For most homebuyers in Seattle and across the Greater Seattle area, conventional loans represent the most common path to homeownership. Unlike government-backed mortgages, these loans follow standards set by Fannie Mae and Freddie Mac, offering flexibility and competitive rates for borrowers with solid credit and stable income. Understanding how these mortgages work, what they require, and when they make sense can help you make confident decisions in competitive markets like Bellevue, Redmond, and Kirkland. With home prices ranging from entry-level condos in Lynnwood to luxury properties in Seattle's most desirable neighborhoods, knowing your financing options is essential.

What Defines a Conventional Loan

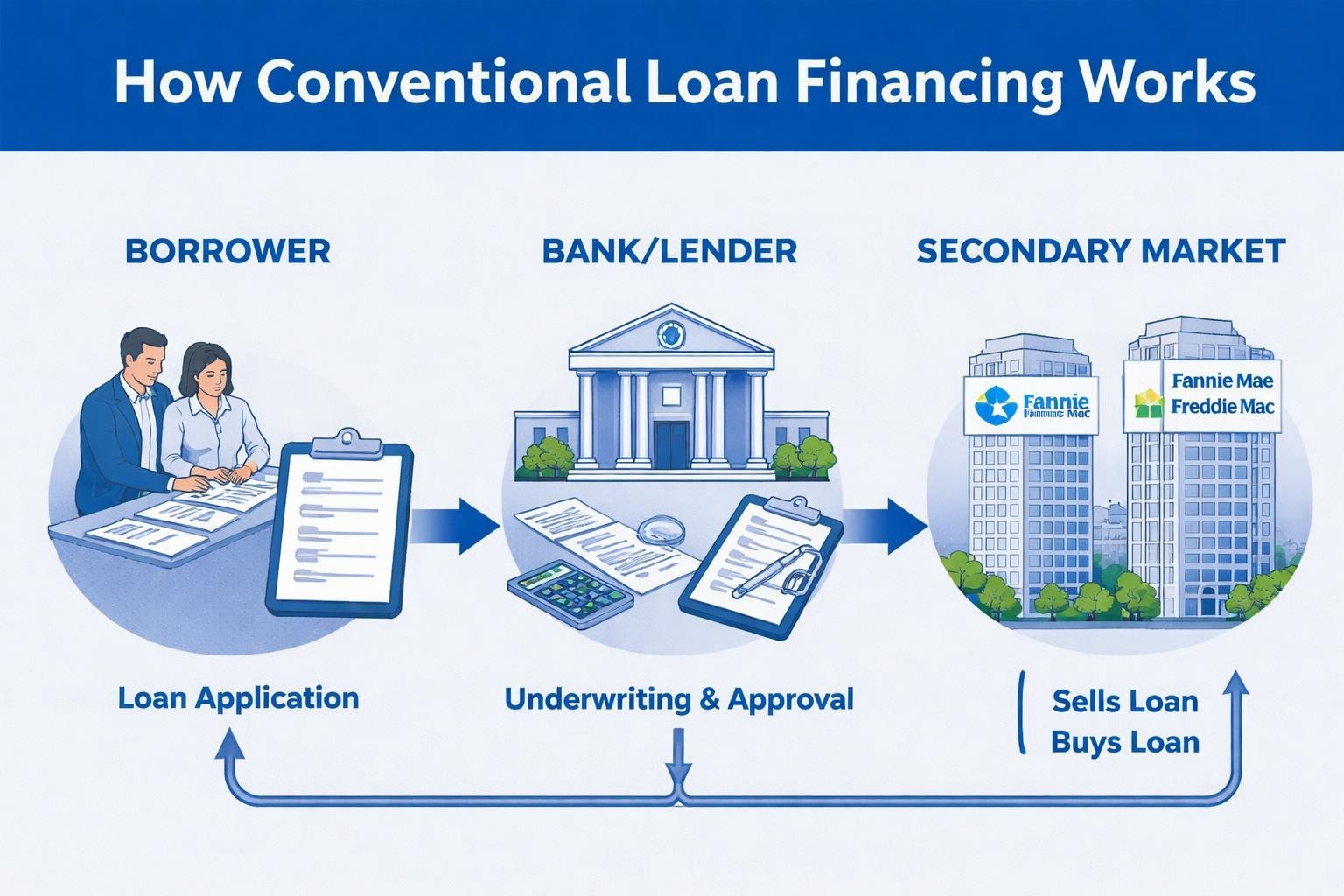

A conventional loan is any mortgage not insured or guaranteed by a federal government agency. The Consumer Financial Protection Bureau provides comprehensive guidance on how these mortgages differ from FHA, VA, and USDA loans. Instead of government backing, these loans are funded by private lenders and typically sold to Fannie Mae or Freddie Mac in the secondary market.

