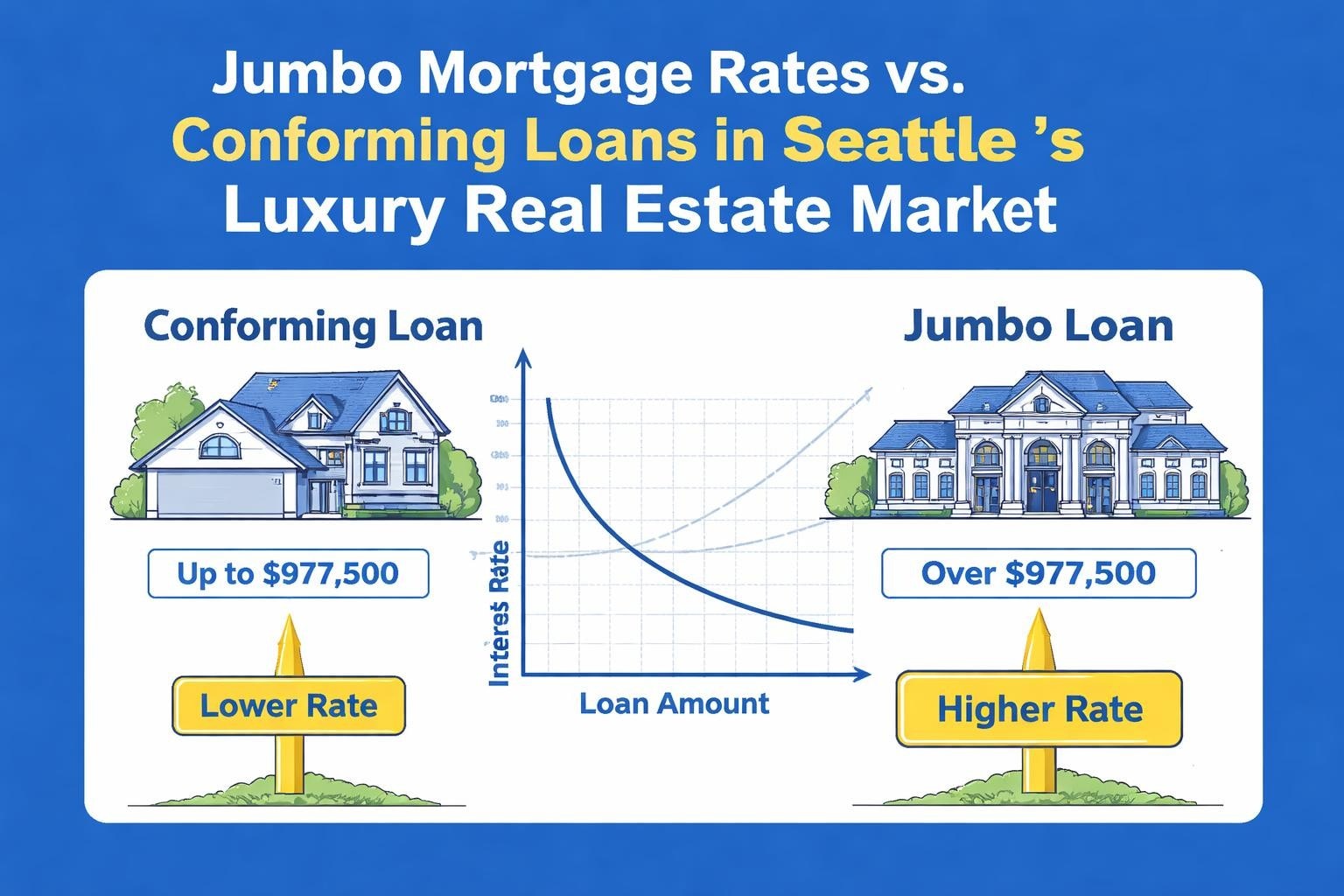

Navigating the Seattle luxury housing market requires a solid understanding of jumbo rates mortgage financing. For homebuyers purchasing properties above the conforming loan limit, which stands at $1,063,750 in most of Washington state for 2026, jumbo loans represent the primary financing option. These specialized mortgage products come with unique qualification requirements, pricing structures, and strategic considerations that differ significantly from conventional loans. Whether you're eyeing waterfront estates in Shoreline, tech-executive homes in Redmond, or luxury condos in downtown Seattle, understanding how jumbo rates work empowers you to make confident financial decisions in one of the nation's most competitive real estate markets.

