When purchasing a luxury home in Seattle, Bellevue, or Redmond, you'll likely encounter financing amounts that exceed standard loan limits. That's where jumbo loans become essential. These specialized mortgage products allow qualified borrowers to finance properties above conventional loan thresholds, opening doors to Seattle's competitive high-value housing market. For tech professionals at Amazon, Microsoft, and other major employers in the region, understanding how these loans work is critical to maximizing buying power while securing favorable terms.

What Are Jumbo Loans and When Do You Need One

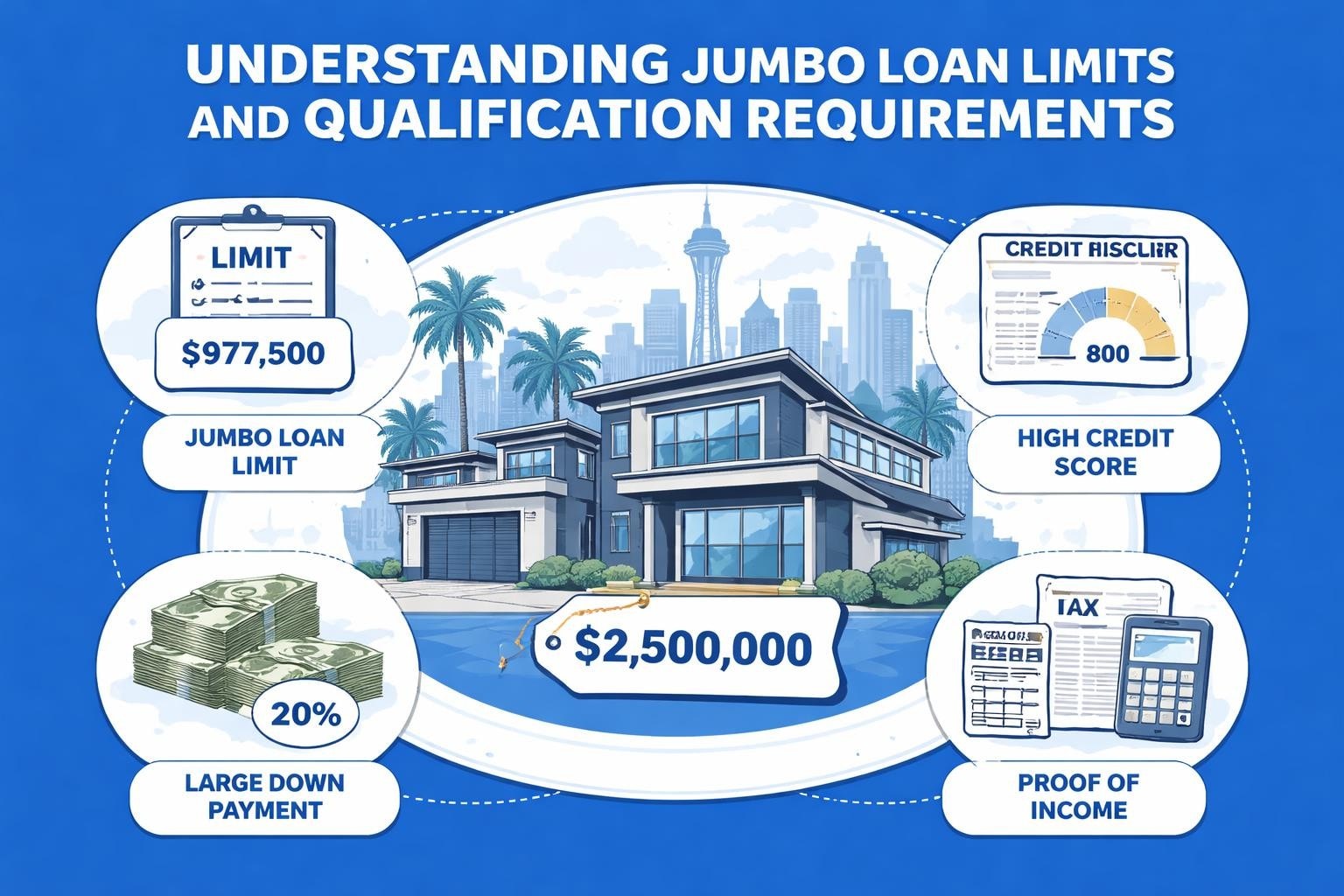

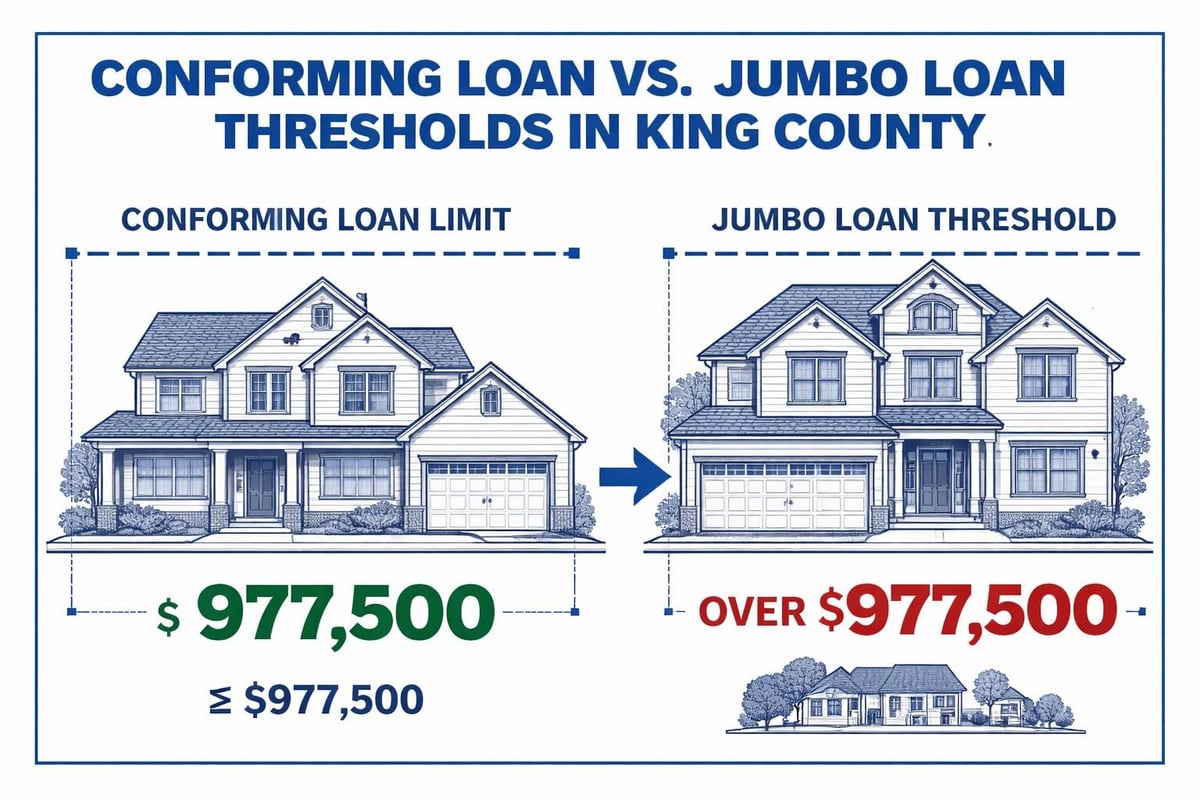

A jumbo mortgage is a home loan that exceeds the maximum lending limits set by the Federal Housing Finance Agency for conforming loans. In King County, where Seattle sits, the 2026 conforming loan limit stands at $806,500 for single-family homes. Any mortgage amount above this threshold requires a jumbo loan structure.

These loans exist because government-sponsored enterprises like Fannie Mae and Freddie Mac won't purchase or guarantee loans above conforming loan limits. This creates additional risk for lenders, which translates into stricter qualification requirements and different pricing structures.

Why Seattle Homebuyers Frequently Need Jumbo Financing

Seattle's robust housing market consistently pushes home prices above national averages. In neighborhoods like Madison Park, Queen Anne, and Capitol Hill, median home prices routinely exceed $1.2 million. Even in neighboring cities like Shoreline and Lake Forest Park, desirable single-family homes often surpass conforming limits.

The region's concentration of high-earning tech professionals creates sustained demand for premium properties. When your target home in Bellevue or Kirkland costs $1.5 million, understanding jumbo loan mechanics becomes non-negotiable.

