Seattle's competitive real estate market consistently pushes home prices beyond conforming loan limits, making jumbo financing a critical tool for buyers across the region. Whether you're purchasing a waterfront property in Seattle, a luxury estate in Bellevue, or a tech-corridor home in Redmond, understanding how jumbo loans work can mean the difference between securing your ideal property or missing opportunities in a fast-moving market. These specialized mortgages serve homebuyers whose financing needs exceed the Federal Housing Finance Agency's conforming loan limits, which for 2026 stand at $806,500 for most single-family homes in King County. As a Seattle mortgage broker with over 25 years of experience, I've helped hundreds of clients navigate jumbo financing successfully, particularly tech professionals whose stock compensation and RSU packages position them perfectly for these larger loan amounts.

What Is Jumbo Financing and When Do You Need It

Jumbo financing refers to mortgage loans that exceed the conforming loan limits established annually by the Federal Housing Finance Agency. In Seattle and surrounding areas like Shoreline, Lynnwood, and Lake Forest Park, these limits determine whether your loan falls into conventional territory or requires jumbo status.

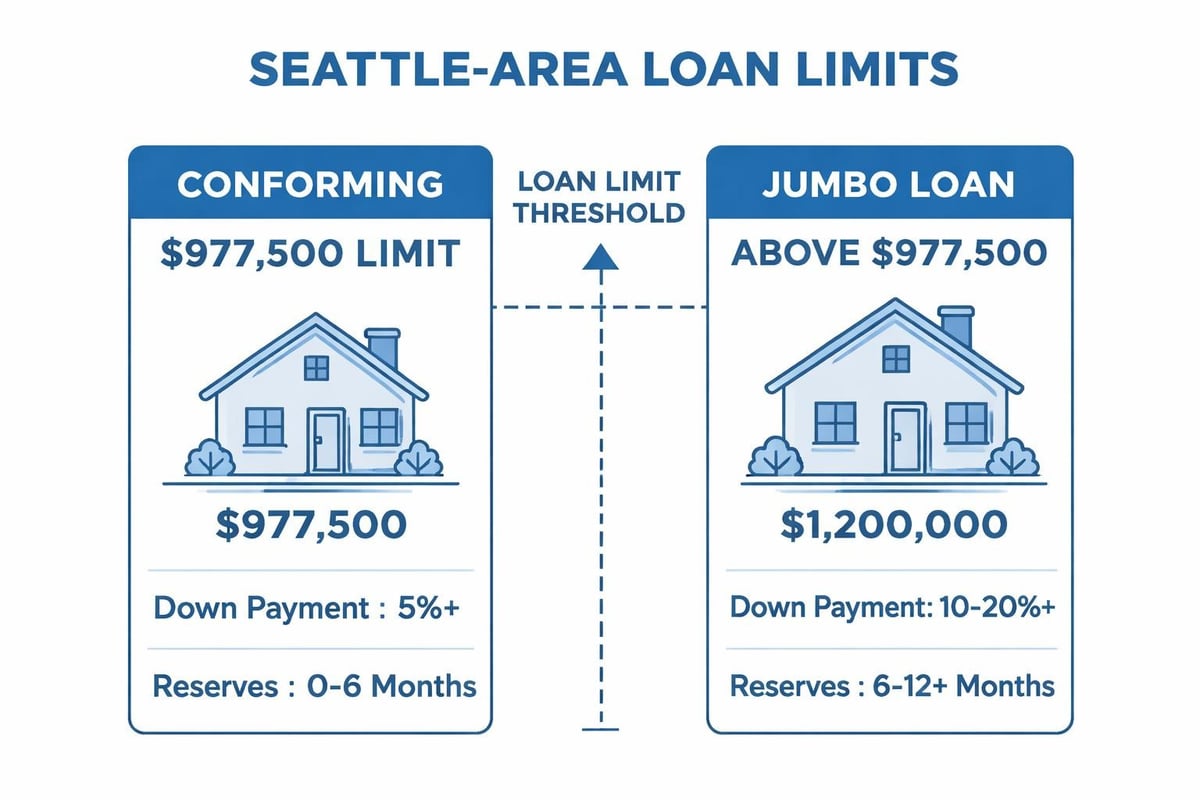

What is a jumbo mortgage loan becomes relevant when your purchase price and loan amount push beyond these thresholds. For 2026, the baseline conforming limit sits at $806,500, though this varies by county. King County qualifies as a high-cost area, but many properties still exceed these caps given Seattle's median home prices.

