Are you curious about the home loan approval time in 2026? You are not alone, as approval times are changing quickly with new technology and regulations. Knowing what to expect can help you plan your home buying journey with confidence.

This guide will break down the home loan approval time, highlight what is different in 2026, and give you clear steps to navigate the process. We will explore each phase, from application to closing, and reveal how new trends can impact your experience.

Expect actionable strategies, expert tips, and a roadmap to help you move from application to homeownership smoothly. Let us get started on understanding what shapes your approval journey and how you can take control.

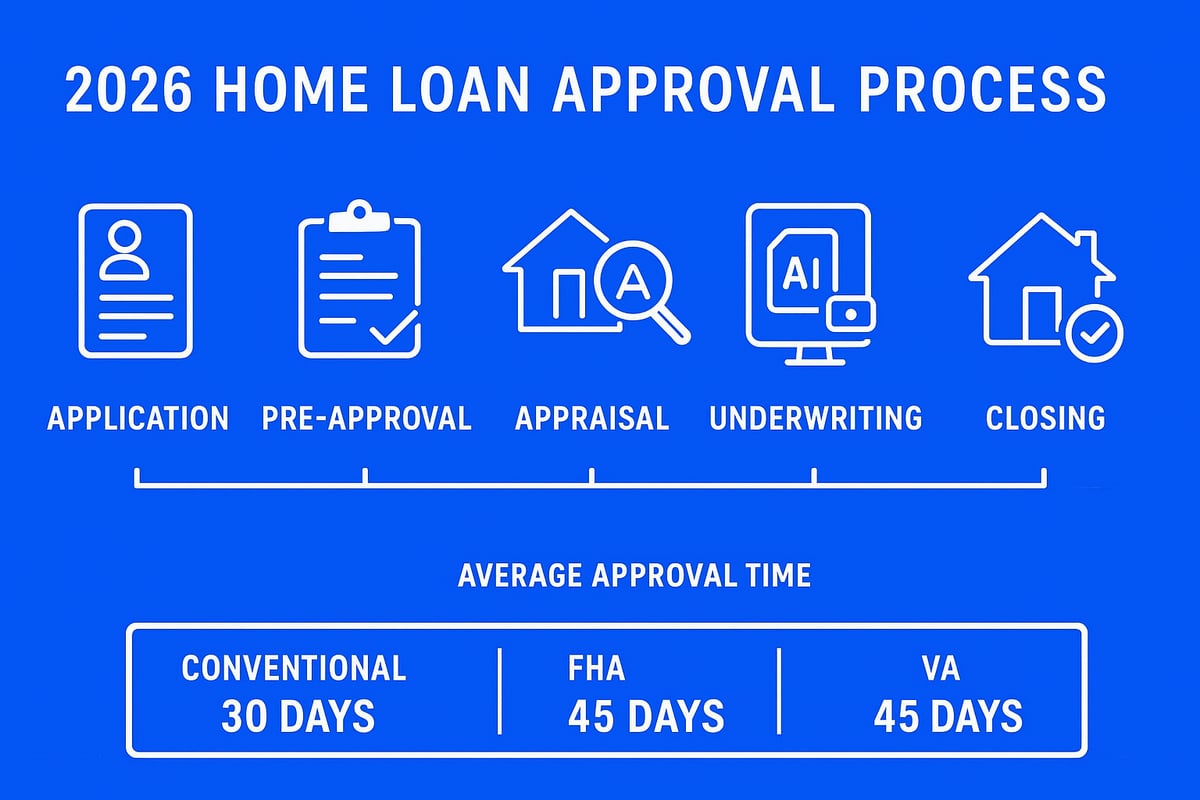

Understanding the Home Loan Approval Process in 2026

Are you curious about how the home loan approval time will look in 2026? The process is evolving, and understanding each step is crucial for a smooth experience. Let’s break down what you need to know for a seamless journey from application to closing.

