A home loan officer serves as your primary guide through one of the most complex financial transactions you'll ever make: securing a mortgage. Whether you're purchasing your first condo in Seattle, refinancing a single-family home in Shoreline, or exploring jumbo financing options in Bellevue, the expertise of a skilled loan officer can make the difference between a smooth closing and a stressful ordeal. Understanding what these professionals do, how they differ from other mortgage industry roles, and what qualifications separate exceptional advisors from average ones will help you make informed decisions in today's competitive real estate market.

What a Home Loan Officer Does

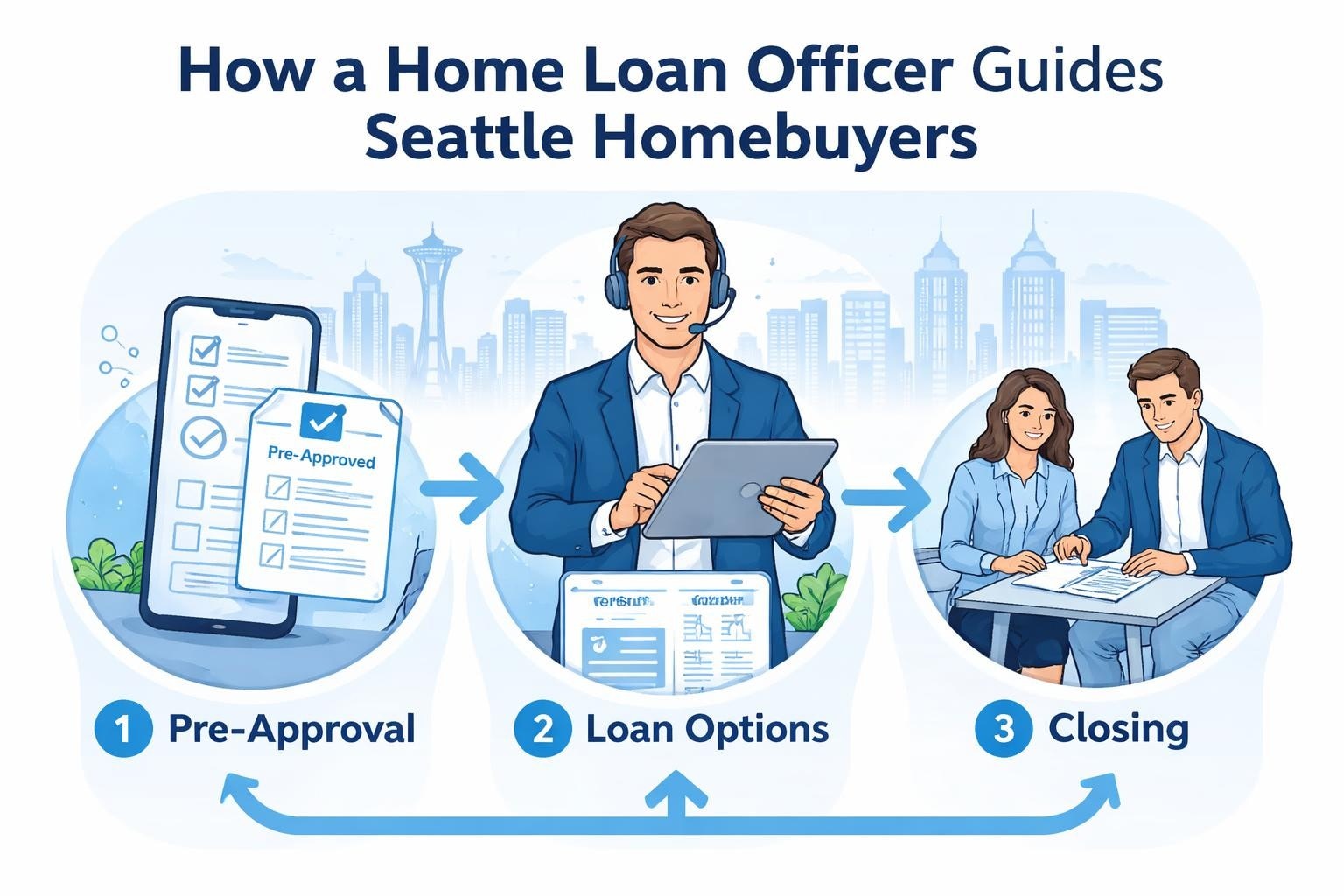

A home loan officer operates as your advocate and advisor throughout the mortgage process, connecting you with appropriate financing solutions based on your financial profile, property type, and long-term goals. These licensed professionals work directly with borrowers to evaluate income, assets, credit history, and debt obligations, then recommend loan products that align with specific circumstances.

