Shopping for a mortgage in Seattle's competitive real estate market requires more than just looking at interest rates. When you home loans compare, you're evaluating multiple dimensions: loan programs, lender fees, closing timelines, qualification requirements, and long-term financial impact. For buyers in Seattle, Shoreline, and surrounding communities, understanding how to properly compare home loan options can mean the difference between a smooth transaction and costly mistakes. This guide breaks down the essential framework for comparing mortgages with transparency and strategy.

Understanding the Core Elements of Mortgage Comparison

When you home loans compare, you're analyzing several critical components that work together to determine your total cost and monthly obligation. The interest rate captures most attention, but it's only one piece of the equation.

Annual Percentage Rate (APR) reflects the true cost of borrowing by incorporating both the interest rate and lender fees, expressed as a yearly percentage. This makes APR a more reliable comparison tool than interest rate alone. For example, a lender offering 6.5% with $8,000 in fees might have a higher APR than another offering 6.625% with $2,000 in fees.

Key Comparison Metrics

- Interest rate: The percentage charged on the principal balance

- APR: Total borrowing cost including fees and points

- Loan term: Typically 15 or 30 years, affecting monthly payment and total interest

- Down payment requirement: Ranges from 0% (VA/USDA) to 20%+ for conventional

- Monthly payment: Principal, interest, taxes, insurance, and HOA fees

- Total closing costs: Lender fees, third-party services, prepaid items

The Consumer Financial Protection Bureau provides detailed guidance on comparing Loan Estimates, which lenders are required to provide within three business days of your application. This standardized form makes it easier to compare offers side by side.

Major Loan Program Categories in Seattle Markets

The Greater Seattle area offers access to all major loan programs, each serving different buyer profiles and financial situations. Understanding these categories is fundamental when you home loans compare.

| Loan Type | Down Payment | Credit Minimum | Loan Limits (2026) | Best For |

|---|---|---|---|---|

| Conventional | 3-20% | 620+ | $806,500 (Seattle area) | Strong credit, stable income |

| FHA | 3.5% | 580+ | $644,000 (King County) | Lower credit, smaller down payment |

| VA | 0% | No minimum | $806,500 | Veterans, active military |

| USDA | 0% | 640+ | Varies by location | Rural/suburban eligible areas |

| Jumbo | 10-20%+ | 700+ | Above conforming limits | High-value Seattle properties |

Conventional Loans

Conventional mortgages represent the majority of home purchases in Seattle, Bellevue, and Redmond. These loans aren't government-backed, which means underwriting standards focus heavily on credit score, debt-to-income ratio, and employment stability.

For tech professionals at Amazon, Microsoft, or Google headquarters, conventional loans offer flexibility in qualifying stock compensation and bonuses. Different mortgage loan types serve varying needs, but conventional programs typically provide the best rates for borrowers with strong credit profiles.

Down payment requirements start at 3% for first-time buyers, though putting down less than 20% requires private mortgage insurance (PMI). In Seattle's high-cost market, that 20% threshold often exceeds $150,000, making lower down payment options attractive even for well-qualified buyers.

Government-Backed Programs

FHA loans serve buyers in Lynnwood, Mill Creek, and Everett who may have credit challenges or limited savings. The 3.5% down payment requirement and more lenient credit standards make homeownership accessible, though borrowers pay both upfront and ongoing mortgage insurance premiums.

VA loans eliminate the down payment barrier entirely for eligible veterans and service members. With no PMI requirement and competitive rates, VA financing often provides the strongest purchasing power for qualified buyers. In Seattle's competitive market, the ability to offer a strong, zero-down financing package can be decisive.

USDA loans target eligible suburban and rural areas. While Seattle proper doesn't qualify, portions of Lake Forest Park and areas north toward Everett may be eligible depending on population density and median income thresholds.

