Choosing the right financing partner represents one of the most critical decisions in your home buying journey. First home buyer lenders specialize in helping new purchasers navigate the mortgage process, offering programs designed specifically for those entering the real estate market for the first time. In competitive markets like Seattle, Bellevue, and Redmond, understanding which lenders provide the strongest support, best rates, and most flexible qualification criteria can make the difference between securing your dream home and missing out. This comprehensive guide examines what distinguishes quality first home buyer lenders, which loan programs they offer, and how to select the right partner for your specific financial situation.

Understanding First Home Buyer Lenders

First home buyer lenders are financial institutions or mortgage professionals who specialize in serving purchasers with limited home buying experience. These lenders offer specialized knowledge about programs designed for first-time buyers and typically provide enhanced educational support throughout the mortgage process.

What Makes These Lenders Different

Not all mortgage lenders focus equally on first-time purchasers. Those who specialize in this market segment understand the unique challenges new buyers face, including limited savings for down payments, unfamiliarity with closing procedures, and questions about long-term affordability.

Key characteristics of specialized first home buyer lenders include:

- Access to low down payment programs (3% to 3.5% down)

- Experience with down payment assistance programs

- Patient communication and educational resources

- Flexible qualification criteria for those with limited credit history

- Knowledge of local first-time buyer incentives and grants

Many first home buyer lenders in the Seattle area maintain relationships with state and local housing agencies, enabling them to connect clients with programs specifically designed for the region. For instance, buyers in Mill Creek or Lynnwood may qualify for different assistance programs than those purchasing in downtown Seattle, and specialized lenders know these distinctions.

Types of Lending Institutions

The mortgage marketplace includes several types of institutions that serve first-time buyers, each with distinct advantages and operational models.

| Lender Type | Advantages | Considerations |

|---|---|---|

| Mortgage Brokers | Access to multiple lenders, personalized service, competitive rate shopping | Relationship-based, local market expertise |

| Direct Lenders/Banks | Direct underwriting, potential relationship discounts | Limited to their own loan products |

| Credit Unions | Member benefits, lower fees | Membership requirements, smaller loan limits |

| Online Lenders | Streamlined digital process, competitive rates | Less personal guidance, limited local expertise |

For tech professionals working at Amazon, Microsoft, or Google in the Seattle area, working with a broker who understands stock-based compensation can be particularly valuable when qualifying for higher loan amounts.

Essential Loan Programs for First-Time Buyers

First home buyer lenders typically offer several loan programs specifically designed for purchasers with limited equity or down payment funds. Understanding these options helps you identify lenders who can best serve your needs.