Current Jumbo Loan Limits Across the Greater Seattle Area

Loan limits vary by county and property type. Here's what Seattle-area homebuyers need to know for 2026:

| County | Single-Family Limit | Two-Unit Limit | Three-Unit Limit | Four-Unit Limit |

|---|---|---|---|---|

| King County | $806,500 | $1,032,500 | $1,248,350 | $1,550,500 |

| Snohomish County | $806,500 | $1,032,500 | $1,248,350 | $1,550,500 |

| Pierce County | $806,500 | $1,032,500 | $1,248,350 | $1,550,500 |

Any loan amount exceeding these thresholds qualifies as a jumbo loan. In areas like Everett and Mill Creek within Snohomish County, buyers pursuing properties above $806,500 will automatically enter jumbo territory.

For ultra-luxury properties exceeding $2 million or $3 million, some lenders designate these as super jumbo mortgages, which carry even more stringent requirements and specialized underwriting processes.

Qualification Requirements for Jumbo Loans

Lenders impose stricter standards for jumbo loans compared to conventional financing. Understanding these requirements helps you prepare effectively and avoid surprises during the application process.

Credit Score Expectations

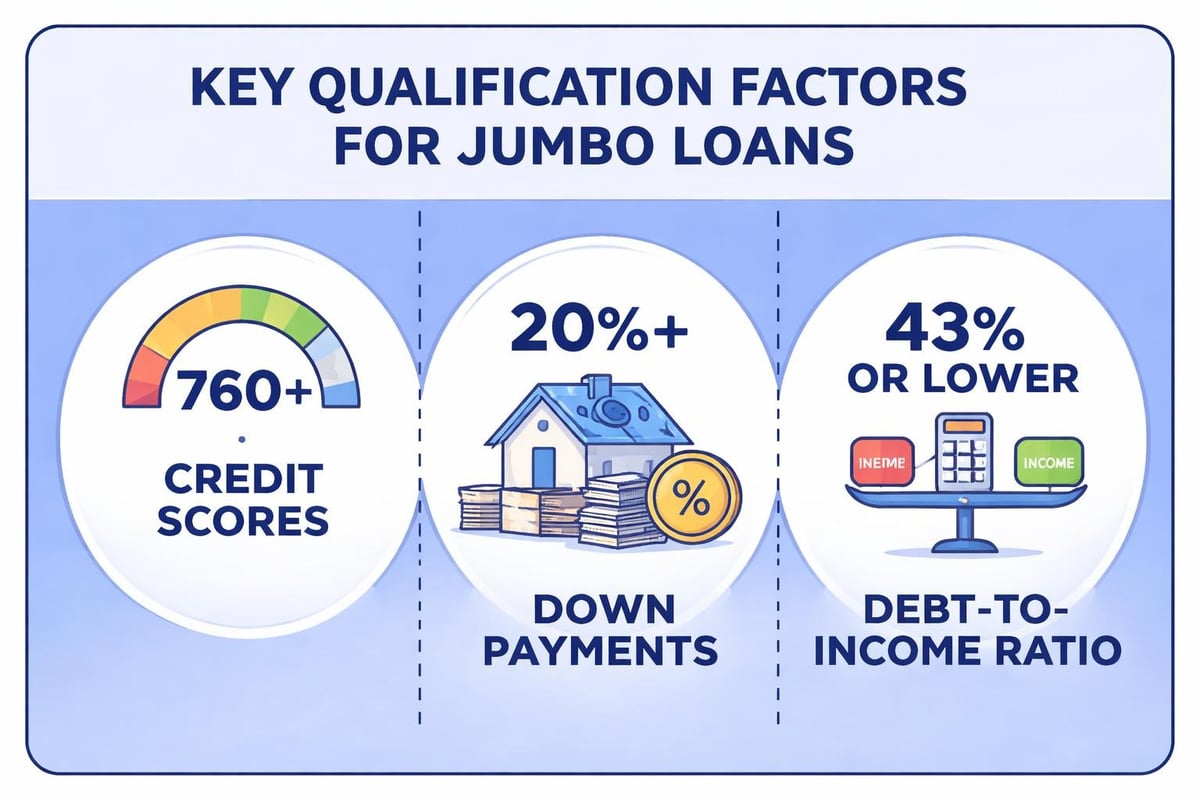

Most lenders require minimum credit scores between 700 and 720 for jumbo loan approval. Some portfolio lenders may accept scores as low as 680, but expect higher interest rates and larger down payments. Maintaining excellent credit history with minimal outstanding debts strengthens your application considerably.