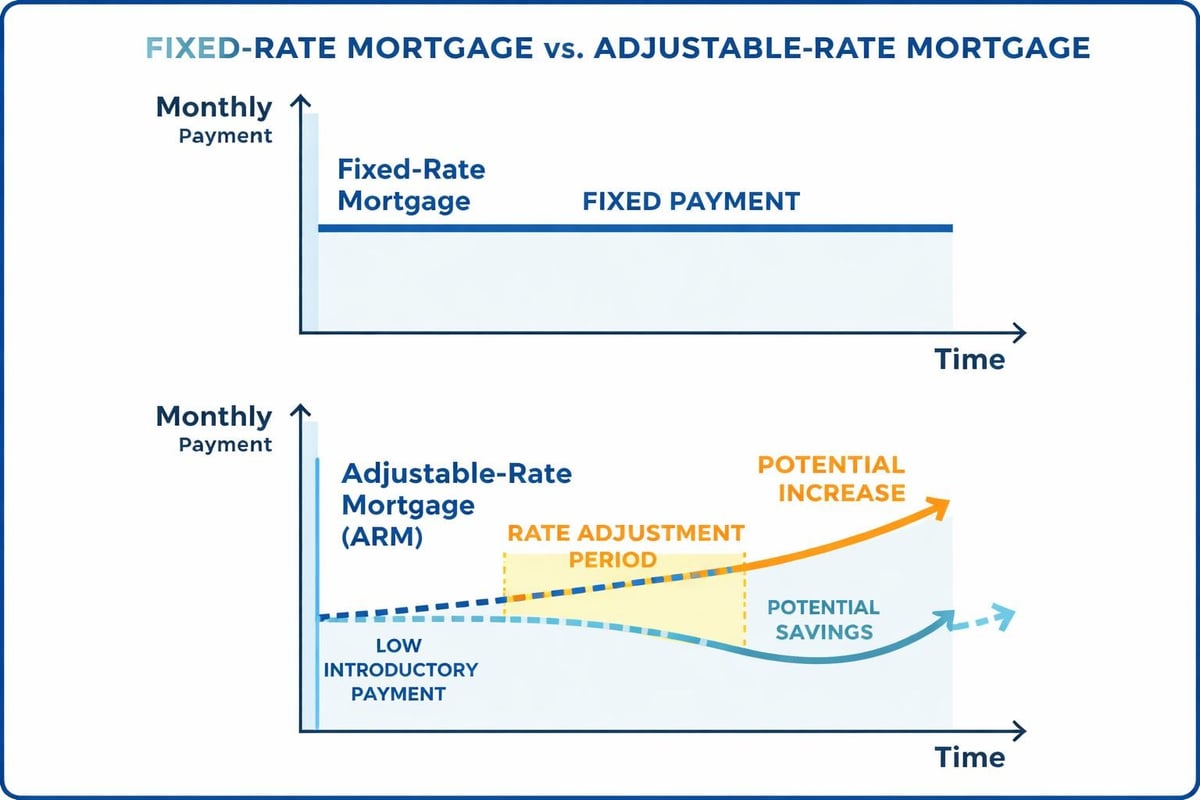

Fixed-Rate vs. Adjustable-Rate Mortgages

Beyond program type, the rate structure fundamentally shapes your financial commitment. This distinction is critical when you home loans compare.

Fixed-rate mortgages lock your interest rate for the entire loan term-typically 15 or 30 years. Your principal and interest payment remains constant, providing predictable budgeting and protection against rising rates. In 2026, with rates stabilizing after recent volatility, many Seattle buyers prioritize this certainty.

Adjustable-rate mortgages (ARMs) start with a lower fixed rate for an initial period (commonly 5, 7, or 10 years), then adjust annually based on market indices. A 7/1 ARM, for instance, maintains its initial rate for seven years before adjusting yearly.

When ARMs Make Strategic Sense

- You plan to sell or refinance before the adjustment period

- The initial rate savings justify the future uncertainty

- You expect income growth to offset potential payment increases

- You're buying in Shoreline or Lynnwood with planned relocation timelines

For a $750,000 purchase in Seattle, the difference between a 6.5% fixed-rate and a 5.875% 7/1 ARM translates to roughly $250 monthly savings during the fixed period. Over seven years, that's $21,000 in reduced payments, which must be weighed against adjustment risk.

