Buying your first home in 2026 is both thrilling and nerve-wracking. The real estate market is fast-paced, and first-time buyers often feel overwhelmed by all the choices and challenges.

From understanding new mortgage rules to competing in bidding wars, the process can seem daunting. Many are unsure where to start or how to secure the best deal.

That is where a first home buyer broker becomes invaluable. These professionals help simplify every step, offering expert guidance and giving buyers a real advantage in the market.

This article is your step-by-step roadmap for working with a first home buyer broker in 2026. You will learn what to expect, how to choose the right partner, and the latest strategies for success. We will also cover the broker’s role, how to prepare, and key trends shaping this year’s market.

Understanding the Role of a First Home Buyer Broker

Buying your first home in 2026 can feel overwhelming, especially when faced with new regulations and a fast-moving market. A first home buyer broker is your dedicated guide, helping you navigate the journey with confidence. This section explains what makes a first home buyer broker unique, how they simplify the process, and why their expertise is invaluable for first-time buyers.

What is a First Home Buyer Broker?

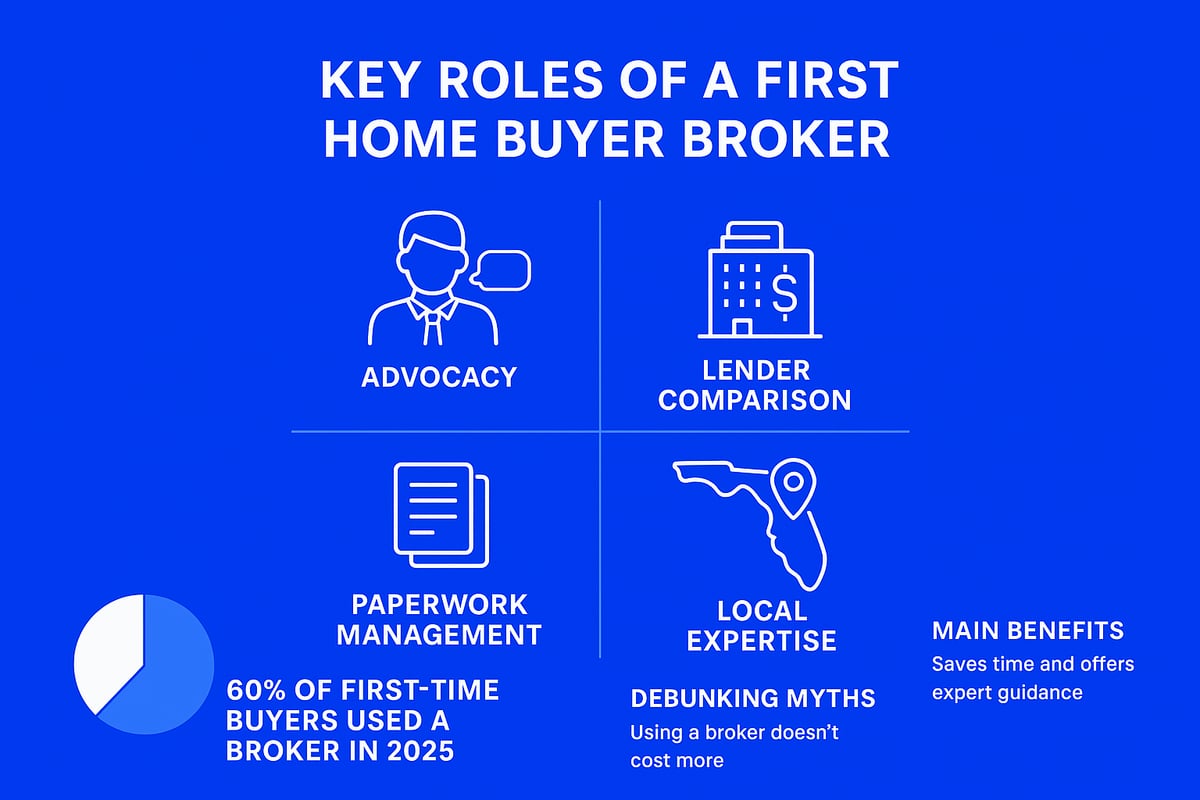

A first home buyer broker specializes in helping individuals purchase their first property, acting as an advocate throughout the process. Unlike traditional mortgage brokers, who may serve a broad range of clients, or real estate agents, who focus on property selection and negotiation, a first home buyer broker is dedicated to the specific needs of first-timers.