Understanding Conforming Loan Limits

The distinction between conforming and jumbo loans carries significant implications:

- Conforming loans meet Fannie Mae and Freddie Mac guidelines, allowing lenders to sell these mortgages on the secondary market

- Jumbo loans remain in portfolio or get sold to private investors, creating different risk profiles for lenders

- Limit calculations reflect local housing costs, with annual adjustments based on home price appreciation

When the Federal Housing Finance Agency recently increased conforming loan limits, many borrowers found themselves with more conventional financing options. However, Seattle's robust housing market means jumbo financing remains essential for properties throughout the region.

Seattle Market Context

Seattle's housing landscape makes jumbo financing particularly relevant. Consider these scenarios:

A software engineer at Amazon purchasing a $1.2 million home in Mill Creek needs jumbo financing. A couple upgrading to a $950,000 property in Everett crosses into jumbo territory. An investor acquiring a waterfront home in Seattle proper at $2.1 million definitely requires specialized jumbo products.

Geography matters significantly. While Lynnwood might offer more properties near conforming limits, Seattle and Bellevue inventory frequently demands jumbo solutions. Your financing strategy should account for these regional variations.

Qualification Requirements for Jumbo Loans

Jumbo financing carries stricter qualification standards than conforming mortgages. Lenders assume greater risk with these larger loans, translating into more rigorous approval criteria across multiple dimensions.

