Buying your first home in the Greater Seattle area represents both an exciting milestone and a significant financial decision. With median home prices remaining elevated across Seattle, Bellevue, and surrounding communities, understanding loans for first time homebuyers becomes essential to making confident, informed choices. The good news is that multiple loan programs exist specifically designed to help new buyers overcome common obstacles like limited down payment savings and credit concerns. Whether you're a tech professional in Redmond evaluating stock compensation or a young family in Shoreline exploring conventional financing, the right mortgage strategy can transform homeownership from a distant dream into achievable reality.

Understanding First-Time Homebuyer Status

The definition of a first-time homebuyer extends beyond what many people assume. According to most lending guidelines, you qualify as a first-time buyer if you haven't owned a primary residence in the past three years. This means even if you previously owned a home, you may still access first-time buyer programs and benefits.

Key eligibility factors include:

- No ownership of a principal residence within 36 months

- Single parents who only owned with a former spouse

- Displaced homemakers who only owned with a spouse

- Individuals who only owned property not permanently affixed to a foundation

This broader definition opens opportunities for buyers in Mill Creek or Lake Forest Park who may have rented after selling a previous home years ago. Understanding your status helps determine which loan programs and assistance options you can access.

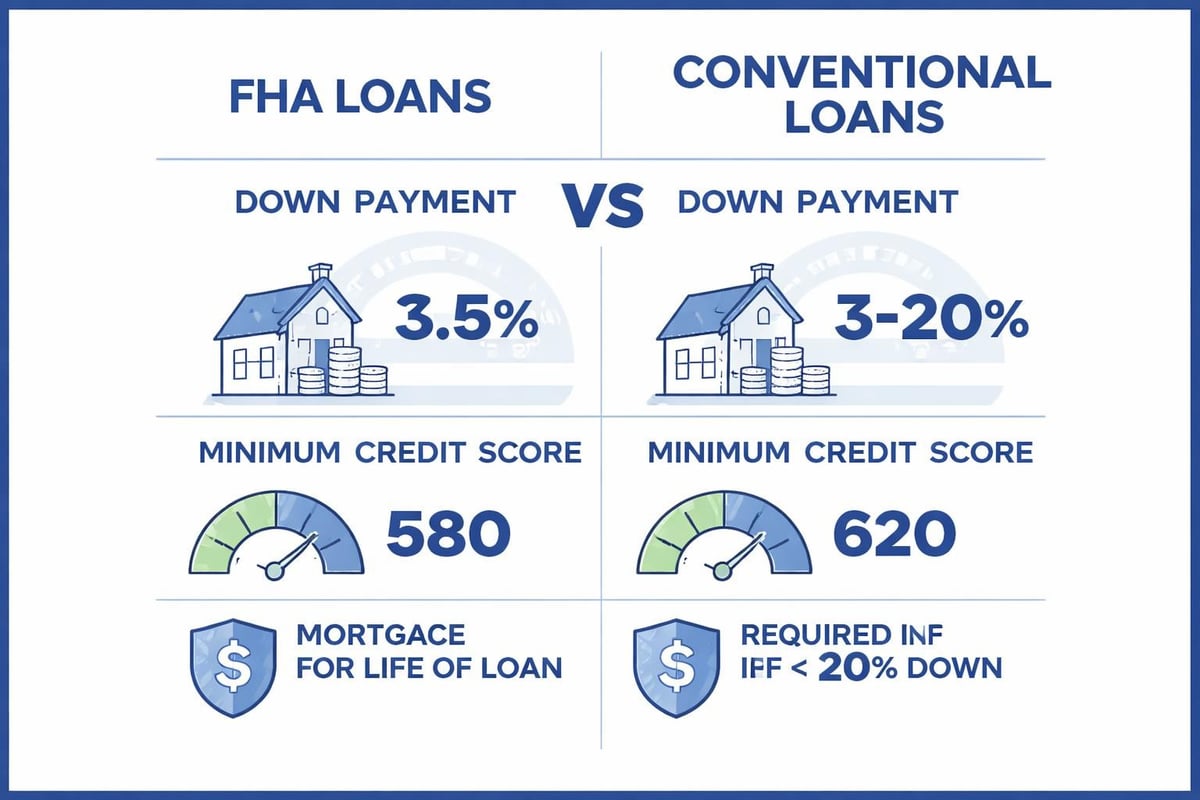

FHA Loans: The Most Popular First-Time Option

Federal Housing Administration (FHA) loans remain the most widely used financing solution for first-time buyers across Seattle and surrounding areas. These government-backed mortgages offer significant advantages for buyers with limited savings or credit histories that aren't yet pristine.