They guide buyers from initial financial assessment to closing, ensuring each step is clear and manageable. According to the National Association of Realtors, over 60% of first-time buyers in 2025 used a broker, underlining the growing value of this service.

How Brokers Simplify the Homebuying Process

A first home buyer broker streamlines the often complex homebuying journey. They help you understand a wide variety of mortgage products, eligibility rules, and lender requirements. By comparing multiple lenders on your behalf, brokers find the most favorable rates and terms.

They also manage essential paperwork, from pre-approvals to regulatory disclosures, reducing stress and minimizing errors. With a broker’s support, first-time buyers can focus on finding the right home rather than getting lost in documentation.

Broker vs. Direct Lender: Pros and Cons

Choosing between a first home buyer broker and a direct lender is a key decision. Brokers offer access to a variety of lenders, increasing your options for rates and loan products. Direct lenders only present their own offerings, which may limit flexibility.

| Feature | First Home Buyer Broker | Direct Lender |

|---|---|---|

| Lender Access | Multiple | Single |

| Service Flexibility | High | Moderate |

| Advocacy | Dedicated to Buyer | Lender-Focused |

| Paperwork Assistance | Comprehensive | Limited |

| Fee Structure | Varies | Typically Fixed |

Case studies show that buyers working with brokers often secure better terms and feel more supported throughout the process.

Typical Broker Fees and Payment Structures

Understanding how a first home buyer broker is compensated is essential for transparency. Brokers may be paid by the lender, the borrower, or a combination of both. Lender-paid compensation is most common, meaning you may not pay a fee directly.

Federal regulations require clear disclosure of all broker fees, protecting buyers from hidden costs. Always review fee structures early to avoid surprises and ensure your broker operates with full transparency.

The Broker’s Fiduciary Duty to Buyers

A first home buyer broker is legally and ethically obligated to act in your best interest. This fiduciary duty requires complete honesty, full disclosure, and the avoidance of conflicts of interest. It protects buyers from predatory lending and ensures recommendations are always tailored to your benefit.

This commitment builds trust and empowers first-time buyers to make informed decisions with confidence.

The Value of Local Expertise

Local knowledge sets a first home buyer broker apart. They understand neighborhood trends, down payment assistance, and unique programs in your area. For example, brokers in Seattle, Austin, and Miami leverage city-specific incentives to maximize affordability.

To explore local programs that may be available, see these Seattle first-time homebuyer programs for practical examples of how brokers connect buyers to valuable resources.

Common Misconceptions About Brokers

Some first-time buyers believe using a first home buyer broker is costly or that brokers only have access to a limited pool of lenders. In reality, most buyers do not pay broker fees out of pocket, and brokers often work with dozens of lending partners.

Other misconceptions include concerns about bias or missing out on exclusive deals. However, regulations require brokers to disclose all incentives and ensure recommendations serve your interests. By debunking these myths, buyers can approach the process with greater clarity and trust.

Preparing for Your First Home Purchase in 2026

Buying your first home in 2026 is both exciting and challenging. With the guidance of a first home buyer broker, you can navigate this process with confidence and clarity. Preparing early, understanding your finances, and setting clear expectations will set the foundation for success.

Assessing Your Financial Readiness

The journey begins with a thorough look at your finances. A first home buyer broker will help you review your credit score, which averaged 684 for first-time buyers in 2025. Understanding your debt-to-income ratio and true affordability is crucial. Brokers can offer personalized tips to strengthen your financial profile, making you more attractive to lenders.

Key steps include:

- Checking your credit report for errors

- Calculating your monthly expenses

- Reviewing your savings and income

Having these details ready ensures you make informed decisions with your first home buyer broker.