The role extends far beyond simply processing applications. A qualified home loan officer educates clients about conventional loans, FHA financing, VA benefits, USDA programs, and specialized products like jumbo mortgages or bank statement loans. In markets like Seattle and surrounding communities such as Lynnwood and Mill Creek, where tech professionals often have complex compensation structures, experienced loan officers understand how to properly document and qualify restricted stock units (RSUs), stock options, and performance bonuses.

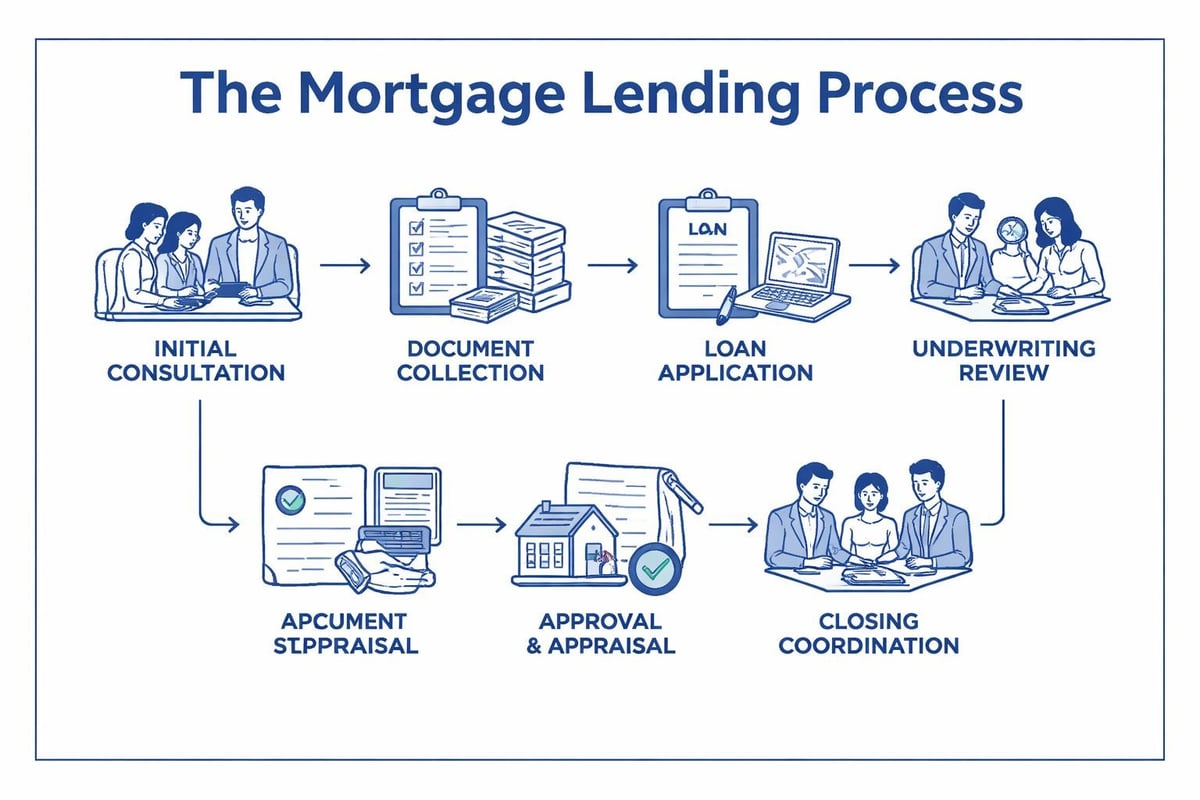

Core Responsibilities Throughout the Loan Lifecycle

Pre-qualification and Pre-approval Phase:

- Analyzing borrower financial documents including pay stubs, tax returns, and bank statements

- Running credit reports and explaining how scores impact interest rates and loan options

- Calculating debt-to-income ratios to determine maximum purchasing power

- Issuing pre-approval letters that strengthen offers in competitive markets

Application and Processing Phase:

- Collecting comprehensive documentation required by underwriting guidelines

- Submitting complete loan files to processing and underwriting teams

- Responding to conditions and requests for additional documentation

- Coordinating with appraisers, title companies, and escrow officers

Closing and Post-Closing Support:

- Reviewing final loan terms and closing disclosures with borrowers

- Ensuring all parties meet closing timelines

- Addressing last-minute questions or concerns

- Maintaining relationships for future refinancing or purchase needs

How Home Loan Officers Differ from Mortgage Brokers

Understanding the distinction between a home loan officer and a mortgage broker helps you choose the right professional for your situation. A home loan officer typically works directly for a specific lender, whether a large bank, credit union, or mortgage company. They offer loan products exclusively from their employer's portfolio, which may limit options but often provides streamlined processing and competitive rates.