What Makes Jumbo Mortgage Rates Different

Jumbo rates mortgage products stand apart from conventional loans due to the increased risk lenders assume when financing higher loan amounts. Unlike conforming loans, jumbo mortgages cannot be purchased by Fannie Mae or Freddie Mac, meaning lenders hold these loans in their own portfolios or sell them to private investors. This fundamental difference affects pricing, underwriting standards, and availability.

The relationship between loan size and interest rates isn't always straightforward. While jumbo rates historically carried a premium over conforming rates, market conditions in 2026 have created periods where the spread narrows or even inverts. Current jumbo mortgage rates often reflect broader economic factors including Federal Reserve policy, investor appetite for mortgage-backed securities, and regional housing market dynamics.

Rate Pricing Factors for Jumbo Loans

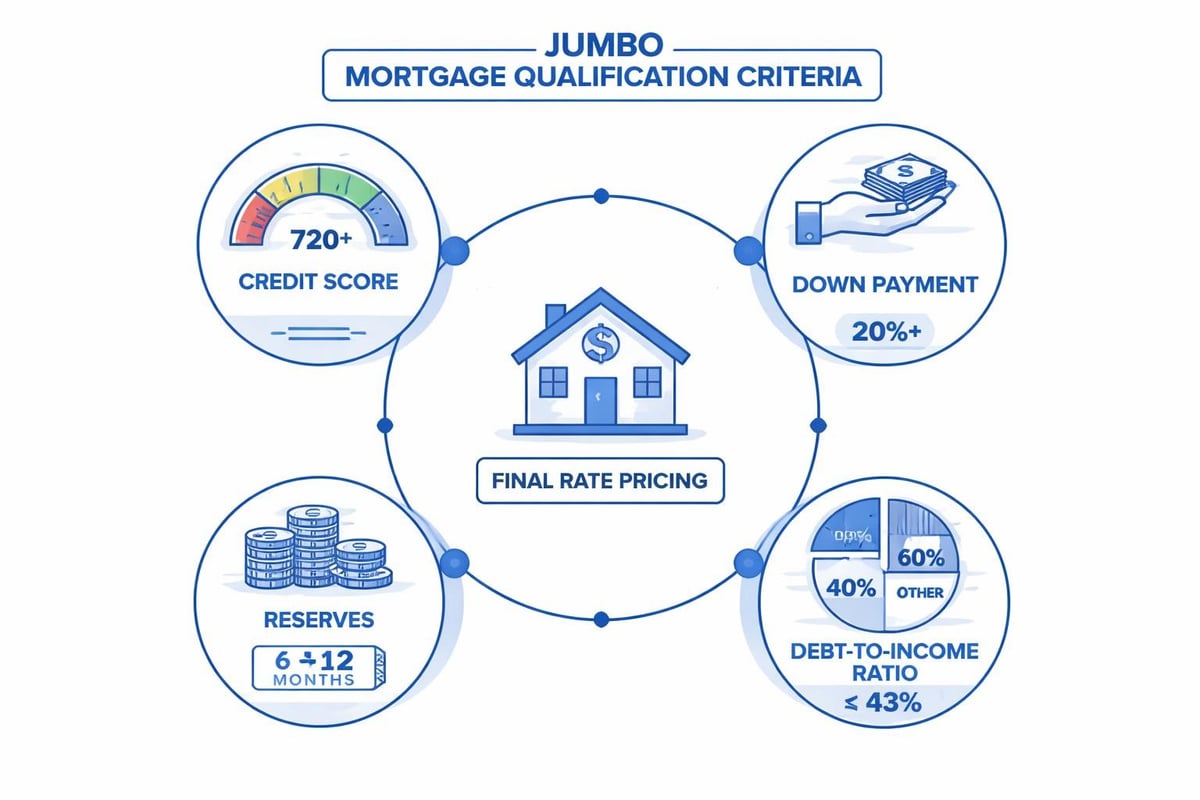

Several critical elements determine your final jumbo rates mortgage pricing:

- Credit score requirements: Most lenders require minimum scores of 700 for competitive rates, with the best pricing reserved for borrowers above 740

- Down payment amount: Larger down payments (typically 20% minimum, preferably 25% or more) significantly improve rate offerings

- Debt-to-income ratio: Lenders prefer DTI ratios below 43%, though qualified borrowers may extend to 45% with compensating factors

- Loan amount: Super jumbo loans exceeding $2 million may carry additional rate adjustments