Down Payment Requirements

While conventional loans often accept down payments as low as 3% to 5%, jumbo loans typically require:

- 10% minimum for properties up to $1.5 million

- 15% to 20% for properties between $1.5 million and $2 million

- 20% to 30% for properties exceeding $2 million

Some lenders offer 10% down programs for exceptionally qualified borrowers with strong compensating factors like substantial liquid reserves or significant stock compensation.

Debt-to-Income Ratio Standards

Your debt-to-income (DTI) ratio measures monthly debt obligations against gross monthly income. For jumbo loans, lenders generally require:

- Maximum DTI of 43% for most borrowers

- DTI up to 45% with strong compensating factors

- Lower ratios preferred for applicants with minimal reserves

Tech professionals in Seattle often benefit from strategies that maximize stock compensation when calculating qualifying income, particularly those holding RSUs at Amazon or Microsoft.

Reserve Requirements

Lenders require substantial cash reserves after closing, typically:

- Six to twelve months of mortgage payments in liquid assets

- Higher reserves for investment properties or multiple mortgages

- Retirement accounts may count but often at discounted values

For a $1.2 million home in Redmond with a $960,000 mortgage, you might need $60,000 to $120,000 in accessible reserves beyond your down payment and closing costs.

Documentation Standards for Jumbo Loan Applications

Jumbo loans demand comprehensive documentation verifying income, assets, employment, and creditworthiness. Expect to provide:

- Two years of personal tax returns with all schedules

- Two years of W-2s or 1099s from all income sources

- Recent pay stubs covering the most recent 30 days

- Two to three months of bank statements for all accounts

- Investment account statements showing balances and holdings

- Written explanations for large deposits or transfers

- Employment verification directly from your employer

- Rental income documentation if claiming property income

For self-employed borrowers, additional requirements include business tax returns, profit and loss statements, and potentially CPA-prepared financials. Self-employed applicants in Lynnwood or Mill Creek should prepare for 60 to 90 days of documentation gathering.

Interest Rates and Pricing Considerations

Jumbo loan interest rates historically traded higher than conforming rates due to increased lender risk. However, market dynamics in 2026 have narrowed this gap considerably. In some cases, jumbo rates actually price competitively with or below conforming rates.

Factors Influencing Your Rate

Several variables affect your final interest rate:

- Credit score: Higher scores unlock better pricing tiers

- Loan-to-value ratio: Larger down payments reduce rates

- Property type: Single-family homes receive better rates than condos or investment properties

- Reserves: Substantial liquid assets demonstrate lower risk

- Debt-to-income ratio: Lower DTI often correlates with better pricing

- Occupancy: Primary residences price better than second homes or rentals

A borrower in Seattle with 780+ credit, 25% down, and strong reserves might secure rates within 0.125% to 0.25% of conforming loan pricing.

Points and Rate Buydowns

Jumbo borrowers often have flexibility to purchase discount points, paying upfront fees to reduce interest rates. Each point typically costs 1% of the loan amount and reduces your rate by approximately 0.25%.

On a $1 million mortgage, one point costs $10,000 and might lower your rate from 6.75% to 6.50%. Whether this makes sense depends on how long you plan to keep the loan and your cash position after closing.

Property Type and Location Considerations

Not all properties qualify equally for jumbo financing. Lenders scrutinize property characteristics more carefully when loan amounts increase.

Acceptable Property Types

Most jumbo lenders readily finance:

- Single-family detached homes

- Townhomes and condominiums (with review of HOA documents)

- Planned unit developments (PUDs)

- Multi-unit properties (two to four units with higher down payments)

Condominiums require additional review, including warrantability checks, HOA financial health assessments, and owner-occupancy ratios. A luxury condo in downtown Seattle needs thorough documentation showing the building meets lender requirements.