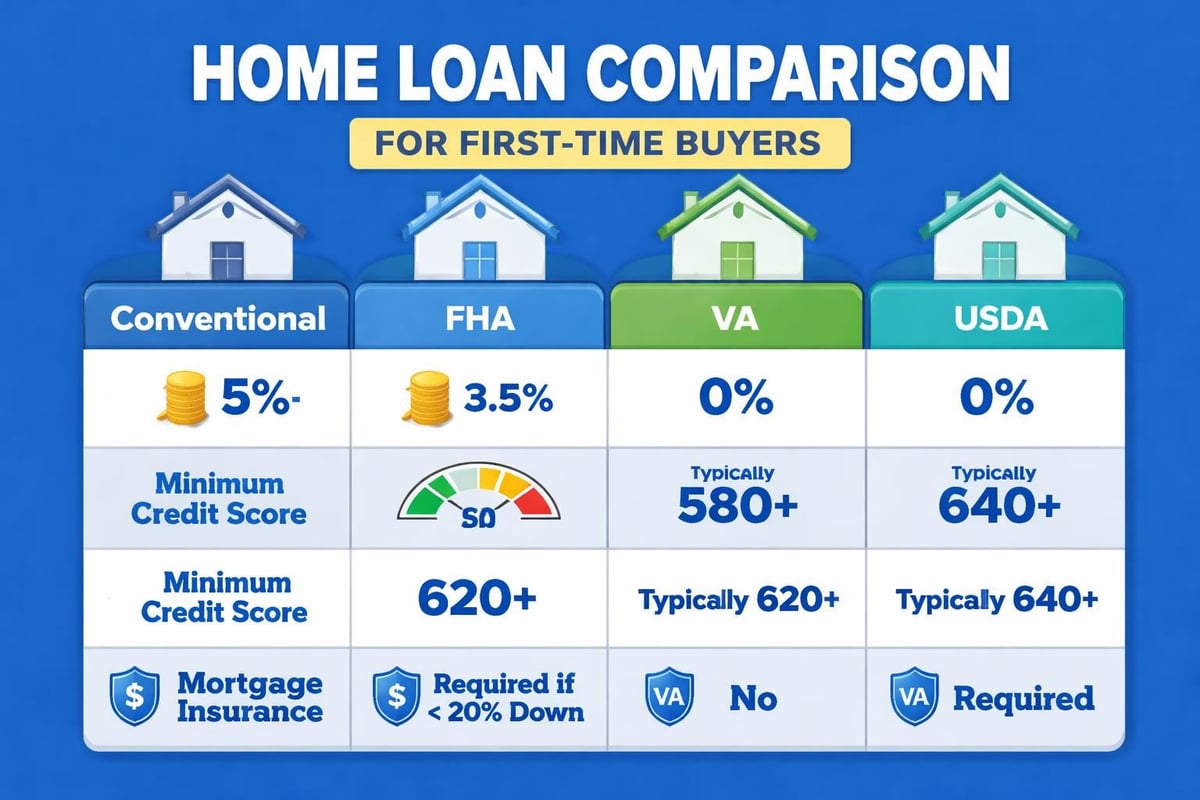

Conventional 97 and HomeReady Programs

Conventional loans with as little as 3% down have become increasingly popular among first-time buyers. The Conventional 97 program and Fannie Mae's HomeReady loan allow qualified borrowers to purchase with minimal down payment while accessing competitive interest rates.

HomeReady program benefits include:

- Down payment as low as 3%

- Flexible income sources (including rental income from boarders)

- Reduced mortgage insurance costs compared to standard conventional loans

- Income limits apply in some areas

- Mandatory homebuyer education course

These programs work particularly well for buyers in Shoreline or Lake Forest Park who may have strong income but limited savings due to high Seattle-area rental costs. Multiple mortgage lenders for first-time home buyers offer these conventional products with varying qualification requirements.

FHA Loans

Federal Housing Administration loans remain a cornerstone offering among first home buyer lenders. With down payments as low as 3.5% and credit score requirements starting at 580, FHA loans provide accessible financing for many new purchasers.

The program allows higher debt-to-income ratios than conventional loans, making qualification easier for buyers with student loans or car payments. However, FHA loans require both upfront and ongoing mortgage insurance premiums, which increases the total monthly payment.

In the Seattle metro area, FHA loan limits for 2026 allow borrowers to finance properties up to $869,400 in King County, accommodating many single-family homes and condos in areas like Everett and Lynnwood.

VA Loans

Veterans, active-duty service members, and eligible surviving spouses can access VA loans with zero down payment and no mortgage insurance requirement. This government-backed program represents one of the most powerful tools available to first-time buyers with military service.

VA loan advantages include:

- No down payment required

- No ongoing mortgage insurance

- Competitive interest rates

- Flexible credit requirements

- Limited closing costs

First home buyer lenders experienced with VA financing understand the certificate of eligibility process and can expedite approval timelines. Various loan programs available to first-time home buyers each offer distinct benefits depending on your qualification profile.

