Understanding jumbo rates is essential for homebuyers in Seattle's competitive real estate market, where property values frequently exceed conforming loan limits. With the 2026 conforming loan limit set at $832,750 for most counties, many Seattle-area homebuyers find themselves needing financing that falls into the jumbo category. These larger loans come with their own pricing structures, qualification standards, and strategic considerations that can significantly impact your monthly payment and long-term financial planning.

What Are Jumbo Rates and How Do They Work

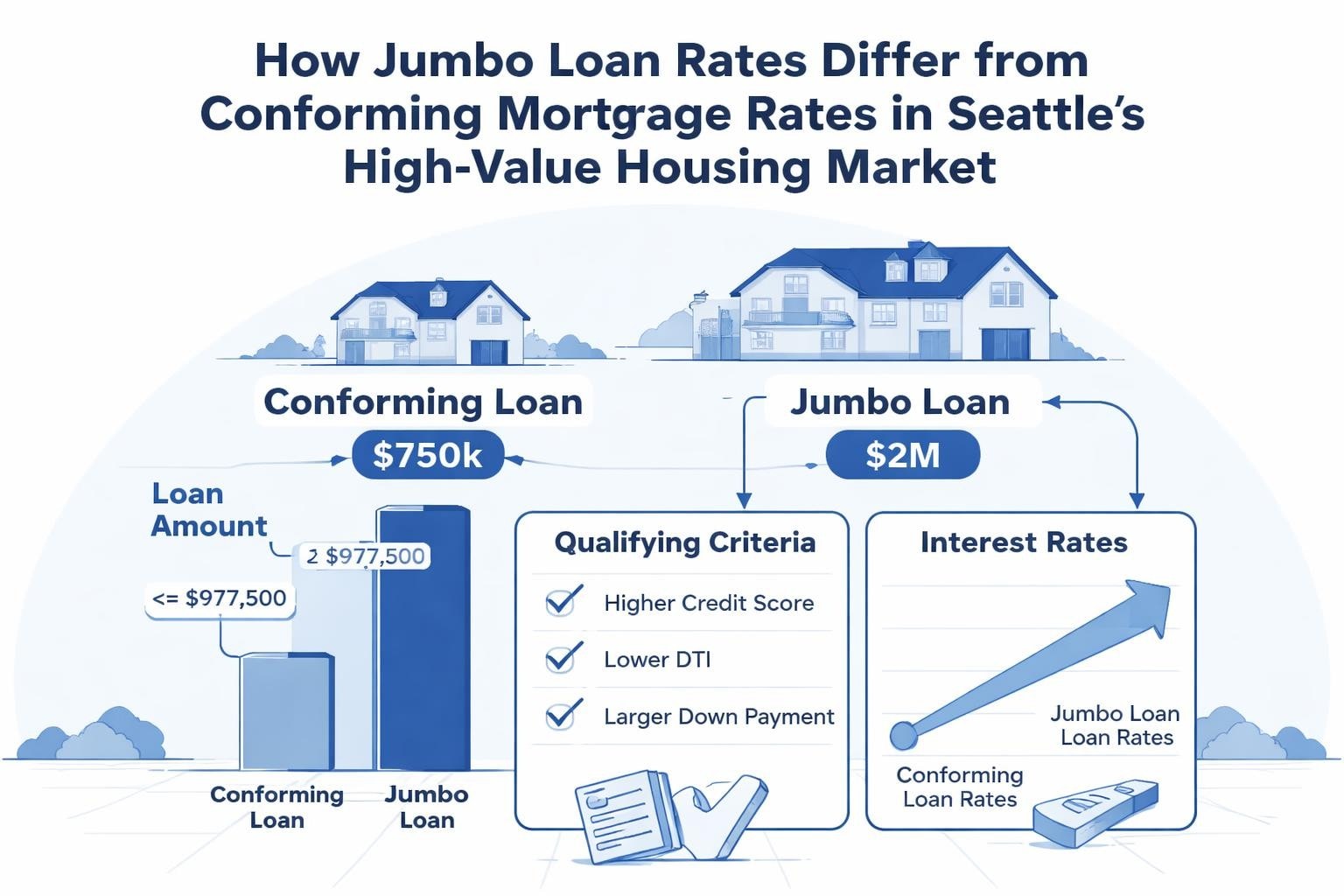

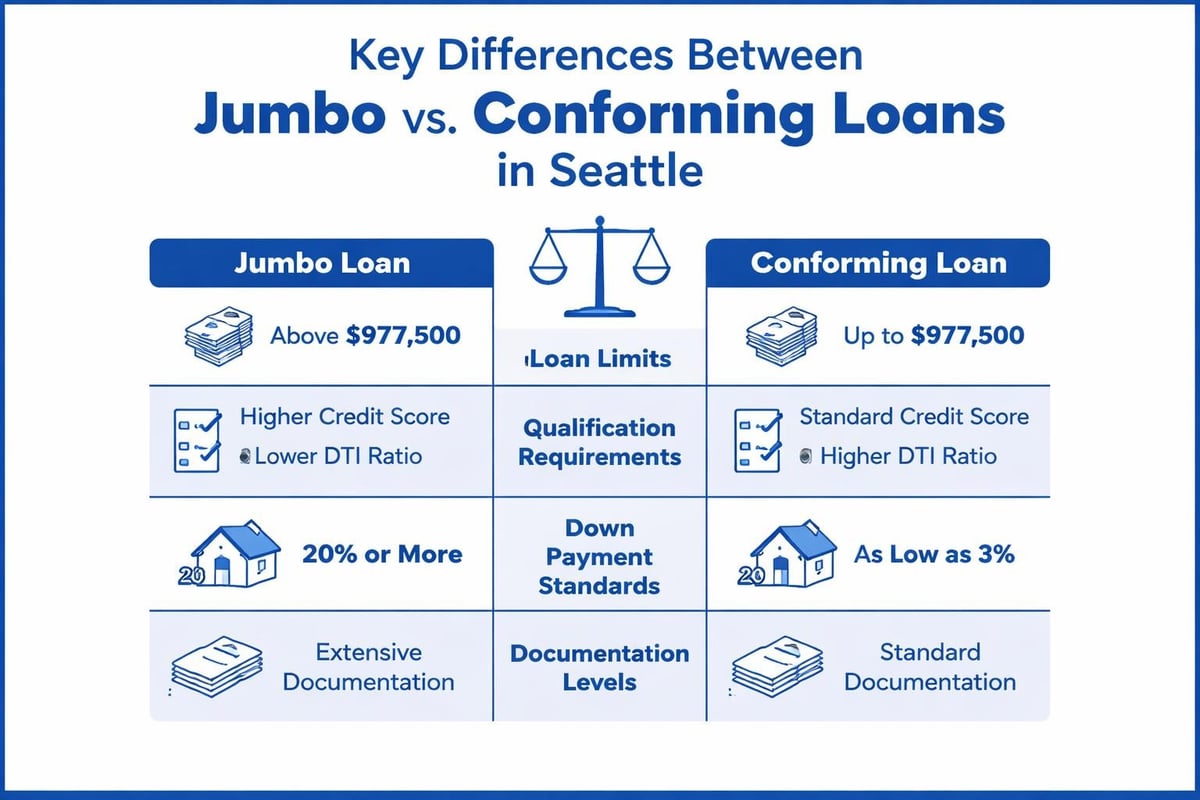

Jumbo rates refer to the interest rates charged on jumbo loans-mortgages that exceed the conforming loan limits established by the Federal Housing Finance Agency. In King County and Snohomish County, where Seattle, Bellevue, Redmond, and surrounding cities are located, any loan amount above $832,750 is generally classified as a jumbo loan.

The pricing on these loans differs from conventional conforming mortgages because they carry additional risk for lenders. Without the backing of Fannie Mae or Freddie Mac, lenders assume full responsibility for these loans, which translates to more rigorous underwriting standards and often different rate structures.