Credit Score Expectations

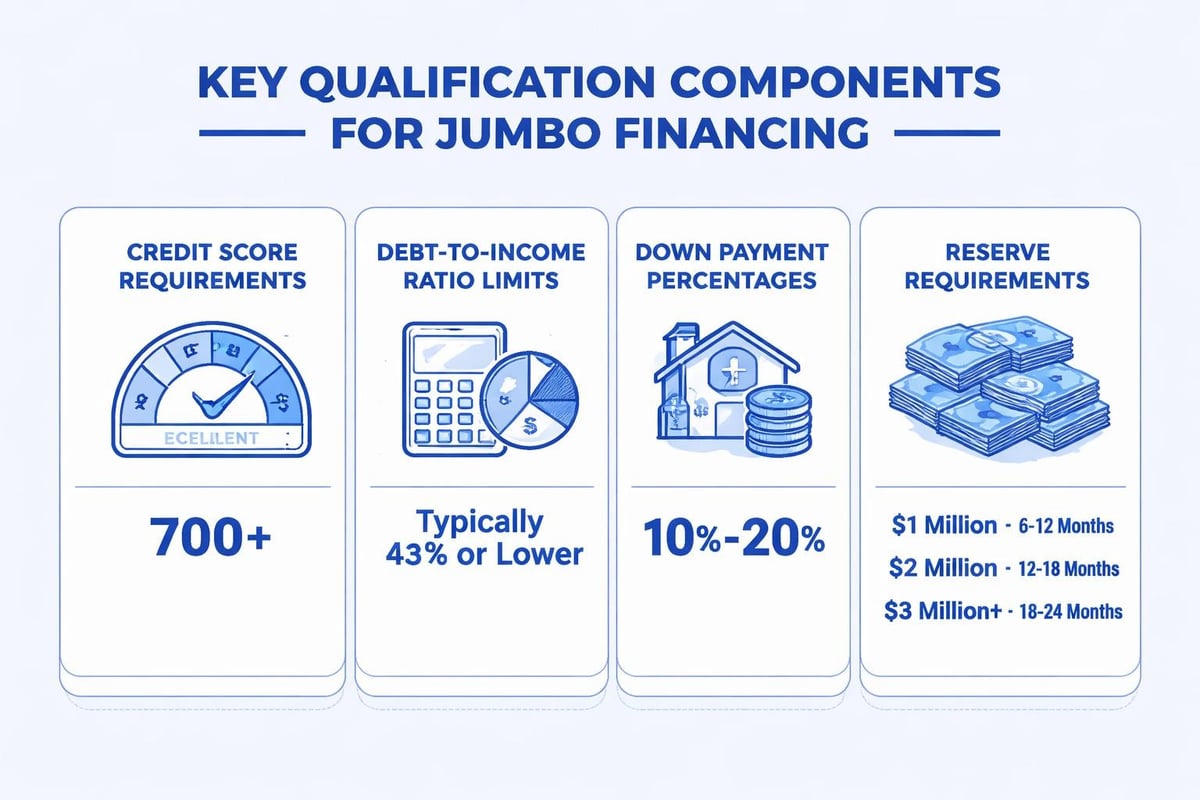

Most jumbo lenders require minimum credit scores between 680 and 720, though competitive rates typically demand 740 or higher. Here's the breakdown:

| Credit Score Range | Likely Outcome | Rate Impact |

|---|---|---|

| 760+ | Best rates, most favorable terms | Baseline pricing |

| 720-759 | Approved with solid profile | 0.125% – 0.25% higher |

| 680-719 | May require compensating factors | 0.25% – 0.50% higher |

| Below 680 | Challenging, limited options | 0.50%+ higher or declined |

Your credit profile extends beyond the score itself. Lenders scrutinize payment history, credit utilization, recent inquiries, and derogatory marks with heightened attention for jumbo financing applications.

Income Documentation and Verification

Jumbo lenders demand comprehensive income verification. For W-2 employees, expect to provide two years of tax returns, recent pay stubs, and employment verification. Tech professionals with stock compensation face additional documentation:

- RSU vesting schedules showing future income potential

- Stock award letters confirming grant amounts and timing

- Historical RSU income demonstrated through tax returns and W-2s

- Bonus history establishing consistent supplemental income patterns

Seattle's concentration of tech employers means many jumbo borrowers carry substantial equity compensation. I specialize in mortgage types that accommodate these income streams, maximizing qualification potential for Microsoft, Amazon, and Google employees.

Self-employed borrowers need two years of business tax returns, profit and loss statements, and sometimes year-to-date financials. Underwriters calculate qualifying income conservatively, often averaging two years and applying depreciation add-backs selectively.

Down Payment Standards

Jumbo financing typically requires larger down payments than conforming loans. While 20% represents the standard threshold, many lenders offer programs starting at 10% or 15% down for well-qualified borrowers.

Down payment tiers and their implications:

- 20% down or more – Access to best rates, no mortgage insurance, simplified approval

- 15% – 19.99% down – Slightly higher rates, possible mortgage insurance, strong credit required

- 10% – 14.99% down – Limited lender options, compensating factors needed, higher reserves

- Less than 10% – Rare for jumbo financing, requires exceptional borrower profile

Reserve requirements accompany down payment considerations. Lenders typically want 6 to 12 months of mortgage payments in liquid reserves after closing. For loan amounts above $1.5 million, expect 12 to 24 months of reserves.

Debt-to-Income Ratio Considerations

Your debt-to-income (DTI) ratio measures monthly debt obligations against gross monthly income. Jumbo lenders typically cap DTI at 43%, though some programs allow up to 45% with strong compensating factors.

Calculating DTI for jumbo financing involves nuances:

- Include all minimum credit card payments, even with zero balances on some cards

- Count student loan payments based on actual monthly obligation or 1% of balance

- Factor in homeowners insurance, property taxes, and HOA dues for new property

- Add any rental property debt obligations, even with offsetting rental income

Seattle-area borrowers often carry higher housing costs relative to income, making DTI management critical. Strategic pay-down of revolving debt before application can improve qualification outcomes significantly.

