Thinking of growing your wealth with real estate in 2026? The right financing can be the difference between an average investment and a profitable one. For many, the conventional loan for investment property remains a proven path to building a strong portfolio.

This guide cuts through the confusion surrounding the conventional loan for investment property, so you can make informed, profitable choices. You will discover what these loans are, how to qualify, step-by-step application details, the benefits and drawbacks, 2026 market trends, comparisons with other financing, and expert strategies for investors.

If you want clarity and actionable advice about the conventional loan for investment property, you are in the right place. Let’s unlock your investment potential together.

Understanding Conventional Loans for Investment Properties

Understanding how a conventional loan for investment property works is essential for real estate investors in 2026. With the right financing, you can maximize your returns, scale your portfolio, and manage risks. This section explains what conventional loans are, their defining features, pros and cons, and who should consider them for their next investment.

What is a Conventional Loan?

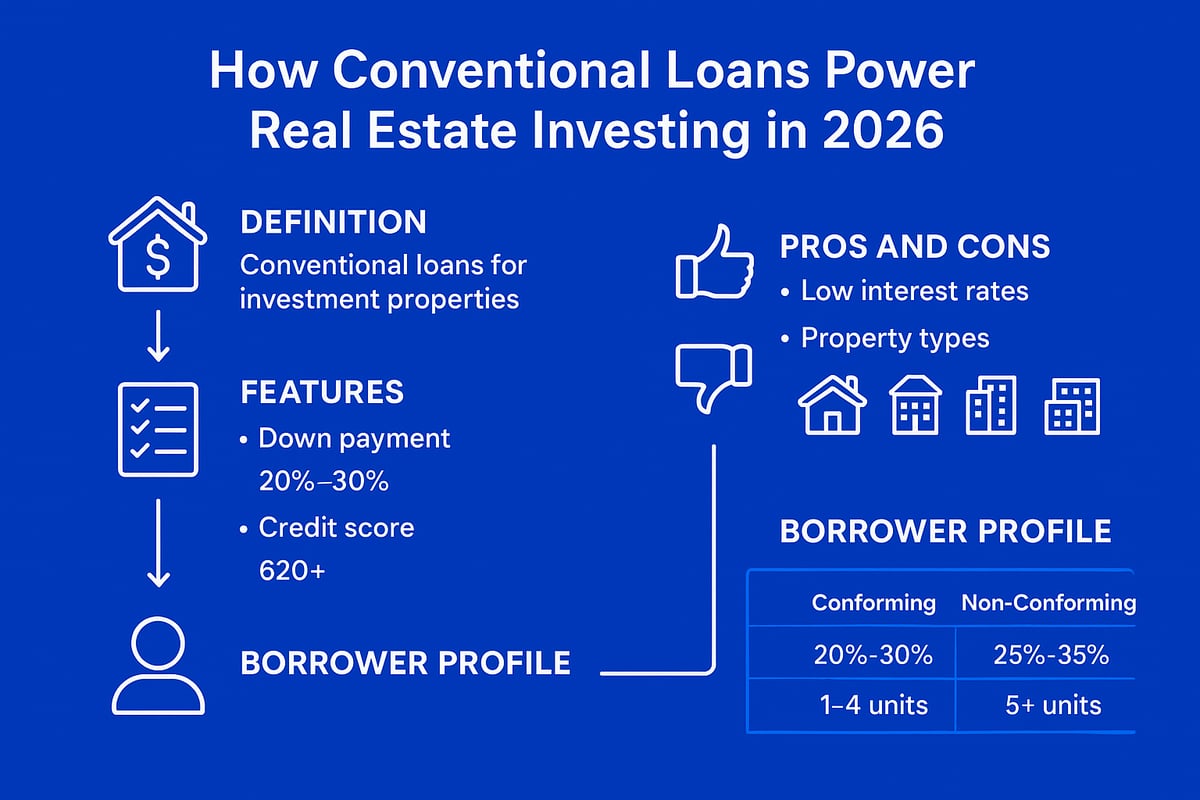

A conventional loan for investment property is a mortgage not backed by government agencies such as FHA, VA, or USDA. Instead, these loans are offered by private lenders and typically follow the conforming loan standards set by Fannie Mae and Freddie Mac. Conforming loans must meet specific criteria, including loan limits and credit requirements, while non-conforming loans do not.