Mortgage brokers, by contrast, work with multiple lenders and can shop your application across various institutions to find optimal terms. This flexibility proves particularly valuable for borrowers with unique financial situations, such as self-employed individuals in Seattle or real estate investors purchasing properties in Everett.

| Factor | Home Loan Officer | Mortgage Broker |

|---|---|---|

| Lender Access | Single institution | Multiple lenders |

| Product Variety | Limited to company offerings | Broader selection |

| Processing Speed | Often faster (in-house) | May vary by chosen lender |

| Compensation | Salary plus commission | Commission-based |

| Relationship Continuity | Long-term with one company | Access to changing lender networks |

Many borrowers in Lake Forest Park and surrounding areas find success working with loan officers at established mortgage companies that combine the personalized service of a dedicated professional with access to diverse loan programs through their lending platform.

Essential Qualifications and Licensing Requirements

Every legitimate home loan officer must obtain specific licenses and meet regulatory standards before working with borrowers. The Nationwide Multistate Licensing System (NMLS) requires completion of 20 hours of pre-licensing education, passing the SAFE Mortgage Loan Originator Test, and completing comprehensive background checks including credit and criminal history reviews.

Becoming a licensed loan officer involves several critical steps that ensure professionals understand federal lending laws, ethical standards, and technical mortgage knowledge. Washington State maintains additional requirements beyond federal minimums, reflecting the complexity of lending in markets like Seattle where property values often exceed conforming loan limits.

Ongoing Education and Professional Development

Licensed loan officers must complete eight hours of continuing education annually to maintain their credentials. This requirement ensures professionals stay current on:

- Changes to qualified mortgage rules and ability-to-repay standards

- Updates to government-backed loan programs (FHA, VA, USDA)

- Evolving underwriting guidelines from Fannie Mae and Freddie Mac

- New technology platforms and digital mortgage solutions

- Fair lending practices and compliance requirements

The most effective loan officers go beyond minimum requirements, pursuing designations like Certified Mortgage Planning Specialist (CMPS) or specialized training in complex income documentation for tech employees common throughout Seattle's Eastside communities.

Key Skills That Separate Exceptional Loan Officers

Technical knowledge of guidelines represents just one component of effective mortgage lending. The daily responsibilities of loan officers demand a unique combination of analytical capabilities, communication skills, and problem-solving abilities that directly impact client outcomes.

Communication and Education:

Exceptional loan officers translate complex mortgage concepts into clear, actionable information. When working with first-time buyers in Shoreline, this means explaining the difference between principal, interest, taxes, and insurance components of monthly payments. For experienced investors in Mill Creek, it involves analyzing cash-out refinance scenarios and discussing tax implications.

Financial Analysis and Problem-Solving:

Strong loan officers quickly identify potential obstacles before they derail transactions. If a self-employed borrower's tax returns show business deductions that reduce qualifying income, skilled professionals can suggest alternative documentation methods or timing strategies to improve approval odds.

Attention to Detail:

Mortgage underwriting scrutinizes every aspect of a borrower's financial profile. Small documentation errors or missing signatures can delay closings by weeks. The best loan officers maintain meticulous files and catch issues before submission.

Market Knowledge:

Understanding local real estate dynamics helps loan officers serve clients more strategically. Knowing that Seattle's competitive market often requires escalation clauses and appraisal gap coverage enables better pre-approval conversations and realistic budget setting.

Compensation Structure and Career Outlook

Most home loan officers earn income through a combination of base salary and commission based on loan volume. The typical compensation model rewards productivity while providing stable income during slower market periods. In high-cost markets like Seattle, experienced loan officers with established referral networks can earn substantial incomes, though performance varies significantly based on market conditions and individual effort.

The mortgage industry operates cyclically, with refinance volume heavily dependent on interest rate fluctuations. Purchase lending remains more stable, particularly in supply-constrained markets like Seattle and surrounding cities where housing inventory consistently falls short of demand. Loan officers who build diverse client bases serving both purchases and refinances tend to maintain steadier production across economic cycles.