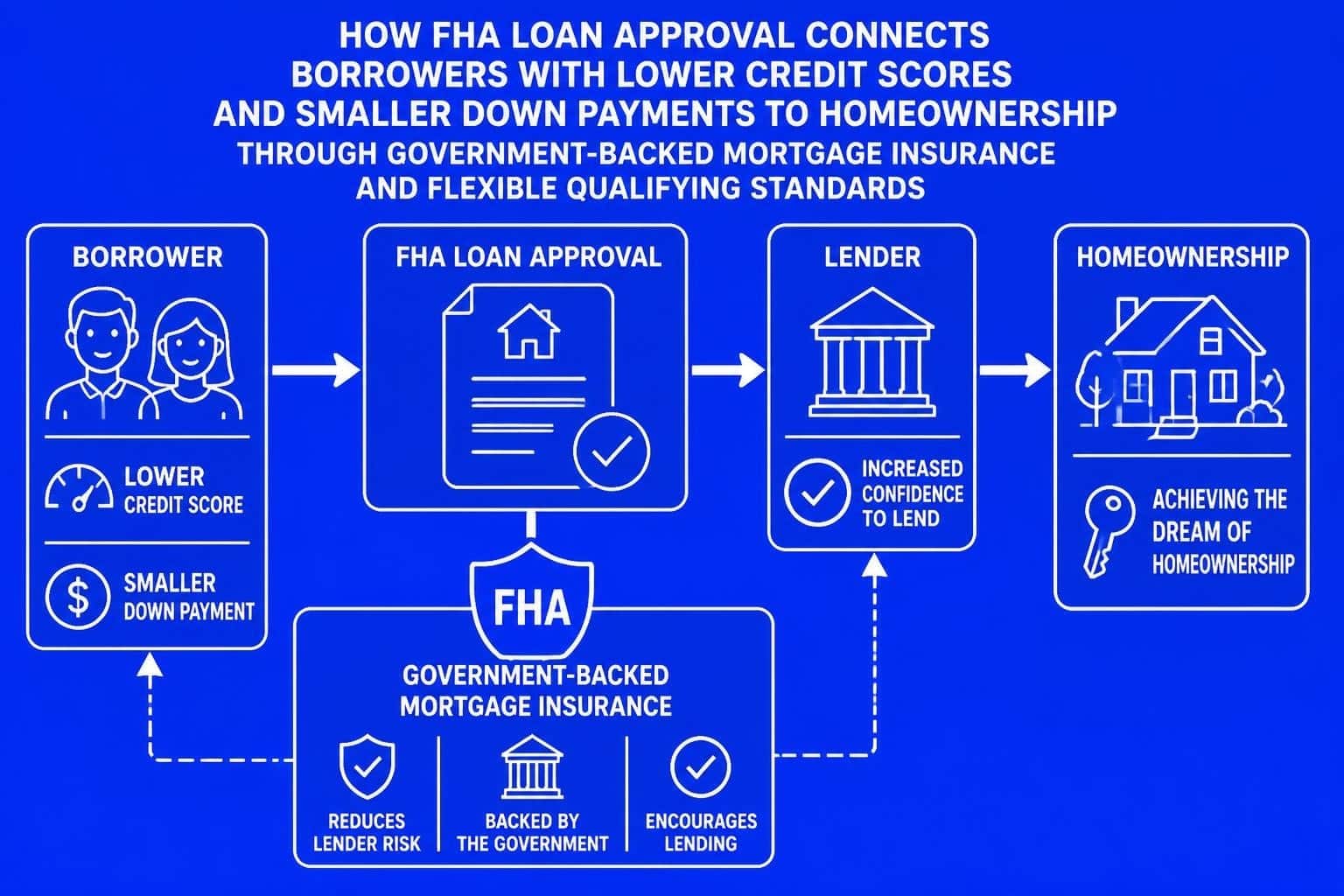

Saving for Down Payment and Closing Costs

Most first-time buyers in 2026 will need a down payment of 3 to 5 percent for conventional loans, 0 percent for VA loans, or 3.5 percent for FHA loans. Your first home buyer broker will outline all expected costs, including hidden fees like appraisal, inspection, insurance, and taxes.

Remember to ask about:

- Down payment assistance programs

- Local grants for first-time buyers

- How to estimate and budget for closing costs

With the right plan, your first home buyer broker can help you unlock programs that make homeownership more affordable.

Gathering Documentation and Pre-Approval

Being organized speeds up the loan process. Your first home buyer broker will provide a checklist of documents such as pay stubs, bank statements, tax returns, and identification. Securing pre-approval is critical in competitive markets, showing sellers you are a serious buyer.

Typical documents include:

- Proof of income (W-2s, pay stubs)

- Asset statements (savings, investments)

- Debt information (loans, credit cards)

For a detailed roadmap, review this How to buy a home guide to ensure nothing is overlooked when preparing with your first home buyer broker.