Two primary categories exist:

- Conforming conventional loans meet the loan limit guidelines set annually by the Federal Housing Finance Agency

- Non-conforming conventional loans (jumbo loans) exceed these limits and carry different requirements

In 2026, the conforming loan limit for King County stands at $806,500 for single-family homes, reflecting the high-cost area designation. Properties in Seattle, Shoreline, and surrounding cities frequently exceed this threshold, requiring jumbo financing.

Conforming vs. Non-Conforming Structures

The distinction between conforming and non-conforming loans impacts your rate, requirements, and approval process. Conforming loans benefit from standardized underwriting guidelines, making them easier to qualify for and generally offering lower interest rates. Non-conforming jumbo loans require stronger financial profiles but provide financing for Seattle's premium properties.

| Loan Type | 2026 King County Limit | Typical Down Payment | Credit Score Minimum |

|---|---|---|---|

| Conforming | Up to $806,500 | 3-20% | 620-640 |

| Jumbo | Above $806,500 | 10-20% | 680-700 |

| High-Balance Conforming | $806,500 (max) | 5-20% | 640-660 |

For tech professionals in Mill Creek or Everett considering move-up properties, understanding these thresholds helps you plan your financing strategy months before making an offer.

Credit and Income Requirements

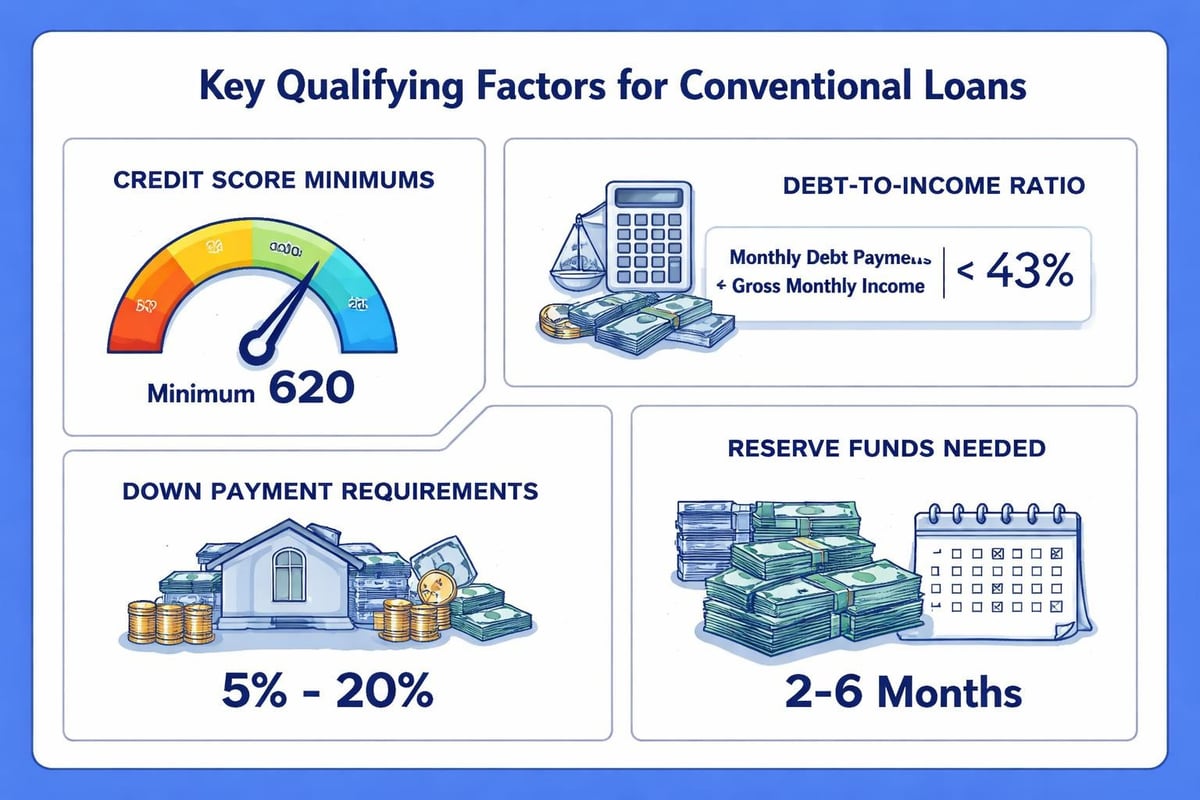

Conventional loans demand stronger credit profiles than government-backed options. Most lenders require a minimum FICO score of 620, though securing the best rates typically requires scores above 740. Your credit history receives thorough examination, with recent delinquencies, collections, or charge-offs creating potential obstacles.

Income documentation standards include:

- Two years of W-2s and recent pay stubs for employed borrowers

- Two years of personal and business tax returns for self-employed applicants

- Detailed documentation for stock compensation, bonuses, and RSU income

- Consistent employment history with minimal unexplained gaps

For Amazon, Microsoft, and Google employees across the Seattle area, qualifying stock-based compensation requires specific calculation methods. RSUs typically count once vested, with underwriters examining historical vesting schedules and future grant timelines. This specialized knowledge becomes critical when maximizing your purchasing power in competitive neighborhoods from Lake Forest Park to downtown Seattle.

Debt-to-Income Ratio Standards

Your debt-to-income (DTI) ratio measures monthly debt obligations against gross income. Conventional loans typically allow maximum DTI ratios of 43-50%, depending on compensating factors. Strong credit scores, substantial reserves, or larger down payments can justify higher ratios.

Monthly debts included in calculations:

- Proposed mortgage payment (principal, interest, taxes, insurance, HOA)

- Student loan payments

- Auto loans and leases

- Credit card minimum payments

- Personal loans and other installment debt

- Child support or alimony obligations

A software engineer in Redmond earning $180,000 annually with a $3,200 car payment, $800 in student loans, and $400 in credit card minimums would have approximately $4,400 in existing debt. With a proposed $4,500 mortgage payment, the total debt of $8,900 against gross monthly income of $15,000 yields a 59% DTI-likely requiring compensating factors or debt paydown before approval.

