Navigating the Seattle housing market as a first-time buyer presents unique challenges in 2026, from high home prices to competitive bidding situations. Understanding your first time home owners loan options can make the difference between feeling overwhelmed and confidently moving forward with one of the biggest financial decisions of your life. The good news is that numerous programs exist specifically to help buyers like you overcome common barriers like down payment requirements, credit concerns, and income limitations. This guide breaks down the most effective loan options, eligibility requirements, and strategic considerations for first-time buyers across Seattle, Shoreline, Lynnwood, and surrounding communities.

Understanding First Time Home Owners Loan Programs

A first time home owners loan isn't a single product but rather a category of mortgage programs designed specifically for buyers who haven't owned a home in the past three years. These programs typically offer more favorable terms than conventional mortgages, including lower down payment requirements, reduced interest rates, and assistance with closing costs.

The definition of "first-time homebuyer" is more flexible than many people realize. If you haven't owned a primary residence in the last three years, you generally qualify. Single parents who previously owned a home only with a former spouse also meet the criteria, as do individuals who only owned property that wasn't permanently affixed to a foundation.

Key Benefits of First-Time Buyer Programs

- Lower down payment requirements (as low as 0-3.5%)

- Reduced mortgage insurance premiums in some cases

- Down payment assistance grants and forgivable loans

- Seller concessions allowed up to 6% in many programs

- Gift funds accepted from family members

- Flexible credit requirements compared to conventional loans

These advantages significantly reduce the cash needed to close and can accelerate your timeline from renting to owning, particularly important in markets like Bellevue and Redmond where home prices continue climbing.