Interest Rates and Pricing for Jumbo Loans

Historically, jumbo financing carried higher interest rates than conforming loans due to increased lender risk. However, the competitive landscape has shifted dramatically. Current jumbo mortgage rates often match or occasionally beat conforming rates, particularly for borrowers with excellent credit and substantial down payments.

Rate Influencing Factors

Multiple variables impact your jumbo rate:

- Loan amount – Larger loans sometimes receive better pricing due to lender portfolio goals

- Loan-to-value ratio – Lower LTV translates to better rates

- Credit score – Each 20-point increment can affect pricing

- Property type – Single-family residences get best rates; condos, investment properties higher

- Occupancy status – Primary residences receive favorable pricing versus second homes or rentals

- Reserves – Higher post-closing reserves can improve pricing

- Geographic location – Lenders price differently across markets based on local trends

Tech professionals in Seattle often secure excellent jumbo rates because their income stability, stock compensation growth, and substantial reserves position them as lower-risk borrowers despite larger loan amounts.

Fixed vs. Adjustable Rate Products

Jumbo financing offers both fixed-rate and adjustable-rate mortgage (ARM) options:

Fixed-rate jumbo loans provide payment stability across 15, 20, or 30-year terms. These products suit borrowers planning long-term ownership or those prioritizing budget certainty.

Adjustable-rate jumbo loans typically feature initial fixed periods of 5, 7, or 10 years before adjusting annually. ARMs often provide lower initial rates, appealing to buyers expecting income growth, property appreciation, or potential relocation.

For a Microsoft employee purchasing in Redmond with vesting RSUs anticipated to increase income substantially over five years, a 7/1 ARM might offer lower initial payments while maintaining stability through the critical early ownership period.

Special Considerations for Seattle-Area Borrowers

Seattle's unique housing market and employment landscape create specific jumbo financing considerations. Understanding these regional factors helps borrowers navigate the process more effectively.

Tech Compensation and Qualification

Amazon, Microsoft, Google, Meta, and other major employers compensate employees partially through stock awards. Traditional lenders struggle with this income documentation, but specialized jumbo programs recognize RSU income when properly structured.

Effective strategies include:

- Demonstrating two-year RSU history through W-2s and tax returns

- Providing vesting schedules showing future income trajectory

- Calculating sustainable income using conservative stock price assumptions

- Leveraging bonus income with consistent two-year history

I've successfully qualified numerous tech professionals using comprehensive equity compensation, often increasing purchasing power by $200,000 to $400,000 compared to base salary alone.

Property Type Variations

Seattle's diverse housing stock presents different jumbo financing scenarios:

- Single-family detached homes receive most favorable jumbo terms

- Condominiums require warrantable project status and potentially higher rates

- Townhomes typically qualify similarly to single-family homes

- Multi-family properties (2-4 units) need 25% down minimum, higher reserves

Lake Forest Park and Mill Creek feature predominantly single-family inventory, while Seattle and Bellevue include significant condo stock. Understanding these product distinctions helps buyers target appropriate properties aligned with their financing capabilities.

Investment Property Jumbo Loans

Seattle's strong rental market attracts real estate investors seeking jumbo financing for investment properties. These loans require:

- Minimum 25% down payment, often 30% for best pricing

- 740+ credit score for competitive rates

- 12-24 months reserves after closing

- Lower debt-to-income ratio tolerance (typically 43% maximum)

- Six months rental income documentation for experienced investors

Rental income from the subject property typically offsets 75% of projected rent against the mortgage payment when calculating DTI. Existing rental property income requires documentation through leases, tax returns, and Schedule E reporting.