Why Jumbo Rates Differ From Conforming Rates

Several factors contribute to the unique pricing of jumbo rates:

- Portfolio lending risk: Lenders often hold jumbo loans in their own portfolios rather than selling them to government-sponsored enterprises

- Loan amount exposure: Higher loan balances mean greater potential loss in the event of default

- Underwriting complexity: More extensive documentation and verification requirements increase processing costs

- Market liquidity: The secondary market for jumbo loans is less liquid than for conforming loans

Historically, jumbo rates ran consistently higher than conforming rates. However, market dynamics have shifted in recent years. According to current jumbo mortgage rate data from Bankrate, the spread between jumbo and conforming rates has narrowed considerably, and in some cases, jumbo rates actually price lower for well-qualified borrowers.

Current Jumbo Rate Landscape in Seattle

Seattle's housing market presents unique challenges and opportunities for jumbo borrowers. The median home price in neighborhoods like Queen Anne, Capitol Hill, and Wallingford frequently pushes buyers into jumbo territory, making understanding current rate trends crucial for financial planning.

Rate Environment in 2026

The broader mortgage rate environment influences jumbo rates, though not always in lockstep with conforming products. While the average 30-year mortgage rate fluctuates with Federal Reserve policy and economic conditions, jumbo rates respond to additional factors including investor appetite for private-label securities and individual lender portfolio capacity.

For tech professionals working at Amazon, Microsoft, or Google in Seattle, Bellevue, and Redmond, timing your jumbo loan application around rate movements can result in significant savings. A quarter-point difference on a $1.2 million loan equals approximately $180 per month or over $64,000 across a 30-year term.

| Rate Scenario | Monthly Payment (30-Year, $1.2M) | Total Interest Paid |

|---|---|---|

| 6.50% | $7,586 | $1,530,960 |

| 6.75% | $7,782 | $1,601,520 |

| 7.00% | $7,980 | $1,672,800 |

Jumbo Rate Variations by Loan Type

Different jumbo loan structures carry different rate pricing:

- 30-year fixed jumbo: Most common option, offering rate stability and predictable payments

- 15-year fixed jumbo: Lower rates but higher monthly payments, ideal for accelerated equity building

- 7/1 and 10/1 ARM jumbo: Initial rate discount with adjustment risk after the fixed period

- Interest-only jumbo: Lower initial payments with principal deferral, popular with high-income professionals managing stock compensation

Qualification Requirements That Affect Jumbo Rates

Your qualification profile directly impacts the jumbo rates you'll be offered. Lenders price risk through both approval standards and interest rate adjustments, meaning stronger borrowers receive more favorable pricing.

