often lower than government-backed alternatives for borrowers with strong credit profiles

The absence of government backing means lenders evaluate borrowers more rigorously, examining credit history, debt-to-income ratios, employment stability, and asset reserves with careful scrutiny.

Qualification Requirements for Seattle-Area Borrowers

Securing approval for conventional house loans requires meeting specific benchmarks that demonstrate financial stability and repayment capacity. Lenders assess multiple factors simultaneously to determine eligibility and pricing.

Credit Score Expectations

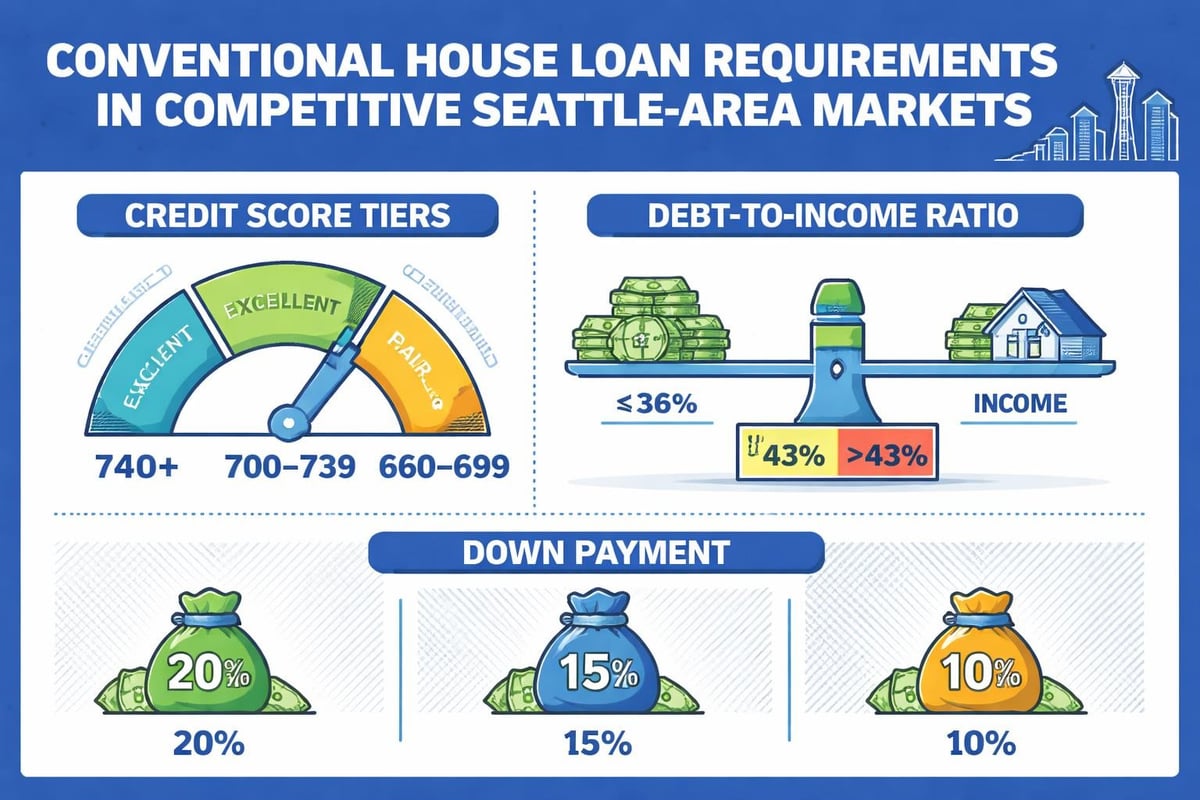

Most conventional loan programs require a minimum credit score of 620, though this baseline doesn't guarantee the best rates or terms. Borrowers in the Seattle area typically benefit from maintaining scores above 740, which unlocks preferential pricing and lower interest rates.

For tech professionals working at Amazon, Microsoft, or Google who may have limited credit history due to recent immigration or career transitions, building credit strategically becomes crucial. Even a difference of 20 points in your credit score can affect your interest rate by 0.25% to 0.5%, which translates to thousands of dollars over a 30-year mortgage.

Income and Employment Verification

Lenders verify employment history spanning at least two years, looking for stability and consistent income patterns. For W-2 employees in Shoreline or Lynnwood, this process remains straightforward with recent pay stubs and tax returns.