| Loan Type | Backed by Government | Fannie/Freddie Guidelines | Typical Uses |

|---|---|---|---|

| Conforming | No | Yes | Rentals, flips |

| Non-conforming | No | No | Jumbo, unique props |

Investors often use a conventional loan for investment property to finance single-family homes, condos, or small multifamily properties. For 2026, the conforming loan limits have been updated, so check the Conventional home loans overview for current thresholds. Fannie Mae and Freddie Mac guidelines are the industry standard for most investment property loans.

Key Features of Conventional Loans for Investors

A conventional loan for investment property comes with specific requirements tailored for investors. Down payments typically range from 15 to 25 percent, depending on property type and borrower profile. Both fixed and adjustable-rate mortgages are available, allowing you to choose based on your risk tolerance and investment horizon.

- Up to 10 financed properties per borrower

- Private mortgage insurance (PMI) usually required if down payment is less than 20 percent

- Amortization periods of 15, 20, or 30 years

- Higher reserve requirements compared to primary residence loans

These features make a conventional loan for investment property a preferred option for long-term rental strategies. Understanding the rules around PMI and property limits is crucial for effective portfolio growth.

Advantages and Disadvantages

Choosing a conventional loan for investment property offers benefits like lower interest rates compared to hard money or private loans. However, these loans have stricter qualification standards, including higher credit scores and larger down payments. Since they are not government-insured, the risk is higher for lenders, which can affect approval odds.

On the plus side, conventional loans can improve cash flow and ROI due to favorable interest rates. For example, a typical investor might save thousands in interest compared to a DSCR or portfolio loan over a five-year hold. On the downside, strict documentation and underwriting can slow the process for some borrowers.

Who Should Consider a Conventional Loan?

A conventional loan for investment property is ideal for borrowers with strong credit (usually 680 or higher), stable income, and some real estate experience. Eligible properties include single-family homes and 2–4 unit properties, provided they are non-owner occupied.

- Best for buy-and-hold investors seeking rental income or appreciation

- Suitable for those with sufficient cash reserves and verifiable income

- Most common among investors financing their first few properties

Recent data suggests that over 60 percent of investment property buyers use a conventional loan for investment property, making it the most popular choice for building a rental portfolio. If your goals align with long-term growth and stable returns, this loan type is worth considering.