Qualification Requirements and Strategies

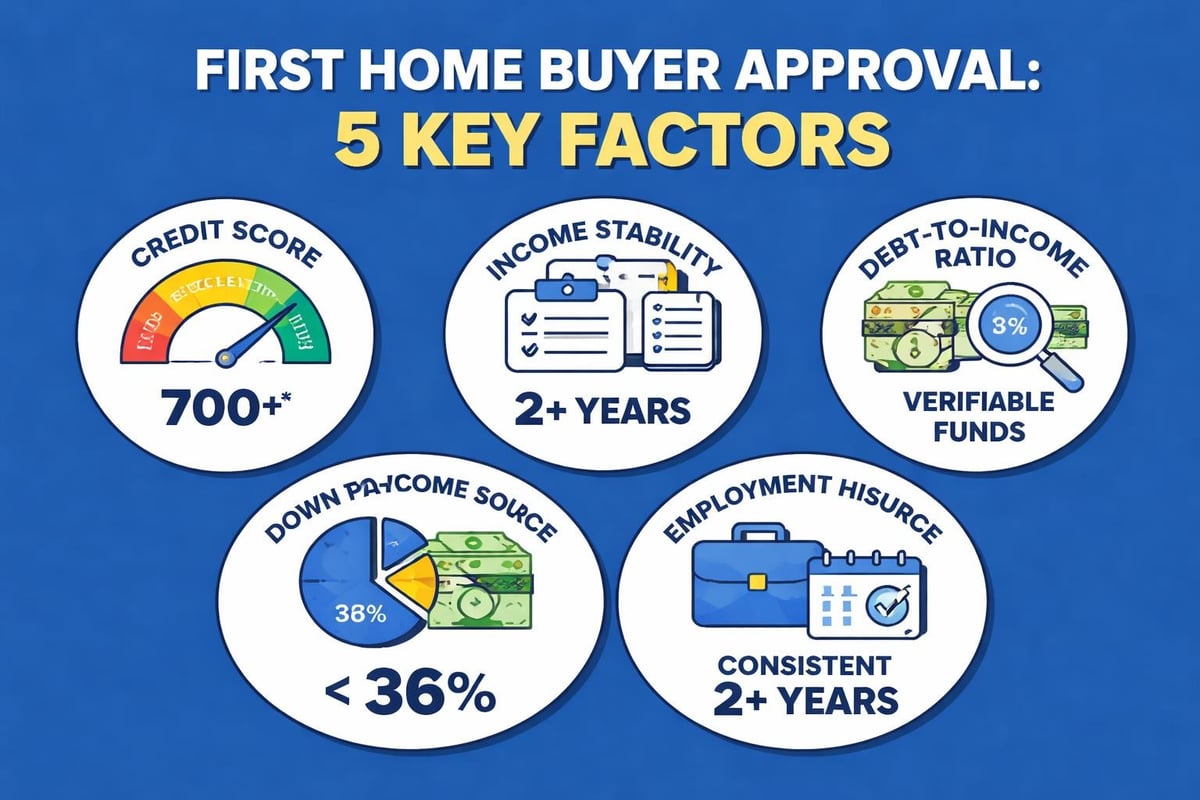

Understanding what first home buyer lenders look for during the approval process helps you prepare a stronger application and avoid common pitfalls that delay or derail financing.

Credit Score Expectations

Different loan programs maintain varying credit score requirements, and individual lenders may impose their own minimums above program guidelines.

| Loan Type | Minimum Score | Preferred Score | Rate Impact |

|---|---|---|---|

| Conventional 97 | 620 | 680+ | Significant below 700 |

| FHA | 580 (3.5% down) | 640+ | Moderate below 660 |

| VA | No minimum | 620+ | Minimal variation |

| USDA | 640 | 660+ | Moderate below 680 |

Buyers in competitive Seattle neighborhoods should aim for scores above 700 when possible to access the best rates and terms. For those with lower scores, FHA or VA programs (if eligible) often provide the most accessible path to homeownership.

Income Documentation for Tech Professionals

Seattle-area tech workers often receive compensation through base salary, bonuses, restricted stock units (RSUs), and stock options. Not all first home buyer lenders have equal expertise in qualifying these income types.

Qualifying stock-based compensation requires:

- Two-year history of receiving equity compensation

- Documentation of vesting schedules

- Conservative calculation of future RSU values

- Understanding of tax implications on gross income

Experienced lenders can often qualify RSU income that less sophisticated competitors might exclude, potentially increasing your buying power by $100,000 or more in Seattle's high-cost market. This expertise proves particularly valuable when pursuing competitive Seattle mortgage rates on higher loan amounts.