Self-employed borrowers face additional documentation requirements, typically needing two years of personal and business tax returns along with profit-and-loss statements. The key challenge involves demonstrating sustainable income after accounting for business deductions that may reduce taxable income but also affect qualifying capacity.

Specialized income considerations for Seattle-area tech workers include:

- Restricted Stock Units (RSUs) evaluated using specific vesting schedules

- Stock options counted when exercisable and verifiable

- Annual bonuses analyzed for consistency over multiple years

- Sign-on bonuses generally excluded unless structured as guaranteed compensation

Down Payment Options and PMI Considerations

One persistent misconception suggests conventional house loans always require 20% down payments. While putting down 20% eliminates private mortgage insurance and reduces monthly payments, multiple lower down payment programs exist for qualified borrowers.

| Down Payment | PMI Required | Typical Use Case | Monthly Impact |

|---|---|---|---|

| 3% | Yes | First-time buyers, limited savings | Higher payment + PMI |

| 5% | Yes | Standard conventional purchase | Moderate payment + PMI |

| 10% | Yes | Stronger equity position | Lower payment + reduced PMI |

| 20% | No | Eliminate PMI, lower rate | Lowest payment, best rate |

Understanding the various types of conventional loans helps borrowers match their financial situation with the most appropriate program structure.

How Private Mortgage Insurance Works

When borrowers put down less than 20%, lenders require PMI to protect against default risk. Unlike FHA mortgage insurance, which remains for the loan's life in many cases, conventional PMI can be removed once the loan balance reaches 80% of the home's original value or current appraised value.

PMI costs typically range from 0.3% to 1.5% of the original loan amount annually, divided into monthly payments. On a $600,000 home in Mill Creek with 5% down, PMI might add $250 to $475 monthly depending on credit score and coverage percentage.

Smart borrowers track their equity accumulation carefully. In Seattle's appreciating market, home values often increase substantially within a few years, allowing owners to request PMI removal earlier than the standard amortization schedule would indicate.

Interest Rates and Loan Terms

Conventional house loans offer flexibility in term selection, with 30-year and 15-year fixed-rate mortgages representing the most common choices. Adjustable-rate mortgages (ARMs) provide another option, featuring lower initial rates that adjust after a specified period.

Fixed-Rate vs. Adjustable-Rate Structures

30-year fixed-rate mortgages deliver payment stability and predictability, making budgeting easier for buyers planning to stay in their Everett or Bellevue homes long-term. The extended amortization period results in higher total interest paid but keeps monthly payments manageable.

15-year fixed-rate mortgages come with higher monthly payments but significantly lower total interest costs and faster equity accumulation. These work well for established professionals with strong income and career stability who want to build wealth more quickly.

Adjustable-rate mortgages such as 5/1, 7/1, or 10/1 ARMs offer reduced initial interest rates for borrowers who anticipate moving or refinancing before the adjustment period begins. In Seattle's dynamic tech economy, where job relocations and career moves happen frequently, ARMs can provide substantial savings for those planning shorter ownership periods.

Current Rate Environment Considerations

Interest rates fluctuate based on broader economic conditions, Federal Reserve policy, inflation expectations, and bond market movements. Conventional house loans typically offer slightly lower rates than government-backed alternatives for borrowers with excellent credit because the loans carry less risk from the lender's perspective.

Rate locks protect borrowers from increases during the closing process, typically available for 30 to 60 days. Extended locks covering longer periods may incur additional costs but provide security in volatile rate environments.

Property Type Eligibility and Loan Limits

Conventional house loans accommodate diverse property types, making them versatile for various housing needs across the Seattle metro area. This flexibility extends from urban condos to suburban single-family homes and even investment properties.

Approved Property Categories

- Single-family residences: The most straightforward category with the fewest restrictions

- Condominiums: Must meet specific project approval standards from Fannie Mae or Freddie Mac

- Townhouses: Treated similarly to single-family homes when structured as fee-simple ownership

- Multi-unit properties: Up to four units qualify, with increasing down payment requirements for additional units

- Manufactured homes: Eligible when permanently affixed to owned land and meeting construction standards

Second homes and investment properties also qualify for conventional financing, though they require larger down payments and may carry slightly higher interest rates than primary residences.

Navigating Conforming Loan Limits

For 2026, the conforming loan limit in King and Snohomish counties sits at $806,500 for single-family homes. Properties requiring financing above this threshold need jumbo loans, which represent a subset of non-conforming conventional mortgages.