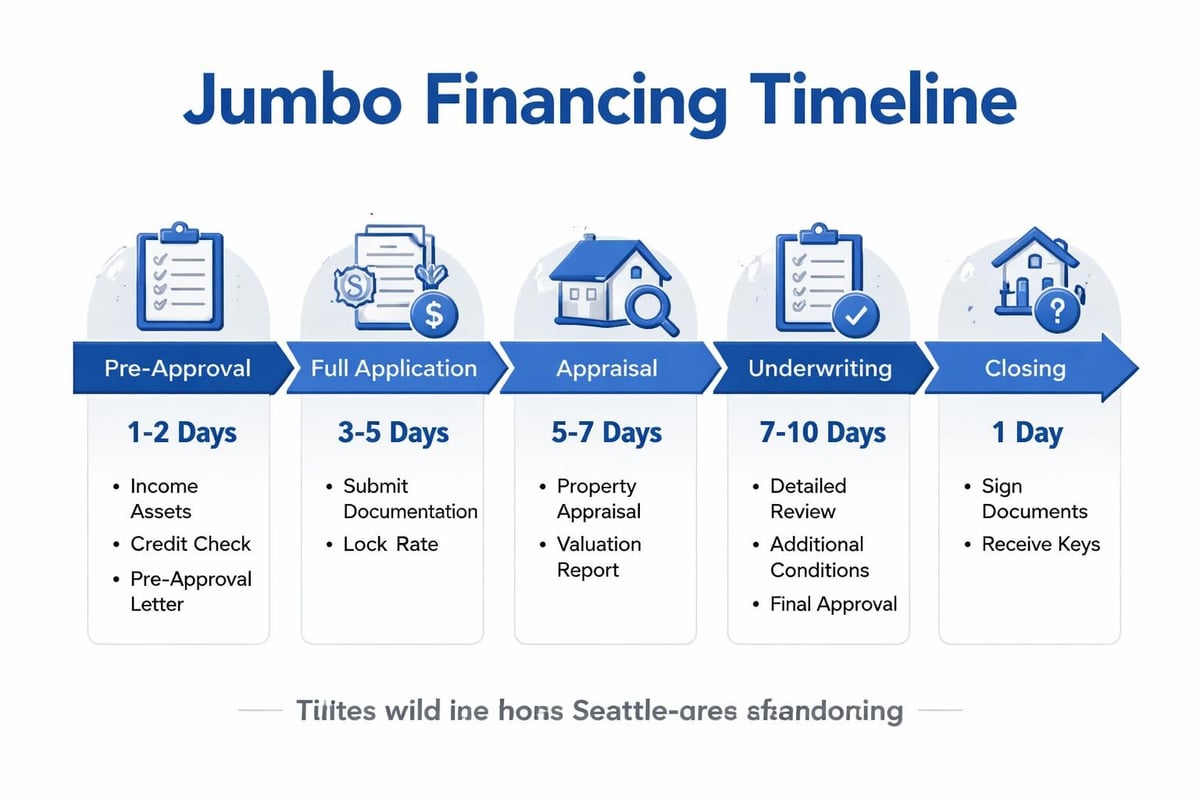

Navigating the Jumbo Loan Application Process

The jumbo financing process mirrors conventional mortgages but demands greater documentation precision and borrower preparation. Understanding the timeline and requirements helps avoid delays in Seattle's competitive market.

Pre-Approval Importance

Strong pre-approval carries exceptional value in Seattle's market. Sellers frequently receive multiple offers, and comprehensive pre-approval signals serious, qualified buyers. For jumbo financing, detailed pre-approval involves:

- Complete income and asset documentation review

- Credit report analysis with score optimization strategies

- Property type and price range discussion aligned with qualification

- Down payment source verification

- Reserve requirements confirmation

Tech professionals should gather RSU documentation, stock award letters, and vesting schedules early. Self-employed borrowers need current profit and loss statements alongside tax returns. Working with an experienced broker streamlines this documentation process significantly.