The Basic Steps: From Application to Closing

The home loan approval time in 2026 typically starts with submitting a digital application and gathering required documents, such as proof of income, assets, identification, and debt details. Pre-approval and pre-qualification are now more distinct, with pre-approval involving deeper credit and income checks.

Lenders conduct credit checks and verify your income, followed by a property appraisal and title search. Underwriting combines automated systems and manual review, streamlining most approvals but still allowing for human oversight when needed. After final approval, you’ll receive closing disclosures and move to the closing stage.

Here’s a simplified timeline for a typical borrower in 2026:

| Step | Estimated Time (Days) |

|---|---|

| Application | 1-2 |

| Pre-Approval | 1-3 |

| Appraisal/Title | 3-5 |

| Underwriting | 2-4 |

| Closing | 1-2 |

For a deeper dive, visit the Understanding home loans process page for detailed guides on each phase.

Key Changes in 2026: What’s New?

In 2026, automation and artificial intelligence are transforming the home loan approval time. Most lenders now use AI-driven underwriting, which accelerates document review and risk assessment. Digital document verification and e-signatures have become standard, eliminating the need for paper forms.

Regulatory updates require tighter compliance checks, but technology helps streamline these steps. Appraisals are faster thanks to Automated Valuation Models (AVMs) and hybrid appraisals. Enhanced data sharing between lenders and agencies reduces back-and-forth delays.

For example, many buyers in 2026 report that AI shaved several days off their approval process, especially when all digital documents are in order. This shift is making the home loan approval time shorter for many applicants.

Typical Approval Timeframes: What to Expect

The average home loan approval time in 2026 continues to improve compared to previous years. Industry data shows that most conventional loans close in 10-15 days, while FHA and VA loans may take slightly longer due to additional checks. Jumbo loans, with their higher value and risk, usually require more scrutiny and time.

Approval times also vary by region. Urban areas with advanced digital infrastructure often see faster processing than rural locations. Other influencing factors include lender workload and seasonal market demand.

Here’s a quick comparison of approval times by loan type:

| Loan Type | Avg. Approval Time (Days) |

|---|---|

| Conventional | 10-15 |

| FHA | 12-18 |

| VA | 14-20 |

| Jumbo | 15-22 |

Understanding these averages helps set realistic expectations for your home loan approval time.

Common Delays and How to Avoid Them

Even with modern tech, some issues can slow your home loan approval time. Common delays include missing or incorrect documentation, unresolved credit issues, and appraisal or property-related problems. Employment or income verification hiccups and compliance red flags can also stall your process.

To avoid these problems:

- Double-check all document submissions for accuracy.

- Resolve credit report errors before applying.

- Stay in regular contact with your lender for updates.

- Respond quickly to requests for additional information.

- Use pre-application checklists to stay organized.

By preparing ahead and staying proactive, you can minimize delays and keep your home loan approval time on track.

Step-by-Step Timeline: The Home Loan Approval Journey in 2026

Navigating the home loan approval time in 2026 means understanding each phase of the process. With new technologies and changing lender requirements, knowing what to expect at every step is essential. Below is a detailed breakdown to help you plan your journey from application to closing.

Step 1: Preparing and Submitting Your Application

The journey begins with gathering all required documentation. In 2026, lenders typically request digital copies of your income statements, tax returns, asset reports, debt summaries, and photo identification.

Most applications are now submitted through secure online portals or mobile apps, making the process faster and more transparent. According to recent reports, the increased use of digital lending tools has significantly reduced the home loan approval time for many borrowers. Completing a pre-application checklist, such as verifying your credit and organizing paperwork, can cut days off your timeline.

Commonly requested documents in 2026:

- Pay stubs and W-2 forms

- Two years of tax returns

- Recent bank statements

- Government-issued ID

- List of debts and monthly payments

Ensuring accuracy and completeness at this stage sets a solid foundation for a smooth process.

Step 2: Pre-Approval and Initial Review

Once your application is submitted, the lender conducts an initial review. In 2026, many lenders use automated pre-approval systems that perform soft credit pulls and instant eligibility checks. This technology speeds up the home loan approval time, providing pre-approval letters within hours in most cases.