Down Payment and Credit Requirements

FHA loans require as little as 3.5% down for borrowers with credit scores of 580 or higher. For a $600,000 home in Lynnwood, that translates to just $21,000 down compared to the traditional 20% ($120,000) often associated with conventional mortgages.

Buyers with scores between 500-579 can still qualify with 10% down, though most lenders prefer higher scores. The Consumer Financial Protection Bureau offers an overview of different mortgage loan options to help you compare features across loan types.

Mortgage Insurance Considerations

FHA loans require both upfront and annual mortgage insurance premiums (MIP). The upfront premium of 1.75% can be rolled into your loan amount, while annual MIP ranges from 0.45% to 1.05% depending on your loan-to-value ratio and term.

| Loan Amount | Down Payment (3.5%) | Upfront MIP (1.75%) | Monthly MIP Estimate |

|---|---|---|---|

| $500,000 | $17,500 | $8,444 | $354/month |

| $700,000 | $24,500 | $11,821 | $496/month |

| $900,000 | $31,500 | $15,199 | $638/month |

Unlike conventional loans, FHA mortgage insurance typically remains for the life of the loan if you put down less than 10%. This long-term cost should factor into your decision-making process.

Gift Funds and Seller Concessions

FHA guidelines allow your entire down payment to come from gift funds provided by family members, employers, or charitable organizations. Sellers can also contribute up to 6% toward your closing costs, significantly reducing your out-of-pocket expenses. These flexible sourcing rules make FHA particularly attractive for loans for first time homebuyers in competitive markets like Everett or Shoreline.

Conventional Loans for First-Time Buyers

Conventional conforming loans backed by Fannie Mae and Freddie Mac have become increasingly accessible to first-time buyers through programs requiring as little as 3% down. These mortgages offer distinct advantages over FHA for qualified borrowers.

HomeReady and Home Possible Programs

Fannie Mae's HomeReady and Freddie Mac's Home Possible programs specifically target first-time and low-to-moderate income buyers. Both allow 3% down payments and offer flexible income qualifications, including boarder income and non-occupant co-borrower support.

Program highlights:

- 3% minimum down payment requirement

- Income limits apply (typically 80% of area median income)

- Reduced mortgage insurance rates

- First-time homebuyer education requirement

- Flexible credit score minimums (typically 620+)

For Seattle-area buyers, these programs work well in neighborhoods where property values align with conforming loan limits ($806,500 in 2026 for King County). Buyers in Lake Forest Park or Mill Creek can leverage these options effectively.

Private Mortgage Insurance (PMI) Advantages

Conventional loans require PMI when you put down less than 20%, but unlike FHA's permanent insurance, PMI automatically cancels once you reach 22% equity through payments and appreciation. In Seattle's appreciating market, this can happen relatively quickly.

Monthly PMI rates typically range from 0.3% to 1.5% annually, depending on your credit score and down payment. A buyer with a 740 credit score and 5% down might pay 0.5% annually, while someone with a 660 score and 3% down could pay 1.2%.

VA Loans for Eligible Veterans and Service Members

VA loans represent one of the most powerful financing tools available, offering zero down payment options without monthly mortgage insurance. If you're a veteran, active-duty service member, or qualifying surviving spouse in the Seattle area, this program deserves serious consideration.

Zero Down Without PMI

The VA home loan benefit eliminates two major obstacles for first-time buyers. You can purchase a home with no down payment while avoiding the monthly mortgage insurance costs that burden FHA and low-down conventional loans. The U.S. Department of Veterans Affairs outlines VA home loan benefits in comprehensive detail.

For a $650,000 home in Redmond, a VA borrower avoids the $22,750 down payment (3.5% FHA) and saves approximately $450 monthly by eliminating mortgage insurance. Over just five years, that's $27,000 in insurance savings alone.