FHA Loans: The Most Popular First Time Home Owners Loan

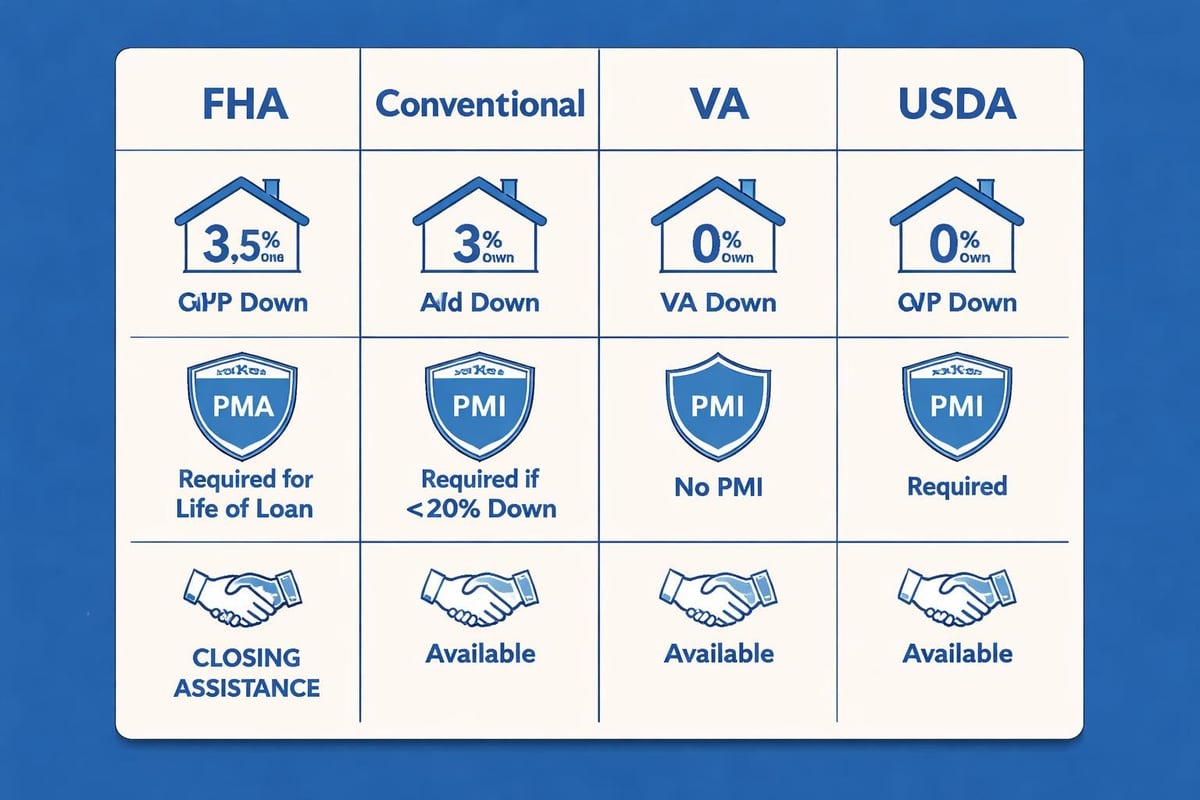

Federal Housing Administration (FHA) loans remain the most common choice for first-time buyers in the Greater Seattle area. With a minimum down payment of just 3.5% and credit score requirements as low as 580, FHA loans provide accessible entry points into homeownership.

For a $600,000 home in Shoreline, you would need $21,000 down plus closing costs. However, FHA allows you to receive gift funds from family members for your entire down payment and closing costs, making it possible to purchase with minimal personal savings if you have family support.

| Loan Feature | FHA Requirement | Conventional Comparison |

|---|---|---|

| Minimum Down Payment | 3.5% | 3-5% |

| Credit Score | 580 minimum | 620-640 minimum |

| Debt-to-Income Ratio | Up to 50% with compensating factors | Typically 43-45% |

| Mortgage Insurance | Required for life of loan (if <10% down) | Removable at 20% equity |

| Gift Funds | 100% allowed | Allowed with restrictions |

FHA Loan Considerations for Seattle Buyers

The Seattle-Tacoma-Bellevue metropolitan area has FHA loan limits of $1,063,750 for single-family homes in 2026, well above the national baseline. This higher limit reflects our elevated housing costs and allows first-time buyers to access FHA financing even in more expensive neighborhoods.

One important factor to understand is FHA mortgage insurance. You'll pay an upfront mortgage insurance premium (1.75% of the loan amount) that can be rolled into your loan, plus annual mortgage insurance premiums that typically range from 0.55% to 1.05% depending on your down payment and loan amount.

Conventional 97 and HomeReady Programs

Conventional loans with just 3% down have gained significant traction among Seattle-area first-time buyers, particularly those with strong credit profiles and stable employment. Fannie Mae's HomeReady program and Freddie Mac's Home Possible program cater specifically to low-to-moderate income buyers.

These programs offer several advantages over FHA loans for qualified buyers. Mortgage insurance on conventional loans can be removed once you reach 20% equity through payments or appreciation. Given Seattle's historical appreciation rates, this can happen relatively quickly and save thousands annually compared to FHA's permanent mortgage insurance requirement.

Income Limits and Property Eligibility

HomeReady and Home Possible loans have income limits based on area median income (AMI). In King County, the limits vary by census tract, but many areas allow incomes up to 100% of AMI, which translates to approximately $137,000 for a single person or $196,000 for a family of four in 2026.

These programs also allow you to count non-borrower household income (like a roommate's income) toward qualification, expanding your buying power without adding that person to the loan and title. This flexibility proves particularly valuable in cities like Lynnwood and Lake Forest Park where buyers sometimes purchase homes with plans to rent out rooms.

Washington State Housing Finance Commission Programs

Washington State offers powerful down payment assistance programs specifically for first-time buyers that can be combined with FHA, conventional, or USDA loans. The Home Advantage program provides down payment assistance through either a deferred second mortgage or lender credits.

The House Key program offers multiple options:

- House Key Home Loan: 30-year fixed rate with competitive pricing

- House Key Plus: Adds up to 5% down payment assistance

- House Key Opportunity: For buyers with lower credit scores (640 minimum)

- House Key Advantage: Combines the base loan with down payment help

Eligibility Requirements for State Programs

To qualify for Washington State housing programs, you must meet income and purchase price limits that vary by county. King County income limits reach $168,600 for households of 1-2 people and $211,575 for larger families in 2026. Purchase price limits top out at $926,350, covering the majority of homes in Mill Creek, Everett, and similar suburban markets.

You'll complete a homebuyer education course (typically 6-8 hours online) before closing, which also satisfies requirements for many other assistance programs and provides valuable knowledge about budgeting, maintenance, and avoiding foreclosure.