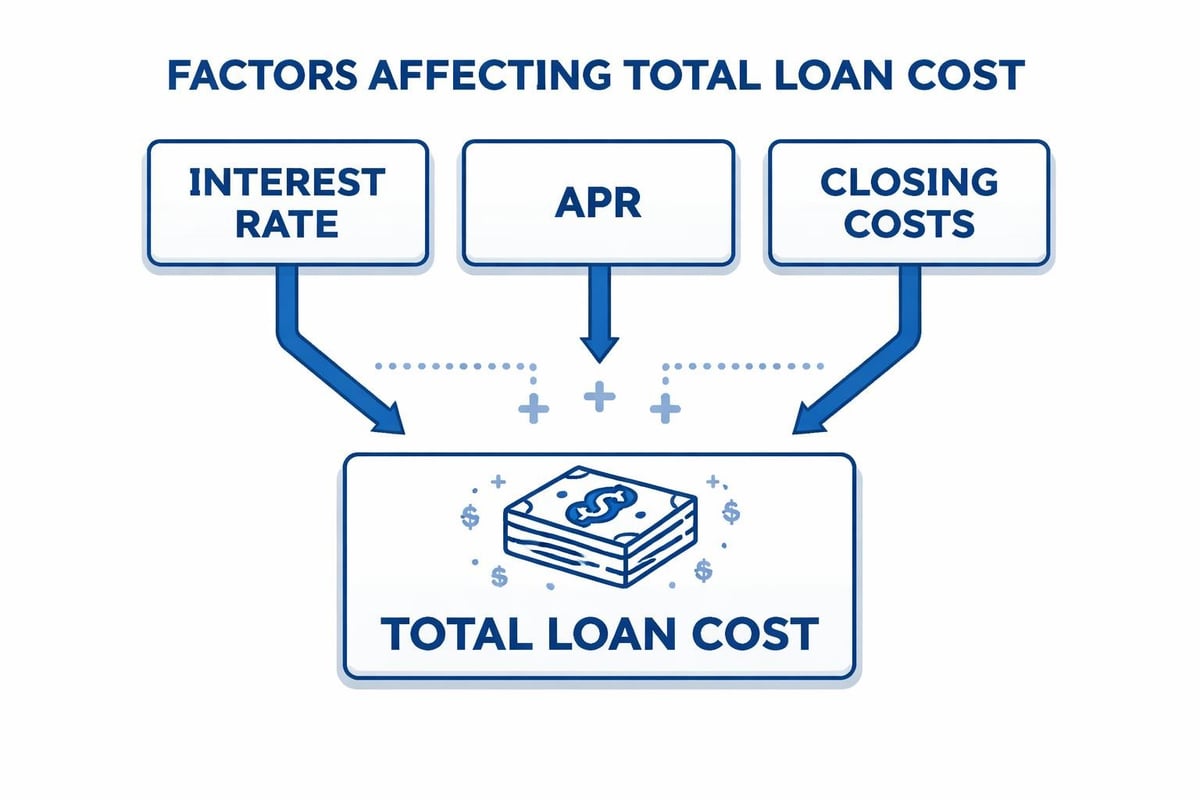

Comparing Actual Loan Estimates

Federal law requires lenders to provide a standardized Loan Estimate within three business days of application. This three-page document is your primary comparison tool and should be the foundation when you home loans compare.

Page One: Loan Terms and Projected Payments

This section details your loan amount, interest rate, monthly principal and interest payment, and whether these can change over time. It also projects your total payment including estimated property taxes, homeowner's insurance, and HOA fees if applicable.