Credit Score Impact

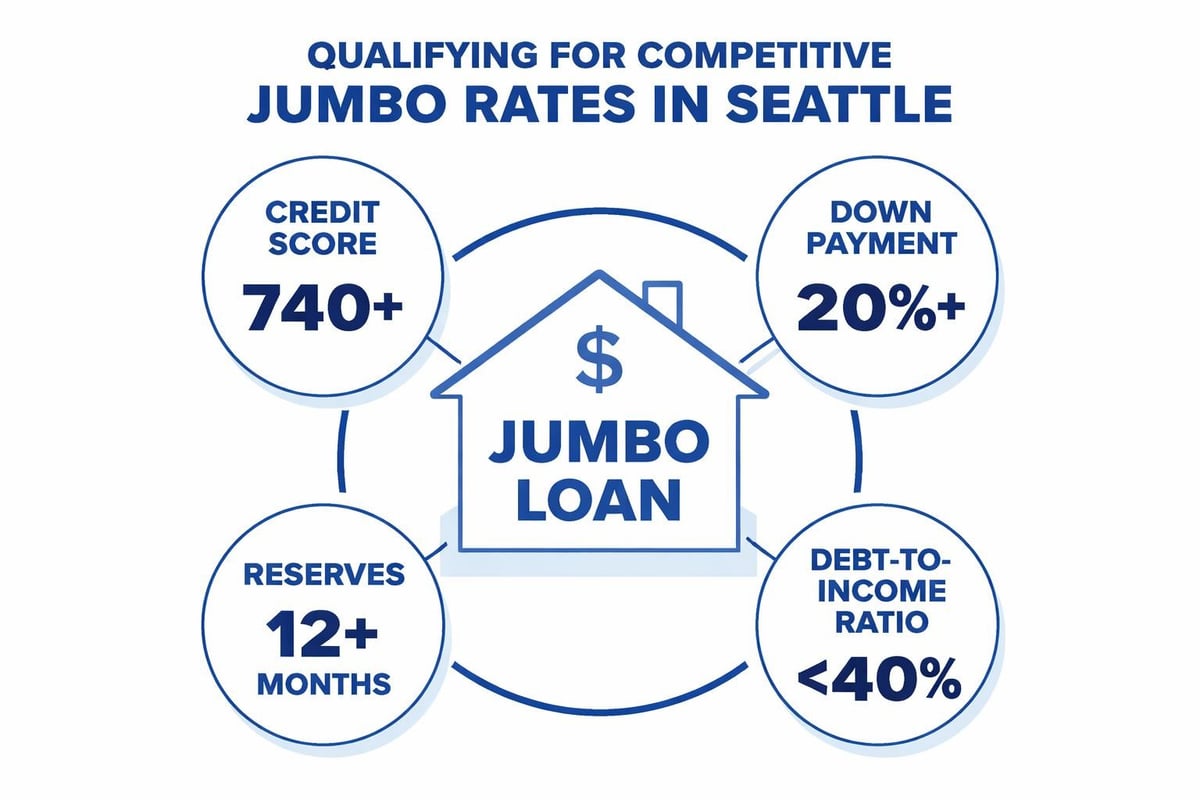

Credit scores play an outsized role in jumbo rate pricing. While conforming loans may be available with scores as low as 620, jumbo lenders typically require minimum scores of 680 to 700, with the best rates reserved for borrowers above 740.

Credit Score Rate Tiers:

- 760+: Best available jumbo rates

- 740-759: Slight rate adjustment (typically 0.125% to 0.25%)

- 720-739: Moderate pricing adjustment (0.25% to 0.50%)

- 680-719: Higher rates and potentially reduced loan-to-value limits

Down Payment and Loan-to-Value Requirements

Down payment size significantly influences both approval odds and rate pricing. Most jumbo lenders require at least 10% down, though 20% is standard for competitive rates.

Borrowers in Shoreline, Lynnwood, or Lake Forest Park purchasing homes in the $900,000 to $1.1 million range should expect:

- 20% down (80% LTV): Standard jumbo rates apply

- 15% down (85% LTV): Rate adjustment of 0.25% to 0.375%

- 10% down (90% LTV): Rate adjustment of 0.50% to 0.75% plus possible mortgage insurance

Larger down payments below 80% LTV can sometimes qualify for rate discounts, particularly for super-jumbo loans above $2 million.

Income Documentation and Debt-to-Income Standards

Jumbo lenders maintain strict debt-to-income (DTI) ratio requirements, typically capping total DTI at 43% to 45%, though some portfolio products may extend to 50% for exceptionally strong borrowers.

Qualifying RSUs and Stock Compensation

For Seattle-area tech professionals, properly documenting and qualifying restricted stock units (RSUs), stock options, and bonus income is critical to maximizing buying power with jumbo loans. According to Experian’s guidance on jumbo mortgages, lenders require extensive documentation for non-W2 income.

Acceptable Stock Compensation Documentation:

- Two years of vesting history and tax returns showing RSU income

- Current vesting schedule from employer HR department

- YTD paystubs reflecting stock income

- Employer verification letter confirming ongoing compensation structure

Most jumbo lenders will average two years of documented stock income, though some portfolio products allow for first-year RSU income if sufficiently documented and likely to continue.

