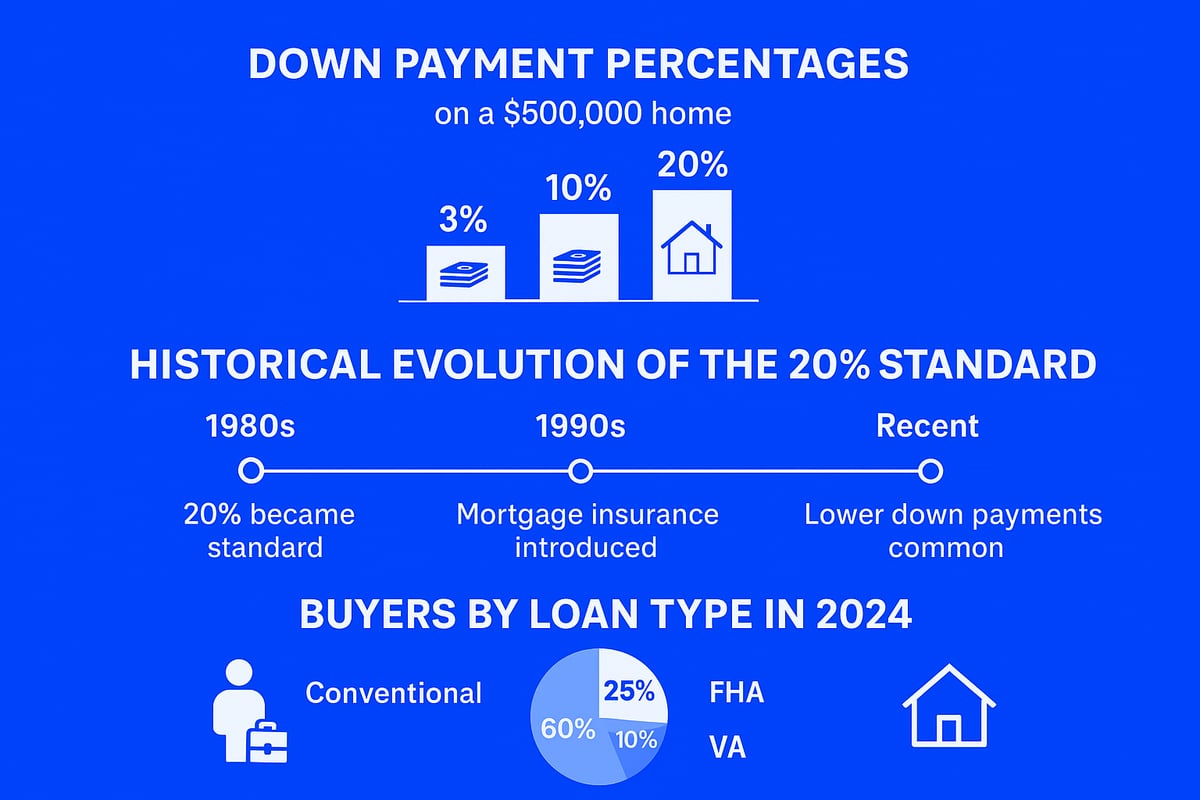

In 2026, the mortgage 20 down payment continues to spark debate and confusion among homebuyers as the real estate market evolves. While many still believe 20% is the golden rule, recent data shows that most first-time buyers put down much less, with the median at just 9% according to 2024 figures.

This guide is designed to demystify the mortgage 20 down payment. You will discover why it became the standard, its real benefits and drawbacks, and what alternatives exist in today’s lending landscape.

Whether you are a first-time buyer or planning your next move, this article offers clear, practical strategies and insights. Ready to make confident, informed decisions? Read on to uncover the best approach for your financial future.

Understanding the 20% Mortgage Down Payment

Buying a home is a major milestone, and understanding the mortgage 20 down payment is crucial for making informed decisions. The 20% figure is often cited, but what does it really mean for buyers in 2026? Let’s break down the concept, history, and lender perspectives to help you navigate the process with confidence.

What Is a Down Payment?

A down payment is the initial lump sum you pay upfront when purchasing a home, representing a percentage of the property’s total price. For example, a mortgage 20 down payment on a $500,000 home equals $100,000 out of pocket.