2026 Qualification Requirements for Conventional Investment Property Loans

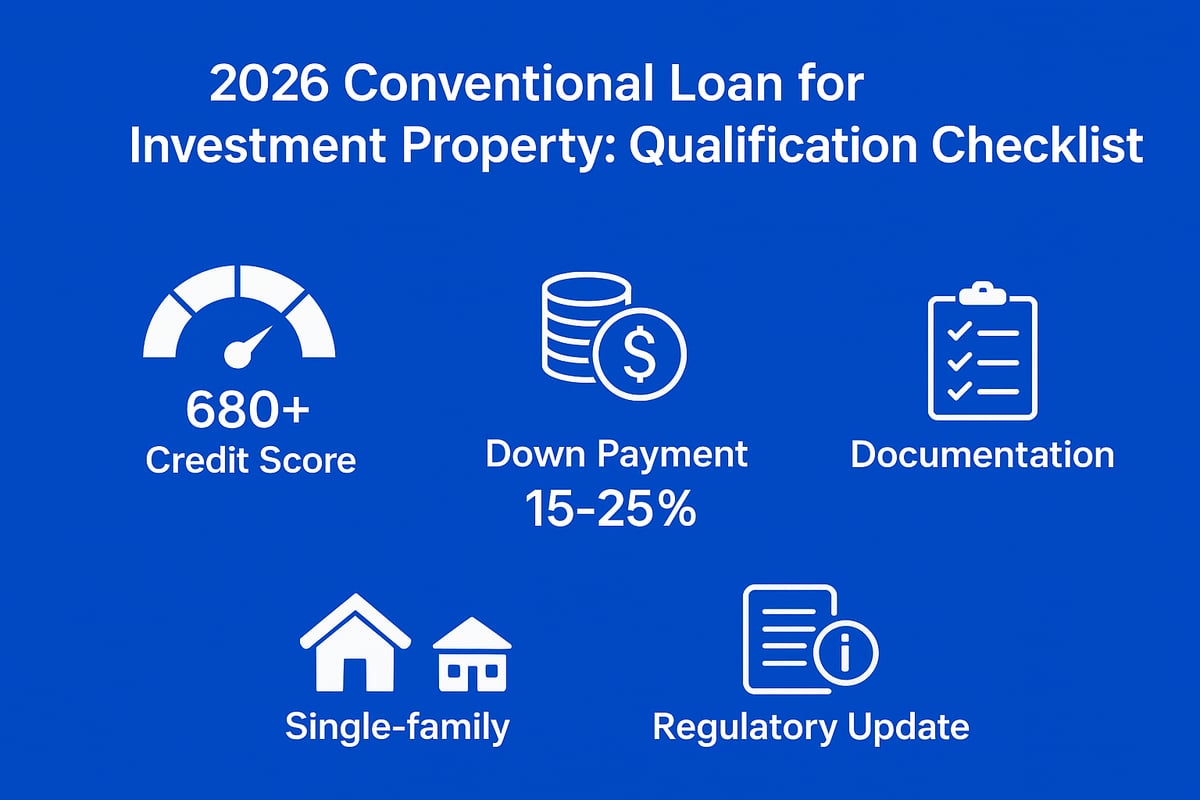

Understanding the 2026 qualification standards for a conventional loan for investment property is essential for investors seeking to maximize approval chances. Lenders have increased their scrutiny, so knowing what to expect around credit, down payments, documentation, and property rules helps you prepare strategically.

Credit Score and Financial Health

Lenders require a strong credit profile for a conventional loan for investment property. Most set a minimum credit score of 680, though higher scores are preferred for better rates and smoother approvals. A score of 740 or above can yield significant interest rate reductions, translating to thousands in savings over the loan’s life.

Debt-to-income (DTI) ratios are also critical, typically capped at 45 percent. Lenders want to see that your total monthly obligations, including the new property, won’t strain your finances. Additionally, expect to show reserves equal to at least two to six months of mortgage payments, depending on your overall risk profile.

Down Payment and Loan-to-Value (LTV)

For a conventional loan for investment property, down payment requirements are steeper than for primary residences. Investors generally need to put down 15 to 25 percent, depending on property type and loan terms. Single-family homes may qualify for the lower end, while multi-unit properties often require more.

Higher down payments improve approval odds and can eliminate the need for private mortgage insurance (PMI). Gift funds may be permitted, but restrictions usually apply. For a detailed look at requirements and scenarios, see 15 percent down conventional loans. For example, on a $400,000 investment, a 20 percent down payment means $80,000 upfront, reducing overall risk and monthly costs.

Income Verification and Documentation

Proving sufficient, stable income is a must for any conventional loan for investment property. Lenders typically require W-2s, recent tax returns, and pay stubs. If you plan to use rental income from the property, you must provide executed leases and sometimes a rental history.

Self-employed borrowers face additional scrutiny, needing two years of tax returns and business financials. A documentation checklist for 2026 may include:

- Two years of tax returns

- Recent pay stubs or business statements

- Lease agreements for rental income

- Bank statements for reserves

Using projected rental income can help boost qualifying power, especially for those scaling their portfolios.