Debt-to-Income Ratio Considerations

Your debt-to-income (DTI) ratio compares your monthly debt obligations to your gross monthly income. Most first home buyer lenders limit total DTI to 43-50%, depending on the loan program and compensating factors.

Monthly debts included in DTI calculations:

- Future mortgage payment (principal, interest, taxes, insurance)

- Student loan payments

- Auto loans and leases

- Credit card minimum payments

- Personal loans

- Child support or alimony obligations

Buyers with student debt should understand that lenders use either the actual payment or a calculated payment (typically 1% of the balance) when determining qualification. Working with knowledgeable first home buyer lenders helps you structure your application to optimize DTI ratios within program guidelines.

Down Payment and Closing Cost Strategies

Saving for a down payment represents one of the biggest hurdles for first-time purchasers in expensive markets like Seattle and Bellevue. First home buyer lenders can help you navigate multiple strategies to reduce upfront cash requirements.

Gift Funds and Family Assistance

All major loan programs allow borrowers to use gift funds from family members for down payment and closing costs. Proper documentation is essential, including a gift letter stating the funds are a gift (not a loan) and bank statements showing the transfer.

Parents or relatives gifting funds to buyers in Redmond or Kirkland should understand that the borrower must typically contribute at least 1% of their own funds on conventional loans, though FHA and VA loans permit 100% gifted down payments.

Down Payment Assistance Programs

Washington State and local jurisdictions offer several programs that provide grants or second mortgages to help first-time buyers with down payments. First home buyer lenders familiar with these programs can guide you through application processes and coordinate with housing agencies.

Popular assistance programs in the Seattle area include:

- Washington State Housing Finance Commission programs

- Seattle Office of Housing assistance

- County-specific first-time buyer grants

- Employer-sponsored homebuyer programs (common among tech companies)

These programs often require income limits and homebuyer education courses, but can provide $5,000 to $25,000 in assistance that doesn't need to be repaid (if you meet occupancy requirements).

Seller Concessions

In balanced or buyer-friendly markets, negotiating seller-paid closing costs can significantly reduce your cash requirement at closing. Most loan programs allow sellers to contribute 3-6% of the purchase price toward buyer closing costs.

Experienced first home buyer lenders can calculate exactly how much you need to request in your offer and ensure concessions are structured to comply with program limits. This strategy works particularly well in areas like Everett or Mill Creek where competition may be less intense than in central Seattle neighborhoods.

Selecting the Right Lender for Your Situation

Not all first home buyer lenders offer the same level of service, expertise, or access to programs. Evaluating potential lenders across multiple dimensions helps you identify the best partner for your specific circumstances.

Questions to Ask Prospective Lenders

Before committing to work with any lender, gather information that reveals their expertise and approach.

-

How many first-time buyers do you work with annually? Lenders who specialize in this market segment typically close 50+ first-time buyer transactions yearly.

-

Which down payment assistance programs do you have experience with? Generic awareness differs significantly from actual implementation experience.

-

How do you handle RSU or stock-based compensation? Critical for Seattle-area tech employees who need maximum qualification.

-

What is your average time to close? Speed matters in competitive markets, but realistic timelines prevent disappointment.

-

Can you provide references from recent first-time buyer clients? Strong lenders maintain extensive review profiles across multiple platforms.

Comparing Loan Estimates

Federal law requires lenders to provide a standardized Loan Estimate within three business days of application. This document enables accurate comparison across different first home buyer lenders.

Key sections to compare include:

- Interest rate and annual percentage rate (APR)

- Loan origination fees and points

- Third-party service costs (appraisal, title, escrow)

- Lender credits or discounts

- Estimated monthly payment

- Cash required at closing

Remember that the lowest rate doesn't always represent the best value. A lender offering 6.25% with $3,000 in fees may cost less over the first several years than one offering 6.125% with $8,000 in fees, depending on how long you plan to keep the loan.

Technology and Communication Standards

Modern first home buyer lenders leverage technology to streamline the application and approval process, but technology should enhance, not replace, personal communication.