Funding Fee and Exemptions

VA loans do require a one-time funding fee ranging from 1.4% to 3.6% depending on down payment and usage. However, veterans with service-connected disabilities receive complete funding fee exemptions. First-time VA loan users with zero down pay 2.15%, while those putting down 5% or more pay just 1.4%.

King County Loan Limits

In 2026, the VA loan limit for King County is $806,500 for standard entitlement. Veterans can borrow above this amount, but would need a down payment equal to 25% of the difference between the purchase price and the county limit. For most first-time buyers in Seattle, Shoreline, or Lynnwood, the current limits provide substantial purchasing power.

USDA Loans for Suburban and Rural Areas

United States Department of Agriculture (USDA) loans offer another zero-down option for eligible properties and borrowers. While Seattle proper doesn't qualify, certain areas in the broader region may be eligible for this program.

Some outer suburban and rural properties near Everett or beyond traditional King County boundaries could potentially qualify. USDA loans feature competitive interest rates, no down payment requirement, and relatively affordable mortgage insurance (0.35% annual guarantee fee).

Eligibility requirements include:

- Property must be in a USDA-eligible rural or suburban area

- Household income cannot exceed 115% of area median income

- Must demonstrate creditworthiness (typically 640+ credit score)

- Property must be your primary residence

Check current USDA eligibility maps to determine if properties you're considering qualify. These loans work exceptionally well for buyers seeking more affordable areas outside Seattle's urban core.

Down Payment Assistance Programs in Washington State

Washington State and local housing authorities offer various down payment assistance (DPA) programs that can be combined with FHA, conventional, and VA loans. These resources significantly reduce the cash needed to close for qualifying first-time buyers.

Washington State Housing Finance Commission

The Washington State Housing Finance Commission administers several programs providing down payment and closing cost assistance. Their House Key program offers conventional and FHA options with competitive rates and DPA for eligible borrowers.

House Key features:

- Down payment assistance up to 5% of loan amount

- Available with both conventional and FHA financing

- Income and purchase price limits apply

- Homebuyer education requirement

- Repayment not required if you remain in the home

King County and Local Options

King County periodically offers additional assistance through its housing authority. These programs often target specific income brackets or geographic areas, providing forgivable loans or grants to reduce upfront costs.

Explore first-time homebuyer programs available in each state to discover current opportunities. Programs change regularly, so working with a knowledgeable local mortgage broker ensures you access all available assistance.

Qualifying Income for Tech Professionals

Seattle's concentration of major tech employers creates unique opportunities and challenges for first-time buyers. Many Amazon, Microsoft, and Google employees receive significant compensation through restricted stock units (RSUs), bonuses, and equity grants that can be used to qualify for larger loan amounts.

Using RSUs and Stock Compensation

Lenders can count RSU income if you demonstrate a two-year history of receipt and likely continuation. The calculation typically uses a conservative average of vested stock over the previous two years, even accounting for market volatility.

For example, if you've received $80,000 in vested RSUs annually for two years and your vesting schedule shows continued grants, lenders can add a portion of that income to your base salary. This can dramatically increase your purchasing power when buying in competitive areas like Bellevue or Redmond.

Bonus Income Qualification

Regular annual bonuses follow similar treatment, requiring two-year histories and evidence of continuation. Variable compensation gets averaged, and underwriters may apply haircuts if income shows declining trends. However, for tech professionals with stable employment and consistent performance compensation, these calculations often add $50,000 to $150,000 in qualifying income.

Jumbo Loans for Higher-Priced Properties

When your desired home exceeds conforming loan limits ($806,500 in King County for 2026), you'll need a jumbo loan. These non-conforming mortgages follow stricter guidelines but remain accessible for qualified first-time buyers, especially those with substantial income or assets.

Jumbo Loan Requirements

Jumbo lenders typically require higher credit scores (usually 700+), larger down payments (often 10-20%), and lower debt-to-income ratios than conforming loans. Cash reserves of 6-12 months often become mandatory.

| Loan Type | Min. Credit Score | Min. Down Payment | Max DTI Ratio | Reserves Required |

|---|---|---|---|---|

| Jumbo First-Time | 700 | 10% | 43% | 6-12 months |

| Conventional | 620 | 3% | 50% | 2-6 months |

| FHA | 580 | 3.5% | 50% | 2-3 months |

Despite stricter requirements, tech professionals with substantial total compensation often qualify easily. The key is working with lenders experienced in evaluating complex income structures common in Seattle's employment market.