Reserve Requirements

Cash reserves-liquid assets remaining after closing-represent another key qualification criterion that influences jumbo rates. Lenders typically require:

- 6 months reserves for loan amounts $750,000 to $1.5 million

- 9 to 12 months reserves for loans $1.5 million to $2.5 million

- 12 to 18 months reserves for super-jumbo loans above $2.5 million

Reserves can include checking accounts, savings, investment accounts, retirement accounts (with 30% to 40% discounting), and vested stock holdings.

Strategies to Secure Better Jumbo Rates

Positioning yourself as a low-risk borrower directly translates to more favorable jumbo rates. Several strategic approaches can improve your rate pricing.

Timing Your Application

Rate locks typically range from 30 to 60 days, though extended locks up to 90 days are available for a fee. In Seattle's fast-paced market, particularly in competitive neighborhoods across Bellevue, Redmond, and Kirkland, coordinating your rate lock with your purchase timeline prevents rate exposure.

Working with an experienced mortgage broker allows you to monitor daily rate sheets and lock when pricing improves, rather than being restricted to a single lender's rate movements.

Relationship Pricing and Portfolio Products

Many banks offer preferred pricing to existing customers with substantial deposits, investment accounts, or business relationships. These relationship discounts can range from 0.125% to 0.50% off standard jumbo rates.

Portfolio jumbo products from lenders who retain loans on their balance sheets often provide more flexibility in:

- Debt-to-income ratio tolerance

- Documentation requirements for self-employed borrowers

- Property type approval (condos, investment properties)

- Loan amount maximums

Rate Buydown Options

Paying discount points-prepaid interest paid at closing-reduces your ongoing interest rate. Each point (1% of the loan amount) typically reduces your rate by 0.20% to 0.25%, though the exact exchange varies by lender and market conditions.

| Points Paid | Rate Reduction | Cost on $1.2M Loan | Break-Even Period |

|---|---|---|---|

| 0 | Baseline | $0 | N/A |

| 1 | -0.25% | $12,000 | ~45 months |

| 2 | -0.50% | $24,000 | ~48 months |

For borrowers planning to stay in their Mill Creek or Everett home long-term, buying down the rate makes financial sense. However, those anticipating a move within five years typically benefit from minimizing upfront costs.

Comparing Jumbo Loan Options

Not all jumbo products are created equal. Understanding the distinctions helps you select the best fit for your financial situation and goals.

Fixed-Rate vs Adjustable-Rate Jumbo Loans

Fixed-rate jumbo mortgages provide payment stability and rate protection, making them ideal for long-term homeownership. The jumbo mortgage calculator tools available online help compare total costs across different rate scenarios.

Adjustable-rate mortgages (ARMs) offer lower initial rates, typically 0.50% to 1.00% below comparable fixed products. Common ARM structures include:

- 7/1 ARM: Fixed for seven years, then annual adjustments

- 10/1 ARM: Fixed for ten years, then annual adjustments

- 5/1 ARM: Fixed for five years, then annual adjustments

For professionals expecting significant income growth or planning to relocate within the fixed period, ARMs can provide substantial savings. However, rate adjustment caps and worst-case scenarios must be carefully evaluated.

Conventional Jumbo vs Portfolio Jumbo

Conventional jumbo loans follow standardized underwriting guidelines and are sold to private investors. Portfolio jumbo products are retained by the originating lender, allowing more flexibility but sometimes carrying slightly higher rates.

When Portfolio Jumbo Makes Sense:

- Self-employment with complex income documentation

- DTI ratios above 45%

- Unique property types or locations

- Foreign national borrowers

- Super-jumbo amounts exceeding $3 million

Regional Considerations for Seattle-Area Jumbo Borrowers

Seattle's specific market characteristics influence both jumbo loan availability and pricing strategies.