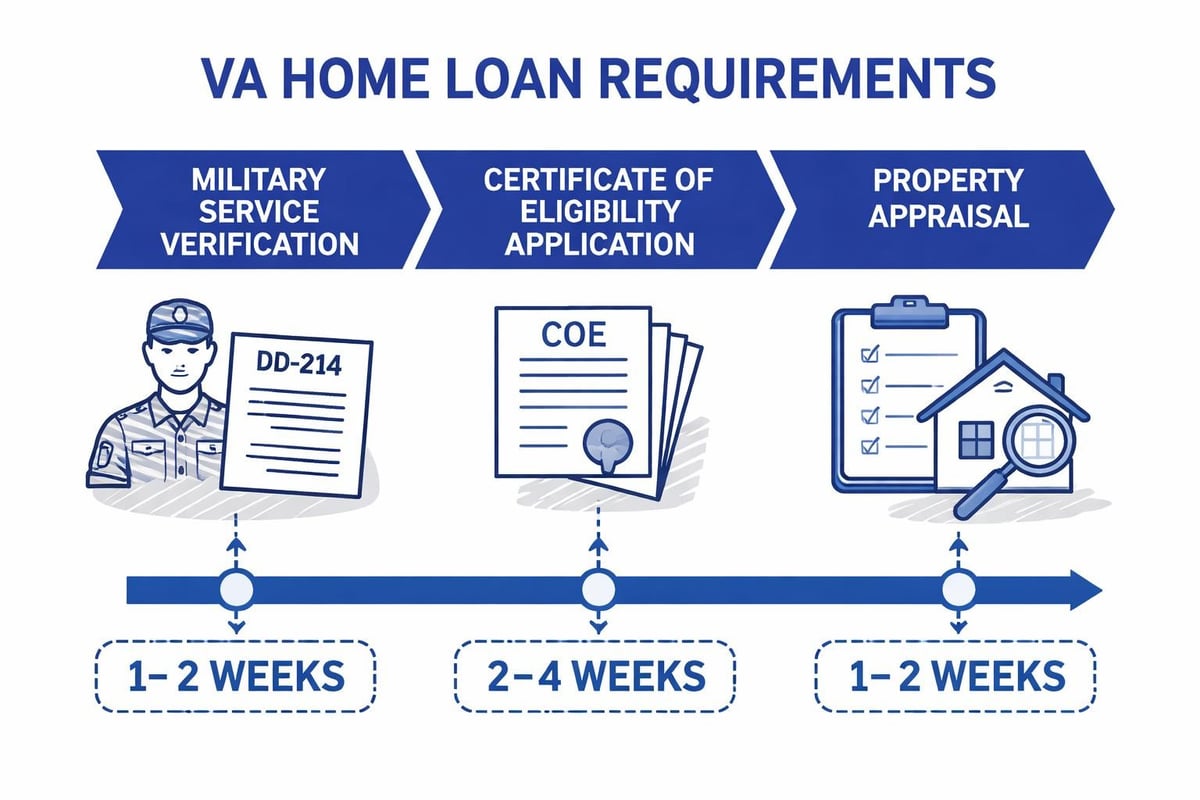

VA Loans for Military Members and Veterans

Veterans Affairs (VA) loans represent perhaps the strongest first time home owners loan option available for those who qualify through military service. VA loans require no down payment, no monthly mortgage insurance, and feature competitive interest rates typically 0.25% to 0.50% below conventional rates.

Eligibility extends to active-duty service members, veterans, National Guard and Reserve members, and certain surviving spouses. You'll need a Certificate of Eligibility (COE) from the VA, which your mortgage broker can often obtain electronically within minutes.

Key VA Loan Advantages:

- Zero down payment required

- No monthly mortgage insurance premiums

- Funding fee (2.3% for first-time use, 3.6% for subsequent use) can be financed

- Lenient credit requirements

- Seller can pay all closing costs

- No prepayment penalties

In the competitive Seattle market, VA loans sometimes face challenges in multiple offer situations due to stricter property condition requirements and appraisal guidelines. However, a skilled mortgage broker can structure your offer to remain competitive while protecting your interests.

USDA Loans for Suburban and Rural Properties

United States Department of Agriculture (USDA) loans offer another zero-down-payment option for first-time buyers purchasing in eligible suburban and rural areas. While most of Seattle proper doesn't qualify, portions of Snohomish County including areas near Everett and Mill Creek fall within USDA-eligible zones.