Down Payment Options and PMI

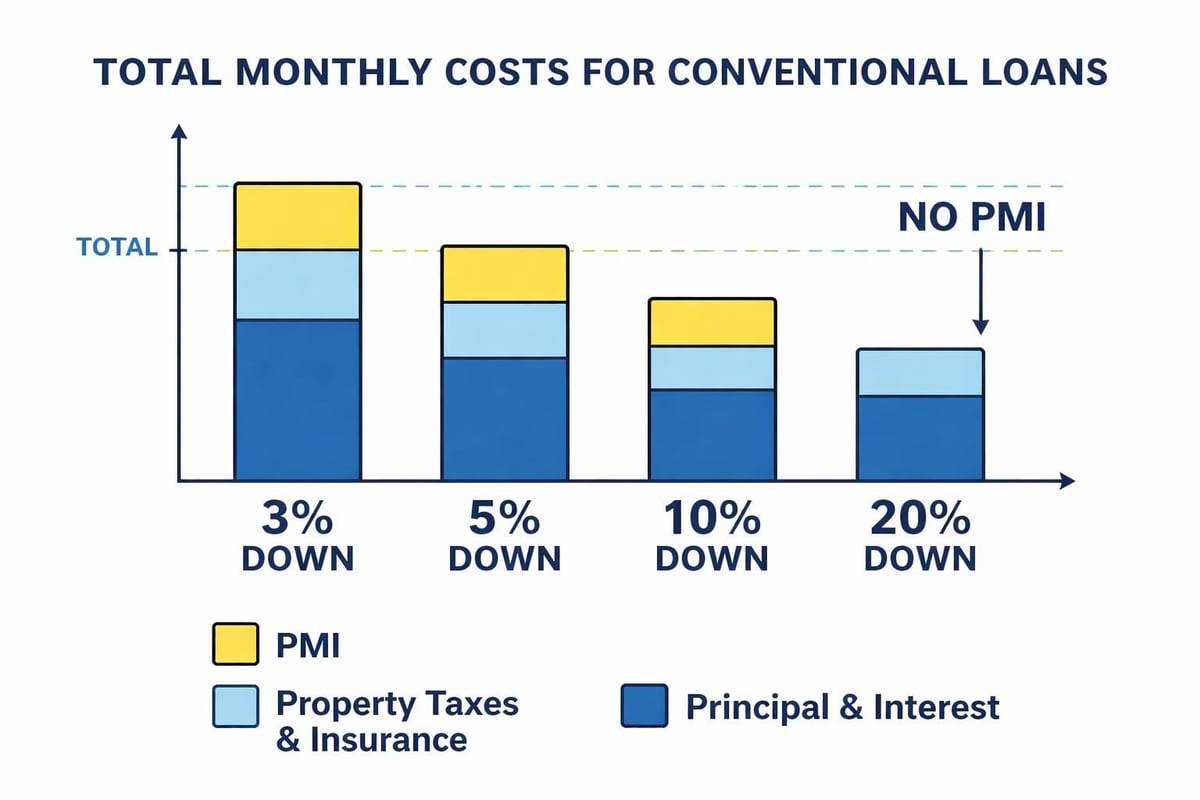

One significant advantage of conventional financing involves flexible down payment options. While the traditional 20% down payment eliminates private mortgage insurance (PMI), programs exist allowing as little as 3% down for qualified first-time buyers.

Common down payment scenarios:

- 3% down: Available through Fannie Mae HomeReady and Freddie Mac Home Possible programs for income-qualified buyers

- 5% down: Standard conventional option for most borrowers with good credit

- 10% down: Common for investment properties or when minimizing PMI costs

- 20% or more: Eliminates PMI and often secures better rates

PMI protects the lender if you default, typically costing 0.3% to 1.5% of the original loan amount annually. On a $700,000 loan with 10% down, monthly PMI might range from $175 to $788 depending on your credit score and specific loan terms.

Strategies for PMI Removal

Unlike FHA loans with permanent mortgage insurance premiums, conventional PMI can be removed once you reach 20% equity. Understanding mortgage insurance requirements helps you plan for eventual removal and long-term savings.

Three paths to PMI elimination:

- Automatic termination at 78% loan-to-value based on original property value and amortization schedule

- Borrower-requested cancellation at 80% LTV with documented on-time payment history

- New appraisal demonstrating 20% equity through appreciation and principal reduction

In Seattle's appreciating market, homeowners in Shoreline or Lynnwood who purchased two to three years ago with 10% down may already qualify for PMI removal through a new appraisal. This single action can reduce monthly payments by several hundred dollars without refinancing.

Property Type Flexibility