Documentation Checklist

Assembling documentation proactively accelerates approval:

Income verification:

- Two years W-2s and tax returns (all schedules)

- Recent pay stubs covering one month

- RSU vesting schedules and award letters

- Bonus or commission history documentation

- Business tax returns if self-employed or partnership/S-corp owner

Asset verification:

- Two months bank statements (all pages, all accounts)

- Investment account statements showing sufficient reserves

- Retirement account statements if using for reserves

- Gift letter and donor bank statements if receiving gift funds

- Explanation for any large deposits (over $1,000)

Credit and property:

- Authorization for credit report

- Explanation letters for credit inquiries or derogatory items

- Purchase agreement once in contract

- Homeowners insurance quote

- HOA documents if applicable

Lenders scrutinize documentation thoroughly for jumbo financing. Incomplete information delays approval, potentially jeopardizing time-sensitive Seattle transactions.

Appraisal and Property Valuation

Jumbo loans require detailed appraisals meeting strict lender standards. For loan amounts exceeding $1.5 million, lenders often order two full appraisals from separate appraisers, using the lower value for loan calculation.

Appraisers analyze comparable sales, property condition, location factors, and market trends. In rapidly appreciating areas like Shoreline or Everett, recent sales data becomes critical. Unique properties or those in limited-inventory neighborhoods sometimes challenge valuation, potentially requiring additional comparable properties from adjacent areas.

Low appraisals create challenges. Options include:

- Negotiating price reduction with seller

- Increasing down payment to maintain loan amount

- Disputing appraisal with supporting comparable sales data

- Seeking second appraisal if lender allows

- Restructuring with different loan program

Working with experienced listing agents who provide strong comparable sales packages helps appraisers defend valuations in unique or high-value properties.

Jumbo Financing Strategies for Maximum Success

Strategic approaches improve jumbo loan outcomes, particularly in competitive markets requiring quick closes and strong offers.

Timing Your Application

Application timing impacts both rates and approval likelihood. Consider these factors:

Market conditions – Rate environments fluctuate. Monitoring trends helps identify favorable application windows, though attempting to time markets perfectly rarely succeeds.

Employment stability – Avoid job changes during application or shortly before. Lenders verify employment immediately before closing, and changes can derail approval even after initial underwriting.

Credit optimization – Address credit issues months before application. Dispute errors, pay down balances, and avoid new credit inquiries for 90-180 days preceding application.

Income timing – Year-end or vesting periods might boost qualifying income for bonus or RSU-dependent borrowers. Strategic timing around these events can increase purchasing power.

Loan Structure Optimization

Different jumbo structures serve different scenarios:

Single loan – Most straightforward, with one closing and one monthly payment. Best for standard situations where loan amount and LTV fit program parameters.

Piggyback structure (80-10-10 or 80-15-5) – First mortgage at 80% LTV, second mortgage for additional leverage, remainder as down payment. This avoids mortgage insurance on certain programs and can improve rate pricing.

Portfolio loans – Held by originating bank rather than sold. These offer flexibility on unique income situations, property types, or borrower scenarios not fitting agency guidelines.

Lynnwood and Everett buyers sometimes benefit from portfolio products when purchasing unique properties or having non-traditional income. Seattle and Bellevue transactions more frequently use standard jumbo products given property values and borrower profiles.

Rate Lock Strategies

Interest rate locks protect against rate increases during processing. Standard locks run 30, 45, or 60 days, with longer periods carrying higher costs.

Strategic locking considerations:

- Lock immediately when application if rates appear favorable and purchase timeline is certain

- Float initially if rate trends suggest improvement and you can tolerate risk

- Consider extended locks for new construction with uncertain closing dates

- Use float-down provisions if available and rates drop significantly after locking

Seattle's quick-moving market often demands faster closes. I've closed jumbo loans in as few as nine business days when borrowers provide complete documentation upfront and properties appraise smoothly.

Common Jumbo Financing Questions

Can I Get Jumbo Financing with Less Than 20% Down?

Yes, though options narrow. Select lenders offer jumbo programs starting at 10% down for borrowers with excellent credit (typically 760+), strong income stability, and substantial reserves. Wells Fargo’s jumbo loan programs include various down payment options worth exploring.