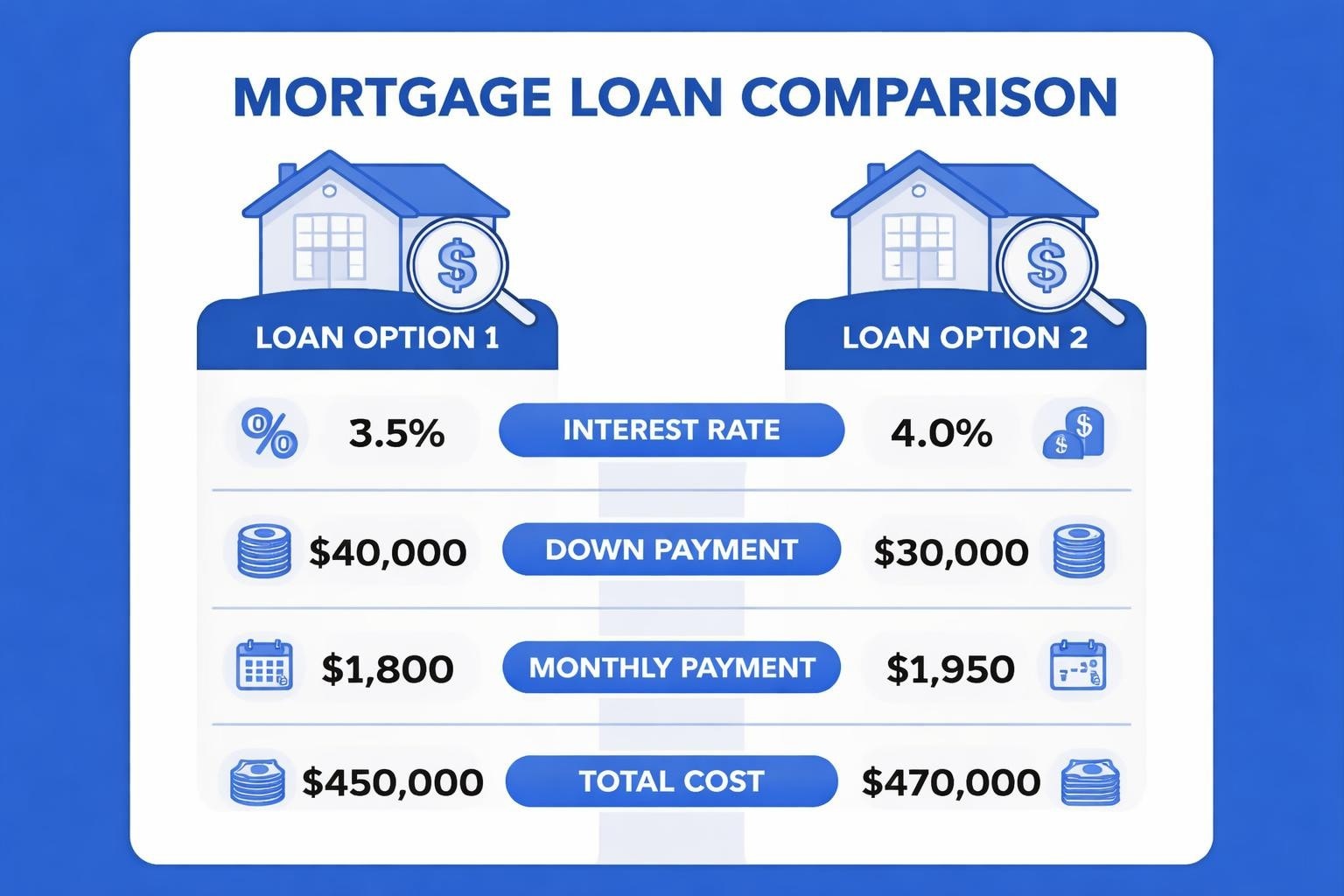

For a $650,000 purchase in Mill Creek with 10% down, you're comparing loan amounts of $585,000. Small rate differences create meaningful long-term impacts:

- At 6.375%: $3,652/month (P&I), $1,314,720 total interest over 30 years

- At 6.625%: $3,760/month (P&I), $1,368,600 total interest over 30 years

- Difference: $108/month, $53,880 over the life of the loan

Page Two: Closing Cost Details

Section B lists origination charges from your lender, while Section C covers third-party services like appraisals, title insurance, and escrow fees. When you home loans compare, focus on Section A (total closing costs) and scrutinize what you can and cannot shop for.

Services you can shop for include title insurance, surveys, and pest inspections. In Seattle and Everett markets, title costs vary significantly between providers-shopping these services can save $500 to $1,500.

Services you cannot shop for are those where the lender requires specific providers. These costs should be competitive but aren't negotiable within that lender's offer.

Page Three: Comparisons and Additional Information

This section shows your total costs over five years (useful for comparison) and your Annual Percentage Rate. It also flags key loan features: prepayment penalties, balloon payments, and whether the loan assumes or negatively amortizes.

Rate Locks, Points, and Fee Structures

Understanding how lenders price their loans is essential for meaningful comparison. Most buyers focus exclusively on the interest rate without considering the trade-offs involved.

Discount points allow you to pay upfront fees to reduce your interest rate. One point equals 1% of the loan amount and typically reduces your rate by 0.25%. On a $600,000 loan, one point costs $6,000.

Whether points make sense depends on your break-even timeline:

- Calculate the monthly payment savings from the lower rate

- Divide the point cost by the monthly savings

- The result is how many months until you recover the upfront cost

If you're paying $6,000 to save $85/month, your break-even is 71 months (nearly six years). If you plan to sell or refinance within five years, paying points costs more than it saves.

Rate locks guarantee your interest rate for a specified period, typically 30 to 60 days. In volatile markets, extended locks provide security but may carry fees. For buyers in competitive Seattle neighborhoods with quick closing timelines, shorter locks often suffice.

Qualifying Power Across Loan Programs

Your purchasing power varies significantly across loan types. When you home loans compare, you're also comparing how much home you can afford under each program's guidelines.