Lenders require down payments to reduce risk and ensure buyers have a financial stake in the property. According to 2024 National Association of Realtors (NAR) data, 74% of buyers finance their purchase with a mortgage, making the down payment a critical step in the process.

It’s important to distinguish between the down payment and closing costs. The down payment directly reduces your loan amount, impacting your loan-to-value (LTV) ratio, which in turn affects your mortgage terms and approval odds. A larger down payment often leads to more favorable loan conditions.

For a detailed breakdown of requirements, see 20 Percent Down Home Loans.

The Origins and Evolution of the 20% Standard

The mortgage 20 down payment standard has roots in traditional lending practices, where lenders sought to minimize risk by requiring buyers to invest substantial equity from the start. This threshold became the benchmark because it generally eliminated the need for private mortgage insurance (PMI), which protects lenders when borrowers put less money down.

However, the landscape has shifted. Recent data shows the median down payment for first-time buyers is now just 9% (NAR 2024), reflecting more flexible loan programs and rising home prices. Generational and regional differences also shape down payment trends, with younger buyers and those in high-cost markets often putting less down.

Government-backed loans like FHA, VA, and USDA have played a major role in this evolution, offering low or zero down payment options. Since 2020, changing market conditions have further influenced buyer behavior, making alternatives to the mortgage 20 down payment more common.

Why Lenders Care About 20% Down

From a lender’s perspective, the mortgage 20 down payment is about reducing risk and ensuring the borrower has “skin in the game.” When you put 20% down, you avoid private mortgage insurance (PMI), which typically costs 0.5 to 1.5% of the loan amount per year.

Higher down payments also correlate with lower default rates, giving lenders more confidence in your ability to repay. The size of your down payment can influence your interest rate offers, as a lower loan-to-value ratio often leads to better terms.

Some loan programs, such as VA and USDA, are designed to minimize or eliminate the down payment for eligible buyers. However, in competitive markets, a mortgage 20 down payment can make your offer stand out to sellers and strengthen your negotiating position.

Pros and Cons of a 20% Down Payment in 2026

Deciding on a mortgage 20 down payment is one of the most important choices homebuyers face in 2026. While this approach offers financial advantages, it also comes with challenges that can affect your timeline, budget, and long-term plans. Below, we break down the benefits, drawbacks, and real-life scenarios to help you make an informed decision.