Understanding Your Must-Haves and Dealbreakers

Creating a homebuying checklist will clarify what matters most. Share your location preferences, property size, must-have features, and commute needs with your first home buyer broker. This helps focus your search and avoids wasting time on unsuitable properties.

Consider listing:

- Preferred neighborhoods

- Essential amenities (parking, laundry, outdoor space)

- Absolute dealbreakers (long commute, outdated systems)

A first home buyer broker uses this information to tailor options and streamline your search.

The Impact of 2026 Market Trends

Interest rates and housing inventory shape your homebuying journey. Your first home buyer broker will explain how forecasted rates and new construction trends affect affordability. In 2026, buyers face ongoing inventory shortages and fluctuating prices, so timing and preparation are more important than ever.

Stay informed by:

- Monitoring rate forecasts

- Watching for new listings

- Exploring alternative neighborhoods

A first home buyer broker keeps you ahead of the curve with timely market insights.

Emotional Preparation and Setting Expectations

Buying a home is a major milestone that can bring stress and decision fatigue. Your first home buyer broker is there to support you through uncertainties, manage your timeline, and keep your confidence high. Setting realistic expectations will help you stay focused and positive throughout the process.

Tips for emotional readiness:

- Allow time for each decision

- Rely on your broker’s expertise for reassurance

- Celebrate milestones along the way

With the guidance of a first home buyer broker, you can approach homeownership with confidence and peace of mind.

How to Choose the Right First Home Buyer Broker

Choosing the right first home buyer broker is a pivotal step in your journey to homeownership. The right partner can clarify the process, advocate for your interests, and help you avoid common pitfalls. Here is a detailed guide to evaluating and selecting the best broker for your needs.

Credentials and Licensing

Begin by verifying the credentials of any first home buyer broker you consider. Check for active licenses with the Nationwide Multistate Licensing System (NMLS) and your state’s regulatory board. Membership in professional associations demonstrates a commitment to industry standards.

Continuous education is essential. Ask brokers about recent courses or certifications they have completed. This ensures your broker is up to date on evolving mortgage regulations and loan products. A qualified broker will provide documentation of their credentials upon request.

Experience with First-Time Buyers

A broker’s experience with first-time homebuyers can make a significant difference. When interviewing a first home buyer broker, ask about their recent client successes, especially with buyers in similar financial situations.

Consider these questions:

- How many first-time buyers have you helped in the past year?

- Can you share a recent success story?

- What challenges do you often help first-time buyers overcome?

According to recent data, 78% of buyers in 2025 reported increased confidence when working with an experienced broker. Select a broker who understands the unique needs of first-time clients.

Local Market Knowledge

Local expertise is a major advantage when choosing a first home buyer broker. Brokers familiar with your target neighborhoods can provide insights into pricing trends, negotiation tactics, and city-specific incentives.

For example, brokers in Seattle, Austin, or Miami often have access to specialized programs and can guide you through local down payment assistance options. Hyper-local knowledge can be the difference between a winning offer and a missed opportunity.

Communication and Accessibility

Effective communication is crucial during the homebuying process. Assess how responsive a first home buyer broker is during your initial interactions. Do they answer questions clearly and promptly?

Preferred communication channels vary. Some buyers want in-person meetings, while others prefer virtual consultations, phone calls, or email updates. Clarify your preferences and ensure your broker can accommodate them. A broker who educates and keeps you informed every step of the way will reduce stress and build trust.

Transparent Fee Structures

Understanding how your first home buyer broker is compensated is key to avoiding surprises. Brokers may be paid by lenders or directly by borrowers. Always request a detailed fee disclosure before committing.

Look out for:

- Clear breakdowns of all fees

- No upfront charges before services are rendered

- Written explanations of compensation models

Be wary of vague terms or hidden costs. Transparency is a sign of a reputable broker.

Client Testimonials and Reviews

Client feedback offers valuable insight into a broker’s reliability and service quality. Search for reviews on platforms like Google, Zillow, and Yelp. Read both positive and negative comments to get a balanced perspective.

Look for patterns in feedback, such as consistent praise for responsiveness or recurring concerns about delays. Authentic testimonials can help you gauge whether a first home buyer broker is the right fit for your needs.