Conventional loans accommodate diverse property types that government programs often restrict or exclude. This flexibility matters significantly in Seattle's varied housing stock, from historic Capitol Hill condos to new construction townhomes in Lake Forest Park.

Eligible property types include:

- Single-family residences

- Condominiums (with approved projects)

- Townhomes and row houses

- Multi-unit properties (2-4 units) as primary residences

- Investment properties and second homes

- Manufactured homes on permanent foundations

For real estate investors in Mill Creek or Everett, conventional financing permits purchasing rental properties with 15-25% down, creating portfolio growth opportunities unavailable through government programs. Multi-unit properties allow owner-occupants to offset mortgage costs with rental income, though lenders apply vacancy factors to rental income calculations.

Condominium Approval Requirements

Condo financing requires project-level approval beyond individual borrower qualification. The condo association must meet specific financial and operational standards, including adequate reserve funds, low delinquency rates, and appropriate insurance coverage.

| Requirement | Fannie Mae Standard | Common Issue |

|---|---|---|

| Owner Occupancy | Minimum 50% | New developments struggle initially |

| Single Entity Ownership | Maximum 10% | Investors concentrate holdings |

| Commercial Space | Maximum 35% | Mixed-use buildings exceed limits |

| Reserve Fund | 10% of annual budget | Older buildings underfunded |

Seattle's diverse condo inventory includes many buildings built before current standards. A seemingly perfect unit in a well-maintained building might require non-warrantable financing if the project fails approval, resulting in higher rates or larger down payments.