Jumbo loans in Seattle's expensive housing market often require:

- Minimum down payments of 10% to 20%

- Higher credit score requirements (typically 700+)

- More substantial cash reserves (6 to 12 months of payments)

- Lower debt-to-income ratios (typically 43% or less)

For buyers pursuing homes in neighborhoods like Madison Park, Queen Anne, or Medina where median prices exceed conforming limits, understanding jumbo qualification becomes essential. Tech professionals with significant equity compensation often find these loans accessible despite the stricter requirements.

Debt-to-Income Ratio Requirements

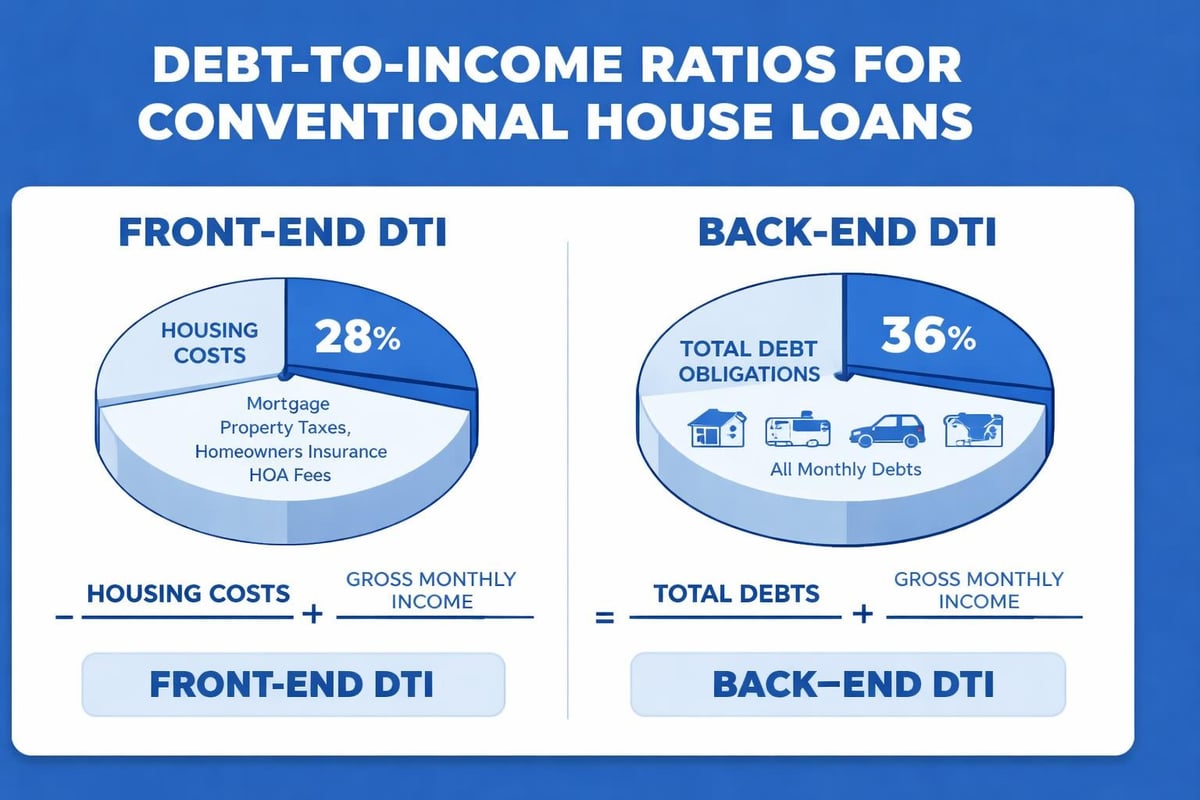

Your debt-to-income (DTI) ratio measures monthly debt obligations against gross monthly income, serving as a critical underwriting factor for conventional house loans. Lenders examine both front-end and back-end ratios to assess affordability.

Front-end DTI calculates housing expenses (principal, interest, taxes, insurance, and HOA fees) as a percentage of gross income. Conventional loans typically allow up to 28%, though this can be exceeded with compensating factors.

Back-end DTI includes all monthly debt obligations: housing expenses plus car payments, student loans, credit card minimum payments, and other installment debts. The standard maximum sits at 43% for conventional financing, though some programs allow up to 50% with strong credit and reserves.