Conforming Loan Limit Impact

The 2026 conforming loan limit increase to $832,750 has shifted the threshold between conforming and jumbo territory. This adjustment by the Federal Housing Finance Agency means some borrowers who previously required jumbo financing now qualify for conforming products with potentially more favorable terms.

However, many Seattle neighborhoods still push buyers into jumbo territory:

- Median home prices in Madison Park, Laurelhurst, and Montlake regularly exceed $1.2 million

- Waterfront properties in Kirkland and Bellevue frequently surpass $2 million

- New construction in downtown Seattle condos often ranges from $900,000 to $1.5 million

Competitive Market Dynamics

Seattle's competitive purchase environment demands fast closings and strong offers. Jumbo loans can close in as few as 9 business days with the right documentation and lender efficiency, providing a competitive advantage in multiple-offer situations.

Pre-approval strength matters significantly. A comprehensive pre-approval with income verification, asset documentation, and credit review complete carries far more weight than a basic pre-qualification letter, particularly for jumbo amounts.

Common Questions About Jumbo Rates

Are Jumbo Rates Always Higher Than Conforming Rates?

Not necessarily. While jumbo rates traditionally ran higher than conforming rates, market conditions in recent years have occasionally reversed this relationship. Well-qualified borrowers with excellent credit, substantial down payments, and strong reserves sometimes access jumbo rates that match or beat conforming pricing.

This occurs because jumbo lenders compete aggressively for low-risk borrowers, and without the guarantee fees charged by Fannie Mae and Freddie Mac, some portfolio lenders can offer competitive pricing to preferred customers.

How Much Income Do I Need for a Jumbo Loan?

Income requirements vary based on loan amount, debt obligations, and local property taxes. For a $1 million jumbo loan in Seattle with 20% down, monthly principal and interest at 6.75% totals approximately $5,185, with property taxes and insurance adding another $1,500 to $2,000 depending on location.

Using the standard 43% DTI maximum, you'd need monthly gross income of approximately $15,000, or $180,000 annually, assuming minimal other debt obligations. Higher loan amounts require proportionally higher income, though borrowers with excellent credit and substantial reserves may qualify with slightly higher DTI ratios.

Can I Refinance a Jumbo Loan?

Yes, jumbo refinancing follows similar processes to jumbo purchase loans. Homeowners in Shoreline, Lynnwood, or surrounding areas may refinance to:

- Secure lower jumbo rates when market conditions improve

- Switch from an ARM to fixed-rate stability

- Eliminate mortgage insurance after reaching 20% equity

- Access equity for renovations or investments

Refinancing requires re-qualifying under current jumbo standards, including credit score, DTI ratio, and reserve requirements. Market appreciation across Seattle has provided many homeowners with substantial equity, making refinancing more accessible.

How Do Points Affect Jumbo Rates?

Discount points provide a direct mechanism to reduce your jumbo rate by prepaying interest. The cost-benefit analysis depends on your expected holding period and available capital.

For jumbo borrowers with significant cash reserves who plan long-term ownership in their Seattle-area home, buying points often makes financial sense. However, those prioritizing liquidity or anticipating refinancing within a few years typically benefit from zero-point pricing.

What Documentation Do Jumbo Lenders Require?

Jumbo loans demand comprehensive documentation across all qualification areas:

Income Verification:

- Two years of personal and business tax returns (if self-employed)

- Two years of W-2s

- 30 days of paystubs

- Verification of employment directly from employer

- Documentation of bonus, commission, or stock compensation history

Asset Documentation:

- Two to three months of bank statements for all accounts

- Investment account statements

- Retirement account statements

- Explanation letters for large deposits

- Gift letters if using gifted down payment funds

Credit and Liabilities:

- Tri-merge credit report

- Explanation letters for any derogatory credit items

- Documentation of all monthly debt obligations

- Proof of debt payoff if paying off accounts to qualify

This extensive documentation requirement means jumbo borrowers should start organizing financial records early in the process, particularly when qualifying complex income like RSUs from Seattle tech employers.