Digital Application and Document Management

Secure online portals allow you to complete applications, upload documents, and track loan progress 24/7. This convenience proves particularly valuable for busy professionals working at Amazon, Microsoft, or other demanding Seattle employers.

Look for lenders offering mobile-responsive platforms that accept electronic signatures and provide real-time status updates. However, ensure technology is paired with accessible human support when you need guidance or have complex questions.

Communication Expectations

First-time buyers typically have more questions and require more explanation than experienced purchasers. Quality first home buyer lenders establish clear communication protocols and maintain accessibility throughout the process.

Expect your lender to provide:

- Response to questions within one business day

- Proactive updates when milestones are reached

- Clear explanation of requirements in plain language

- Availability during evenings or weekends when needed

- Direct access to your loan officer, not just assistants

Reviews and testimonials from previous clients offer insight into communication quality and responsiveness before you commit to working with any lender.

Local Market Expertise in Seattle

First home buyer lenders with deep Seattle-area knowledge bring valuable insights that national online lenders simply cannot match. Understanding neighborhood characteristics, property types, and local market dynamics directly impacts your success.

Neighborhood-Specific Guidance

Different Seattle neighborhoods present distinct opportunities and challenges for first-time buyers. A condo in downtown Bellevue requires different financing considerations than a single-family home in Lake Forest Park or a townhouse in Shoreline.

Local lenders understand which buildings have FHA or VA approval, which neighborhoods are appreciating most rapidly, and where first-time buyers can find the best value. This knowledge helps you make informed decisions about where to focus your home search given your budget and financing options.

Condo Financing Expertise

Many affordable properties in the Seattle metro area are condominiums, which require additional lender scrutiny beyond single-family home financing. The condo project itself must meet specific criteria regarding owner-occupancy ratios, HOA financial health, and completion status.

First home buyer lenders experienced with Seattle-area condo projects can quickly determine whether a building qualifies for your loan program, preventing wasted time on properties that won't finance. This expertise proves particularly valuable in competitive buildings where you may need to move quickly on desirable units.

Pre-Approval Strategy and Timing

Obtaining pre-approval from qualified first home buyer lenders before beginning your home search provides significant advantages in competitive markets like Seattle, Redmond, and Kirkland.

Full Underwriting vs. Pre-Qualification

Understanding the distinction between pre-qualification, pre-approval, and full underwriting helps you position yourself as a strong buyer.

| Status | Documentation Required | Certainty Level | Competitive Advantage |

|---|---|---|---|

| Pre-Qualification | Self-reported information | Low | Minimal |

| Pre-Approval | Income, asset, credit verification | Moderate-High | Significant |

| Full Underwriting | Complete file reviewed by underwriter | Very High | Maximum |

Some first home buyer lenders offer fully underwritten approval before you find a property, removing nearly all financing contingencies from your offer. This positions you similarly to cash buyers and can be decisive when competing against multiple offers in desirable Seattle neighborhoods.

Rate Lock Strategies

Interest rates fluctuate daily, and timing your rate lock appropriately protects you from increases while maintaining flexibility if rates decline. Most lenders offer lock periods from 15 to 60 days, with longer locks typically costing more.

Working with experienced first home buyer lenders helps you understand current rate trends and determine the optimal lock timing. In rapidly changing rate environments, float-down options (which allow you to capture lower rates if they decline after locking) provide valuable insurance for an additional cost.

Working With Real Estate Agents

First home buyer lenders collaborate closely with real estate agents throughout the transaction. Understanding this relationship and choosing complementary professionals strengthens your overall team.

Agent-Lender Coordination

Your agent and lender must communicate effectively to coordinate offer timing, closing dates, and contingency removal. Quality first home buyer lenders maintain strong relationships with local agents and understand how to work efficiently within Seattle-area transaction norms.

Experienced agent-lender teams can often identify and resolve potential issues before they impact your transaction timeline or success. This coordination proves particularly valuable during the inspection period when repair negotiations may affect your financing or appraisal.

Offer Structure and Financing Terms

How you structure your financing terms directly impacts offer competitiveness. Shorter contingency periods, larger earnest money deposits, and appraisal gap coverage all strengthen your position but require careful coordination with your lender.