USDA loans feature low mortgage insurance (0.35% annually), competitive rates, and flexible credit requirements. Income limits apply based on household size and county, with King County limits at approximately $123,800 for a family of four in most eligible areas.

Determining USDA Eligibility

Property eligibility is address-specific and changes periodically as communities grow. The USDA website provides an interactive map where you can verify whether a specific property qualifies. Generally, properties must be in areas with populations under 35,000 and be used as your primary residence.

Down Payment Assistance Programs Beyond State Options

While Washington State programs provide excellent assistance, additional down payment help exists through various channels that can be layered with your primary first time home owners loan.

Many counties and cities offer localized programs. Boston’s assistance programs demonstrate how municipal governments support first-time buyers, and similar initiatives exist in Pacific Northwest communities. Additionally, employer-sponsored programs have grown in 2026, with several Seattle-area tech companies offering down payment grants or forgivable loans to employees.

| Assistance Type | Typical Amount | Repayment Structure |

|---|---|---|

| Forgivable Loan | $5,000-$25,000 | Forgiven after 3-10 years of occupancy |

| Deferred Loan | $7,500-$50,000 | No payments until sale, refinance, or payoff |

| Grant | $2,500-$10,000 | No repayment required |

| Matched Savings | Up to $8,000 | Must save portion, then receive match |

Combining Multiple Assistance Sources

Many buyers successfully combine state assistance with local programs or employer benefits. For example, a Seattle buyer might use a HomeReady loan with 3% down, add House Key Plus for another 5% in assistance, and receive a $10,000 employer grant, effectively purchasing a $600,000 home with minimal out-of-pocket expense.

Your mortgage broker should analyze all available options and structure your financing to maximize benefits while ensuring you qualify under all program guidelines. Some assistance programs restrict what other help you can receive simultaneously, requiring careful coordination.