Key Benefits of Putting 20% Down

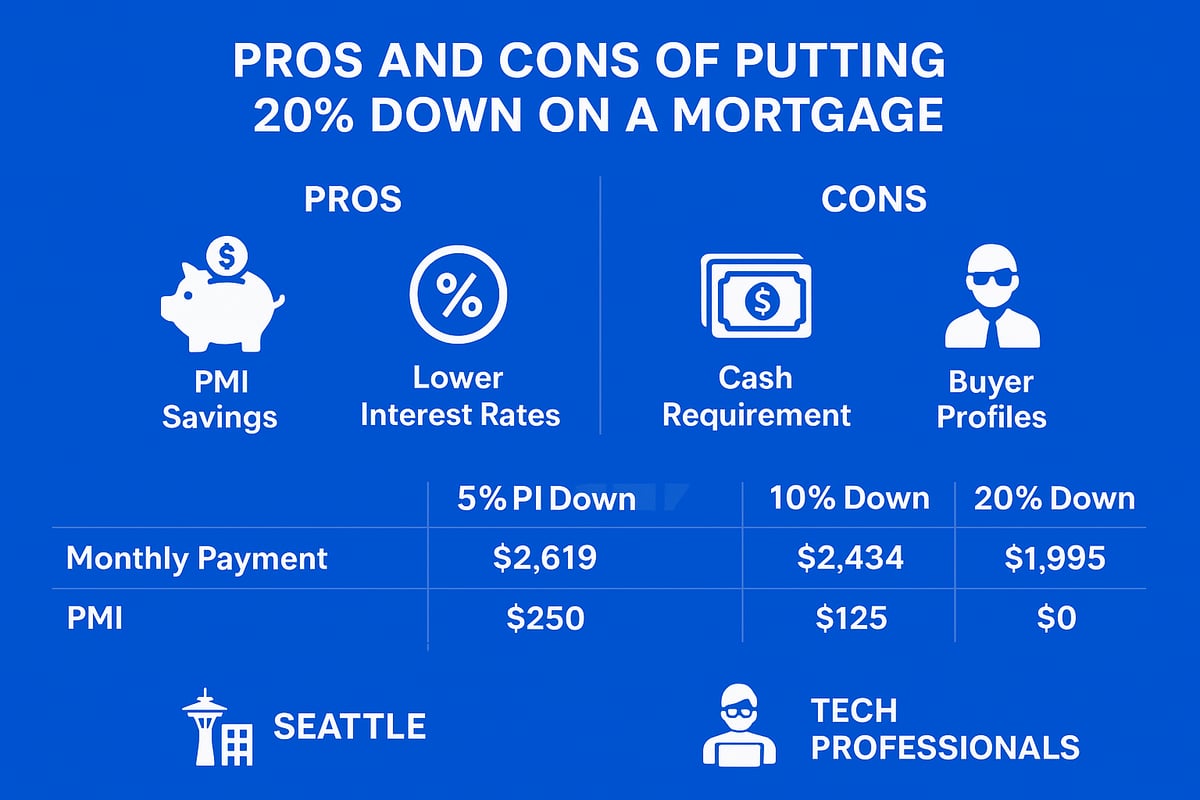

Choosing a mortgage 20 down payment can unlock several advantages for homebuyers. The most immediate benefit is avoiding private mortgage insurance (PMI), which can save you thousands over the life of your loan. Lenders typically require PMI when your down payment is less than 20 percent, so reaching this threshold keeps your monthly payments lower.

You may also qualify for a lower interest rate. Lenders view a mortgage 20 down payment as a sign of financial stability, often rewarding you with better terms. Lower principal means your monthly payments are smaller, freeing up cash for other expenses.

Other benefits include:

- Building more home equity from the start

- Making your offer more competitive in a bidding war

- Lower risk of negative equity if property values drop

Consider this example for a $500,000 home, assuming a 7 percent interest rate and monthly PMI of 1 percent on loans under 20 percent down:

| Down Payment | Loan Amount | Monthly Payment* | PMI/Month | Total Monthly |

|---|---|---|---|---|

| 5% ($25,000) | $475,000 | $3,163 | $396 | $3,559 |

| 10% ($50,000) | $450,000 | $3,002 | $375 | $3,377 |

| 20% ($100,000) | $400,000 | $2,668 | $0 | $2,668 |

*Estimates only, excluding taxes and insurance.

With a mortgage 20 down payment, you could save nearly $900 per month compared to 5 percent down. This can add up to significant long-term savings and peace of mind.

Drawbacks and Challenges of Saving 20%

Saving for a mortgage 20 down payment is not without its obstacles. The most obvious challenge is the large upfront cash requirement. With home prices rising, accumulating $80,000 to $100,000 or more can take years, especially for first-time buyers.

This delay may mean renting longer while you save. During that time, property values could increase, making it harder to catch up. Tying up so much cash in your home also means less flexibility for investments or emergencies, which may not align with your financial goals.

Other challenges include:

- Risk of draining your emergency or retirement savings

- Opportunity cost of missing out on investment growth

- Potential to miss out on low down payment programs with attractive rates

For context, the median down payment for first-time buyers was just 9 percent in 2024, far below the mortgage 20 down payment level. This shows that many buyers are finding success with less cash upfront.

If you put all your funds toward a mortgage 20 down payment, you may leave yourself financially vulnerable if unexpected expenses arise. Carefully consider whether waiting to save the full 20 percent is worth the trade-offs.

Real-Life Scenarios: Who Should and Shouldn’t Put 20% Down?

A mortgage 20 down payment is ideal for buyers with strong savings, stable income, and a desire for long-term cost savings. Move-up buyers who have equity from a previous sale, or those in high-paying tech fields in Seattle or Bellevue, may benefit most from this approach.

On the other hand, first-time buyers or those in expensive markets might struggle to save that much. In these cases, putting down 5 percent or 10 percent could make homeownership possible sooner without overextending finances. Investors often prefer to keep cash liquid to fund multiple properties instead of tying up capital in one.