Your debt-to-income ratio and credit score remain critical factors during this step. Lenders also verify your employment and assets digitally. In competitive markets, a fast pre-approval can give you an edge when making an offer.

Pre-approval highlights:

- Automated systems for rapid decisions

- Immediate feedback on eligibility

- Digital verification of employment and assets

A strong financial profile and prompt responses to lender queries help maintain momentum.

Step 3: Appraisal, Title, and Property Checks

The next phase focuses on the property itself. Lenders use Automated Valuation Models (AVMs) or hybrid appraisals to quickly estimate property value, which can shave days off the home loan approval time. Title searches and insurance processes are also streamlined with digital platforms.

Despite these advances, potential delays can arise from unresolved title issues or property defects. Integration of appraisal data into underwriting systems ensures faster review and fewer manual steps.

Key property checks:

- AVMs or hybrid appraisals for efficiency

- Digital title search and insurance

- Automated integration with underwriting platforms

Proactive communication with your lender or agent can help resolve issues early.

Step 4: Underwriting and Final Approval

Underwriting is where your full financial profile and property information are reviewed. In 2026, AI handles much of the data analysis, but human underwriters oversee final decisions to ensure compliance. Conditional approvals may require additional documents or clarifications.

The typical turnaround for underwriting has shortened, but the home loan approval time can still vary based on lender workload and case complexity.

Fast-track approval case study:

| Step | Typical Duration (2026) |

|---|---|

| AI Review | 1-2 days |

| Human Oversight | 1 day |

| Conditional Follow-up | 1 day |

Meeting all conditions promptly keeps your loan on track for closing.

Step 5: Closing and Funding

The final step involves signing disclosures, completing a last walkthrough, and disbursing funds. E-signature platforms and remote closing technologies are now standard, enabling many borrowers to close from anywhere.

On closing day, expect a review of final numbers and confirmation of ownership transfer. Staying in close contact with your lender and agent helps ensure the home loan approval time stays on schedule.

Tips for a smooth closing:

- Review closing disclosures in advance

- Schedule your walkthrough early

- Use digital tools for e-signatures

With these improvements, many buyers experience faster, more convenient closings.

Factors Influencing Home Loan Approval Time in 2026

Several variables determine your home loan approval time in 2026. Understanding these factors can help you anticipate challenges and streamline your experience. Let’s break down the key influences shaping timelines this year.

Borrower-Specific Factors

Your personal financial profile has a significant effect on home loan approval time. Lenders closely review:

- Credit score and recent credit activity

- Employment history and current stability

- Income level and documentation

- Down payment amount and source of funds

- Debt-to-income ratio and existing liabilities

A strong financial background often leads to faster processing, while inconsistencies or missing paperwork can add days or even weeks. For example, applicants with steady jobs, high credit scores, and organized records typically move through the process more quickly.

For a deeper dive into how your finances influence timelines, see this guide on factors influencing mortgage approval.

Lender and Loan Program Factors

The lender you choose and the type of loan program both play a direct role in your home loan approval time. Consider these variables:

- Lender workload and staffing levels

- Loan type: conventional, FHA, VA, jumbo, or investor

- Use of automated technology for underwriting

- Whether you pursue pre-approval or direct underwriting

Some lenders offer fast-track programs with digital tools, while others rely on traditional, manual reviews. For instance, a lender with advanced automation may deliver quicker results than one facing high application volumes or staffing shortages.

The specific requirements of each loan program can also impact timelines, especially for specialized products like VA or jumbo loans.

Market and Regulatory Factors

External conditions are another major driver of home loan approval time. In high-demand markets, lenders may experience backlogs, causing delays. Key influences include:

- Overall housing market activity and application volume

- New regulations affecting documentation and compliance checks

- Regional differences in processing speed

- Appraisal and title service bottlenecks

For example, during a hot real estate season, approval times may stretch beyond the average, especially in urban areas with more competition. Regulatory changes, such as updated verification standards, can also introduce new steps that lengthen the process.