- Property type: Single-family primary residences receive the most favorable pricing compared to condos, second homes, or investment properties

- Reserve requirements: Demonstrating 12-24 months of mortgage payments in liquid reserves strengthens your rate position

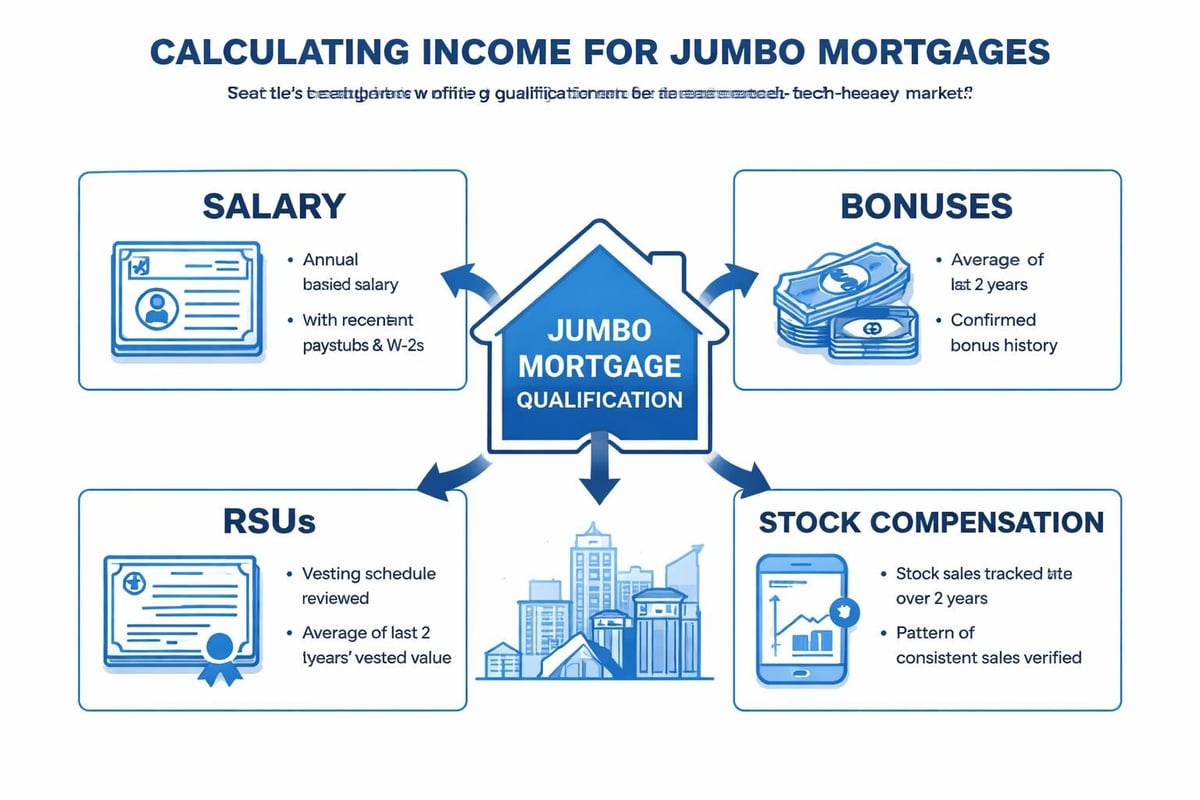

Documentation standards for jumbo loans exceed conventional loan requirements. Lenders typically require two years of tax returns, recent pay stubs, comprehensive asset statements, and detailed employment verification. For Seattle-area tech professionals with stock compensation, qualifying RSUs, ESPP proceeds, and bonus income requires specialized underwriting expertise to maximize buying power without triggering rate penalties.

Current Market Trends Affecting Jumbo Rates Mortgage Pricing

The Seattle housing market presents unique challenges and opportunities for jumbo borrowers in 2026. Median home prices in neighborhoods like Madison Park, Laurelhurst, and West Seattle's Alki area frequently exceed conforming loan limits, making jumbo financing essential for local buyers.

National jumbo mortgage rate trends show rates fluctuating between 6.25% and 7.15% for well-qualified borrowers on 30-year fixed products as of March 2026. However, regional variations exist. The Pacific Northwest, with its concentration of high-income tech workers and limited luxury inventory, often sees competitive jumbo rate offerings as lenders compete for qualified borrowers.