Let’s compare the long-term costs for different down payment amounts on a $500,000 home:

- 5 percent down: higher monthly payments, more spent on PMI, less equity at the start

- 10 percent down: moderate payments, some PMI, more flexibility

- 20 percent down: lowest payments, no PMI, fastest equity growth

Your age, career stage, and family needs also play a role. Younger buyers may value liquidity, while those nearing retirement might prioritize equity. In competitive markets, a mortgage 20 down payment can make your offer stand out.

If you want to explore the numbers for different scenarios, the Conventional Loan Down Payment Comparison provides a detailed breakdown to help guide your decision.

Ultimately, the right choice depends on your goals, market conditions, and personal finances. Weigh the pros and cons of a mortgage 20 down payment carefully to find the best fit for your journey.

Current Down Payment Requirements and Loan Options in 2026

Navigating today’s home financing landscape means understanding how the mortgage 20 down payment standard fits into a wider array of loan options. Requirements have evolved, and homebuyers in 2026 face a more diverse set of programs than ever before. Let’s break down minimum down payments, how your chosen amount impacts mortgage insurance and rates, and what assistance is available to help you reach your homeownership goals.

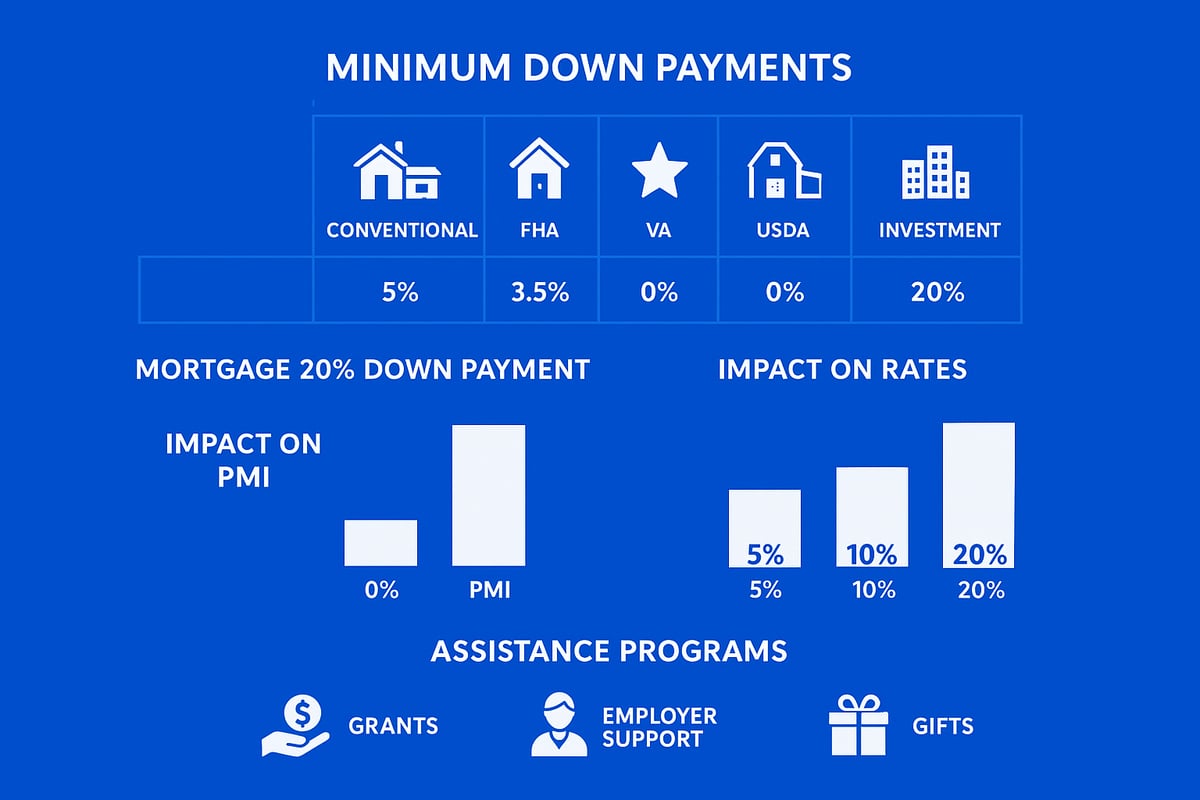

Minimum Down Payments by Loan Type

Understanding the minimum required down payment for each loan type is essential when considering the mortgage 20 down payment. Here’s a quick comparison:

| Loan Type | Minimum Down Payment | Key Eligibility Criteria |

|---|---|---|

| Conventional | 3–5% | Good credit, income verification |

| FHA | 3.5% (580+ credit) | Lower credit, primary residence |

| VA | 0% | Eligible veterans, service members |

| USDA | 0% | Rural areas, income limits |

| Jumbo | 5–10%+ | High loan amounts, strong finances |

| Investment | 20%+ | Non-owner-occupied properties |

If you’re purchasing a second home or investment property, expect higher down payment requirements. Programs like HomeReady and HomePossible allow qualifying buyers to put just 3% down. Jumbo loans, which exceed conforming limits, usually require at least 10% down, and lenders scrutinize credit and assets closely.

Your credit score can affect the minimum down payment. For example, FHA loans require 3.5% down for scores above 580, but buyers with scores between 500–579 may need to put 10% down. Special programs target first-time and low-income buyers, helping them compete even if they can’t meet the mortgage 20 down payment threshold.

How Down Payment Size Impacts Mortgage Insurance and Rates

The size of your mortgage 20 down payment has a direct effect on mortgage insurance and the interest rate you’ll pay. If you put less than 20% down on a conventional loan, you’ll need private mortgage insurance (PMI), which typically adds 0.5–1.5% of the loan amount to your annual costs. FHA loans require a mortgage insurance premium (MIP), both upfront and annually, regardless of down payment, while VA loans have a funding fee based on factors like service history and loan size.

Consider the difference in monthly payments:

- $400,000 loan with 5% down: Higher payment, plus $150/month PMI.

- $400,000 loan with 20% down: Lower payment, no PMI.

A larger down payment reduces your loan-to-value ratio, often resulting in a better interest rate and long-term savings. Reaching 20% equity lets you request PMI removal on conventional loans, usually after a few years of steady payments. For FHA loans, removing MIP may require refinancing.

Choosing the mortgage 20 down payment route can make your offer more attractive to sellers and set you up for lower long-term costs.

Down Payment Assistance and Alternative Solutions

If saving for a mortgage 20 down payment feels out of reach, you have options. Down payment assistance programs can bridge the gap for eligible buyers, offering:

- Grants that do not require repayment.

- Forgivable or deferred-payment loans.

- Matched savings programs that boost your contributions.

- Employer-sponsored homebuyer benefits.

- Gifts from family, which must be properly documented.

- Accessing retirement accounts, such as a 401k loan or IRA withdrawal, though this comes with risks and tax considerations.

Special programs exist for veterans and buyers in rural areas, making zero-down payment loans possible. Always review eligibility requirements and the long-term implications, such as repayment terms or resale restrictions.

For Washington State buyers, resources like the Loan Down Payment Home Loans in Washington State page provide a comprehensive overview of programs and strategies to help you secure a home with less than 20% down.

Combining assistance with personal savings allows more buyers to achieve homeownership sooner, even if the traditional mortgage 20 down payment is not feasible.

Strategies to Save for a 20% Down Payment

Saving for a mortgage 20 down payment can feel daunting, but a structured approach makes it achievable. By breaking the process into actionable steps, you’ll build momentum and confidence as you move closer to your goal.

Step 1: Set a Realistic Savings Goal

Begin your mortgage 20 down payment journey by determining how much you need to save, based on your target home price and chosen loan type. For example, if you’re aiming for a $400,000 home, a 20% down payment means setting aside $80,000.

Factor in additional expenses such as closing costs, moving fees, and required cash reserves. Use online calculators to test different scenarios and see how varying down payment amounts affect your purchase power.

Consider current market trends and local price growth. According to Median down payment for first-time buyers, the typical first-time buyer puts down 9%. Setting a mortgage 20 down payment goal may mean a longer timeline, but it can also provide substantial long-term benefits.

Step 2: Optimize Your Budget and Cut Expenses

Audit your current spending to identify areas where you can redirect funds toward your mortgage 20 down payment. Review discretionary expenses such as streaming services, dining out, or subscriptions.