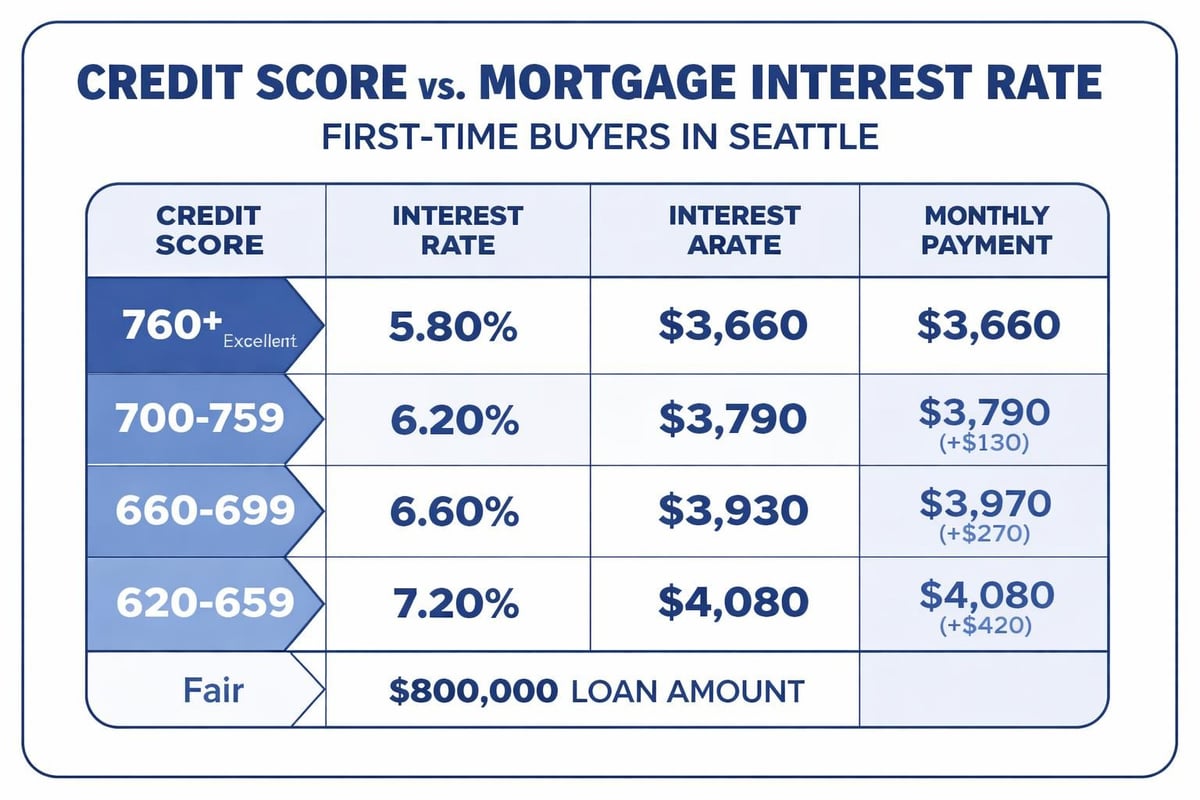

Credit Score Requirements and Improvement Strategies

Credit scores significantly impact both your ability to qualify for a first time home owners loan and the interest rate you'll receive. Different loan programs have varying minimum requirements, but higher scores always provide better terms.

Minimum Credit Scores by Program:

- FHA: 580 (500-579 requires 10% down)

- Conventional: 620-640

- VA: No official minimum (most lenders require 580-620)

- USDA: 640

- HomeReady/Home Possible: 620

If your score falls below these thresholds, specific strategies can improve it within 60-90 days:

- Pay down credit card balances below 30% of limits (ideally below 10%)

- Dispute inaccurate items on your credit report through all three bureaus

- Become an authorized user on a family member's well-managed account

- Avoid new credit inquiries in the months before applying

- Pay all bills on time without exception

A 40-point credit score improvement can reduce your interest rate by 0.50% or more, saving over $200 monthly on a $500,000 loan and making the difference between approval and denial.

Calculating How Much House You Can Afford

Understanding your maximum purchase price prevents disappointment and focuses your home search appropriately. Lenders evaluate your debt-to-income ratio (DTI), which compares your monthly debt payments to gross monthly income.

Most first time home owners loan programs allow DTI ratios up to 43-50%, though staying below 43% provides more flexibility and financial breathing room. Calculate your front-end ratio (housing payment only) and back-end ratio (all debts including housing).

Seattle-Specific Affordability Considerations

Given Seattle's high cost of living, buyers should factor property taxes (approximately 0.92% of assessed value in King County), homeowners insurance ($1,200-$2,400 annually), and HOA fees if applicable. A $650,000 home in Redmond might require these monthly payments:

- Principal & Interest (6.5% on $630,250): $3,982

- Property Tax: $498

- Insurance: $150

- HOA: $200

- Mortgage Insurance: $315

Total Housing Payment: $5,145

To qualify with a 43% back-end DTI and no other debts, you'd need monthly gross income of approximately $11,965 ($143,580 annually). If you have a $500 car payment and $200 in student loans, you'd need $13,570 monthly income ($162,840 annually).

Qualifying Stock Compensation and Tech Industry Income

Seattle's concentration of tech employers creates unique opportunities for first-time buyers who receive stock-based compensation. Amazon, Microsoft, Google, and other major employers grant RSUs (Restricted Stock Units), stock options, and performance bonuses that can be used to qualify for larger loan amounts.

Most mortgage programs allow you to count RSU income after it vests, typically requiring a two-year history or documentation of future vesting schedules. The calculation method varies by loan type. Conventional loans often average the last two years of stock income, while FHA may use a more conservative approach.

Maximizing Tech Income for Qualification

Working with a mortgage broker experienced in tech compensation proves critical. At Mortgage Reel, we specialize in structuring files to maximize stock income while meeting investor guidelines. This expertise often increases buying power by $100,000-$200,000 compared to brokers unfamiliar with these income sources.

If you're early in your career with limited stock income history, strategies exist to bridge the gap. Some buyers delay purchase by 6-12 months to establish two years of vesting history. Others use only base salary for initial qualification, then refinance after stock income history develops, eliminating mortgage insurance through appreciation and increased income documentation.

Pre-Approval: Your First Strategic Step

Getting pre-approved before house hunting provides multiple advantages in competitive markets like Seattle and Kirkland. Pre-approval means a lender has verified your income, assets, and credit, issuing a commitment letter stating the loan amount you qualify for.