Debt-to-income (DTI) ratios measure your monthly debt obligations against gross income. Maximum DTI varies by loan type:

- Conventional: 43-50% depending on compensating factors

- FHA: 43-50% with strong credit or automated approval

- VA: No strict maximum, but residual income requirements apply

- Jumbo: Typically 43%, sometimes 38% for larger loans

For a household earning $15,000/month gross in Bellevue or Redmond, a 43% DTI allows $6,450 in total monthly debt. If you carry $800 in car and student loans, you have $5,650 available for housing (PITI).

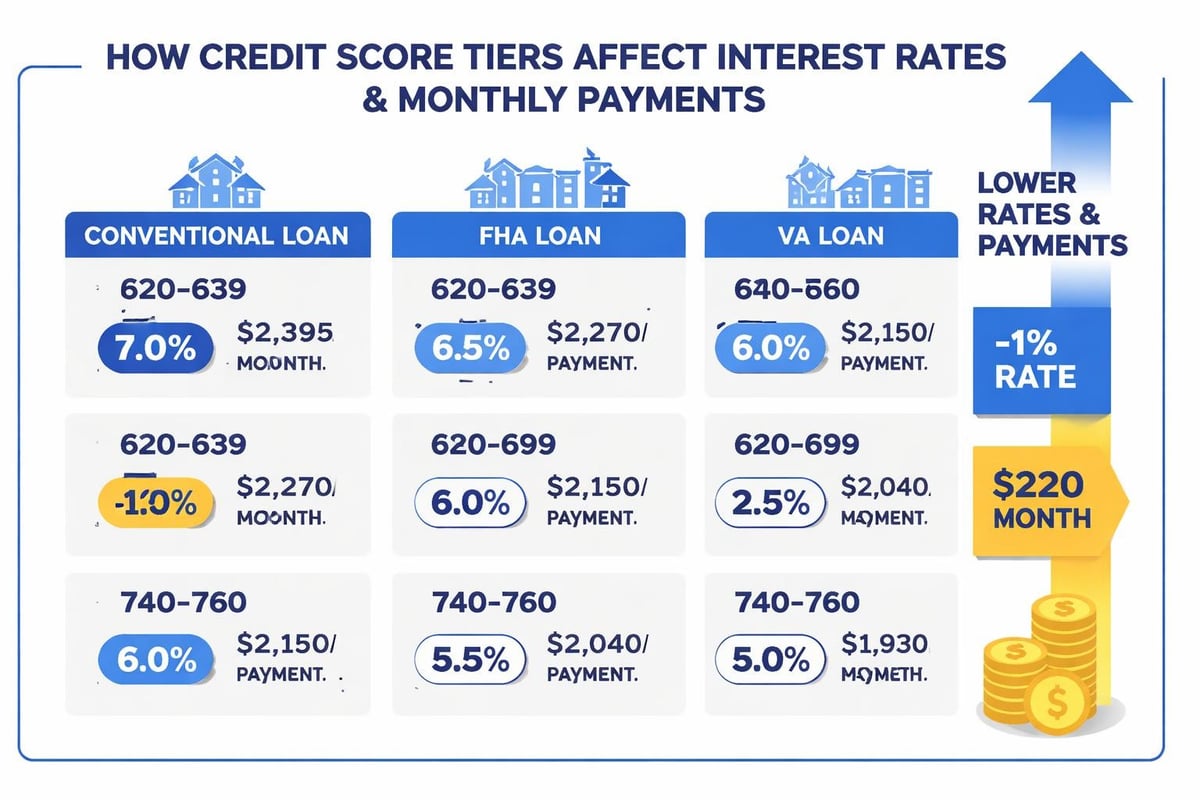

Credit Score Impact on Pricing

Your credit score directly affects your interest rate, especially with conventional loans. The difference between a 680 and 740 score might be 0.50% to 0.75% in rate, translating to significant monthly and lifetime costs.

| Credit Score | Rate Adjustment | Monthly Impact ($600K loan) | 30-Year Cost |

|---|---|---|---|

| 760-850 | Base rate | $0 | $0 |

| 700-759 | +0.25% | +$90 | +$32,400 |

| 680-699 | +0.50% | +$185 | +$66,600 |

| 660-679 | +0.875% | +$335 | +$120,600 |

Evaluating Lenders Beyond Rate Sheets

Interest rates and fees matter, but lender capabilities and service quality significantly impact your experience-especially in Seattle's competitive market where properties often receive multiple offers.