Comparing Loan Products and Terms

| Loan Type | Typical Rate Range | Down Payment | Credit Minimum | Reserve Requirements |

|---|---|---|---|---|

| 30-Year Fixed Jumbo | 6.35% – 7.15% | 20% – 25% | 700+ | 12-24 months |

| 15-Year Fixed Jumbo | 5.85% – 6.65% | 20% – 25% | 700+ | 12-24 months |

| 7/1 ARM Jumbo | 5.95% – 6.75% | 20% – 25% | 720+ | 18-24 months |

| Conforming 30-Year | 6.15% – 6.85% | 3% – 20% | 620+ | 2-6 months |

Recent changes to conforming loan limits have shifted the jumbo threshold upward, allowing more borrowers to access conventional financing. In high-cost King County areas including Bellevue, Kirkland, and Redmond, understanding where your purchase price falls relative to these limits significantly impacts your financing strategy and overall costs.

The spread between jumbo and conforming rates remains a critical consideration. When evaluating properties near the conforming limit boundary, buyers in areas like Lake Forest Park or Mill Creek should calculate total costs across both loan types. Sometimes structuring a purchase to stay within conforming limits through larger down payments yields better long-term value despite requiring more cash upfront.

Qualification Strategies for Competitive Jumbo Rates

Securing the best jumbo rates mortgage pricing requires strategic preparation months before home shopping begins. Unlike conforming loans with more standardized guidelines, jumbo underwriting involves greater lender discretion, creating opportunities for well-prepared borrowers to negotiate favorable terms.

Credit optimization represents the foundation of jumbo rate strategy. Beyond the minimum 700 score, each 20-point increment above 740 typically improves pricing by 0.125% to 0.250%. For borrowers in Everett or Lynnwood planning jumbo purchases, spending six months improving credit scores through strategic debt paydown and credit utilization management often saves thousands in interest costs.

Documentation Best Practices

Comprehensive documentation preparation accelerates approval timelines and strengthens rate lock negotiations:

- Organize two full years of personal and business tax returns with all schedules and K-1s if applicable

- Compile three months of statements for all checking, savings, investment, and retirement accounts

- Document the source of down payment funds including seasoning periods for gifted funds or asset sales

- Prepare employment verification with direct supervisor contact information and recent pay history

- Calculate and document all income sources including base salary, bonuses, RSUs, ESPP, and rental income

- Address any credit anomalies proactively with written explanations for recent inquiries or score changes

For Seattle-area professionals with complex compensation structures, early consultation with experienced jumbo lenders prevents surprises during underwriting. Stock-based compensation requires specialized calculation methods, with many lenders averaging two years of vesting history or applying conservative discounts to unvested equity when determining qualifying income.

Rate Lock Timing and Strategy Considerations

Jumbo rates mortgage pricing changes rapidly based on daily market conditions. Understanding rate lock mechanics and timing strategies protects borrowers from adverse rate movements while preserving flexibility when beneficial.

Standard rate locks range from 30 to 60 days, with extensions available for fees typically ranging from 0.125% to 0.375% of the loan amount per 15-day period. In Seattle's competitive market where properties often close in 30-45 days, coordinating your lock period with realistic closing timelines prevents unnecessary extension costs.

Float-down options provide protection against rate decreases during your lock period, though they typically cost 0.125% to 0.250% upfront and include minimum improvement thresholds (often 0.25% or greater). For borrowers in markets like Shoreline or Redmond where purchase timelines extend due to inspection negotiations or appraisal delays, float-down provisions offer valuable flexibility.

When to Lock Your Jumbo Rate

Market conditions and personal circumstances determine optimal lock timing:

- Lock immediately when rates are at historical lows or trending upward consistently

- Consider floating when economic indicators suggest rate decreases ahead or if your closing timeline exceeds 45 days

- Use float-down locks when uncertain about market direction but uncomfortable with full floating risk

- Negotiate lock extensions early if delays appear likely, as last-minute extensions carry premium pricing

Working with lenders offering in-house jumbo portfolio products sometimes provides more flexibility on rate lock policies compared to lenders who must adhere to investor guidelines. This distinction matters particularly for borrowers managing complex transactions involving contingent sales, new construction, or investment property exchanges.

Portfolio Lenders Versus Wholesale Jumbo Products

Understanding where your jumbo rates mortgage originates impacts pricing, flexibility, and approval likelihood. Portfolio lenders retain jumbo loans on their own balance sheets, allowing greater underwriting discretion and sometimes more competitive pricing for specific borrower profiles. Wholesale jumbo products follow investor guidelines with less flexibility but sometimes offer better rates for straightforward scenarios.