Interest Rates and Timing Your Purchase

Interest rate environments significantly impact affordability for loans for first time homebuyers. Understanding rate factors and timing strategies helps optimize your borrowing costs over the life of your mortgage.

Factors Affecting Your Rate

Multiple variables determine your specific interest rate beyond general market conditions. Credit scores, down payment size, loan type, property type, and occupancy all influence pricing.

Rate impact factors:

- Credit score: Each 20-point increment can affect rates by 0.125% to 0.5%

- Down payment: Higher down payments (10%+ vs 3%) typically reduce rates

- Loan type: VA loans often offer the lowest rates, followed by conventional and FHA

- Points: Paying upfront points can reduce your rate permanently

- Lock period: Longer rate locks (60+ days) may carry higher rates

A first-time buyer in Seattle with a 780 credit score, 10% down, and a conventional loan might receive a rate 0.75% lower than someone with a 660 score and 3% down on the same loan program.

Rate Buydowns and Seller Credits

Temporary buydowns allow you to reduce your interest rate for the first 1-3 years of the mortgage. A 2-1 buydown, for example, reduces your rate by 2% in year one and 1% in year two before returning to the note rate.

Sellers can contribute toward buydown costs through concessions, making this strategy particularly effective in buyer-favorable markets. When negotiating on properties in Mill Creek or Lynnwood, consider requesting seller credits for rate buydowns rather than purely price reductions.

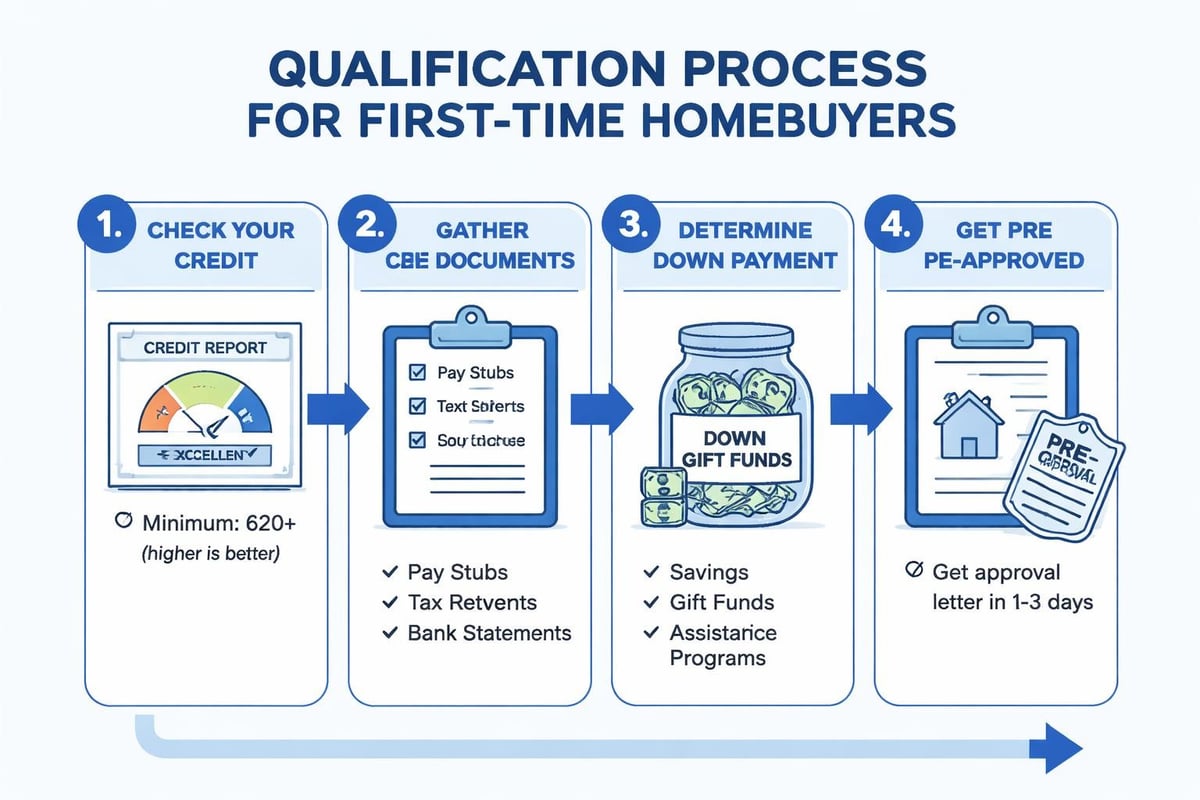

Pre-Approval Process and Timeline

Getting pre-approved represents your first concrete step toward homeownership. Unlike pre-qualification (an informal estimate), pre-approval involves full documentation review and underwriter evaluation of your financial profile.