Closing timeline can make or break your offer. A lender capable of closing in 15 business days versus 30-45 days provides a competitive advantage. For tech buyers relocating to Shoreline or Lake Forest Park with RSU vesting schedules, timing flexibility matters.

Underwriting expertise with non-traditional income becomes critical for Microsoft and Amazon employees with stock compensation. Not all lenders qualify RSUs, ESPP income, or signing bonuses consistently. Finding a mortgage broker who specializes in these scenarios prevents surprises during underwriting.

Communication and transparency separate smooth transactions from stressful ones. When you home loans compare, interview loan officers about their process, response times, and how they handle challenges. A slightly higher rate with exceptional service often proves more valuable than the lowest rate with poor execution.

What to Ask Potential Lenders

- How many loans do you close monthly in Seattle and surrounding areas?

- What's your average timeline from application to closing?

- How do you handle RSU/stock compensation qualification?

- What happens if my appraisal comes in below purchase price?

- Who will I communicate with throughout the process?

- What technology do you offer for document upload and tracking?

Special Considerations for Seattle-Area Buyers

The Greater Seattle market presents unique scenarios that affect how you should home loans compare.

Jumbo loan requirements apply to loans exceeding $806,500 in 2026. Many homes in Seattle, Bellevue, and Redmond fall into this category. Jumbo programs typically require larger down payments (often 20%), higher credit scores (700+), and lower debt-to-income ratios. However, rates on jumbo loans sometimes match or even beat conforming rates when you qualify.

Condo financing in Seattle high-rises requires additional lender review of the building's financial health, insurance coverage, and owner-occupancy ratios. Some lenders avoid condos entirely, while others specialize in them. When comparing loans for a Seattle condo, verify the lender's experience with condo projects and their specific requirements.

Stock compensation strategies for tech professionals require lenders who understand how to document and qualify RSUs, bonuses, and ESPP income. The various mortgage programs available have different guidelines, but expertise in applying them to complex income makes the difference.

Mortgage Insurance and Its True Cost

When you put down less than 20%, most loans require mortgage insurance-a monthly premium that protects the lender if you default. The cost and structure vary by loan type.

Conventional PMI ranges from 0.30% to 1.50% of the loan amount annually, depending on your credit score, down payment, and loan-to-value ratio. On a $500,000 loan at 0.75% PMI, you'll pay $312.50 monthly ($3,750 annually). The advantage: PMI automatically cancels when you reach 20% equity through payments or appreciation.

FHA mortgage insurance includes both an upfront premium (1.75% of the loan amount, typically financed) and monthly premiums (0.55% to 1.05% annually). Unlike conventional PMI, FHA insurance remains for the loan's life if you put down less than 10%, requiring refinancing to remove it.

VA funding fees replace mortgage insurance for eligible borrowers. The fee ranges from 1.25% to 3.3% depending on down payment and whether it's your first VA loan. This can be financed into the loan amount, and disabled veterans receive exemptions.

For a $550,000 purchase in Lynnwood with 5% down:

- Conventional: $522,500 loan + $326/month PMI (0.75% rate)