Seattle-area credit unions and regional banks often maintain robust jumbo portfolio programs tailored to local market conditions and borrower profiles. These lenders may offer advantages for self-employed borrowers, those with unconventional income documentation, or properties that don't fit standard investor guidelines.

National wholesale jumbo investors provide scale and competitive pricing through aggregated loan programs. Mortgage brokers access multiple investors simultaneously, comparing offerings to secure optimal terms for each borrower's unique situation. This approach works particularly well for W-2 employees with straightforward income, strong credit, and conforming property types in areas like Kirkland or Bellevue.

| Lender Type | Advantages | Considerations |

|---|---|---|

| Portfolio Lender | Flexibility on guidelines, relationship pricing, faster decisions | Potentially higher rates, limited availability |

| Wholesale Investor | Competitive rates, consistent standards, broad product range | Strict guidelines, less flexibility |

| Correspondent Lender | Balance of flexibility and pricing, local servicing option | Rate dependent on investor appetite |

Calculating True Costs Beyond the Interest Rate

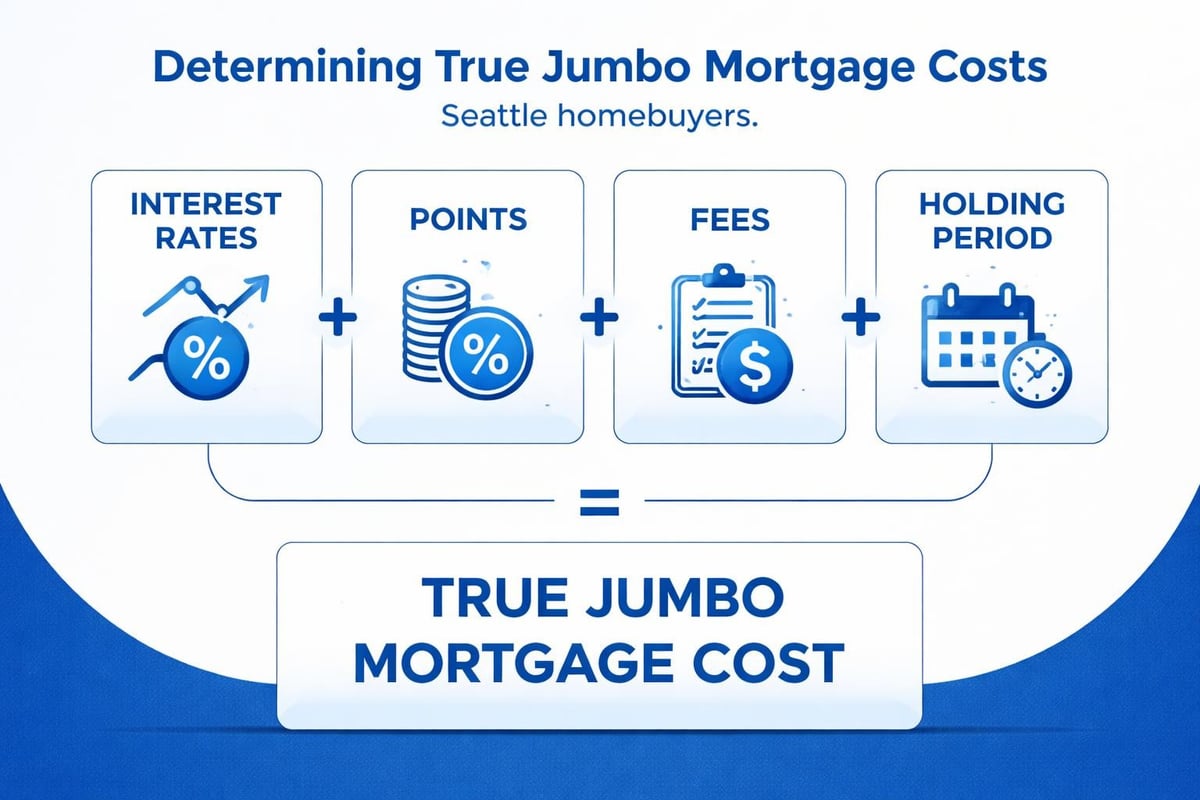

Jumbo rates mortgage comparison requires analysis beyond the base interest rate. Annual percentage rate (APR) incorporates closing costs, points, and fees into a standardized comparison metric, though even APR doesn't capture the complete financial picture for shorter holding periods or specific scenarios.