Documentation Requirements

Lenders require comprehensive documentation to issue pre-approvals. Gathering these items proactively accelerates the process and demonstrates preparedness to listing agents in competitive markets.

Standard documentation includes:

- Two years of W-2s and tax returns

- 30 days of pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts

- Government-issued photo identification

- Authorization for credit report

- Explanation letters for any credit issues or employment gaps

Tech employees with RSUs should also provide vesting schedules and brokerage statements showing received equity compensation. Self-employed buyers need additional documentation including profit and loss statements and business tax returns.

Accelerated Underwriting Options

Some lenders offer expedited underwriting that can deliver pre-approvals in as little as 24-48 hours with complete documentation. This speed becomes crucial in Seattle's competitive market where sellers often review multiple offers simultaneously.

Advanced underwriting platforms can close transactions in as few as 9 business days for well-documented borrowers with clean credit and straightforward income. This capability provides significant advantages when competing against cash buyers or making offers on desirable properties in Redmond or Bellevue.

Managing Debt-to-Income Ratios

Your debt-to-income (DTI) ratio represents one of the most critical qualification metrics for loans for first time homebuyers. This calculation compares your total monthly debt obligations to your gross monthly income.

Calculating Front-End and Back-End Ratios

Front-end DTI considers only housing expenses (principal, interest, taxes, insurance, HOA fees) divided by gross income. Back-end DTI includes housing expenses plus all other monthly debt payments (student loans, car payments, credit cards, personal loans).

Most loan programs allow back-end DTIs up to 43-50%, though lower ratios improve approval odds and rate pricing. A buyer earning $10,000 monthly with $2,000 in housing costs and $1,500 in other debts would have a 35% back-end DTI ($3,500 ÷ $10,000).

Strategies to Improve Your Ratio

If your DTI exceeds program limits, several strategies can help you qualify. Paying off smaller debts entirely removes them from calculations. Increasing your down payment reduces your loan amount and monthly housing costs. Adding a co-borrower brings additional income into the equation.

Student loan calculations under conventional loans often use 0.5% or 1% of the outstanding balance as the monthly payment, regardless of your actual payment. Federal income-driven repayment plans showing $0 payments can dramatically improve DTI for borrowers with substantial student debt.

Homebuyer Education Requirements

Many first-time buyer programs and down payment assistance options require completion of homebuyer education courses. These courses provide valuable information about the purchase process, mortgage responsibilities, and homeownership costs.

Online and In-Person Options

HUD-approved housing counseling agencies offer both virtual and in-person classes covering topics from budgeting to home maintenance. Most courses take 6-8 hours and cost $50-$100, though many down payment assistance programs offer free education to participants.

Certificates of completion remain valid indefinitely and can be used for multiple loan applications. Taking education courses early in your homebuying journey provides knowledge that proves invaluable during property searches and offer negotiations.

Benefits Beyond Requirement Fulfillment

Even if not required by your specific loan program, homebuyer education offers substantial value. You'll learn about predatory lending practices, understand different mortgage structures, gain insights into home inspections, and develop realistic maintenance budgets.

Bankrate reviews and compares mortgage lenders to help you identify institutions offering quality education resources alongside competitive financing.

Working With a Seattle Mortgage Broker

Navigating the complexity of loans for first time homebuyers becomes significantly easier with experienced local guidance. Mortgage brokers access multiple lenders and loan programs, providing options you wouldn't find working directly with a single bank.

Broker Advantages for First-Time Buyers

Brokers offer several distinct benefits over retail bank lending. They can shop your scenario across numerous lenders to find optimal pricing and programs. They provide education and guidance without sales pressure tied to a single product line. They often have access to wholesale rates not available to consumers directly.