- FHA: $531,638 loan (includes upfront MIP) + $381/month MIP

- VA: $556,875 loan (includes 2.15% funding fee) + $0/month insurance

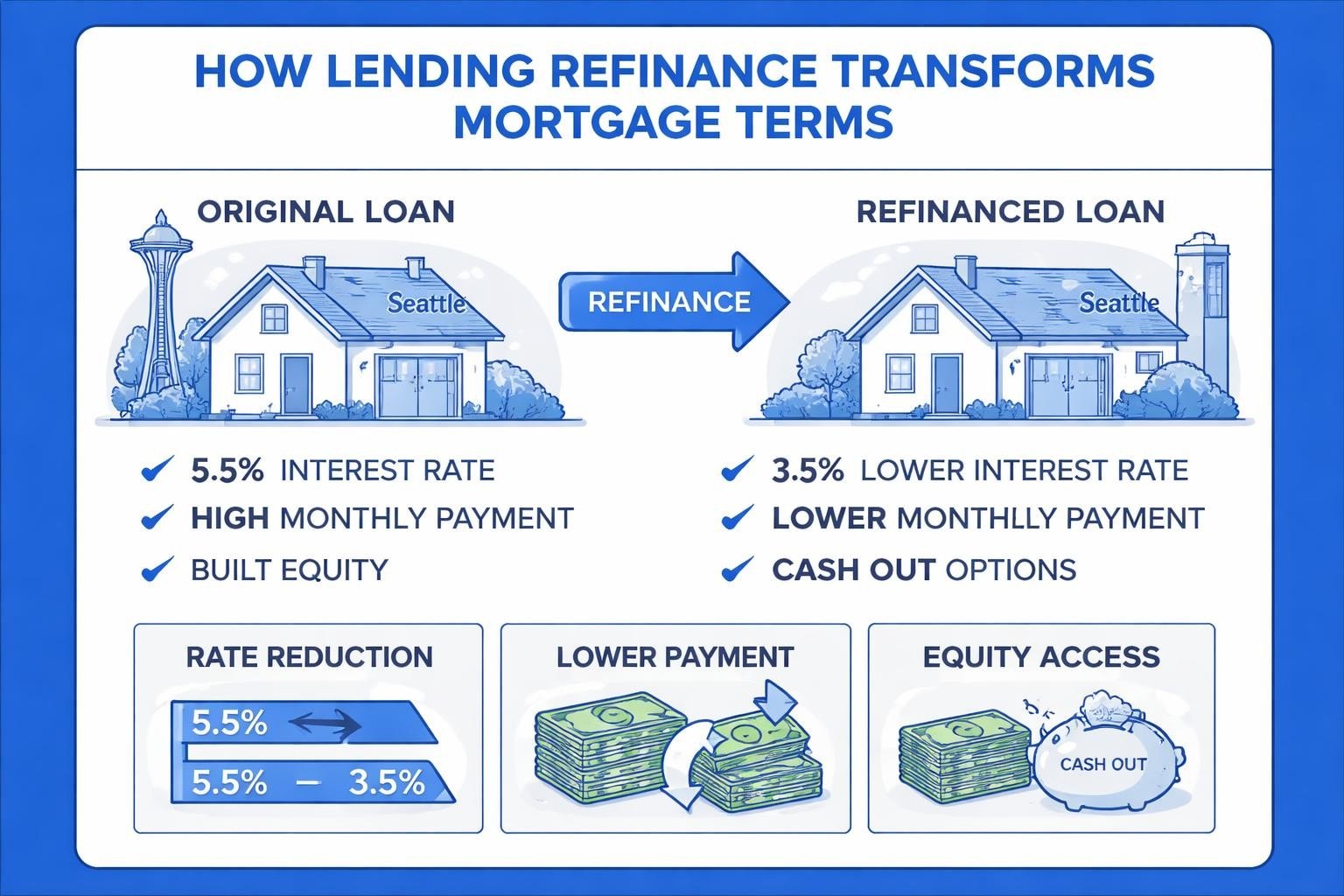

Refinance Comparison Strategies

When you home loans compare for refinancing, the calculation differs from purchase scenarios. You're evaluating whether the savings justify the costs and how long you'll keep the new loan.

Rate-and-term refinances modify your interest rate or loan term. The standard break-even analysis applies: divide closing costs by monthly savings to determine recovery time. If refinancing costs $4,500 and saves $225/month, you break even after 20 months.

Cash-out refinances tap home equity while potentially changing your rate. These loans carry slightly higher rates than rate-and-term refinances and require re-qualification based on your current income and credit.

For Everett homeowners who purchased at 7.0% in 2024, refinancing to 6.25% in 2026 might save $285/month on a $450,000 balance. With $5,000 in closing costs, you break even in 18 months-worthwhile if you plan to stay beyond that timeframe.

Navigating Pre-Approval vs. Pre-Qualification

In competitive markets like Seattle and Bellevue, understanding the distinction between pre-qualification and pre-approval affects your offer strength.

Pre-qualification provides a rough estimate based on information you supply without verification. It's an informal assessment useful for early planning but carries minimal weight with sellers.

Pre-approval involves submitting documentation (pay stubs, tax returns, bank statements) for lender verification and credit checks. The lender issues a commitment letter stating the loan amount, program, and terms you qualify for, subject to finding an acceptable property.

Underwritten pre-approval takes the process further-your financial documents go through full underwriting before you find a property. This represents the strongest financing position and can differentiate your offer in multiple-bid situations common in Shoreline and Mill Creek.

Technology and Digital Mortgage Platforms

The mortgage industry has embraced technology, creating new comparison opportunities and service models. When you home loans compare in 2026, you'll encounter:

Online lenders operate without physical branches, often offering lower rates due to reduced overhead. They provide efficient digital experiences but may lack local market expertise critical in Seattle's unique neighborhoods.