Strategies for Improving DTI Ratios

Borrowers in competitive positions can optimize their ratios through several approaches:

- Pay down revolving debt: Reducing credit card balances improves DTI more quickly than paying installment loans

- Increase income documentation: Ensure all qualifying income sources are properly documented and considered

- Restructure debt: Refinancing high-payment debts to lower monthly obligations

- Request higher limits: Increasing credit limits without increasing balances lowers utilization ratios

For buyers in Lynnwood or Lake Forest Park facing Seattle's high housing costs, managing DTI effectively often determines whether they qualify for desired properties.

Documentation Requirements and Underwriting Process

The conventional loan underwriting process involves comprehensive financial documentation to verify all aspects of your application. Being prepared with organized documents accelerates approval and reduces stress during the closing period.

Standard Documentation Checklist

Income verification materials:

- Recent pay stubs covering 30 days

- W-2 forms for the previous two years

- Tax returns (personal and business if self-employed)

- Year-to-date profit and loss statements for business owners

- Award letters and vesting schedules for RSUs and stock compensation

Asset documentation:

- Bank statements for all accounts (typically 2 months)

- Investment account statements

- Retirement account statements (for reserve requirements)

- Documentation of gift funds including donor letters

- Paper trail for large deposits requiring explanation

Additional requirements:

- Government-issued identification

- Proof of homeowners insurance

- Purchase agreement and addendums

- Condominium documentation (if applicable)

- Employment verification (lenders contact employers directly)

The FDIC’s consumer resource center offers valuable tips for navigating the mortgage process and understanding lender requirements.

Timeline Expectations

Conventional house loans typically close within 30 to 45 days, though experienced lenders with efficient processes can accelerate this timeline. Working with a mortgage broker who understands Seattle's competitive market becomes crucial when making offers that require quick closings.

Processing begins immediately after application, with initial disclosures delivered within three business days. The underwriter reviews documentation, orders appraisals, and requests additional information as needed. Clear-to-close status arrives once all conditions are satisfied, usually a few days before the scheduled closing date.

Advantages of Choosing Conventional Financing

Conventional house loans offer compelling benefits that make them the preferred choice for many Seattle-area borrowers, particularly those with strong financial profiles and stable employment.

Flexibility and Customization

Unlike government-backed programs with rigid guidelines, conventional loans provide greater flexibility in structuring terms, choosing loan amounts, and selecting property types. This adaptability proves valuable in diverse scenarios from starter condos in Shoreline to luxury estates in Bellevue.

Borrowers can also explore 20 percent down home loans to eliminate PMI and access the most competitive rates available in the market.

Lower Long-Term Costs

For borrowers who qualify for premium pricing, conventional house loans often deliver the lowest total costs over time. The absence of upfront mortgage insurance premiums (unlike FHA loans) and the ability to remove PMI once equity reaches 20% create significant savings.

Investment property financing through conventional loans, while requiring higher down payments, avoids the restrictions that prevent using government-backed programs for non-owner-occupied properties. This makes conventional financing the only viable option for building rental portfolios in growing Seattle suburbs like Mill Creek or Everett.

Common Challenges and How to Address Them

Even well-qualified borrowers sometimes encounter obstacles during the conventional loan process. Recognizing potential challenges and preparing solutions improves outcomes and reduces transaction stress.

Appraisal Issues in Competitive Markets

Seattle's strong housing market occasionally creates situations where appraisals come in below purchase prices, particularly during bidding wars. When this happens, buyers face several options:

- Negotiate with sellers to reduce the purchase price to match the appraisal

- Increase down payment to cover the gap between appraisal and price

- Challenge the appraisal with comparable sales data supporting a higher value

- Walk away using appraisal contingencies if the gap cannot be reconciled

Working with an experienced mortgage professional helps navigate these scenarios with strategies that protect your interests while maintaining transaction momentum.

Complex Income Structures

Tech professionals in Seattle often receive compensation through multiple channels: base salary, RSUs, bonuses, and stock options. Properly documenting and qualifying this income requires expertise in both underwriting guidelines and technology industry compensation structures.

Lenders examine vesting schedules, historical patterns, and likelihood of continuation when evaluating equity compensation. A two-year history of RSU income provides the strongest foundation, though shorter histories may work with additional documentation and conservative calculations.