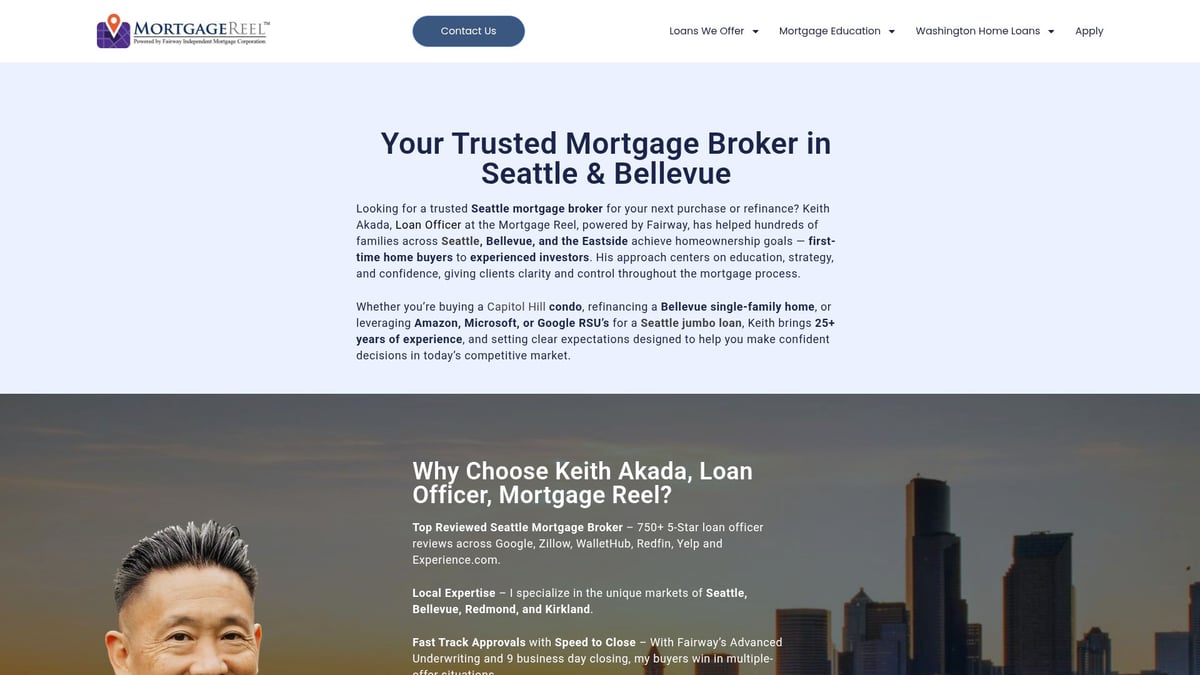

The Mortgage Reel: A Seattle-Based First Home Buyer Broker

The Mortgage Reel, led by Keith Akada, exemplifies what first-time buyers should seek in a first home buyer broker. Their team specializes in tailored loan solutions, including conventional, FHA, VA, and jumbo loans.

Unique features include fast-track approvals, expertise with tech industry clients, and an education-first approach. The Mortgage Reel is renowned for its local reputation, boasting over 750 five-star reviews and a record of 9-business-day closings. For a deeper understanding of the benefits of working with a Seattle mortgage broker, explore their Seattle mortgage broker expertise page, which details their personalized strategies and advantages in the local market.