Lower down payments typically require:

- Higher credit scores than 20% down programs

- Lower debt-to-income ratios (often 40% maximum)

- Increased reserve requirements (12+ months)

- Possible mortgage insurance depending on loan amount

- Premium pricing compared to 20% down

How Do Jumbo Rates Compare to Conforming Rates?

Jumbo rates currently compete favorably with conforming rates, sometimes matching or beating them. Top jumbo lenders price aggressively for well-qualified borrowers. Your specific rate depends on credit score, LTV, reserves, loan amount, and overall borrower profile.

What Credit Score Do I Need?

Minimum credit scores typically range from 680 to 720 depending on compensating factors. However, optimal pricing requires 740 or higher. Seattle's competitive market and high property values mean most successful jumbo borrowers carry 760+ scores.

Can I Use Gift Funds for Down Payment?

Yes, jumbo lenders accept gift funds from family members. Requirements include:

- Gift letter signed by donor stating no repayment expectation

- Documentation of fund transfer from donor to borrower

- Donor bank statements proving funds availability

- Borrower contributing minimum funds from own resources (often 5-10%)

Some lenders restrict gift fund percentage for investment properties or limit donor relationships to immediate family.

How Long Does Jumbo Loan Approval Take?

Standard jumbo approval takes 30 to 45 days from application to closing. However, well-prepared borrowers with complete documentation can close faster. I regularly close jumbo loans in 14 to 21 days, with exceptional cases completing in nine business days when urgency exists and all parties execute efficiently.

Do I Need Mortgage Insurance on Jumbo Loans?

Generally no. Most jumbo programs avoid mortgage insurance even with less than 20% down, instead pricing the additional risk into the interest rate. Some portfolio programs offer mortgage insurance options at lower LTVs as an alternative to rate adjustments.

Regional Lender and Program Selection

Choosing the right lender significantly impacts your jumbo financing experience. Not all lenders offer competitive jumbo products, and program variations can substantially affect qualification and pricing.

Evaluating Lender Capabilities

Strong jumbo lenders demonstrate:

- Portfolio of jumbo loan products with clear qualification guidelines

- Experience with tech compensation and complex income scenarios

- Local market knowledge specific to Seattle and surrounding cities

- Competitive pricing and rate transparency

- Clear communication and responsive service

- Proven ability to close on time, particularly for competitive offers

Working with a broker who maintains relationships across multiple jumbo lenders provides access to broader product selection and competitive pricing. Direct lender relationships offer streamlined processing but potentially limited product options.

Program Feature Comparison

Compare these features across potential jumbo programs:

| Program Feature | Standard Jumbo | Portfolio Jumbo | High-Balance Conventional |

|---|---|---|---|

| Maximum Loan Amount | $3-5M typical | Varies by lender | Up to $1,209,750 |

| Minimum Down Payment | 20% | 10-20% | 5% |

| Credit Score Minimum | 700-720 | 680-700 | 620 |

| Reserve Requirements | 6-12 months | 3-6 months | 2-6 months |

| Rate Competitiveness | Excellent | Good | Good |

High-balance conventional loans serve the gap between standard conforming limits and jumbo territory. In Seattle, the 2026 high-balance limit reaches $1,209,750, providing an alternative to pure jumbo financing for properties in this range.

Understanding Closing Costs

Jumbo financing closing costs mirror conventional loans with some variations:

- Origination fees range from 0% to 1% of loan amount depending on rate selection

- Appraisal costs run higher for jumbo properties, especially if two appraisals required ($600-$1,200 total)

- Title insurance scales with purchase price, increasing proportionally for higher-value properties

- Escrow reserves for taxes and insurance require larger deposits given higher property values

Total closing costs typically range from 2% to 4% of the purchase price. A $1.2 million Seattle purchase might carry $24,000 to $48,000 in closing costs depending on specific fees, property taxes, and selected rate/point structure.

Refinancing Jumbo Loans

Jumbo refinancing follows similar qualification standards as purchase loans. Common refinance scenarios include:

Rate and term refinance – Obtaining better interest rate or adjusting loan term without taking cash out. Requires strong credit, sufficient equity, and qualification under current income guidelines.

