Understanding your down payment options is one of the most critical steps in the homebuying journey, particularly in competitive markets like Seattle, Bellevue, and the surrounding Puget Sound region. Whether you're a first-time buyer in Shoreline, a tech professional purchasing in Redmond, or a family upgrading in Lynnwood, the amount you put down upfront directly impacts your loan terms, monthly payment, interest rate, and overall purchasing power. Many buyers believe they need 20% down to qualify for a mortgage, but that's not always the case. The reality is far more flexible, with numerous programs designed to help buyers enter homeownership with significantly less cash upfront.

How Much Down Payment Do You Actually Need?

The minimum down payment required depends entirely on your loan type, credit profile, and financial situation. Conventional loans backed by Fannie Mae and Freddie Mac allow qualified buyers to put down as little as 3% on primary residences. FHA loans, popular among first-time buyers throughout Seattle and Mill Creek, require just 3.5% down with credit scores as low as 580. VA loans for eligible military members and veterans require zero down payment, making them exceptionally powerful for qualified buyers in Everett and Lake Forest Park.

Understanding minimum down payment requirements for different mortgage types helps you align your savings goals with realistic homeownership timelines. USDA loans also offer zero-down financing for eligible rural and suburban properties, though availability in King and Snohomish Counties is limited compared to more rural Washington areas.

Conventional Loan Down Payment Options

Conventional financing offers the most flexibility for buyers with strong credit and stable income. Here's how the down payment tiers work:

- 3% down: Available for first-time buyers and qualified repeat buyers on primary residences

- 5% down: Standard option for most conventional borrowers with good credit

- 10% down: Often unlocks better pricing and rate adjustments

- 15% down: Further reduces mortgage insurance costs

- 20% down: Eliminates private mortgage insurance entirely

The amount you choose affects more than just your upfront costs. It influences your interest rate, monthly payment, and whether you'll need to pay for private mortgage insurance. For Seattle-area buyers purchasing homes at or above the conforming loan limit ($806,500 in 2026 for most of King County), a larger down payment may be strategically important to avoid jumbo loan territory or secure better terms.

Down Payment Impact on Your Monthly Payment

The relationship between your down payment and monthly housing costs is straightforward: more money down means a smaller loan amount, which translates to lower monthly principal and interest payments. But there's another significant factor at play-private mortgage insurance, or PMI.

When you put down less than 20% on a conventional loan, lenders require PMI to protect against default risk. This insurance typically costs between 0.3% and 1.5% of the original loan amount annually, divided into monthly payments. On a $600,000 home in Bellevue with 5% down ($30,000), you'd finance $570,000. At 0.5% PMI, that's approximately $237 per month in mortgage insurance alone.

| Down Payment | Loan Amount | PMI (Monthly) | P&I Payment* | Total Monthly** |

|---|---|---|---|---|

| 3% ($18,000) | $582,000 | $340 | $3,458 | $3,798 |

| 5% ($30,000) | $570,000 | $237 | $3,388 | $3,625 |

| 10% ($60,000) | $540,000 | $180 | $3,210 | $3,390 |

| 20% ($120,000) | $480,000 | $0 | $2,853 | $2,853 |

*Based on 6.5% interest rate, 30-year fixed

**Excludes property taxes and homeowners insurance

The difference between 5% and 20% down on this example is $772 per month. Over a year, that's $9,264 in additional housing costs-but it also means you kept $90,000 in savings or invested it elsewhere. The optimal strategy depends on your complete financial picture, investment opportunities, and comfort with monthly cash flow.

FHA Loans and Down Payment Flexibility

Federal Housing Administration loans remain exceptionally popular in Seattle's competitive market, particularly among first-time buyers and those with credit scores below 700. The minimum down payment is 3.5% with a credit score of 580 or higher. Borrowers with scores between 500-579 face a 10% minimum requirement.

FHA loans carry both upfront and annual mortgage insurance premiums regardless of your down payment size. The upfront premium is 1.75% of the loan amount, typically financed into the mortgage. Annual premiums range from 0.45% to 1.05% depending on loan amount, loan-to-value ratio, and term.

Key Advantages of FHA Financing

Lower credit score requirements make homeownership accessible to buyers rebuilding credit or establishing financial history. Seller concessions up to 6% of the purchase price can cover closing costs, reducing your total cash needed at closing. Gift funds fully allowed from family members provide flexibility for buyers whose savings fall short of the required amount.