Understanding these market forces can help you set realistic expectations and prepare for possible slowdowns.

Technology and Process Improvements

Advancements in digital tools are rapidly shortening home loan approval time in 2026. Here’s how technology is making a difference:

- AI-driven document review and fraud detection speed up verification

- E-closing and remote notarization allow for faster, more convenient closings

- Digital portals enable real-time communication with lenders and agents

- Centralized data sharing among real estate professionals reduces manual errors

Recent statistics show that applicants using digital platforms often close days sooner compared to traditional methods. For example, a borrower submitting documents online and signing electronically could see their home loan approval time cut by up to 30 percent.

Embracing these process improvements ensures a smoother, faster path from application to closing, especially in a fast-evolving mortgage landscape.

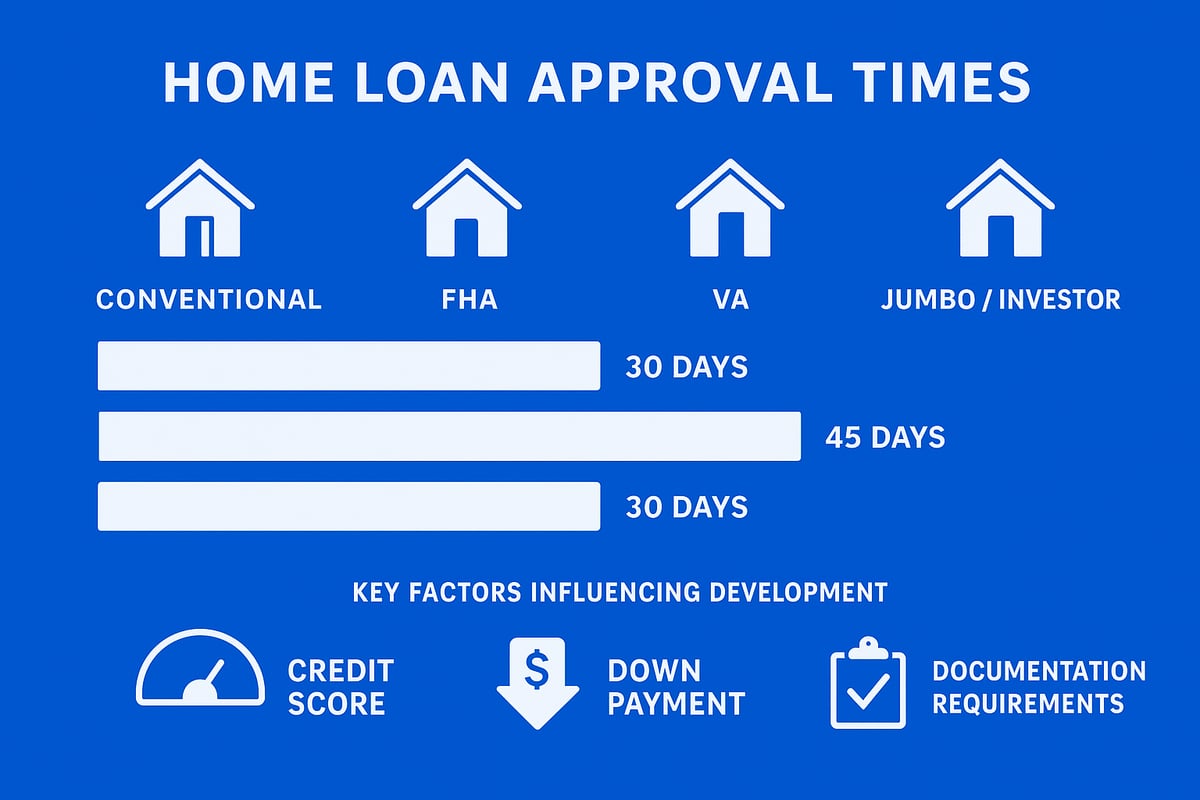

Comparing Home Loan Approval Times by Loan Type

Choosing the right loan can make a significant difference in your home loan approval time. In 2026, the timeline varies not only by lender but also by loan type, documentation, and borrower profile. Understanding these nuances helps you set realistic expectations and plan your next steps.