Refinancing Considerations with Conventional Loans

Conventional house loans also serve homeowners seeking to refinance existing mortgages, whether to lower rates, access equity, or change loan terms. The same qualification standards apply, though the process focuses on current home value rather than purchase price.

Rate-and-Term Refinancing

This straightforward refinance replaces your existing mortgage with a new loan, ideally at a lower interest rate or more favorable term. Borrowers typically pursue this option when rates drop significantly or when they want to switch from an ARM to a fixed-rate mortgage for stability.

The break-even analysis considers closing costs against monthly savings to determine whether refinancing makes financial sense. Generally, if you plan to stay in the home long enough to recoup closing costs through reduced payments, refinancing proves worthwhile.

Cash-Out Refinancing

Cash-out refinances allow homeowners to tap accumulated equity, receiving the difference between the new loan amount and existing mortgage balance in cash. These funds commonly finance home improvements, consolidate higher-interest debt, or fund major expenses.

Conventional cash-out refinances typically limit loan-to-value ratios to 80%, meaning you need at least 20% equity after the refinance. Requirements remain similar to purchase loans, with credit score minimums, DTI limits, and income verification applying equally.

Comparing Conventional to Government-Backed Alternatives

Understanding how conventional house loans stack up against FHA, VA, and USDA loans helps borrowers select the optimal financing for their situations. Each program serves different needs with unique advantages and limitations.

| Loan Type | Min. Down Payment | Credit Score Requirement | Mortgage Insurance | Property Type Flexibility |

|---|---|---|---|---|

| Conventional | 3% | 620+ | Removable PMI | Excellent |

| FHA | 3.5% | 580+ | Permanent MIP | Limited |

| VA | 0% | No minimum | None | Good |

| USDA | 0% | 640+ | Annual fee | Rural only |

For first-time buyers in Seattle considering different options, exploring various mortgage types provides essential context for informed decision-making.

When Conventional Makes the Most Sense

Conventional financing typically emerges as the best choice when:

- Your credit score exceeds 680

- You can afford at least 5% down payment

- You're purchasing in urban or suburban areas (not rural)

- The property exceeds FHA loan limits

- You're buying a condo that doesn't meet FHA approval requirements

- You want to eliminate mortgage insurance after reaching 20% equity

For Seattle-area buyers with strong financial profiles, conventional house loans deliver optimal terms and maximum flexibility across the widest range of scenarios.

Working with Lenders and Mortgage Professionals

Selecting the right lending partner significantly impacts your conventional loan experience, affecting everything from interest rates to closing timeline and ongoing support. Not all lenders offer equivalent service, expertise, or product availability.

What to Look for in a Mortgage Broker

Experience in your local market matters tremendously. A broker familiar with Seattle's competitive environment understands how to structure offers that appeal to sellers, manages appraisal challenges unique to the area, and knows which underwriters handle complex income scenarios effectively.

Look for professionals who:

- Provide transparent rate quotes with detailed fee breakdowns

- Explain options clearly without pushing specific products

- Respond promptly to questions and concerns

- Have established relationships with multiple lenders

- Understand tech industry compensation and can qualify RSUs effectively

- Offer competitive closing timelines to strengthen offers

Reading reviews across platforms like Google, Zillow, and Redfin reveals patterns in how brokers serve clients, communicate during stress points, and deliver on commitments. Consistent five-star ratings across hundreds of transactions indicate reliable performance.

The Value of Local Expertise

Seattle's housing market operates differently than national averages, with unique factors including:

- Bidding wars that require quick preapprovals and decisive action

- Tech industry employment creating concentrated income sources

- Condo market complexity with varying HOA financial health and approval status

- Neighborhood appreciation patterns that affect refinancing opportunities

- High home prices pushing many transactions into jumbo loan territory

A mortgage professional deeply embedded in the Seattle market brings this contextual knowledge to every transaction, helping you navigate challenges that out-of-area lenders might not anticipate or understand.

Conventional house loans provide Seattle-area homebuyers with flexible, competitive financing that adapts to diverse financial situations and property types. Understanding qualification requirements, documentation needs, and strategic considerations positions you to secure optimal terms and execute successfully in competitive markets. Whether you're purchasing your first condo in Lake Forest Park or refinancing a Bellevue estate, working with Keith Akada at Mortgage Reel connects you with 25+ years of expertise, proven execution, and specialized knowledge of qualifying tech industry compensation for maximum buying power in the Greater Seattle area.