For complex income scenarios common among Seattle tech workers, brokers with expertise in RSU qualification and jumbo underwriting become particularly valuable. They understand local market dynamics in neighborhoods from Shoreline to Everett and can structure offers that compete effectively.

Questions to Ask Potential Lenders

When evaluating mortgage brokers or loan officers, ask specific questions about their experience, available programs, and process transparency. How many first-time buyers have they helped in the past year? What down payment assistance programs do they actively use? Can they provide recent client references?

Understanding fee structures upfront prevents surprises. Reputable brokers explain all costs clearly and provide loan estimates promptly. They should demonstrate willingness to educate rather than simply process applications.

Common Mistakes First-Time Buyers Make

Learning from others' errors helps you avoid costly missteps during your homebuying journey. Several mistakes appear repeatedly among first-time buyers, particularly in competitive markets like the greater Seattle area.

Shopping Before Pre-Approval

Falling in love with properties before understanding your buying power leads to disappointment and wasted time. Sellers and listing agents give preference to buyers with solid pre-approvals, especially in multiple offer situations common across Bellevue and Redmond.

Get pre-approved before attending open houses or scheduling private showings. This discipline ensures you focus energy on homes you can actually afford and positions you as a serious buyer when ready to make offers.

Depleting All Savings for Down Payment

Using every available dollar for down payment and closing costs leaves you financially vulnerable after closing. Unexpected repairs, moving expenses, and furniture needs add up quickly. Lenders also require reserves (savings remaining after closing) for many loan programs, particularly jumbos.

Maintain emergency funds equivalent to 3-6 months of expenses even after your purchase. Consider slightly smaller down payments to preserve liquidity during your first year of homeownership.

Ignoring Total Housing Costs

Monthly principal and interest represent only part of your housing expenses. Property taxes in King County vary by jurisdiction but average 0.9-1.1% annually. Homeowners insurance adds another $1,000-$2,500 yearly for typical properties. HOA fees in condos can range from $200-$800 monthly.

Calculate total housing costs including taxes, insurance, utilities, maintenance, and HOA fees before determining your comfortable price range. A rule of thumb suggests budgeting 1-2% of purchase price annually for maintenance alone.

Making Major Financial Changes

Opening new credit cards, financing furniture, or changing jobs during your transaction can derail your approval. Lenders re-verify credit and employment shortly before closing. New debts change your DTI ratio while job changes may require re-underwriting with different income documentation.

Maintain financial status quo from application through closing. Major purchases and career moves can wait until after you've secured your new home.

Market Insights for Seattle-Area Buyers

Understanding local market conditions helps first-time buyers make strategic decisions about timing, neighborhoods, and offer structures. Seattle's housing market in 2026 continues evolving with distinct patterns across different areas.

Neighborhood Price Variations

Median home prices vary significantly across the greater Seattle region. Downtown Seattle and Bellevue command premium prices often requiring jumbo financing, while areas like Lynnwood and Mill Creek offer more accessible entry points for first-time buyers with conventional and FHA loans.

According to research on homebuyer trends from the National Association of Realtors, first-time buyers typically purchase smaller, less expensive properties in emerging neighborhoods rather than established premium areas. This pattern holds true locally, with many first-time buyers starting in Shoreline, Lake Forest Park, or Everett before eventually moving to pricier locations.

Seasonal Purchase Timing

Seattle's housing market shows distinct seasonal patterns. Spring and summer bring maximum inventory and competition, with multiple offers common on well-priced properties. Fall and winter typically offer less competition, potentially better negotiating leverage, and motivated sellers.

However, inventory also decreases during colder months. The optimal strategy often involves getting pre-approved in winter, understanding the market during slower periods, then being ready to act decisively when the right property appears.

Understanding loans for first time homebuyers requires navigating multiple programs, requirements, and strategies, but the right guidance transforms complexity into confidence. Whether you're a tech professional in Redmond evaluating stock compensation or a growing family in Shoreline seeking FHA financing, knowing your options positions you for success in Seattle's competitive market. Keith Akada at Mortgage Reel brings 25+ years of experience helping first-time buyers across Seattle, Bellevue, and surrounding communities make informed decisions with transparent communication and expert strategy. With 750+ five-star reviews and the ability to close loans in as few as 9 business days, he provides the education, responsiveness, and execution that turn homeownership dreams into reality.