Property Eligibility and Condition

Not all properties are eligible for a conventional loan for investment property. Acceptable options include single-family homes, condos, and 2-4 unit properties, but they must be non-owner occupied. Appraisals are mandatory to confirm value and condition, and properties must meet minimum standards.

Restrictions may apply to short-term rentals, so check lender overlays and local rules. For example, investing in a condo requires reviewing HOA guidelines to ensure the property qualifies. Lenders may reject properties with deferred maintenance or legal/occupancy issues.

Recent Regulatory and Market Changes (2026)

In 2026, updated Fannie Mae and Freddie Mac guidelines have introduced nuanced changes for a conventional loan for investment property. These include revised loan limits, stricter documentation for short-term rentals, and evolving reserve requirements.

Interest rates remain volatile, impacting both affordability and qualification thresholds. Some regions are seeing tighter underwriting due to local market risks or regulatory shifts. According to recent data, approval rates have stabilized, but denials often result from insufficient reserves or property ineligibility. Staying current on these trends positions investors for success in a dynamic market.

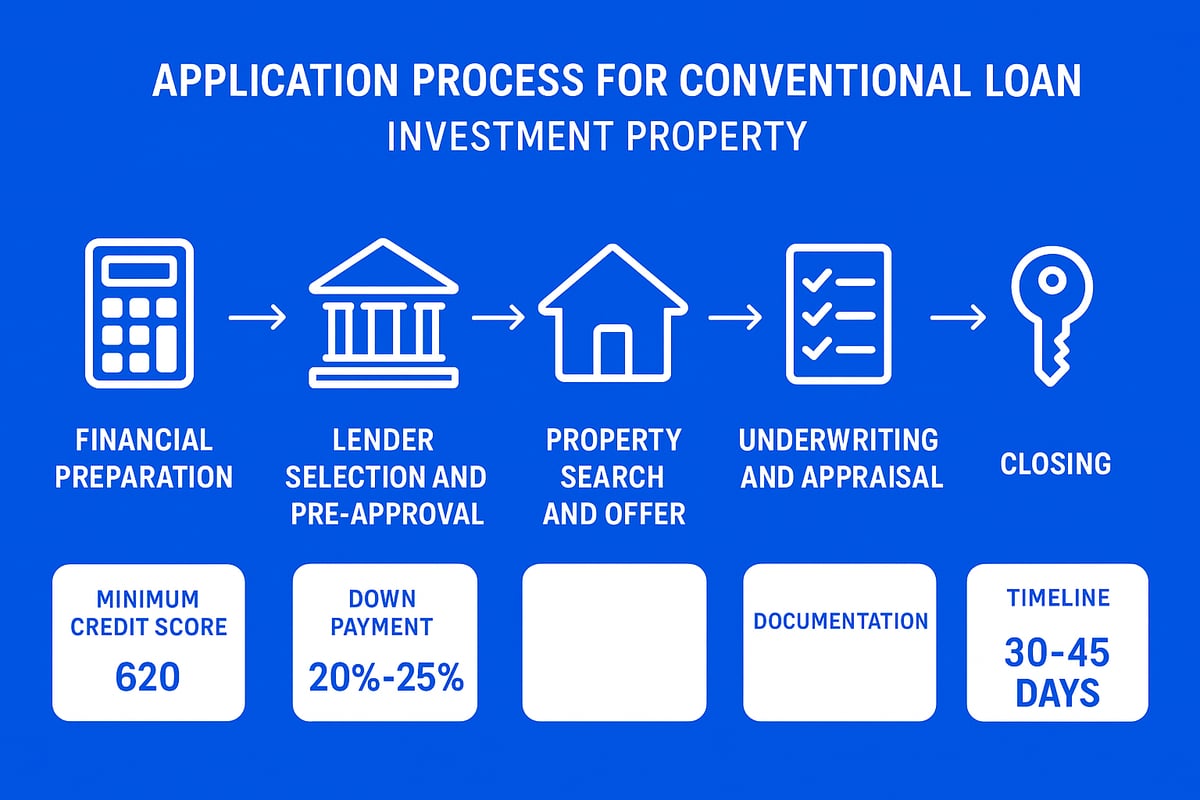

Step-by-Step Application Process for a Conventional Investment Property Loan

Navigating the application process for a conventional loan for investment property requires careful planning, documentation, and strategy. Here is a clear, step-by-step guide to help investors move from preparation to closing with confidence.

Preparing Your Finances

Before you apply for a conventional loan for investment property, assess your financial health. Begin by reviewing your credit report, correcting any errors, and aiming for a score of 680 or higher. Pay down existing debts to improve your debt-to-income ratio, as most lenders prefer it below 45 percent.

Next, assemble the required cash reserves. For most investment properties, you will need at least six months of mortgage payments on hand. Organize your financial documents, including recent tax returns, W-2s, and bank statements. Compare down payment options early, as requirements for a conventional loan for investment property typically range from 15 percent to 25 percent. For a detailed breakdown, see this Conventional loan down payment comparison.

Start this process at least 60 days before you plan to apply. Early preparation increases your approval odds.

Choosing a Lender and Getting Pre-Approved