First home buyer lenders can advise on realistic timelines for removing financing contingencies based on current appraisal and underwriting volumes. Committing to impossible timelines to win an offer ultimately helps no one if you cannot perform as promised.

After You Choose Your Lender

Once you select from among competing first home buyer lenders, your responsibility shifts to responsive cooperation throughout the approval process.

Document Collection and Organization

Lenders require extensive documentation to verify income, assets, employment, and credit. Providing complete, organized documentation accelerates approval and prevents delays.

Standard documents include:

- Two years of W-2 forms and tax returns

- 30 days of recent pay stubs

- Two months of bank statements for all accounts

- Explanation letters for any credit issues or unusual deposits

- Documentation of gift funds or down payment assistance

- For tech workers: RSU vesting schedules and equity compensation history

First home buyer lenders typically provide detailed checklists customized to your specific loan program and situation. Following these requirements precisely prevents repeated requests and expedites closing.

Managing the Process Timeline

Understanding the typical mortgage timeline helps you plan effectively and know when action or patience is required.

- Application and initial disclosure (Day 0-3)

- Document collection and submission (Day 1-7)

- Property appraisal ordered (Day 3-5)

- Loan submission to underwriting (Day 7-14)

- Initial underwriting review (Day 10-20)

- Conditional approval issued (Day 15-25)

- Final conditions cleared (Day 20-35)

- Clear to close (Day 30-40)

- Closing (Day 35-45)

Experienced first home buyer lenders in Seattle can often accelerate this timeline, particularly when working with responsive borrowers who provide complete documentation upfront. Some advanced lenders can close loans in as few as 9-14 business days when necessary to secure competitive properties.

Staying Financially Stable

Between application and closing, maintain financial stability by avoiding major purchases, job changes, or new credit applications. Even positive changes like paying off debt can sometimes complicate underwriting if not properly coordinated with your lender.

First home buyer lenders emphasize the importance of maintaining the financial picture that qualified you for approval. Large deposits, new loans, or employment changes require explanation and potentially re-verification, which can delay closing or, in extreme cases, jeopardize approval.

Understanding True Costs Beyond the Mortgage

Beyond your monthly principal and interest payment, homeownership involves several additional costs that quality first home buyer lenders help you understand and budget for appropriately.

Property Taxes in Seattle Area

Property taxes vary significantly across the Seattle metro area, impacting your total monthly payment and long-term affordability. King County properties currently average 0.92% of assessed value annually, but rates differ by city and taxing district.

A $600,000 home in Everett might carry annual property taxes of $5,500, while a similar home in Bellevue could exceed $6,500 due to different levy rates. First home buyer lenders incorporate accurate tax estimates into your qualification and payment calculations.

Homeowners Insurance Requirements

All mortgage programs require homeowners insurance coverage sufficient to rebuild your property. Insurance costs in the Seattle area typically range from $800 to $1,800 annually depending on coverage limits, deductibles, and property characteristics.

Homes in areas with higher wildfire risk or older construction may face higher premiums. First home buyer lenders can connect you with insurance agents who specialize in Washington State coverage before you make an offer, ensuring you understand true monthly costs.

HOA Fees and Special Assessments

Condos and planned communities assess monthly HOA fees that cover common area maintenance, insurance, and amenities. These fees directly impact your debt-to-income ratio and affordability.

Seattle-area HOA fees range from $200 monthly for basic townhome communities to $800+ for full-service downtown condos with concierge and amenity packages. First home buyer lenders include these fees when calculating your maximum purchase price to prevent you from falling in love with properties you cannot afford.

Navigating the Seattle-area housing market as a first-time buyer requires partnering with the right financing professional who understands your unique situation and local market dynamics. Whether you're a tech professional in Redmond qualifying RSU income or a buyer in Shoreline exploring down payment assistance options, working with a specialized broker makes the difference between uncertainty and confidence. Keith Akada brings 25+ years of experience helping first-time buyers across Seattle, Bellevue, and surrounding communities secure the right financing with clear guidance and reliable execution-connect with Mortgage Reel to start your journey toward homeownership with a trusted local expert.