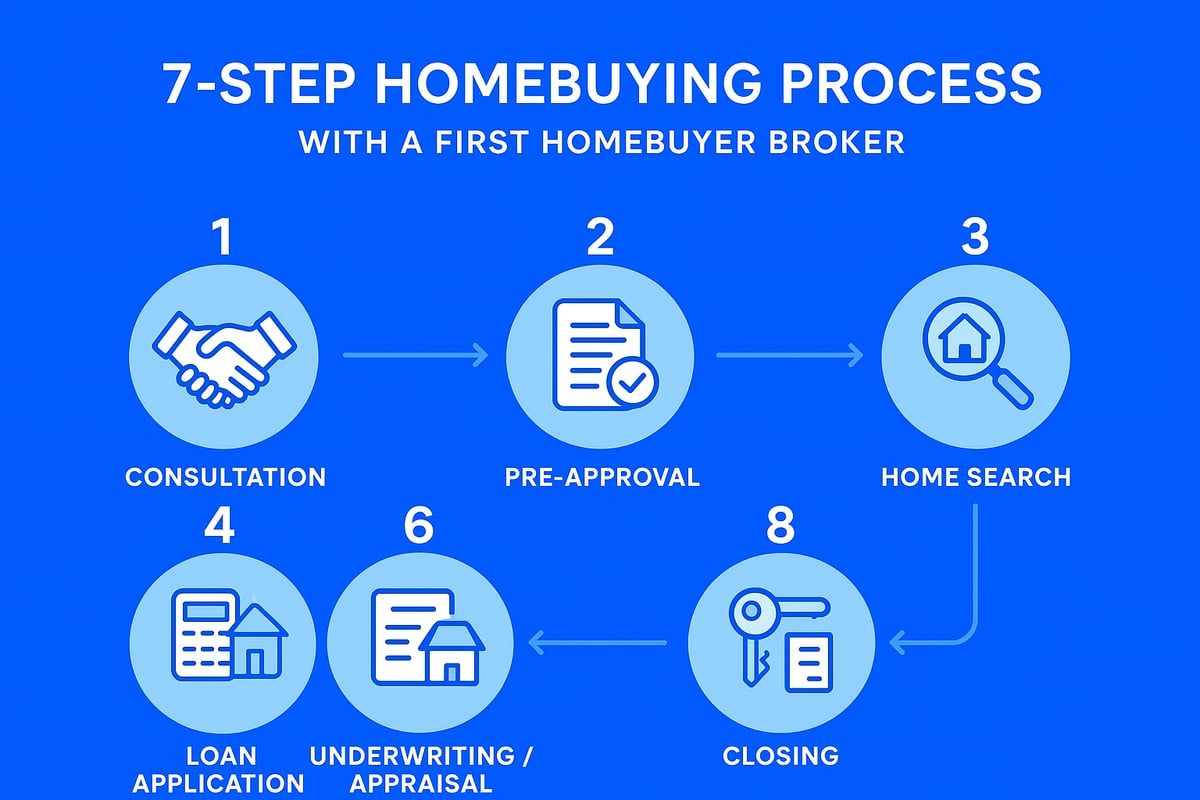

Step-by-Step: The First Home Buyer Broker Process in 2026

Buying your first home in 2026 can feel overwhelming, but a first home buyer broker can break the process into clear, manageable steps. By understanding each phase, buyers can approach the market with confidence and clarity. Here’s a detailed roadmap of what to expect at every stage when working with a first home buyer broker.

Step 1: Initial Consultation and Goal Setting

The journey begins with an initial consultation. During this meeting, the first home buyer broker assesses your goals, financial situation, and market preferences. Expect a detailed discussion about your desired location, property type, budget, and timeline.

Your broker will explain the latest market dynamics, including why the first-time homebuyer share has hit a record low, and how this impacts your search. This step sets the foundation for an efficient process, ensuring your expectations align with current realities.

Buyers receive a checklist of documents and questions to clarify their needs. This stage is about building trust and setting realistic objectives with your first home buyer broker.

Step 2: Mortgage Pre-Approval and Financial Review

Next, your first home buyer broker helps you secure mortgage pre-approval. This involves reviewing your credit, income, and assets to determine your borrowing power. Pre-approval is essential in the competitive 2026 market, giving you an edge when making offers.

The broker compares multiple lenders and mortgage products, identifying the best rates and terms for your situation. They explain each option, ensuring you understand the differences between fixed, adjustable, FHA, VA, and other loan types.

This step streamlines the financial review, making it easier to spot potential issues early and empowering you to act quickly when you find the right home.

Step 3: Home Search and Offer Preparation

With pre-approval in hand, your first home buyer broker collaborates with your real estate agent to begin the property search. They use your checklist of must-haves and dealbreakers to present properties that fit your lifestyle and budget.

Brokers offer local insights, pointing out neighborhood trends, school ratings, and future development plans. When you’re ready to make an offer, the broker helps draft a competitive bid, advising on contingencies, escalation clauses, and negotiation strategies.

This partnership ensures your offer stands out in a crowded field, maximizing your chances of acceptance.

Step 4: Loan Application and Documentation

Once your offer is accepted, the first home buyer broker guides you through the formal loan application. You’ll provide updated financial documents, such as pay stubs, bank statements, and identification.

The broker manages the paperwork, ensuring all disclosures and forms are completed accurately. They use secure digital platforms for document uploads, reducing errors and saving time.

Their experience helps you avoid common pitfalls, such as missing information or incorrect entries, which could delay the process.

Step 5: Underwriting and Appraisal

During underwriting, your lender reviews your application in detail. The first home buyer broker acts as your advocate, communicating with the lender to resolve questions and expedite the review.