Research lenders who specialize in the conventional loan for investment property. Compare banks, mortgage brokers, and direct lenders on rates, fees, and their experience with investment properties. Look for investor-friendly features, such as streamlined underwriting or flexible qualification for rental income.

Pre-approval is critical. It demonstrates to sellers that you are a serious buyer and can compete in a fast-moving market. During pre-approval, the lender reviews your credit, income, assets, and the specifics of your intended investment. They will issue a pre-approval letter, which strengthens your purchase offers.

A conventional loan for investment property requires more documentation than a primary residence loan, so have your financial records organized in advance.

Property Search and Offer Process

With pre-approval in hand, work with a real estate agent who understands investment properties. Focus on properties that meet your cash flow and appreciation goals. Analyze potential returns using rent-to-price ratios and projected expenses.

When you find a promising property, make an offer that leverages your pre-approval for a competitive edge. Include financing contingencies to protect your earnest money if the loan falls through. Negotiate for seller concessions, such as closing cost credits, to maximize your investment.

A successful offer on a property suitable for a conventional loan for investment property can set the stage for long-term wealth growth.

Underwriting and Appraisal

Once your offer is accepted, the lender begins underwriting for your conventional loan for investment property. Underwriters review your finances, property details, and rental income potential. They request additional documentation if needed.

The appraisal is a crucial step. It determines the property's value and ensures the loan-to-value ratio meets guidelines. If the appraised value is lower than expected, you may need to renegotiate or provide a larger down payment.

Lenders also evaluate the condition of the property and how rental income will support the loan. Respond promptly to any requests to keep the conventional loan for investment property process on track.

Closing the Loan

After final approval, the lender issues a clear-to-close. Review your closing disclosure and settlement statement carefully to understand all costs. On closing day, funds are transferred, documents are signed, and the mortgage is officially recorded.

Expect the period from offer acceptance to closing to take 30 to 45 days. Once closed, you take ownership and can begin managing your investment. Proper planning ensures a smooth closing for your conventional loan for investment property and positions you for future acquisitions.