Interest Rates and Terms

Conventional loan interest rates fluctuate based on broader economic conditions, your credit profile, down payment, and loan term. In 2026, rates for well-qualified borrowers remain competitive with historical averages, though individual pricing varies significantly.

Factors influencing your rate:

- Credit score (higher scores receive better pricing)

- Loan-to-value ratio (more equity means lower rates)

- Debt-to-income ratio (lower DTI improves pricing)

- Property type (single-family homes rate better than condos)

- Occupancy status (primary residences beat investment properties)

- Loan amount (very small or jumbo loans may carry adjustments)

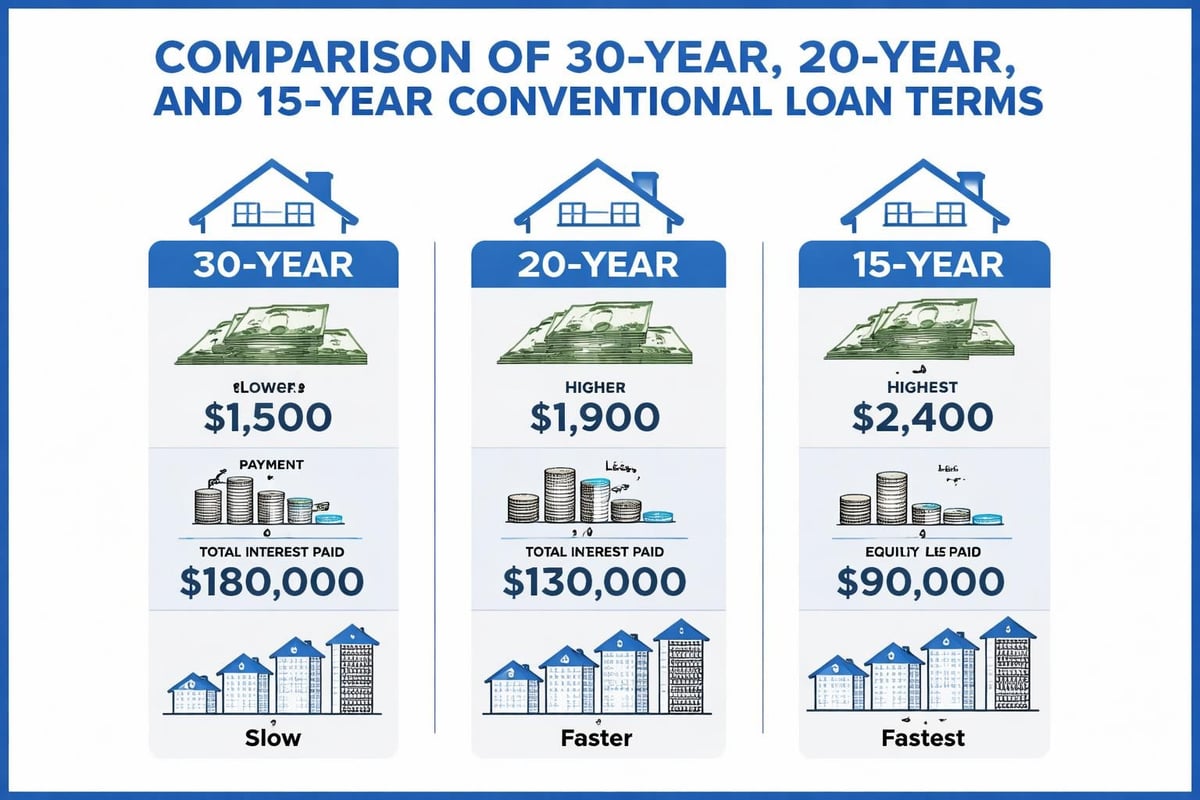

A borrower in Bellevue with a 780 credit score, 25% down payment, and 35% DTI might receive a rate 0.75% to 1.25% lower than someone with a 660 score, 5% down, and 48% DTI purchasing a comparable property. Over 30 years, this difference represents tens of thousands in interest costs.

Fixed-Rate vs. Adjustable-Rate Options

Most borrowers select fixed-rate mortgages for payment stability, but adjustable-rate mortgages (ARMs) offer lower initial rates for those with shorter ownership timelines or income growth expectations.