An independent appraisal is scheduled to verify the property’s value. If the appraisal comes in lower than expected, the broker helps negotiate with the seller or adjust your financing plan.

Throughout underwriting and appraisal, your broker keeps you informed, so you’re never left wondering about your application’s status.

Step 6: Closing the Deal

The final stage before ownership is closing. Your first home buyer broker prepares you for the last steps, which include a final walkthrough, reviewing closing disclosures, and signing documents.

They explain each form, from loan agreements to title insurance, so you understand every detail. If issues arise, such as unexpected fees or last-minute changes, the broker intervenes to resolve them quickly.

This hands-on support ensures a smooth, stress-free closing, culminating in the moment you receive your keys.

Step 7: Post-Closing Support

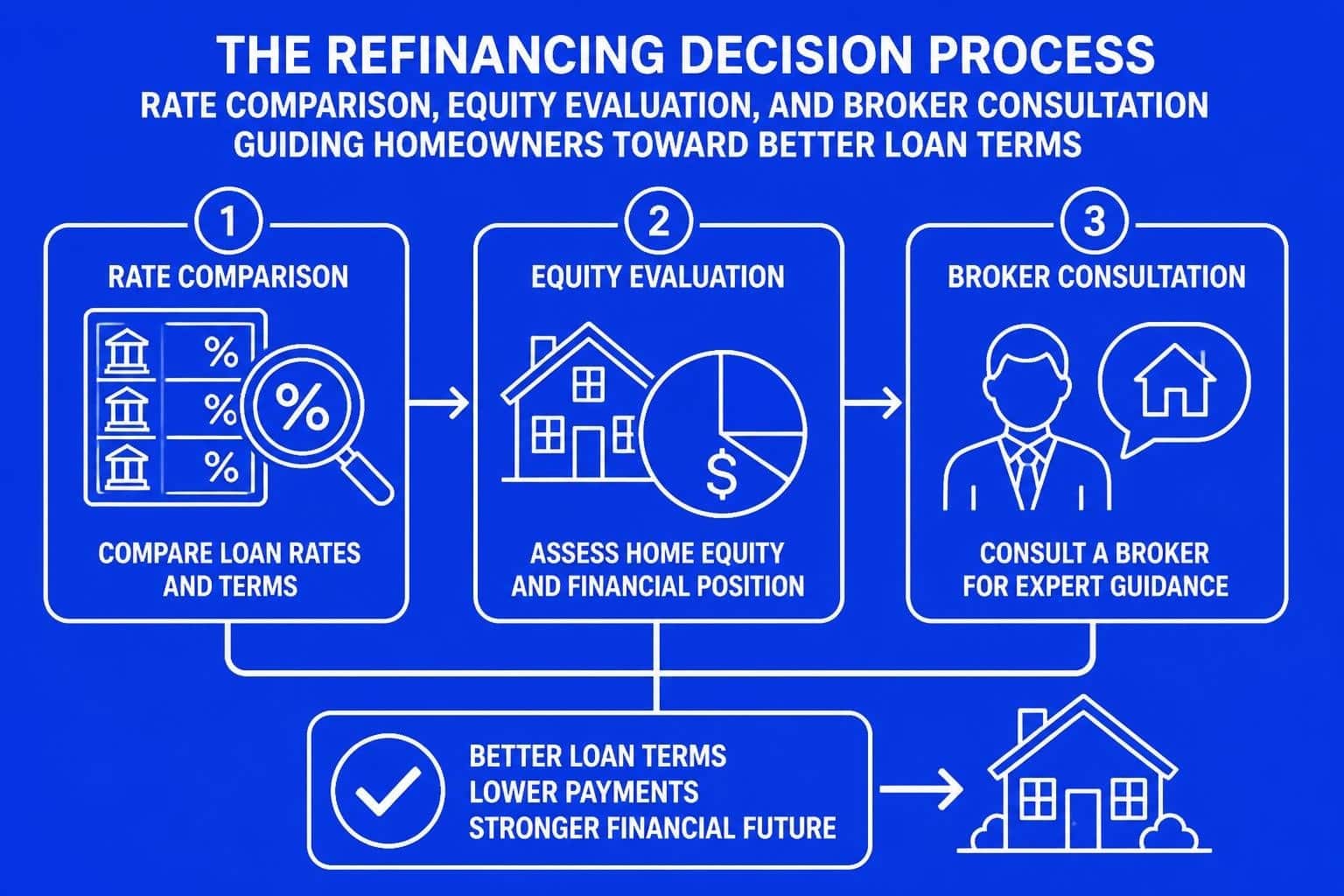

Your relationship with your first home buyer broker doesn’t end at closing. Brokers offer ongoing support, such as guidance on refinancing, market updates, and homeownership resources.