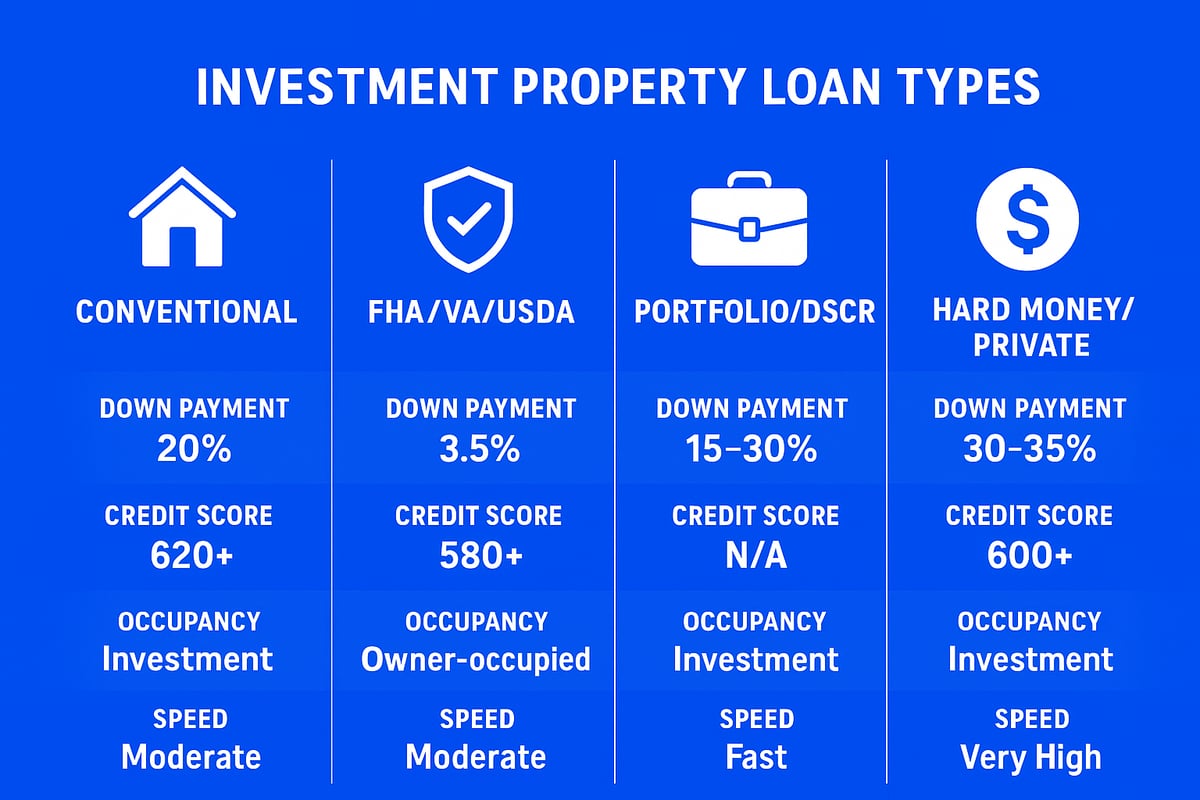

Comparing Conventional Loans to Other Investment Property Financing Options

Choosing the right financing can make or break your investment returns. Understanding how a conventional loan for investment property stacks up against other loan types helps investors select the best fit for their strategies. The table below summarizes key differences:

| Loan Type | Down Payment | Credit Score | Occupancy Requirement | Speed | Flexibility |

|---|---|---|---|---|---|

| Conventional | 15–25% | 680+ | Non-owner occupied | Moderate | Medium |

| FHA/VA/USDA | 3.5–5% | 580+ | Owner occupied | Moderate | Low |

| Portfolio/DSCR | 20–30% | 620+ | Non-owner occupied | Fast | High |

| Hard Money/Private | 20–40% | Flexible | Non-owner occupied | Fastest | Very High |

Conventional vs. FHA/VA/USDA Loans

When considering a conventional loan for investment property, investors quickly see major differences from FHA, VA, or USDA loans. The most important distinction is occupancy: government-backed loans almost always require the property to be owner-occupied, which disqualifies most investment properties.