Common ARM structures:

- 5/1 ARM: Fixed for 5 years, then adjusts annually

- 7/1 ARM: Fixed for 7 years, then adjusts annually

- 10/1 ARM: Fixed for 10 years, then adjusts annually

Tech professionals in Kirkland expecting RSU vesting acceleration or promotion-driven income growth might benefit from ARM structures, accepting eventual rate adjustments in exchange for lower initial payments. However, rate caps, margin calculations, and index selection require careful analysis to avoid payment shock.

Reserve Requirements and Asset Verification

Beyond down payment and closing costs, conventional loans often require documented reserves-liquid assets remaining after closing. Reserve requirements increase with loan amount, property type, and risk factors.

Typical reserve standards:

- Primary residence, conforming: 0-6 months of PITI (principal, interest, taxes, insurance)

- Primary residence, jumbo: 6-12 months of PITI

- Second home: 2-6 months of PITI

- Investment property: 6-12 months of PITI

- Multiple financed properties: Additional 2-6 months per property

For a $5,000 monthly PITI, six months of reserves equals $30,000 in verified liquid assets. Acceptable reserves include checking accounts, savings accounts, money market funds, stocks, bonds, and vested retirement accounts (with potential discounts for early withdrawal penalties).

Stock Compensation as Reserves

Seattle-area tech employees can often count vested stock holdings as reserves. Underwriters typically apply a 30% discount to stock values, accounting for potential market volatility and liquidation costs. Recently vested RSUs scheduled for vesting within 30 days may also count, subject to documentation and lender guidelines.

A Microsoft employee in Redmond with $100,000 in vested stock held in a brokerage account would receive approximately $70,000 in reserve credit. Combined with $20,000 in savings, this satisfies even demanding jumbo loan reserve requirements while maintaining investment positions.

Documentation and Underwriting Process

Conventional loan underwriting follows standardized automated systems combined with manual review. Understanding required documentation and timeline expectations helps you prepare effectively and avoid delays in competitive markets.

Core documentation package:

- Government-issued photo identification

- Two years of W-2s and 1040 tax returns

- Recent pay stubs (typically 30 days)

- Two months of bank statements for all accounts

- Purchase agreement and property details

- Homeowners insurance quote

- HOA documents (if applicable)

Self-employed borrowers in Lake Forest Park or Everett face additional scrutiny, with underwriters examining profit and loss statements, business bank accounts, and Schedule C details. Recent business startups or significant income fluctuations complicate qualification, sometimes requiring larger down payments or additional documentation.

Automated Underwriting Systems

Fannie Mae’s Desktop Underwriter and Freddie Mac’s Loan Product Advisor analyze your application against thousands of data points, generating approval recommendations. These systems evaluate credit, income, assets, and property details simultaneously, often providing initial decisions within minutes.

Possible automated findings:

- Approve/Eligible: Application meets guidelines with specified conditions

- Refer: Manual underwriting required for final determination

- Out of Scope: Application falls outside automated parameters

- Ineligible: Application fails to meet minimum standards

Even "approve" findings require documentation verification and property appraisal before final clear-to-close. Conditional approvals might request explanation letters for recent deposits, credit inquiries, or employment changes. Responding promptly to underwriter conditions keeps your transaction moving toward scheduled closing.

Closing Costs and Financial Planning

Beyond down payment and reserves, closing costs typically range from 2% to 5% of the purchase price on conventional loans. These expenses cover lender fees, third-party services, prepaid items, and various administrative costs.

Typical closing cost components:

- Loan origination or processing fees

- Appraisal ($600-$1,000 in Seattle area)

- Credit report ($50-$100)

- Title insurance and escrow fees

- Recording fees and transfer taxes

- Prepaid property taxes

- Homeowners insurance premium

- Initial escrow deposit (taxes and insurance)

On a $750,000 purchase in Shoreline with 10% down, expect closing costs between $15,000 and $37,500. Washington's lack of state income tax is offset partially by recording fees and local transfer taxes that vary by jurisdiction.