Discount points allow borrowers to pay upfront fees in exchange for reduced interest rates, with each point typically costing 1% of the loan amount and reducing the rate by approximately 0.25%. For a $1.5 million jumbo loan in Seattle, one point costs $15,000 but reduces monthly payments by roughly $200 to $225, creating a breakeven period of approximately 67 to 75 months. Borrowers planning to hold properties for 10-plus years often benefit from paying points, while those expecting shorter ownership periods should minimize upfront costs.

Fee Structures to Compare

Comprehensive jumbo loan comparison requires analyzing:

- Origination fees: Typically 0% to 1% of loan amount, negotiable based on rate selection

- Underwriting and processing charges: Usually $800 to $1,500 combined

- Appraisal costs: Jumbo properties often require $600 to $1,200 for complex or high-value homes

- Title and escrow fees: Scale with purchase price, typically $2,000 to $5,000 for jumbo transactions

- Property insurance: Luxury homes carry higher premiums, often $3,000 to $8,000 annually in Seattle

Jumbo mortgage calculators help model different scenarios, comparing total costs across various rate and point combinations. These tools prove particularly valuable when evaluating whether to pay points, select adjustable-rate products, or structure loans to stay within conforming limits through larger down payments.

Adjustable-Rate Jumbo Products for Specific Scenarios

While 30-year fixed jumbo rates mortgage products dominate the market, adjustable-rate mortgages (ARMs) deserve consideration for certain borrower profiles and property intentions. Jumbo ARMs typically offer initial fixed periods of 5, 7, or 10 years before adjusting annually based on index performance plus a predetermined margin.

Rate advantages for jumbo ARMs compared to fixed products range from 0.375% to 0.625% depending on the initial fixed period length. For a $2 million jumbo loan in Redmond, this translates to approximately $625 to $1,040 in monthly savings during the fixed period. Borrowers certain they'll sell, refinance, or pay down principal substantially within the fixed period benefit from these savings without exposure to future rate adjustments.

Cap structures limit adjustment risk through periodic and lifetime rate increase restrictions. Standard jumbo ARM caps follow a 2/2/5 or 5/2/5 structure, meaning the first adjustment can increase rates by up to 2% or 5%, subsequent annual adjustments by up to 2%, and lifetime increases cannot exceed 5% above the initial rate. Understanding these mechanisms helps borrowers evaluate worst-case scenarios when considering ARM products.

Ideal ARM Candidates

Jumbo ARM products work best for:

- Relocating professionals expecting job transfers within 5-7 years, common among Seattle tech workers

- Strategic refinancers planning to restructure debt once property appreciation builds equity

- Bridge buyers purchasing luxury homes before selling existing properties, expecting quick payoff

- Aggressive prepayment planners targeting substantial principal reduction during the fixed period

- Rate environment speculators betting on lower rates in future years enabling favorable refinancing

Mill Creek and Lynnwood buyers purchasing starter luxury homes with plans to upgrade within a decade often find 7/1 or 10/1 jumbo ARMs provide optimal balance between savings and stability. The decision requires honest assessment of future plans, risk tolerance, and market outlook rather than simply choosing the lowest initial rate.

Tax Implications and Deduction Strategies

Jumbo mortgage interest deductibility changed substantially following the Tax Cuts and Jobs Act, with mortgage interest deductions now limited to interest on the first $750,000 of acquisition debt for loans originated after December 15, 2017. For jumbo borrowers in high-tax states like Washington, which has no state income tax but substantial property taxes, understanding these limitations impacts overall financing strategy.

Interest on jumbo loan amounts exceeding $750,000 remains tax-deductible if the original loan predates the December 2017 cutoff, or if the loan refinances qualifying pre-existing debt. Borrowers purchasing properties in Seattle's luxury neighborhoods should consult tax professionals about structuring acquisitions to maximize deductibility, potentially through separate financing vehicles or strategic use of taxable investment accounts for portions exceeding deductible limits.

Property tax deductions face separate SALT (state and local tax) limitations capping combined property tax, state income tax, and local tax deductions at $10,000 annually. While Washington's lack of state income tax allows the full $10,000 toward property tax deductions, luxury property owners in Bellevue or Kirkland with annual property taxes exceeding this threshold receive no federal deduction benefit for amounts above the cap.