For buyers in Shoreline or Lynnwood purchasing homes under $500,000, FHA loans can provide a reliable pathway to homeownership when conventional options feel out of reach. The trade-off is higher ongoing mortgage insurance costs compared to conventional loans.

VA Loans: Zero Down Payment for Eligible Veterans

Veterans, active-duty service members, and eligible surviving spouses have access to one of the most powerful mortgage products available: VA loans with zero down payment required. This benefit eliminates the largest barrier to homeownership for many military families throughout the Puget Sound region.

Beyond the zero-down advantage, VA loans don't require monthly mortgage insurance, even with 100% financing. This creates substantial monthly savings compared to conventional and FHA options. VA loans also typically offer competitive interest rates and allow sellers to pay all buyer closing costs and prepaid items.

The VA funding fee, which ranges from 1.4% to 3.6% depending on down payment and whether it's your first VA loan use, is the primary cost. First-time VA borrowers with zero down pay a 2.3% funding fee, which can be financed into the loan amount. Disabled veterans are exempt from this fee entirely.

Strategic Down Payment Considerations for Seattle Buyers

Market conditions in Seattle, Bellevue, and Redmond remain highly competitive in 2026, with inventory constraints continuing to put upward pressure on prices. Determining the appropriate down payment amount requires balancing multiple priorities: winning competitive offers, preserving emergency reserves, maintaining investment portfolios, and managing monthly cash flow.

Larger down payments strengthen offers in competitive situations by reducing financing contingency risk and demonstrating financial capacity. Sellers often favor buyers putting 20% or more down, particularly on properties receiving multiple offers. However, depleting all savings to maximize your down payment can leave you financially vulnerable after closing.

Emergency reserves matter more than many buyers realize. Homeownership brings unexpected expenses-roof repairs, HVAC failures, foundation issues-that rentals don't. Maintaining 6-12 months of expenses in accessible savings provides crucial financial stability during your first years of ownership.

Opportunity costs deserve consideration when deciding how much to put down. Tech professionals throughout Seattle earning RSU compensation and stock options may find higher returns investing excess cash in diversified portfolios rather than sinking everything into home equity. The historically low interest rates of recent years made this calculation particularly compelling, though rising rates in 2025-2026 shift the equation somewhat.

Down Payment Assistance Programs in Washington State

First-time buyers in Seattle, Mill Creek, and Lake Forest Park have access to several down payment assistance programs that can bridge the gap between savings and homeownership. The Washington State Housing Finance Commission offers the Home Advantage program, providing down payment and closing cost assistance with income and purchase price limits.

King County and Snohomish County both maintain local programs for qualified buyers. These typically involve second mortgages or forgivable loans that cover a portion of your down payment, often 3-5% of the purchase price. Requirements vary but generally include:

- First-time homebuyer status (no ownership in past 3 years)

- Income limits based on area median income

- Purchase price caps aligned with conforming loan limits

- Homebuyer education course completion

- Primary residence requirement with occupancy commitments

Combining these programs with low-down-payment conventional or FHA financing can make homeownership accessible with minimal personal savings. However, assistance programs often come with restrictions, secondary liens, and repayment obligations if you sell or refinance within specified timeframes.

Jumbo Loans and Higher Down Payment Requirements

Seattle's median home prices frequently exceed conforming loan limits, particularly in desirable neighborhoods throughout Bellevue, Kirkland, and Redmond. Jumbo loans-those exceeding $806,500 in most of King County-typically require larger down payments, usually 10-20% minimum depending on the lender and loan size.

For loan amounts between $806,500 and $1.5 million, most lenders accept 10-15% down with excellent credit (720+) and strong reserves. Loans above $1.5 million generally require 20-25% down, with requirements becoming more stringent as loan amounts increase. Tech professionals purchasing higher-priced properties can often qualify using RSU income and stock compensation, but documentation requirements are thorough.

| Loan Amount | Minimum Down | Typical Credit | Reserve Requirements |

|---|---|---|---|

| $806,500-$1M | 10% | 720+ | 6-12 months |

| $1M-$1.5M | 15% | 740+ | 9-12 months |

| $1.5M-$2M | 20% | 760+ | 12-18 months |

| $2M+ | 25%+ | 780+ | 18-24 months |

Reserve requirements represent months of housing payments (principal, interest, taxes, insurance, HOA) you must have in savings after closing. These ensure you can weather financial disruptions without defaulting on a substantial loan.