- Cancel unused memberships.

- Limit takeout and entertainment costs.

- Shop for better deals on insurance or utilities.

Set up automatic transfers into a separate savings account dedicated to your mortgage 20 down payment. Apply any windfalls, such as tax refunds or bonuses, directly to your goal. Track your progress monthly, and make adjustments as your situation evolves.

Step 3: Choose the Right Savings Vehicle

Where you keep your mortgage 20 down payment savings matters. Compare high-yield savings accounts, money market accounts, and certificates of deposit (CDs) to maximize your interest earnings while maintaining liquidity.

| Savings Vehicle | Pros | Cons |

|---|---|---|

| High-yield Savings | Easy access, higher rates | Rates can fluctuate |

| Money Market Account | Check-writing, stable | May require higher minimums |

| CDs | Locked rates, higher yield | Early withdrawal penalties |

Avoid investment accounts with high risk or limited access, since you’ll need your funds available on your timeline. Match your savings vehicle to your expected homebuying date to optimize returns on your mortgage 20 down payment.

Step 4: Explore Side Income and Windfalls

Boost your mortgage 20 down payment savings by increasing your income. Consider freelance work, side gigs, or part-time jobs. Even earning an extra $200 a month can significantly shorten your savings timeline.

Sell unused items or assets to generate quick cash. Renting out a room or leveraging the sharing economy can also add to your savings. Whenever you receive a bonus, commission, or inheritance, allocate a portion directly to your mortgage 20 down payment fund.

If your employer offers homebuyer assistance, take advantage of it. Steer clear of high-risk investments that could jeopardize your savings progress.

Step 5: Leverage Down Payment Assistance and Gifts

Many buyers reach their mortgage 20 down payment goal by combining personal savings with outside help. Research local and national down payment assistance programs, including grants, forgivable loans, or matched savings plans.

Understand the documentation rules for using gifted funds from family or close friends. Coordinate closely with your lender to ensure compliance and avoid delays. When eligible, a $10,000 grant or gift can significantly reduce your personal savings requirement for your mortgage 20 down payment.

Stay updated on new programs, as offerings and eligibility criteria can change. Combining assistance with disciplined savings can help you achieve homeownership sooner.

Deciding If a 20% Down Payment Is Right for You

Choosing whether to make a mortgage 20 down payment is one of the most impactful decisions in your homebuying journey. This decision affects your finances, your flexibility, and your future goals. To help you decide, let's break down the key factors every buyer should consider in 2026.

Assessing Your Financial Situation and Goals

Begin by taking a close look at your current financial picture. How much have you saved, and how stable is your income? A mortgage 20 down payment often means tapping a significant portion of your liquid assets. While this can reduce your loan amount and monthly payments, it may also limit your ability to handle unexpected expenses or pursue other financial priorities.

Think about your broader goals. Are you also saving for retirement, college, or an emergency fund? If making a mortgage 20 down payment would drain your reserves, consider whether you might be better off with a smaller down payment and more cash on hand. Use online mortgage calculators to compare the long-term costs of different down payment scenarios. For example, compare the total interest paid over 30 years with 5% versus 20% down, factoring in mortgage insurance and potential investment growth on your savings.

Consulting with a financial advisor can provide personalized guidance. They can help you weigh the trade-offs between upfront equity and long-term liquidity and ensure your mortgage 20 down payment aligns with your risk tolerance and life plans.

Market Conditions and Timing Considerations in 2026

Next, evaluate the real estate landscape in your area. In 2026, home prices are expected to continue rising in many markets, including high-demand regions like Seattle and Bellevue. If you wait too long to save for a mortgage 20 down payment, you may find that home prices have outpaced your savings rate, making it even harder to reach your goal.

Interest rates also play a critical role. A slight uptick in rates can dramatically increase your monthly payment, even if your down payment is larger. In some cases, buying sooner with a smaller down payment may be more beneficial than waiting to accumulate the full mortgage 20 down payment, especially if home values are appreciating rapidly.

Consider your personal timeline. Are you relocating for work, expanding your family, or seeking stability in a competitive market? Sometimes the urgency of your move outweighs the ideal of waiting for a larger down payment. Weigh the cost of renting longer against the potential for home price appreciation. For example, if prices rise 5% annually, a $500,000 home could cost $25,000 more just one year from now, possibly offsetting the benefits of a mortgage 20 down payment.