Geographic Preferences

Lenders favor properties in stable, established markets with consistent appreciation. The Greater Seattle area generally receives favorable treatment due to:

- Strong employment base across multiple industries

- Limited housing supply relative to demand

- Historical price stability and appreciation

- Diverse economic drivers beyond single sectors

Properties in Shoreline, Lake Forest Park, and Everett benefit from proximity to Seattle's economic engine while offering comparatively lower entry prices.

Special Considerations for Tech Professionals

Seattle's concentration of technology companies creates unique opportunities and challenges for jumbo loan applicants. Many tech employees receive significant compensation through restricted stock units (RSUs), bonuses, and equity awards.

Qualifying Stock Compensation

Lenders can include RSUs and stock grants in qualifying income calculations, but specific rules apply:

- Two-year history of receiving stock compensation

- Vesting schedules documented and verified

- Averaging formulas applied to variable income

- Discounts for volatility or restricted liquidity

A software engineer at Microsoft with a $200,000 base salary plus $100,000 in annual RSUs might qualify using $250,000 to $270,000 in total income, depending on vesting patterns and documentation quality.

Managing Multiple Income Sources

Tech professionals often juggle W-2 income, RSUs, bonuses, consulting income, and side business revenue. Presenting these income streams clearly and documenting them thoroughly strengthens your jumbo loan application significantly.

Working with a mortgage broker experienced in tech compensation packages ensures proper calculation and presentation to underwriters, maximizing your purchasing power in competitive Seattle neighborhoods.

Jumbo Loan Programs and Portfolio Options

Multiple jumbo loan programs exist, each with distinct features and qualification requirements.

Agency Jumbo Programs

Some lenders offer conforming jumbo programs that mirror conventional loan guidelines but extend to higher loan amounts. These programs typically feature:

- Streamlined documentation similar to conventional loans

- Competitive interest rates

- Flexible occupancy and property type options

- Lower reserve requirements than traditional jumbo programs

Portfolio Jumbo Loans

Portfolio lenders hold loans on their own balance sheets rather than selling them to investors. This creates flexibility for unique situations:

- Non-traditional income documentation accepted

- Recent credit events considered with explanations

- Foreign national borrowers may qualify

- Higher DTI ratios possible with compensating factors

A real estate investor in Bellevue purchasing a fourth rental property might access portfolio jumbo financing when conventional programs decline the application.

Fixed-Rate versus Adjustable-Rate Options

Jumbo loans come in both fixed-rate and adjustable-rate (ARM) structures:

Fixed-Rate Jumbo Loans provide:

- Predictable payments for 15, 20, or 30 years

- Protection against rising interest rates

- Simplified budgeting and planning

- Higher initial rates compared to ARMs

Adjustable-Rate Jumbo Mortgages offer:

- Lower initial rates during fixed periods (typically 5, 7, or 10 years)

- Potential savings if you plan to sell or refinance before adjustment

- Rate caps limiting increases at adjustment and over loan life

- Higher risk if rates rise significantly after the fixed period

A tech professional planning to upgrade in five to seven years might benefit from a 7/1 ARM, capturing lower initial rates while selling before the first adjustment.

Common Jumbo Loan Mistakes to Avoid

Even sophisticated borrowers make preventable errors during the jumbo loan process. Awareness helps you navigate smoothly.

Insufficient Reserve Planning

Many applicants focus entirely on down payment accumulation while neglecting reserve requirements. After providing 20% down on a $1.5 million home in Kirkland ($300,000), you still need six to twelve months of reserves ($60,000 to $120,000 in liquid assets).

Planning total cash needs before making offers prevents scrambling for documentation or delaying closings.

Large Undocumented Deposits

Depositing large sums into bank accounts during the mortgage process triggers scrutiny. Underwriters require written explanations and source documentation for any deposit exceeding 25% of your monthly income.

Cashing out stocks, receiving gifts from family, or selling assets should be documented contemporaneously with clear paper trails.

Job Changes During Application

Changing employers or shifting to self-employment during the loan process complicates approval significantly. Even lateral moves within the same industry may require additional verification and delay closing.

If a career change is imminent, consider either completing the home purchase first or waiting until you've established two years of income history in your new position.

Underestimating Closing Timelines

Jumbo loans typically require 30 to 45 days for closing, though experienced lenders can compress timelines to as few as nine business days with complete documentation. Underestimating this timeline leads to missed closing dates, rate lock expirations, and purchase contract complications.