Conventional loans, by contrast, are designed for non-owner-occupied homes, with down payments typically between 15 and 25 percent. FHA and VA loans offer lower down payments but come with higher mortgage insurance costs and stricter occupancy rules. Credit score requirements are also generally higher for a conventional loan for investment property. For a comprehensive breakdown, see this FHA home loans vs. conventional comparison.

Many investors choose conventional loans for their flexibility, even if the initial investment is larger, because long-term rental income and appreciation are easier to pursue.

Conventional vs. Portfolio and DSCR Loans

A conventional loan for investment property offers lower interest rates and predictable terms, but it comes with stricter underwriting and a cap on the number of properties that can be financed (often 10). Portfolio and DSCR (Debt Service Coverage Ratio) loans are issued by lenders who keep the loans in-house, allowing more flexibility.

These alternatives allow investors to qualify based on property cash flow rather than personal income, making them ideal for those with larger portfolios or complex finances. However, rates are usually higher than a conventional loan for investment property, and down payment requirements may increase.

For investors looking to scale quickly or who may not meet traditional income verification, portfolio or DSCR loans can be a strategic choice, especially for multifamily or mixed-use properties.

Conventional vs. Hard Money and Private Loans

Hard money and private loans are appealing for investors who need speed or have unique situations. Unlike a conventional loan for investment property, these loans can close in days and are based more on asset value than borrower credentials.

However, the trade-off comes in the form of much higher interest rates and shorter loan terms, usually 6–24 months. These loans are best suited for fix-and-flip projects, bridge financing, or situations where traditional approval is unlikely.

In contrast, a conventional loan for investment property is better for long-term buy-and-hold investors aiming for stable cash flow and lower costs over time. Always compare the total costs and exit strategies before choosing hard money over conventional financing.

When to Use Each Loan Type

Selecting the right financing depends on your investment strategy, timeline, and portfolio goals. A conventional loan for investment property is typically best for buy-and-hold investors seeking predictable payments and long-term appreciation.

Portfolio and DSCR loans suit those expanding beyond the conventional loan property cap or needing more flexible qualification. Hard money is ideal for fast acquisitions or properties requiring major rehab.

Many investors use a mix of financing types as their needs evolve. Data shows that the majority of small-scale investors start with a conventional loan for investment property, then diversify as their portfolio grows or as market conditions shift.

Market Trends and Forecasts for Investment Property Financing in 2026

Navigating the 2026 real estate landscape requires a clear understanding of shifting trends. For those using a conventional loan for investment property, staying ahead of market changes can be the difference between a profitable venture and a missed opportunity. Let’s explore what the year ahead might hold for rates, lending standards, regional dynamics, and regulations.

Interest Rate Projections and Their Impact

Interest rates are set to play a major role in the accessibility of a conventional loan for investment property in 2026. Recent forecasts suggest rates may remain elevated compared to pre-2020 levels, although some sources anticipate modest declines if inflation stabilizes. Even a 1% increase on a $500,000 loan can raise monthly payments by over $300, directly impacting investor cash flow.

When planning your financing, be mindful of updated conventional loan limits for 2026, as these thresholds determine maximum loan amounts and eligibility for conforming rates. Many investors are considering locking in fixed rates to hedge against future increases, while others explore adjustable-rate options for short-term holds.

Lending Standards and Investor Demand

Lenders are expected to maintain strict underwriting standards for any conventional loan for investment property. Minimum credit scores will likely stay at 680 or higher, and requirements for reserves and documentation remain robust. Debt-to-income ratios are scrutinized closely, especially as property values fluctuate.

Investor demand continues to be strong, driven by rising rents and limited housing supply. However, lenders may adjust criteria in response to regional economic factors or shifts in rental demand. Keeping an eye on lender appetite and changing guidelines is crucial for securing favorable terms as an investor.