Building Lender Relationships for Optimal Pricing

Jumbo rates mortgage pricing reflects not just market conditions but also lender competition for quality borrowers. Building relationships with multiple lender types-portfolio lenders, correspondent lenders, and wholesale brokers-creates competitive tension that often improves final terms by 0.125% to 0.375% compared to single-lender approaches.

Transparency during initial consultations establishes credibility that lenders reward with aggressive pricing. Providing complete financial pictures upfront, including all assets, liabilities, income sources, and property intentions, allows lenders to structure optimal solutions rather than generic rate quotes that may not reflect your final pricing.

Timing matters significantly in jumbo lending relationships. Engaging lenders 60 to 90 days before serious home shopping begins allows time for credit optimization, documentation preparation, and pre-approval positioning without pressure. Shoreline and Everett buyers entering competitive multiple-offer situations with comprehensive pre-approvals demonstrating verified qualification for jumbo financing stand out to sellers compared to generic pre-qualification letters.

Questions to Ask Potential Jumbo Lenders

Vet jumbo lenders thoroughly by asking:

- What is your current volume of jumbo loan originations in Seattle and how does portfolio versus wholesale split?

- How do you handle complex income situations including stock compensation, and what documentation do you require?

- What is your typical timeline from application to clear-to-close for jumbo purchases?

- Do you offer relationship pricing for clients who maintain deposits, investments, or other products with your institution?

- What rate lock flexibility do you provide, and what are the specific costs for extensions or float-down options?

- How do you handle appraisal management for unique or luxury properties that may require specialized valuations?

Lenders specializing in Seattle's market understand local property types, typical transaction timelines, and the specific challenges of waterfront estates, view properties, and luxury condos that dominate the jumbo price range. This local expertise accelerates approvals and prevents surprises during underwriting.

Investment Properties and Second Home Jumbo Financing

Jumbo rates mortgage pricing for investment properties and vacation homes carries additional considerations beyond primary residence financing. Rate premiums typically range from 0.375% to 0.750% compared to primary residence jumbo rates, reflecting higher default risk statistics for non-primary properties.

Down payment requirements increase substantially for investment and second home jumbo purchases, with most lenders requiring 25% to 30% down regardless of borrower creditworthiness. These higher equity requirements protect lenders against potential market corrections while ensuring borrowers maintain meaningful financial commitment to the property.

Debt-to-income calculations for investment properties include projected rental income, though lenders typically apply conservative adjustments. Most underwriters count only 75% of expected rental income while including 100% of the projected mortgage payment, property taxes, insurance, and HOA fees. This asymmetric treatment means investment property purchases often require significantly higher income qualification than comparable primary residence scenarios.

Lake Forest Park and Mill Creek investors purchasing luxury single-family rentals should anticipate reserve requirements extending to 18 to 24 months of mortgage payments across all financed investment properties, not just the subject property. These substantial liquidity requirements ensure borrowers can weather vacancy periods or unexpected maintenance expenses without payment disruptions.

Preparing for the Jumbo Application Process

Successful jumbo rates mortgage applications reflect months of preparation rather than spontaneous decisions. The enhanced scrutiny and documentation requirements mean borrowers benefit from systematic approaches addressing each underwriting component methodically.

Asset seasoning represents a critical but often overlooked requirement. Most jumbo lenders require down payment and reserve funds to season in accounts for at least two months before application. Large deposits during this period trigger detailed documentation requirements including complete paper trails showing fund sources. Seattle-area borrowers should plan major financial transactions like stock sales, bonuses, or account transfers well in advance of jumbo applications.

Credit management during the pre-application period requires discipline and strategy. Avoid opening new credit accounts, closing existing cards, making large purchases on credit, or co-signing loans for others. Each of these activities can impact credit scores or debt-to-income ratios in ways that affect jumbo qualification or pricing. Even seemingly minor changes like increasing credit card balances from 10% to 30% utilization can reduce scores by 20 to 40 points, potentially costing 0.125% to 0.250% in rate pricing.

Pre-Approval Checklist

Complete these steps before formal jumbo pre-approval:

- Review credit reports from all three bureaus and dispute any inaccuracies at least 90 days before applying

- Calculate realistic debt-to-income ratios including projected jumbo payment and property expenses

- Document all income sources with the specific evidence lenders require for your income type

- Verify down payment and reserve funds are properly seasoned and documented

- Research property types, neighborhoods, and price ranges to focus search efforts

- Connect with real estate professionals experienced in luxury and jumbo-financed transactions

- Compare multiple lender offerings on standardized scenarios to identify competitive options

Redmond and Kirkland buyers working with real estate agents familiar with jumbo transactions benefit from coordinated strategies aligning financing preparation with property search timelines. These professionals understand that jumbo purchases require more extensive due diligence periods for inspections, appraisals, and final underwriting, influencing offer structure and contingency timelines.