Career Growth Opportunities

Successful loan officers can advance into several directions:

- Team Leadership: Managing junior loan officers and support staff

- Branch Management: Overseeing office operations and recruiting

- Specialized Lending: Focusing on niches like jumbo loans, investment properties, or physician mortgages

- Executive Roles: Moving into regional or national leadership positions

Many professionals appreciate the flexibility and relationship-driven nature of mortgage lending, choosing to remain in origination roles throughout their careers while continuously expanding their client base and expertise.

Questions to Ask When Choosing a Home Loan Officer

Selecting the right loan officer significantly impacts your mortgage experience and potentially your long-term financial outcomes. Before committing to work with a professional, ask strategic questions that reveal their experience, processes, and value proposition.

Experience and Expertise Questions

How long have you been originating mortgages, and how many loans do you close annually?

Volume and longevity indicate established systems and market knowledge. A loan officer closing 100+ transactions yearly typically has refined processes and strong lender relationships that benefit clients.

Do you specialize in certain loan types or borrower profiles?

Specialists often provide deeper expertise. If you're a tech employee with RSU compensation working in Seattle, a loan officer experienced in documenting stock-based income offers significant advantages over generalists unfamiliar with equity compensation structures.

Can you provide recent client references or reviews?

Consistent five-star feedback across multiple platforms (Google, Zillow, Yelp) demonstrates reliable service quality. Pay particular attention to comments about communication, problem-solving, and meeting timelines.

Process and Communication Questions

What's your typical response time for questions and updates?

Clear expectations about availability prevent frustration. Some loan officers respond within hours; others may take a full business day. Neither is inherently wrong, but knowing upfront helps you plan accordingly.

How do you handle challenges that arise during underwriting?

The answer reveals problem-solving approach and transparency. Strong loan officers proactively address potential issues and present solutions rather than simply reporting problems.

What technology do you use for document collection and loan tracking?

Modern platforms enable secure document uploads, electronic signatures, and real-time status updates. Loan officers still relying heavily on email and paper documents may create unnecessary delays.

Rate and Fee Questions

How do your rates and fees compare to other lenders?

While rates fluctuate daily, loan officers should clearly explain their pricing structure and how closing costs break down. Be wary of anyone unwilling to provide detailed fee worksheets or good faith estimates.

Do you offer rate locks, and what terms are available?

Understanding lock periods (typically 30, 45, or 60 days) and whether extensions incur fees helps you plan your purchase or refinance timeline appropriately.

| Evaluation Criteria | Why It Matters | What to Look For |

|---|---|---|

| Licensing and credentials | Legal compliance and baseline competency | Active NMLS number, clean regulatory history |

| Local market expertise | Relevant guidance for Seattle-area transactions | Familiarity with neighborhood pricing, common appraisal challenges |

| Communication style | Clarity and confidence throughout process | Prompt responses, proactive updates, clear explanations |

| Technology adoption | Efficiency and convenience | Secure portals, e-signatures, mobile accessibility |

| Reviews and reputation | Track record of client satisfaction | Consistent positive feedback across multiple platforms |