Regional Differences and Hot Markets

Not all markets move in sync, so the outlook for a conventional loan for investment property varies by region. According to 2026 Real Estate Market Trends, cities like Austin, Atlanta, and select Sunbelt metros are projected to see robust rental growth and investor activity.

| Top Markets | Rental Growth | Investor Activity |

|---|---|---|

| Austin | High | Strong |

| Atlanta | High | Strong |

| Seattle | Moderate | Growing |

| Phoenix | High | Strong |

| Nashville | High | Steady |

Local regulations, such as restrictions on short-term rentals, can also influence financing options and returns. Always research both the economic and regulatory environment before choosing your investment location.

Regulatory and Policy Developments

In 2026, policy shifts could affect the availability and terms of a conventional loan for investment property. Fannie Mae and Freddie Mac periodically update guidelines for investor loans, sometimes tightening limits on the number of financed properties or introducing new documentation requirements.

At the state and local level, new laws may impact short-term rental eligibility or impose additional taxes on non-owner-occupied properties. Investors should also monitor potential changes in tax codes that could affect deductions or capital gains strategies. Staying informed about these developments will help you adapt your approach and protect your investment returns.

Strategic Tips for Success with Conventional Investment Property Loans

Achieving success with a conventional loan for investment property in 2026 requires more than just meeting lender criteria. Strategic planning, careful financial management, and understanding the nuances of these loans can help you maximize your approval odds, optimize returns, and grow your portfolio efficiently.

Maximizing Approval Odds

To improve your chances of securing a conventional loan for investment property, focus on your financial profile well before applying. Start by checking your credit score and addressing any errors. Aim for a score above 700, as this can unlock better rates and smoother approval.

Build strong cash reserves, ideally covering six months of mortgage payments for each property. Lenders also examine your debt-to-income ratio, so pay down existing debts and avoid taking on new obligations during the application process.

Prepare comprehensive documentation, including proof of income, tax returns, and evidence of rental income if applicable. A real investor improved approval odds by consolidating debts and presenting organized records, resulting in a fast, favorable loan decision.

Optimizing Cash Flow and ROI

Selecting the right property is crucial for maximizing cash flow with a conventional loan for investment property. Focus on homes or multifamily units with strong rent-to-price ratios, ensuring rental income comfortably covers mortgage payments and expenses.

Factor in all costs, such as private mortgage insurance, closing fees, and required reserves. Use amortization schedules to project long-term profits and monitor how loan terms impact your returns.

For example, compare a duplex and a single-family home side by side. The duplex may yield higher cash flow due to multiple rental streams, making it a smarter investment under the conventional loan for investment property structure.

Scaling Your Portfolio with Conventional Loans

Expanding your holdings with a conventional loan for investment property comes with unique challenges. Lenders often cap the number of financed properties at ten, so planning is essential.

Leverage equity from existing properties to fund new purchases, and consider forming partnerships or using LLCs to increase eligibility. Multifamily investments are particularly effective for scaling, as they offer multiple units in a single transaction.

For more on growth strategies and 2026 trends, explore Multifamily Investment Strategies 2026. Many successful investors have grown from one to ten properties by strategically refinancing and reinvesting profits from each acquisition.

Exit Strategies and Long-Term Planning

Long-term success with a conventional loan for investment property depends on thoughtful exit planning. Refinancing can help you secure better rates or extract equity as your portfolio appreciates.

Consider a 1031 exchange to defer capital gains taxes when selling one property to purchase another, preserving more capital for reinvestment. Plan ahead for property disposition, whether you intend to pass assets to heirs or liquidate for retirement.

A common strategy is to refinance out of a conventional loan for investment property after increasing equity, freeing up resources to pursue additional opportunities and sustain portfolio growth.

Now that you’ve explored the ins and outs of conventional loans for investment properties in 2026 and seen how strategic financing can elevate your real estate journey, you might have questions specific to your own goals or market circumstances. Whether you’re weighing your next move or want to clarify how these lending trends apply to your plans, I’m here to help you chart the right path. Let’s connect and discuss your investment strategy in detail—together, we can create a plan that empowers your success. Let’s have a conversation