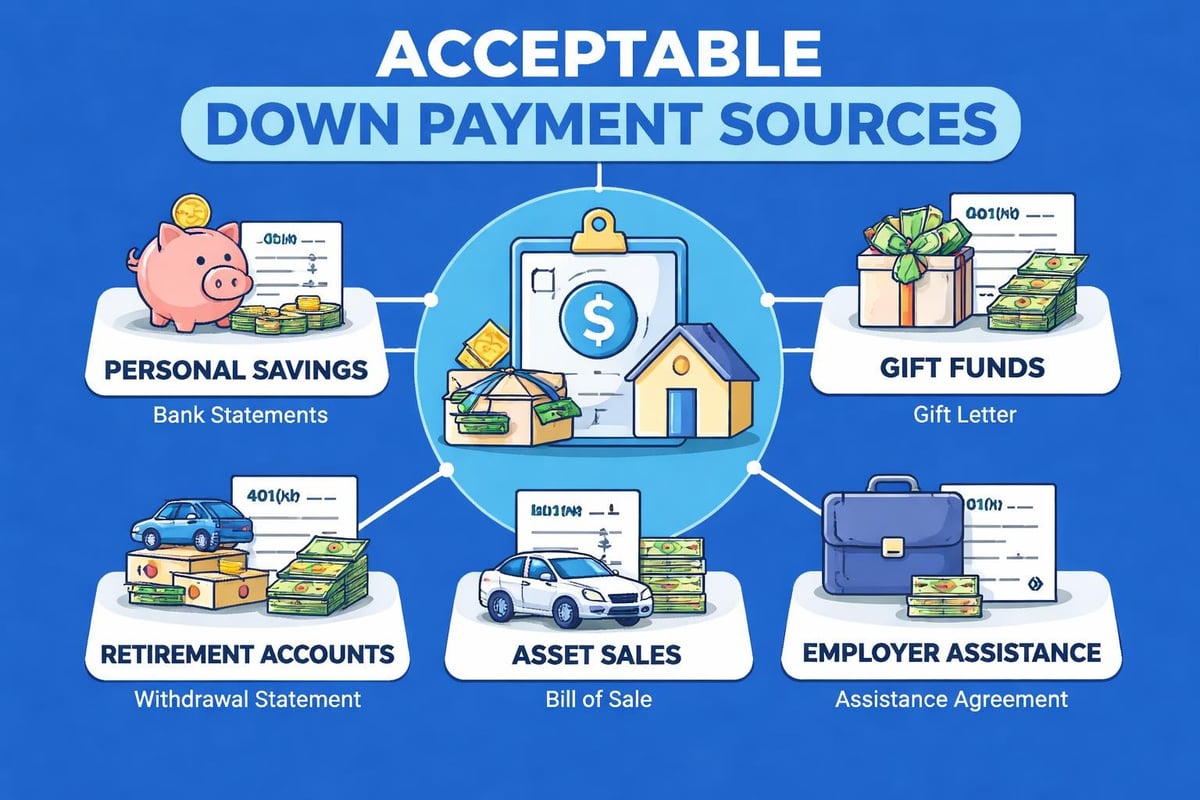

Creative Down Payment Sources and Strategies

Buyers often ask about acceptable down payment sources beyond traditional savings accounts. Understanding your options for funding a down payment expands your strategic possibilities while ensuring you meet lender guidelines.

Gift funds from family members are widely accepted on conventional, FHA, and VA loans with proper documentation. Donors must provide gift letters stating the funds are gifts, not loans requiring repayment. Bank statements showing the donor's ability to provide the funds are typically required.

Retirement account withdrawals are permitted but carry tax implications and potential penalties. First-time buyers can withdraw up to $10,000 from IRAs penalty-free for home purchases, though income taxes still apply. 401(k) loans or hardship withdrawals are options but come with repayment obligations and risks if you change employment.

Sale of assets including stocks, bonds, or other investments provides legitimate down payment funds. Expect to document the sale transaction and transfer of proceeds into your bank account. Large deposits require explanation and sourcing during the mortgage approval process.

Grants from employers or relocation assistance for transferring employees can supplement your down payment. Tech companies throughout Seattle sometimes offer housing assistance packages for new hires or relocating staff, which can be combined with traditional financing.

What you cannot use: unsecured personal loans, cash advances from credit cards, or borrowed funds requiring repayment. These create additional debt obligations that impact your debt-to-income ratio and potentially disqualify you from mortgage approval.

Down Payment Timing and Market Considerations

Deciding when to buy based on your down payment readiness involves more than just hitting a savings target. Seattle's real estate market experiences seasonal patterns, with spring and early summer bringing peak inventory and competition. Fall and winter often present opportunities for buyers with strong financial positions, including substantial down payments, to negotiate more effectively.