Advanced Jumbo Rate Strategies for High-Net-Worth Borrowers

Sophisticated borrowers can employ several strategies to optimize their jumbo financing beyond simply securing the lowest rate.

Asset Depletion Mortgages

For borrowers with substantial investment assets but limited documented income-such as retirees or those living on investment income-asset depletion jumbo programs calculate qualifying income based on liquid assets divided by the loan term.

For example, a borrower with $3 million in investment accounts applying for a $1 million jumbo loan might qualify based on $100,000 annual income ($3 million divided by 30 years), regardless of actual documented cash flow.

Private Banking Jumbo Solutions

Major banks offer specialized jumbo products for private banking clients with significant relationship deposits. These programs may include:

- Discounted rates based on combined deposit and investment balances

- Streamlined approval processes with dedicated underwriting teams

- Higher loan amounts (up to $10 million or more)

- More flexible property type approval

The relationship requirements typically start at $250,000 to $500,000 in deposits, though true private banking tiers often require $1 million or more.

Interest-Only Jumbo Structures

Interest-only payment options allow borrowers to pay only the interest portion for an initial period (typically 5 to 10 years), significantly reducing monthly obligations. This strategy works well for:

- High-income professionals expecting substantial compensation growth

- Borrowers managing significant stock compensation with irregular vesting schedules

- Real estate investors maximizing cash flow from rental properties

- Individuals expecting large cash inflows (business sale, inheritance) within the interest-only period

After the interest-only period, the loan fully amortizes over the remaining term, resulting in significantly higher payments. This requires careful planning and income stability.

Working With a Seattle Jumbo Mortgage Specialist

Navigating jumbo rates and qualification requirements benefits significantly from specialized expertise. The complexities of documenting tech compensation, coordinating fast closings in competitive markets, and accessing portfolio products require experience specific to Seattle's market dynamics.

What to Look for in a Jumbo Lender

When comparing jumbo mortgage options across Seattle, Bellevue, Redmond, and surrounding cities, evaluate:

Pricing Competitiveness:

- Daily rate sheets and transparent pricing adjustments

- Willingness to negotiate fees and closing costs

- Access to multiple investor products for comparison

Underwriting Expertise:

- Experience qualifying RSUs and stock compensation

- Understanding of tech industry compensation structures

- Ability to navigate complex income documentation

Closing Speed:

- Average closing timeline for jumbo purchases

- Dedicated underwriting and processing teams

- Communication protocols and borrower updates

Track Record:

- Client reviews and testimonials specific to jumbo transactions

- Years of experience in the Seattle market

- Professional credentials and licensing

According to Zillow’s jumbo mortgage resources, getting pre-approved before house hunting strengthens your position significantly, particularly in competitive Seattle neighborhoods where sellers often receive multiple offers.

Rate Shopping Best Practices

Comparing jumbo rates across multiple lenders ensures you secure competitive pricing, but the comparison must account for all cost components:

- Base interest rate

- Discount points or lender credits

- Origination fees

- Third-party closing costs

- Rate lock period and extension policies

Request Loan Estimates from at least three lenders on the same day, as jumbo rates can shift daily. Compare the "Total Loan Costs" section on page 2 of each Loan Estimate for the most accurate cost comparison.

Working with a mortgage broker provides access to multiple wholesale lenders simultaneously, allowing real-time rate shopping without submitting separate applications to each institution.

Understanding jumbo rates and positioning yourself as a strong borrower makes the difference between paying tens of thousands more in interest versus securing optimal financing for your Seattle-area home. From credit optimization to documentation preparation to timing your rate lock strategically, every element contributes to your final pricing. Whether you're purchasing in Seattle, refinancing in Bellevue, or exploring investment properties in Redmond, working with an experienced mortgage professional who specializes in jumbo loans and tech compensation ensures you navigate this complex landscape successfully. Mortgage Reel brings 25+ years of expertise helping Seattle homebuyers secure competitive jumbo financing, with advanced underwriting capabilities and the ability to close in as few as 9 business days-reach out today to explore your options.