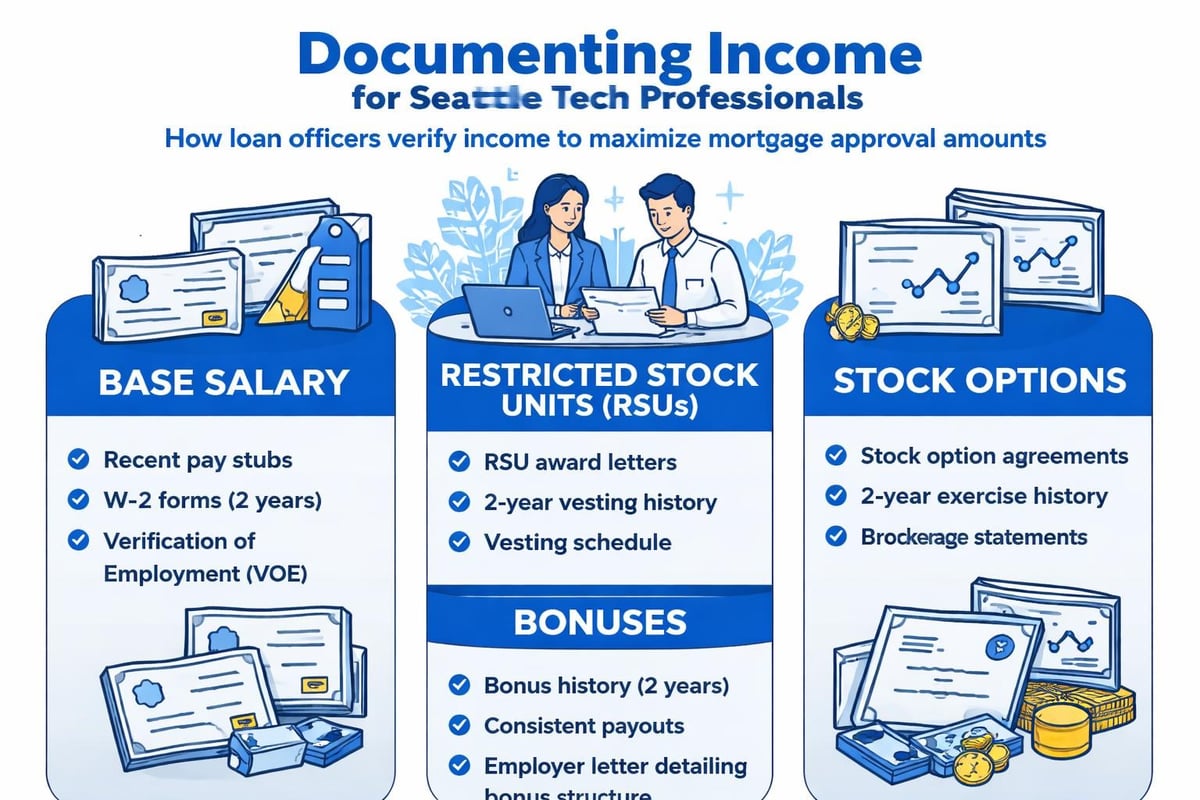

Working with Tech Professionals in Seattle

The Greater Seattle area's concentration of technology employers creates unique mortgage scenarios that require specialized knowledge. Amazon, Microsoft, Google, Meta, and numerous other companies compensate employees with complex packages including base salary, RSUs, stock options, signing bonuses, and performance incentives.

Traditional underwriting guidelines view irregular income skeptically, but experienced loan officers understand how to properly document and qualify these compensation components. For RSUs specifically, most conventional loan programs allow their use in qualifying income calculations once they've vested, though guidelines vary between Fannie Mae, Freddie Mac, and portfolio lenders.

Maximizing Buying Power with Stock Compensation

When evaluating a tech professional's application, skilled loan officers will:

- Review vesting schedules to determine income stability and timing

- Calculate average RSU values over the most recent 12-24 months

- Obtain employment verification letters detailing equity compensation structure

- Work with underwriters who understand technology industry compensation norms

- Explore jumbo loan options when purchase prices exceed conforming limits

For a software engineer in Redmond looking to purchase a $1.2 million home, properly qualifying RSU income might increase purchasing power by $200,000 or more compared to using base salary alone. This documentation expertise directly impacts whether buyers can compete effectively for properties in competitive neighborhoods throughout Seattle and the Eastside.

The Value of Established Lender Relationships

A home loan officer's relationships with underwriters, processors, and closing teams significantly impact transaction smoothness. When loan officers submit clean, complete files with accurate documentation, underwriting teams can work efficiently without excessive condition requests or delays.

Experienced professionals also understand individual underwriters' preferences and interpretation of guidelines. While all lenders follow Fannie Mae and Freddie Mac rules, some apply more conservative overlays while others take reasonable risks on strong files. Knowing which underwriters handle non-traditional income scenarios well, or which processors specialize in quick turnarounds, enables strategic file management.

For borrowers purchasing homes in competitive markets like Lynnwood or Lake Forest Park where sellers often receive multiple offers, the ability to close quickly provides meaningful advantages. Loan officers who can confidently promise 14-day closings (or even faster) based on established lender capabilities and proven execution help buyers win contracts.

Red Flags to Watch When Selecting a Loan Officer

While most mortgage professionals operate ethically and competently, certain warning signs suggest you should continue your search:

Guaranteed approval or rates without financial review:

No legitimate loan officer can promise approval or lock rates before reviewing credit reports, income documentation, and asset verification. Premature guarantees indicate either inexperience or dishonesty.