Interest rate environments also factor into your down payment strategy. When rates are rising, as they have been periodically throughout 2025-2026, locking in financing sooner rather than waiting to save a larger down payment can make economic sense. The monthly payment difference from a 0.5% rate increase often exceeds the savings from mortgage insurance elimination.

Property appreciation in Seattle's strong market historically has outpaced the cost of mortgage insurance for buyers who entered homeownership sooner with smaller down payments. A buyer who purchased in Everett in 2023 with 5% down captured significant equity appreciation despite paying PMI, while a buyer waiting to save 20% missed that appreciation window entirely.

This doesn't mean rushing into homeownership before you're financially prepared. It means evaluating the complete picture: current rates, market appreciation trends, rental costs, and your personal financial stability.

Removing Mortgage Insurance After Purchase

For conventional loan borrowers who put down less than 20%, private mortgage insurance isn't permanent. Once your loan balance reaches 80% of the original purchase price through regular payments, you can request PMI cancellation. At 78% loan-to-value, servicers are required to automatically remove it.

Many borrowers accelerate this timeline through home value appreciation. If your Seattle or Bellevue property increases significantly in value, you can request PMI removal based on a new appraisal showing 20% or more equity. Most lenders require:

- Minimum two years of on-time payments (some allow after one year)

- Current appraisal at borrower's expense

- No subordinate liens on the property

- Demonstration of 20-25% equity based on current value

Alternatively, refinancing into a new loan without mortgage insurance becomes viable once you've built sufficient equity. This strategy works best when current interest rates are competitive with your existing rate, making the refinance cost-effective beyond just PMI elimination.

FHA mortgage insurance operates differently. For loans originated after June 2013 with less than 10% down, annual mortgage insurance premiums remain for the life of the loan. The only way to remove FHA insurance is refinancing into a conventional loan once you've reached 20% equity.

Tax Implications of Down Payment Size

The size of your down payment indirectly affects your tax situation through mortgage interest deductions. Larger down payments mean smaller loan amounts and therefore less mortgage interest paid annually. Since mortgage interest is tax-deductible up to certain limits, this reduces your potential tax benefit.

For 2026, married couples filing jointly can deduct interest on mortgage debt up to $750,000 ($375,000 if married filing separately). Single filers have the same $750,000 limit. With standard deductions remaining high ($30,000 for married couples in 2026), many homeowners don't itemize deductions, making the mortgage interest deduction less valuable than it once was.

This tax consideration shouldn't drive your down payment decision but deserves acknowledgment in your overall financial planning. Buyers in higher tax brackets purchasing expensive properties in Bellevue or Kirkland may benefit more from mortgage interest deductions, making smaller down payments marginally more attractive from a tax efficiency standpoint.

Building Your Down Payment Savings Plan

Developing a realistic savings plan starts with knowing your target purchase price and required down payment percentage. For a $650,000 home in Seattle with 5% down, you need $32,500 plus closing costs (typically 2-3% of purchase price), totaling approximately $45,000-50,000.

Automated savings transfers from every paycheck ensure consistent progress toward your goal. Even $500 per paycheck ($1,000 monthly for biweekly pay) builds $12,000 annually, reaching a $36,000 down payment in three years. High-yield savings accounts maximize your money's growth while maintaining liquidity and safety. Rates in 2026 remain competitive for online savings accounts, often exceeding 4% APY.

Reducing recurring expenses accelerates savings timelines significantly. Dining out, subscription services, and discretionary spending add up quickly. Redirecting $300-500 monthly from lifestyle expenses to your home fund can reduce your timeline by a full year or more.

For tech professionals earning equity compensation, RSU vesting schedules present strategic opportunities. Planning your home purchase around anticipated vesting events ensures maximum down payment capacity. However, timing market transactions around employment compensation requires careful tax planning, as RSU vesting creates taxable income events.

Understanding down payment requirements, options, and strategies puts you in control of your homebuying timeline and financial success. Whether you're ready to move forward with 3% down or strategically building toward 20%, having an experienced mortgage broker guide your decisions ensures you choose the right path for your unique situation. Keith Akada and the team at Mortgage Reel specialize in helping Seattle-area buyers-from first-time purchasers to tech professionals leveraging RSU income-navigate down payment strategies, explore assistance programs, and structure financing that aligns with both immediate homeownership goals and long-term financial health.