Cash-out refinance – Accessing equity while refinancing. Typically limited to 80% LTV for primary residences, 75% for second homes, 70% for investment properties.

ARM to fixed conversion – Converting adjustable-rate jumbo loans to fixed rates before adjustment periods begin. This strategy locks in payment certainty when income allows qualification at fully-amortizing fixed rates.

Mill Creek and Shoreline homeowners who purchased during lower price periods often carry substantial equity, positioning them well for cash-out refinancing to fund renovations, investment opportunities, or debt consolidation.

Advanced Jumbo Financing Scenarios

Sophisticated borrowers and unique situations sometimes require specialized jumbo solutions beyond standard program parameters.

Foreign National Jumbo Loans

Seattle attracts international buyers, particularly from Asia and Canada. Foreign national jumbo programs accommodate non-U.S. citizens without domestic credit or income history.

These programs typically require:

- 30-40% down payment minimum

- Significant reserves (often 12+ months)

- Foreign credit documentation when available

- Valid visa or foreign passport

- U.S. bank account established before closing

- Higher interest rates (typically 0.50-1.00% above standard jumbo rates)

Property types limit to primary residences and second homes, with investment properties generally excluded. Lenders verify income through tax returns from home country, employment letters, or bank statements showing regular deposits.

Bank Statement Jumbo Programs

Self-employed borrowers with complex tax situations sometimes benefit from bank statement jumbo programs. These evaluate income through deposits rather than tax returns, helping borrowers whose tax strategies minimize reported income.

Requirements include:

- 12 to 24 months business and personal bank statements

- Calculation of income based on average deposits

- 20-25% down payment minimum

- 700+ credit score

- Strong reserves

- Detailed business ownership documentation

Rates typically run 0.25% to 0.75% higher than full documentation jumbo loans. Tech consultants, contractors, and business owners in Seattle frequently explore these options when standard documentation understates actual income.

Jumbo Loans for New Construction

Purchasing new construction with jumbo financing adds complexity around timing and valuation. Construction-to-permanent loans combine construction financing and permanent mortgage into single closing, reducing costs and simplifying the process.

Key considerations include:

- Longer rate lock periods (90-180 days) accounting for construction completion

- Builder reputation and track record affecting lender approval

- Appraisal based on plans and specifications rather than completed home

- Draw schedules coordinating funds release with construction milestones

- Higher down payment requirements during construction phase

Everett and Lake Forest Park feature new construction opportunities where these specialized programs provide value. Working with experienced builders who understand lender requirements streamlines approval significantly.

Interest-Only Jumbo Options

Interest-only jumbo loans allow payment of only interest for an initial period (typically 10 years), after which payments adjust to fully-amortizing for the remaining term. This reduces initial monthly obligations while building equity through appreciation.

These products suit borrowers expecting:

- Significant income growth over time (common among tech professionals with increasing RSU vesting)

- Property appreciation outpacing principal reduction benefits

- Investment flexibility to deploy saved payment amounts into higher-return opportunities

- Potential property sale before amortization period begins

Interest-only options require excellent credit (760+), low debt-to-income ratios, and substantial reserves. Qualifying uses the fully-amortizing payment rather than interest-only payment, ensuring borrowers can afford future payment increases.

Jumbo financing opens doors to Seattle's most desirable properties, and understanding the qualification requirements, documentation expectations, and strategic approaches positions you for success in this specialized market. Whether you're a tech professional leveraging equity compensation, a self-employed business owner, or an investor expanding your portfolio, the right jumbo loan structure can maximize your purchasing power while maintaining comfortable payment levels. With 25+ years of experience helping Seattle-area clients navigate complex financing scenarios, I bring the expertise and lender relationships needed to secure competitive jumbo rates and close transactions efficiently, even in competitive multiple-offer situations. If you're ready to explore jumbo financing options for your Seattle, Bellevue, Redmond, Kirkland, or surrounding area purchase, Mortgage Reel is here to guide you through every step with transparency, strategy, and proven results.