Distinguished from pre-qualification (an informal estimate), pre-approval requires documentation including:

- Recent pay stubs (last 30 days)

- W-2s or tax returns (previous two years)

- Bank statements (last 2-3 months)

- Credit authorization

- Employment verification

With proper documentation, experienced brokers can often issue pre-approvals within 24-48 hours, positioning you to act quickly when you find the right property.

Standing Out in Multiple Offer Situations

Pre-approval letters should be tailored to each property, showing the specific purchase price and demonstrating you qualify for that amount. Generic letters for maximum approval amounts appear less serious to sellers. Additionally, pre-approval from a reputable local lender carries more weight than online-only lenders unfamiliar with Pacific Northwest real estate practices.

In Shoreline and Lake Forest Park, where inventory remains tight, some buyers strengthen offers through appraisal gap coverage, showing sellers they'll cover the difference if the home appraises below the contract price up to a certain amount. This strategy requires additional cash reserves but can secure your dream home in competitive situations.

Common First-Time Buyer Mistakes to Avoid

Even well-prepared buyers sometimes make costly errors during the mortgage process. Understanding these pitfalls helps you navigate smoothly toward closing.

Critical Mistakes:

- Changing jobs during the loan process without consulting your lender

- Making large purchases on credit before closing

- Depositing cash without creating a paper trail

- Opening new credit cards that lower your average account age

- Skipping the home inspection to make your offer more competitive

- Draining savings entirely for the down payment without keeping reserves

Lenders verify employment within days of closing. A job change, even to a higher-paying position, can derail your loan if it changes your income structure from salary to commission or if you're in a probationary period. Always consult your mortgage broker before making employment changes during the buying process.

Timeline from Application to Closing

Understanding the mortgage timeline helps you plan your transition from renting to owning. While some lenders advertise 9-day closings with complete documentation, typical first time home owners loan transactions follow this schedule:

- Application to Pre-Approval: 1-3 days

- House Hunting: Variable (typically 4-12 weeks in Seattle area)

- Offer Acceptance to Appraisal Ordered: 1-2 days

- Appraisal Completion: 7-14 days

- Underwriting Review: 3-7 days

- Conditional Approval: Day 10-21

- Final Approval: Day 21-28

- Closing: Day 30-45

Advanced underwriting systems and experienced processors can accelerate this timeline significantly. Some programs offer "clear to close" status in as few as 9 business days with complete documentation upfront, crucial in competitive markets where faster closings strengthen offers.

What Happens at Closing

The closing appointment typically lasts 45-90 minutes and takes place at a title company or escrow office. You'll sign numerous documents including the promissory note (your promise to repay), deed of trust (securing the property), and closing disclosure (detailing all financial terms).

Bring a government-issued ID, cashier's check for closing costs (or arrange wire transfer), and proof of homeowners insurance. Your mortgage broker should review the closing disclosure with you 3-4 days before closing to ensure all numbers match your expectations and no last-minute surprises appear.

Interest Rate Locks and Timing Strategies

Interest rates fluctuate daily based on economic conditions, Federal Reserve policy, and mortgage-backed securities markets. When you apply for a first time home owners loan, you'll typically lock your interest rate for 30, 45, or 60 days depending on your expected closing timeline.

Longer locks sometimes carry slightly higher rates (0.125% to 0.250% more) to compensate lenders for extended interest rate risk. If rates drop significantly after locking, some lenders offer float-down options allowing you to capture lower rates for a fee, though terms vary by lender and program.

2026 Rate Environment and Predictions

As of March 2026, mortgage rates have stabilized after the volatility of recent years. Most first-time buyers receive rates between 6.0% and 7.0% depending on credit score, down payment, and loan program. While these rates exceed the historical lows of 2020-2021, they align with long-term averages and shouldn't prevent qualified buyers from purchasing.

Economic indicators suggest gradual rate declines throughout 2026 as inflation moderates, though dramatic drops appear unlikely. Buyers sometimes ask whether they should wait for lower rates. The answer depends on your personal situation, but remember you can refinance later if rates drop significantly while home prices continue appreciating in strong markets.

Tax Benefits of Homeownership

Beyond the emotional satisfaction of owning your home, significant tax advantages make the first time home owners loan financially attractive compared to renting.