Pressure to exclude information or misrepresent circumstances:

Ethical loan officers never suggest omitting income sources, understating assets, or mischaracterizing property use. Mortgage fraud carries severe penalties for borrowers and originators alike.

Unclear fee structures or resistance to providing written estimates:

Federal law requires specific fee disclosures within three business days of application. Loan officers who avoid discussing costs or provide vague estimates may be hiding excessive fees.

Lack of availability or poor communication:

If a loan officer is difficult to reach during the shopping phase, expect worse during actual transactions when time-sensitive decisions arise regularly.

No verifiable licensing or poor regulatory history:

Always verify NMLS numbers through the official registry and check for complaints, enforcement actions, or license suspensions.

How Technology Is Transforming the Role

Digital mortgage platforms have dramatically changed how loan officers work with clients. Electronic document collection through secure portals eliminates the hassle of scanning and faxing paperwork. Automated asset verification connects directly to bank accounts, pulling statements without manual uploads. Electronic signatures enable closing documents to be signed remotely, expanding flexibility for busy professionals.

Despite technological advancement, the human element remains central to mortgage lending. Complex income documentation, unique property situations, credit repair strategies, and nuanced guideline interpretation still require experienced professional judgment. The most effective loan officers leverage technology to handle routine tasks efficiently while dedicating their expertise to problem-solving and strategic advice.

For borrowers in Everett or other communities throughout the Seattle metro area, this combination of digital convenience and personal expertise delivers optimal experiences. You can upload documents at midnight from your smartphone, then discuss strategic questions with your loan officer the next morning over coffee.

Industry Trends Shaping the Profession

Several developments are influencing how home loan officers operate in 2026:

Tighter inventory and competitive markets continue pushing buyers toward creative financing solutions, including assumption of existing low-rate mortgages, seller concessions, and alternative down payment structures.

Rising home prices in Seattle and surrounding areas mean more transactions exceed conforming loan limits, requiring jumbo financing expertise that not all loan officers possess.

Remote work flexibility has expanded buyer geographic preferences, with some Seattle-area workers now considering properties in more affordable outlying markets while maintaining occasional office attendance.

Increasing regulation continues adding compliance requirements, particularly around ability-to-repay documentation and fair lending practices, making working with properly licensed and trained professionals more important than ever.

Artificial intelligence and automation are beginning to handle initial qualification assessments and document review, allowing loan officers to focus more on consultation and complex scenario management.

The Importance of Local Market Knowledge

National lenders can process mortgages from anywhere, but loan officers with deep local expertise provide distinct advantages. Understanding Seattle's neighborhood dynamics, typical property tax assessments, common homeowners association structures, and regional appraisal challenges helps anticipate issues before they become problems.

When an appraisal comes in below contract price on a Shoreline home, a loan officer familiar with recent comparable sales can help you evaluate whether to request reconsideration or negotiate with the seller. When reviewing title reports, knowledge of common easement patterns in older Mill Creek neighborhoods prevents surprise delays.

Local expertise also means understanding regional employment patterns. A loan officer who knows that Microsoft typically grants RSUs in August can time refinance applications strategically. Familiarity with Boeing's cyclical employment patterns helps assess job stability for aerospace workers applying for mortgages in Everett.

Building Long-Term Relationships

The best home loan officers view client relationships as long-term partnerships rather than single transactions. Your financial needs evolve over time, and working with the same trusted professional through multiple purchases, refinances, and investment property acquisitions creates efficiency and consistency.

A loan officer who closed your first condo purchase already has your employment history, income documentation patterns, and credit profile on file. When you're ready to upgrade to a larger home in Lynnwood or Bellevue three years later, they can expedite pre-approval and anticipate documentation needs based on prior experience.

This continuity also enables proactive communication. When rates drop significantly, established loan officers reach out to existing clients about refinance opportunities. When new loan programs launch that might benefit your situation, you'll hear about them without having to research independently.

Choosing the right home loan officer impacts not just your immediate transaction, but potentially your long-term financial trajectory through access to appropriate loan products, competitive rates, and strategic timing advice. Whether you're purchasing your first home, refinancing to access equity, or expanding a real estate investment portfolio, working with an experienced professional who combines technical expertise with clear communication and local market knowledge makes the complex mortgage process manageable and efficient. Keith Akada at Mortgage Reel brings over 25 years of mortgage lending experience to Seattle-area homebuyers, specializing in helping tech professionals maximize their buying power through expert qualification of stock compensation and RSU income, backed by 750+ five-star reviews and the ability to close loans in as few as 9 business days.