Starting the pre-approval process early and maintaining organized documentation accelerates the overall timeline.

Refinancing Jumbo Loans

Existing jumbo loan holders should evaluate refinancing opportunities when rates drop or financial situations improve. The same qualification standards apply, but borrowers benefit from existing homeownership history and potentially increased home values.

Rate-and-Term Refinancing

This straightforward refinance replaces your existing jumbo loan with a new loan at better terms, lowering monthly payments or shortening the loan term. Seattle's strong appreciation often creates equity gains that improve loan-to-value ratios, unlocking better pricing tiers.

Cash-Out Refinancing

Jumbo cash-out refinancing allows you to access home equity for investment opportunities, debt consolidation, or major purchases. Lenders typically allow cash-out up to 80% loan-to-value, though some portfolio lenders extend to 85% or 90% for exceptionally qualified borrowers.

A homeowner in Redmond who purchased for $1.2 million in 2023 might now have a property worth $1.5 million, creating refinancing opportunities to access equity while maintaining competitive rates.

Working with Experienced Jumbo Loan Specialists

The complexity of jumbo financing demands expertise beyond standard mortgage processing. Specialized jumbo loan brokers understand nuances that dramatically impact approval odds and final terms.

Look for mortgage professionals with:

- Extensive jumbo loan experience closing high-balance transactions regularly

- Access to multiple lenders offering diverse jumbo programs

- Understanding of complex income including stock compensation and self-employment

- Strong communication skills keeping you informed throughout the process

- Proven track record demonstrated through client reviews and referrals

According to research from the National Bureau of Economic Research, jumbo loans carry distinct characteristics and risk profiles that require specialized underwriting expertise.

In Seattle's competitive market, working with a mortgage broker who understands local property values, employment trends, and lender preferences provides significant advantages when structuring your jumbo loan application.

Frequently Asked Questions About Jumbo Loans

Can I get a jumbo loan with less than 20% down?

Yes, many lenders offer jumbo loans with 10% to 15% down payment options for well-qualified borrowers. These typically require higher credit scores, lower debt-to-income ratios, and substantial reserve requirements. Some specialized programs even allow as little as 10% down for primary residences in strong markets like Seattle.

How long does jumbo loan approval take?

With complete documentation, jumbo loans typically close in 30 to 45 days. However, experienced lenders with streamlined processes can close in as few as nine business days when borrowers provide documentation promptly and properties appraise without complications.

Do jumbo loans require mortgage insurance?

Unlike conventional loans below 80% loan-to-value, jumbo loans generally don't require private mortgage insurance (PMI) regardless of down payment amount. Instead, lenders price the additional risk into interest rates and require larger reserves and higher credit scores.

Can self-employed borrowers qualify for jumbo loans?

Absolutely. Self-employed borrowers in Lynnwood, Mill Creek, and throughout the Seattle area regularly qualify for jumbo financing. Expect to provide two years of personal and business tax returns, year-to-date profit and loss statements, and potentially CPA-prepared financial documents. The income documentation process is more rigorous, but qualification remains entirely achievable.

Are jumbo loan rates higher than conventional rates?

Not necessarily. In 2026, jumbo loan rates often price competitively with or even below conventional conforming rates, particularly for well-qualified borrowers. Your specific rate depends on credit score, down payment, reserves, property type, and overall financial profile.

Can I use gift funds for my jumbo loan down payment?

Yes, most jumbo loan programs accept gift funds from eligible family members. You'll need a signed gift letter stating the funds are a gift with no repayment expectation, plus documentation showing the transfer from the donor's account to yours. Some lenders limit the percentage of down payment that can come from gifts, requiring a minimum borrower contribution.

Understanding jumbo loans opens doors to Seattle's premium real estate market, whether you're targeting a waterfront property in Madison Park or a tech-forward home in Redmond. The right financing strategy, combined with thorough preparation and expert guidance, makes high-balance financing accessible and competitive. Keith Akada at Mortgage Reel specializes in jumbo loans for Seattle-area tech professionals, with 25+ years of experience structuring complex compensation packages and closing high-value transactions efficiently. With 750+ five-star reviews and the ability to close in as few as nine business days, Keith provides the expertise and execution you need for confident homebuying decisions.