Many first home buyer brokers provide access to home ownership education resources, helping you maximize your investment and plan for future needs. They’re available to answer questions about maintenance, taxes, or even your next property purchase.

This extended partnership highlights the true value of working with a first home buyer broker, ensuring you’re prepared for every stage of homeownership.

Key Trends and Tips for First Home Buyers in 2026

Navigating the 2026 real estate market requires more than just enthusiasm—it demands insight and adaptability. Savvy buyers recognize that working with a first home buyer broker can be the key to unlocking the best opportunities, especially as new trends and regulations shape the path to homeownership. Let’s explore what you need to know to stay ahead.

Technology and Digital Tools

The homebuying process in 2026 is more digital than ever before. First home buyer broker platforms leverage AI-driven mortgage pre-approvals that deliver results in minutes. Virtual home tours and augmented reality apps allow buyers to explore properties remotely, saving valuable time and energy. Secure mobile apps streamline document uploads, communication, and status tracking, making each step efficient and transparent. By partnering with a first home buyer broker who uses these tools, buyers gain a major edge in a fast-moving market.

Regulatory Changes and Lending Standards

Staying informed about regulatory updates is crucial for success in 2026. Changes to FHA, VA, and conventional loan requirements mean eligibility and documentation standards may shift year to year. New consumer protection laws aim to safeguard buyers from predatory practices, while enhanced disclosure rules provide greater clarity on fees and terms. A first home buyer broker remains up-to-date on these changes, guiding clients through the maze of compliance and ensuring access to the most advantageous loan products.

Market Dynamics: Rates, Inventory, and Competition

Interest rates and housing supply continue to shape the buyer experience. In 2026, rates are projected to fluctuate, directly impacting affordability and monthly payments. Inventory remains tight in many regions, fueling competitive bidding and swift sales. According to the Housing Affordability Index Report, first-time homebuyer monthly payments have risen, underscoring the need for smart financial planning. A first home buyer broker helps clients interpret these trends, identify the right timing, and structure winning offers.

Down Payment Assistance and Incentives

Securing enough funds for a down payment is a common hurdle. Fortunately, 2026 brings expanded state and federal assistance programs, as well as local grants for first-time buyers. A first home buyer broker is adept at uncovering these opportunities, matching clients with programs that fit their financial profile. Brokers can also explain eligibility criteria and help navigate application processes, making homeownership more attainable for those with limited savings.

Sustainable and Energy-Efficient Homes

Demand for green, energy-efficient homes is on the rise. Buyers in 2026 are increasingly interested in properties with solar panels, efficient appliances, and eco-friendly certifications. Mortgage lenders offer incentives for sustainable upgrades, and a first home buyer broker can help clients find homes that qualify for these benefits. By focusing on long-term efficiency, buyers can reduce utility costs and increase their property’s value over time.

Avoiding Common Mistakes

First-time buyers often face pitfalls such as skipping pre-approval, underestimating closing costs, or failing to compare lenders. A first home buyer broker offers critical guidance, helping clients sidestep these errors. Through education, careful preparation, and proactive communication, brokers ensure buyers understand each step and make informed decisions, reducing the risk of costly surprises.

Building Long-Term Wealth Through Homeownership

Homeownership is a powerful wealth-building tool. In 2026, first-time buyers can leverage home equity for future investments, whether through refinancing or acquiring additional properties. A first home buyer broker provides ongoing support, offering insights into market shifts, refinancing strategies, and investment opportunities. This partnership empowers buyers to not only secure their first home but also lay the foundation for long-term financial growth.

You’ve just explored how a first home buyer broker can turn the challenges of 2026’s real estate market into real opportunities—from understanding your financial readiness to navigating the ins and outs of the mortgage process with a trusted expert by your side. If you’re ready to take the next step or still have questions about your unique path to homeownership, I invite you to connect directly. We can talk through your goals, discuss your options, and make sure you have the personalized support you deserve on your homebuying journey. Let’s have a conversation