Below is a quick comparison of average approval times by loan type:

| Loan Type | Typical Approval Time (2026) | Notable Factors |

|---|---|---|

| Conventional | 7-15 days | Fast with strong credit |

| FHA | 10-20 days | Extra compliance checks |

| VA | 12-22 days | Military eligibility verified |

| Jumbo/Investor | 15-30 days | More documentation required |

Conventional Loans

Conventional loans are often the fastest route for well-qualified borrowers. In 2026, the average home loan approval time for conventional loans ranges from 7 to 15 days. Speed is influenced by your credit score, down payment, and the property type.

Borrowers with high credit, stable income, and significant assets often see the quickest approvals. Automated underwriting and instant digital document verification further streamline the process.

For example, a buyer with a 780 credit score, 20% down payment, and a standard single-family home could receive approval in just over a week. This makes conventional loans a preferred choice for many repeat buyers seeking a swift experience.

FHA Loans

FHA loans cater to buyers with lower credit or smaller down payments, but these benefits come with a slightly longer home loan approval time. In 2026, expect timelines of 10 to 20 days due to extra documentation and compliance checks.

Key steps include verifying employment, reviewing debt-to-income ratios, and ensuring the property meets FHA standards. The process is highly regulated and involves more paperwork than conventional loans.

First-time buyers, in particular, should review FHA loan approval insights to understand documentation needs and common timeline factors. For instance, a new buyer with a 650 credit score and 3.5% down payment may see approval in about two weeks if documentation is well-prepared.

VA Loans

VA loans offer unique advantages for veterans and active-duty military, but the home loan approval time can be slightly longer due to eligibility verification. In 2026, approvals typically take 12 to 22 days, depending on how quickly the Certificate of Eligibility is obtained and other required documents are provided.

The process involves confirming military service, reviewing VA-specific appraisal requirements, and ensuring compliance with VA lending guidelines. Digital platforms have helped speed up document collection, but manual checks remain for some steps.

For example, a veteran purchasing in a rural area may experience a 15-day approval, while urban buyers with complete digital files may close even faster.

Jumbo and Investor Loans

Jumbo and investor loans are designed for high-value properties or investment purchases. As a result, the home loan approval time is often the longest, ranging from 15 to 30 days in 2026.

Lenders require extensive documentation, including proof of income, assets, and sometimes multiple appraisals. Underwriting is more rigorous due to the increased risk and loan size.

For example, an investor buying a multi-unit property with complex income streams might wait nearly a month for approval, while a well-documented jumbo borrower could close in just over two weeks. Patience and thorough preparation are key for these loan types.

How to Speed Up Your Home Loan Approval in 2026

Navigating the home loan approval time in 2026 is all about preparation, smart choices, and using the right tools. By following these expert strategies, you can minimize delays and move into your new home faster. Let us break down how you can take control of each step to accelerate your journey.

Proactive Preparation Tips

Starting with strong organization is essential for reducing your home loan approval time. Gather all necessary documents before you apply, such as pay stubs, bank statements, tax returns, and identification.

Create a checklist to ensure nothing is missing:

- Income verification documents

- Asset and debt statements

- Recent credit report

- Government-issued ID

Review your credit report for errors and resolve any issues early. Getting pre-approved before you start house hunting can also speed up the process. An organized approach means fewer surprises and a shorter home loan approval time.

Choosing the Right Lender and Loan Program

Your choice of lender can have a significant impact on your home loan approval time. Compare lenders based on their technology, approval speeds, and customer service.

Consider these factors:

- Does the lender offer digital applications and fast pre-approval?

- Are they experienced with your preferred loan type?

- How strong is their communication and local market knowledge?