Traditional lenders maintain branch networks and local loan officers who understand regional market dynamics, builder relationships, and title company preferences. Their rates might be slightly higher, but their execution in competitive situations often justifies the difference.

Mortgage marketplaces allow you to submit one application and receive multiple offers. Tools for comparing loan options can simplify the process, though you'll want to verify each lender's reputation and capabilities beyond their rate sheet.

For complex scenarios-stock compensation, self-employment income, multi-unit properties-working with experienced local mortgage professionals typically delivers better outcomes than purely digital platforms.

Common Comparison Mistakes to Avoid

Even informed buyers make errors when comparing mortgages. Recognizing these pitfalls protects you from costly decisions.

Focusing only on interest rate without considering fees, closing timeline, and lender reliability creates false comparisons. A lender offering 6.25% with $12,000 in fees costs more than 6.5% with $3,000 in fees on most loan amounts.

Ignoring the loan type differences leads to inappropriate comparisons. You can't directly compare a conventional loan to an FHA loan without accounting for mortgage insurance structures, qualification requirements, and long-term costs.

Overlooking your timeline causes poor decisions on rate locks, points, and ARM products. If you're relocating from Seattle to another city in three years, paying points on a 30-year fixed-rate mortgage wastes money.

Failing to compare Loan Estimates properly means missing fee discrepancies and cost variations. Use the CFPB’s comparison tools to ensure apples-to-apples evaluation.

Building Your Comparison Framework

Effective mortgage comparison requires a systematic approach. Here's a proven framework for Seattle-area buyers:

- Determine your must-haves: Loan amount, maximum monthly payment, preferred down payment

- Identify appropriate loan types: Conventional, FHA, VA, jumbo based on your situation

- Request Loan Estimates from 3-5 lenders: Include at least one traditional lender and one online option

- Normalize the comparisons: Ensure identical loan amounts, terms, and lock periods

- Calculate total costs: Five-year total cost and lifetime interest for each option

- Evaluate intangibles: Lender reputation, closing speed, communication quality

- Verify final numbers: Review the Closing Disclosure three days before closing

This process typically takes two to three weeks but can save tens of thousands over your loan's life.

Market Timing and Rate Shopping

Interest rates fluctuate based on economic factors, Federal Reserve policy, and bond market movements. When you home loans compare, timing your application and rate lock matters.

Shopping multiple lenders within a 45-day window counts as a single credit inquiry for scoring purposes. This protection allows you to compare offers without damaging your credit score through multiple hard pulls.

Rate volatility in 2026 has moderated compared to 2022-2024, but watching trends helps you time your lock. If rates are trending downward, floating your rate while finalizing your purchase might yield savings. If trending upward, locking early provides protection.

Economic indicators to monitor include employment reports, inflation data, and Federal Reserve announcements. These influence mortgage rates within days of release.

For buyers in competitive Seattle markets, balancing rate shopping with move-in timelines requires strategy. Missing your rate lock expiration can force re-locks at higher rates, negating your careful comparison work.

Documentation Requirements Across Programs

When you home loans compare, understanding documentation needs helps you prepare and qualify efficiently. Requirements vary by loan type and employment situation.

Standard W-2 employees provide:

- Two years of W-2s and tax returns

- Recent pay stubs (30 days)

- Two months of bank statements

- Credit report authorization

Self-employed borrowers need:

- Two years of personal and business tax returns

- Year-to-date profit and loss statement

- Business license and verification

Tech employees with stock compensation require:

- RSU vesting schedules

- Stock award documentation

- History of RSU income (1-2 years)

- Calculation of sustainable income from equity compensation

Working with a mortgage broker experienced in Seattle's tech sector streamlines this process. Incorrect documentation or calculation of stock income can delay closings or reduce qualification amounts significantly.

Comparing home loans effectively requires analyzing multiple dimensions beyond advertised rates-from understanding program structures and fee variations to evaluating lender capabilities and your specific financial situation. For Seattle-area buyers navigating a competitive market with complex income scenarios, partnering with an experienced professional makes this comparison process both more efficient and more accurate. Keith Akada brings 25+ years of mortgage expertise to buyers throughout Seattle, Bellevue, Redmond, Shoreline, and surrounding communities, specializing in stock compensation qualification and fast closings that strengthen your competitive position. Connect with Mortgage Reel to compare your options with transparency and strategic guidance tailored to your unique situation.