Market-Specific Considerations for Seattle Jumbo Buyers

Seattle's luxury real estate market presents unique characteristics affecting jumbo rates mortgage strategy. The concentration of high-income tech professionals creates strong demand for properties in the $1.5 million to $3 million range, while limited inventory in desirable neighborhoods maintains price stability even during broader market corrections.

Condo financing in Seattle requires special attention as many luxury buildings face warrants or deferred maintenance issues affecting financeability. Jumbo lenders scrutinize condo association financials, reserve funding levels, and litigation history more intensively than conforming loan underwriters. Buildings with less than 10% commercial space, adequate reserves, and low delinquency rates receive standard financing treatment, while those with concerns may face rate premiums or reduced loan-to-value limits.

Waterfront and view properties throughout the greater Seattle area command premium prices but sometimes face appraisal challenges. Comparable sales for unique estates can be limited, requiring appraisers to make substantial adjustments that introduce subjectivity into valuations. Experienced jumbo lenders maintain relationships with specialized appraisers familiar with luxury property valuation methodologies, reducing the risk of low appraisals derailing transactions.

Current mortgage rate trends show broader economic factors influencing jumbo pricing alongside local market dynamics. Seattle borrowers should monitor Federal Reserve policy, inflation data, and treasury yields as leading indicators of likely jumbo rate direction in coming months. While timing the absolute bottom of rate cycles proves impossible, understanding trends helps inform lock timing and overall purchase timing decisions.

Alternative Structures for Large Purchase Financing

Beyond traditional jumbo rates mortgage products, high-net-worth borrowers sometimes benefit from alternative financing structures that optimize overall financial positioning. While these approaches don't work for every situation, they deserve consideration when specific circumstances align.

Portfolio line of credit financing allows borrowers to pledge investment portfolios as collateral for property purchases rather than traditional mortgages. These products typically offer rates tied to LIBOR or SOFR plus margins ranging from 2.00% to 3.50%, with the advantage of avoiding traditional mortgage underwriting, appraisals, and closing timelines. Institutions like Schwab offer these programs to qualified clients with substantial investment assets, though the floating rate structure and potential margin call provisions require careful risk assessment.

Private banking jumbo mortgages through wealth management relationships sometimes provide relationship pricing unavailable through traditional mortgage channels. Clients maintaining substantial deposits, investment accounts, or other banking products may receive rate discounts of 0.125% to 0.500% compared to standard jumbo offerings. These programs work particularly well for Bellevue or Seattle buyers with existing banking relationships and complex financial profiles benefiting from coordinated wealth management.

Hybrid Financing Approaches

Sophisticated borrowers sometimes structure transactions using multiple financing layers:

- Conforming first mortgage plus secondary financing to maximize lower-rate conventional loan benefits while financing the balance through HELOC or portfolio lines

- 80-10-10 structures with 80% first mortgage, 10% second mortgage or line of credit, and 10% down payment to avoid jumbo thresholds entirely

- Bridge loans covering short-term funding needs before permanent financing or asset liquidation occurs

- Seller financing for portions of luxury purchases where sellers benefit from installment sale tax treatment

Each alternative structure involves trade-offs between rate optimization, qualification simplicity, closing speed, and long-term flexibility. These approaches require coordination between mortgage professionals, wealth advisors, tax professionals, and real estate attorneys to ensure proper execution and optimal outcomes.

Understanding jumbo rates mortgage options empowers Seattle-area luxury homebuyers to make informed financing decisions aligned with their financial goals and market opportunities. Whether you're a tech professional leveraging stock compensation in Redmond, a physician purchasing a waterfront estate in Shoreline, or an executive relocating to Bellevue, specialized jumbo expertise makes the difference between adequate financing and truly optimized solutions. Keith Akada brings over 25 years of mortgage experience specifically serving Seattle's unique luxury market, with proven expertise qualifying complex income, navigating jumbo underwriting, and closing transactions in as few as 9 business days. Connect with Mortgage Reel to explore your jumbo financing options with a trusted local expert who has helped hundreds of clients successfully navigate Seattle's competitive luxury real estate market.