Selecting the best loan program for your situation, such as conventional or FHA, also influences the timeline. Remember, a lender with efficient processes can help you achieve a faster home loan approval time.

Leveraging Technology for Faster Approvals

Embracing digital tools is a proven way to cut down your home loan approval time. Use lenders that offer secure online portals for document uploads, e-signatures, and instant status updates.

Respond quickly to any lender requests and track your application’s progress online. According to recent trends, homebuyers’ increased use of digital lending tools has led to faster pre-approvals and smoother closings.

Tech-savvy buyers often report shorter wait times from application to funding. By staying engaged and leveraging technology, you can streamline your home loan approval time.

Working with Experienced Professionals

A skilled mortgage broker or real estate agent can be your greatest ally in reducing home loan approval time. These professionals anticipate potential issues and resolve them before they become major delays.

Benefits of working with experts:

- Professional guidance through complex paperwork

- Early identification of red flags

- Faster responses from lenders and other parties

For example, a broker-assisted application can help you navigate lender requirements efficiently, leading to a quicker home loan approval time. Partnering with the right team keeps your process on track.

The Future of Home Loan Approvals: Trends to Watch Beyond 2026

The landscape of home loan approval time is set for dramatic changes beyond 2026. Innovations in technology, evolving regulations, shifting consumer expectations, and new industry challenges will all play crucial roles. Understanding these trends now can help you anticipate what lies ahead and make informed decisions when applying for a mortgage.

AI and Automation Innovations

Artificial intelligence is rapidly transforming how lenders assess risk and process applications. By 2027, predictive analytics and machine learning models are expected to handle most routine verifications, reducing manual review and accelerating home loan approval time.

Some lenders are piloting fully digital, end-to-end processing platforms that can approve qualified borrowers in as little as 24 hours. According to industry experts, this shift not only speeds up decisions but also minimizes errors. For more on how these changes impact the mortgage industry, see AI’s impact on mortgage underwriting efficiency.

Borrowers will benefit from faster approvals, though human oversight remains essential for complex cases.

Regulatory and Compliance Changes

Regulatory updates will continue to influence home loan approval time beyond 2026. Lenders must adapt to evolving privacy, security, and anti-fraud standards, which can impact how quickly loans are processed.

One significant change is the adoption of modern credit scoring models like VantageScore 4.0 and FICO 10T. These provide a more nuanced assessment of borrower risk, potentially leading to faster and fairer decisions. For details on these regulatory shifts, visit FHFA’s adoption of modern credit scoring models.

Compliance systems will become smarter, using real-time data checks to streamline approvals while keeping the process secure.

Consumer Experience and Expectations

Borrowers are demanding more transparency and speed in the mortgage process. The rise of mobile-first applications and digital dashboards is shaping new standards for home loan approval time.

Instant notifications, real-time status tracking, and interactive support are becoming the norm. Surveys indicate that most buyers in 2026 expect updates within hours, not days. Lenders responding to these expectations are seeing higher satisfaction rates and fewer abandoned applications.

As digital experiences improve, expect approval times to continue shrinking, making the process less stressful and more predictable.

Potential Challenges and Opportunities

While technology and process improvements promise faster home loan approval time, risks remain. Over-reliance on automation could lead to data errors or missed red flags, highlighting the need for balance between speed and thoroughness.

Opportunities exist for lenders and buyers to collaborate, sharing data securely and resolving issues early. Industry analysts predict that by 2027, the most successful lenders will be those who combine cutting-edge tools with expert human guidance.

Staying informed and proactive will help both borrowers and professionals thrive in this evolving landscape.

Now that you understand the factors shaping home loan approval times in 2026 and how new technologies can accelerate your journey, you might be wondering what your unique timeline could look like. Every homebuyer’s situation is different, and getting tailored guidance can make all the difference—especially with changing regulations and evolving loan options. If you’d like clear answers and a personalized strategy for your home financing goals, I invite you to Let’s have a conversation. Together, we can chart the fastest and most confident path to your new home.