Seller Concessions and Credits

Conventional loans permit sellers to contribute toward buyer closing costs, though limits apply based on down payment percentage. These concessions can significantly reduce cash needed at closing, particularly beneficial for first-time buyers preserving emergency reserves.

| Down Payment | Maximum Seller Concession |

|---|---|

| Less than 10% | 3% of purchase price |

| 10-24% | 6% of purchase price |

| 25% or more | 9% of purchase price |

In competitive Seattle markets, requesting seller concessions might weaken your offer against all-cash or cleaner financed offers. However, in balanced markets or with motivated sellers, negotiating 2-3% toward closing costs provides immediate savings without increasing your loan amount.

When Conventional Loans Make the Most Sense

While conventional financing suits many borrowers, certain scenarios particularly favor this mortgage type over government alternatives. Evaluating your specific situation against program strengths helps optimize your financing strategy.

Ideal conventional loan scenarios:

- Credit scores above 680 with clean payment history

- Down payment of 10% or more available

- Property price exceeding FHA loan limits ($498,257 in King County for 2026)

- Purchase of condominiums, investment properties, or second homes

- Desire to eliminate mortgage insurance once reaching 20% equity

- Strong income documentation including stock compensation

For Amazon or Google employees in Redmond or Kirkland with substantial stock holdings, strong credit, and property targets above government loan limits, conventional jumbo financing often provides the only practical path. The ability to qualify non-traditional income sources maximizes purchasing power unavailable through government programs.

Comparing Conventional to Government Alternatives

Understanding how conventional loans stack up against FHA, VA, and USDA options clarifies when to choose each program type. No single mortgage product fits every borrower, making program knowledge essential for informed decisions.

Quick comparison framework:

- Choose FHA when: Credit scores fall between 580-680, down payment is 3.5%, or recent credit events occurred

- Choose VA when: Eligible for veteran benefits with zero down payment preference

- Choose USDA when: Purchasing in eligible rural areas with zero down and moderate income

- Choose conventional when: Credit exceeds 680, down payment is 5%+, or property type/price exceeds government limits

A first-time buyer in Everett with a 650 credit score and 5% saved might benefit from FHA financing despite higher mortgage insurance costs, while a move-up buyer in Mill Creek with 20% down and 760 credit score clearly benefits from conventional options.

Special Considerations for Seattle Area Buyers

The Greater Seattle housing market presents unique challenges and opportunities that impact conventional loan strategies. High property values, competitive conditions, and local employment patterns require tailored approaches.

Seattle-specific factors:

- Premium property prices require larger down payments in absolute dollars

- Tech industry concentration creates stock compensation qualification opportunities

- Rapid appreciation may allow faster PMI removal than national averages

- Condo inventory requires careful project approval verification

- Remote work trends may shift buying patterns toward surrounding cities

A $900,000 home in Seattle requires $90,000 down at 10% compared to $45,000 for a similar-quality $450,000 home in other markets. While the percentage matches, the absolute dollar requirement challenges even high-earning tech professionals early in their careers, making down payment assistance programs and gift funds particularly valuable.

Leveraging Stock Compensation Effectively

Tech employees throughout Bellevue, Redmond, and Seattle possess significant wealth in equity compensation that traditional mortgage underwriting historically struggled to recognize. Understanding how underwriters evaluate RSUs, stock options, and ESPP shares unlocks purchasing power.

Stock compensation qualification methods:

- Use two-year average of vested RSU value for income calculation

- Include documented future vesting schedules with employer verification

- Count exercised stock options as income in exercise year

- Apply after-tax values accounting for ordinary income treatment

- Exclude underwater options or unvested grants without clear vesting path

A Microsoft employee with $85,000 base salary plus $60,000 annual RSU vesting can qualify based on $145,000 income rather than just base salary. This difference might increase buying power by $150,000 to $200,000, accessing better neighborhoods or larger homes than salary-only qualification permits.

Conventional loans offer flexibility, competitive pricing, and property type options that make them the preferred choice for most Seattle-area homebuyers with solid credit and stable income. Understanding qualification requirements, cost structures, and strategic considerations positions you to make confident decisions whether purchasing your first condo in Lynnwood or upgrading to a luxury home in Bellevue. Keith Akada and the team at Mortgage Reel bring 25+ years of experience helping Seattle homebuyers navigate conventional loan options, with specialized expertise qualifying stock compensation for tech professionals throughout the region. Reach out today to discuss your specific situation and explore how conventional financing can help you achieve your homeownership goals.