Primary Tax Benefits:

- Mortgage interest deduction on loans up to $750,000

- Property tax deduction up to $10,000 (when combined with state/local taxes)

- Mortgage insurance deduction (subject to income limits and annual Congressional extension)

- Capital gains exclusion ($250,000 single, $500,000 married) when you sell after living there 2+ years

- Energy efficiency credits for qualifying home improvements

For a Seattle buyer with a $600,000 home and $580,000 mortgage at 6.5%, first-year interest totals approximately $37,700. Combined with $5,500 in property taxes, you'll have $43,200 in deductions, potentially saving $10,000-$15,000 in federal and state taxes compared to the standard deduction, though tax benefits should be verified with your accountant based on your specific situation.

Resources for First-Time Buyers Across Multiple States

While this guide focuses on Seattle-area buyers, understanding how other states structure their assistance demonstrates the nationwide commitment to homeownership. Programs like New York City’s HomeFirst offering up to $100,000 in assistance show the scale of support available in high-cost markets.

Similarly, New Jersey’s housing agency and Ohio’s programs provide models that informed Washington State's approach. Even Nebraska’s assistance structure and Florida’s offerings demonstrate consistent themes: reducing down payment barriers, offering education, and making homeownership accessible.

These programs share common elements regardless of location-down payment assistance, educational requirements, income limits based on area median income, and purchase price restrictions reflecting local markets. Understanding these patterns helps you recognize legitimate programs versus predatory schemes.

Working with Real Estate Professionals

Your team significantly impacts your home buying success. Beyond your mortgage broker, you'll work with a real estate agent, home inspector, and potentially an attorney depending on local customs.

Choose a buyer's agent with specific expertise in first-time buyers and the neighborhoods you're targeting. Agents working primarily in Everett and Mill Creek understand different market dynamics than those specializing in urban Seattle condos. Your agent should provide comprehensive comparative market analysis, guide negotiation strategy, and coordinate with your lender regarding timelines and contingencies.

Home inspectors deserve careful selection too. The cheapest inspector often misses critical issues, while thorough professionals identify problems before they become your responsibility. Expect to pay $400-$700 for inspection services on a typical Seattle-area home, with additional charges for specialized inspections like sewer scope or radon testing.

Broker Versus Direct Lender

First-time buyers often ask whether to use a mortgage broker or apply directly with a bank. Brokers access multiple lenders and program options, comparing rates and terms to find your best fit. Direct lenders offer only their proprietary products, which may or may not be competitive for your situation.

Experienced brokers also provide strategic value beyond rate shopping. We understand which underwriters have appetite for specific income types (like stock compensation), which appraisal management companies cause delays, and how to structure files for fastest approval. This expertise proves particularly valuable for complex scenarios common among Seattle tech workers.

Private Mortgage Insurance Explained

If you put down less than 20%, conventional loans require private mortgage insurance (PMI) protecting the lender if you default. Monthly PMI typically ranges from 0.3% to 1.5% annually depending on your down payment, credit score, and loan-to-value ratio.

On a $600,000 home with 5% down ($30,000), your loan amount is $570,000. With good credit, PMI might cost 0.6% annually ($3,420 yearly or $285 monthly). While this increases your payment, it allows you to purchase sooner rather than waiting years to save 20% down while prices and rents continue rising.

Removing PMI

Once your loan balance drops to 80% of the original value through payments or appreciation, you can request PMI cancellation. Given Seattle's historical appreciation (averaging 5-8% annually over the past decade), a home purchased at $600,000 might appraise for $660,000 within two years, reaching 80% LTV and eliminating PMI without additional payments beyond your regular amortization schedule.

Understanding first time home owners loan options positions you to make confident decisions in today's Seattle real estate market, whether you're targeting properties in established neighborhoods or emerging areas like Lynnwood and Lake Forest Park. The combination of low-down-payment programs, state assistance, and strategic mortgage structuring makes homeownership achievable even in our competitive, high-priced market. Keith Akada and the team at Mortgage Reel specialize in helping first-time buyers navigate these programs, leverage stock compensation, and close quickly in competitive situations, backed by 25+ years of experience and 750+ five-star reviews from satisfied clients across the Greater Seattle area.