Alternatives to 20% Down: Making the Best Choice for You

A mortgage 20 down payment is not the only path to homeownership. Many buyers successfully purchase homes with 3%, 5%, or 10% down, especially with the support of modern loan programs. Lower down payments may come with private mortgage insurance (PMI) or mortgage insurance premiums (MIP), but these costs can be manageable, especially if you plan to refinance or pay down your mortgage quickly.

Hybrid strategies are increasingly popular. For example, you might buy now with a 10% down payment, then refinance once you reach 20% equity to eliminate PMI. This can keep more cash available for emergencies or investment opportunities. Buyers of high-priced homes should also consider specialized products. If you are deciding between a 10% and 20% down payment for a jumbo loan, see this detailed comparison: Should I Put 10 Percent or 20 Percent Down Jumbo Loan.

Ultimately, the best choice is the one that fits your unique needs. Stress-test your budget for different down payment levels, and remember that the right mortgage 20 down payment is not one-size-fits-all. Your age, career stage, family priorities, and local market competition all influence the optimal approach.

Frequently Asked Questions About 20% Down Payments

Navigating the mortgage 20 down payment landscape brings up many questions for homebuyers. Below, we address the most common concerns, helping you make informed decisions as you plan your path to homeownership.

Is 20% Down Always Required to Buy a Home?

No, putting the traditional mortgage 20 down payment is not always mandatory. Most major loan programs, including conventional, FHA, VA, and USDA, allow for much smaller down payments based on eligibility. For example, conventional loans can start as low as 3%, while VA and USDA loans may require nothing down for qualified buyers. According to first-time homebuyer statistics 2024, the median down payment for first-time buyers is only 9%. However, some scenarios, such as jumbo loans or highly competitive markets, may still favor or require a mortgage 20 down payment. Always check with your lender for the most up-to-date requirements.

What Are the Risks of Putting Less Than 20% Down?

Choosing less than the mortgage 20 down payment means you may face several financial risks. The most immediate is the need to pay private mortgage insurance (PMI) or similar fees, increasing your monthly payment. You also start with less equity, which can be risky if home values fall. Lenders may charge higher interest rates, and your offer might be less competitive. For a clearer picture of how PMI impacts your payment, try this private mortgage insurance cost calculator. Weigh these risks carefully when considering alternatives to the mortgage 20 down payment.

Can I Remove PMI After Reaching 20% Equity?

Yes, one advantage of the mortgage 20 down payment is avoiding PMI altogether, but if you start with less, you can still remove PMI later. On conventional loans, you may request PMI cancellation once your loan-to-value ratio hits 80%. Lenders will typically require an appraisal and a strong payment history. For FHA loans, mortgage insurance premium (MIP) rules differ and may require refinancing to drop insurance. Building equity faster with extra payments can speed up the process. Always check your lender’s specific guidelines related to mortgage 20 down payment and PMI removal.

How Do Down Payment Assistance Programs Work?

Down payment assistance programs can help offset the challenge of meeting a mortgage 20 down payment. These programs include grants, forgivable loans, and matched savings plans, often offered by local, state, or national agencies. Eligibility usually depends on income, location, and first-time buyer status. Some employers also provide homebuyer assistance. When combined with your own savings, these resources can significantly reduce the cash you need upfront. Keep in mind that each program has its own rules and long-term implications, so review the details carefully before relying on assistance to reach your mortgage 20 down payment goals.

Should I Use Retirement Funds for a Down Payment?

Using retirement funds for a mortgage 20 down payment is possible, but there are important pros and cons. You may access 401k loans or IRA withdrawals, sometimes with special provisions for first-time buyers. However, taxes, penalties, and lost investment growth can impact your long-term financial stability. For example, withdrawing $20,000 from an IRA may trigger taxes and reduce your retirement nest egg. It is wise to explore all other options before using retirement savings for your mortgage 20 down payment. Consult with a financial advisor to assess the impact on your overall financial picture.

How Does the Down Payment Affect My Mortgage Rate?

The size of your mortgage 20 down payment directly influences your mortgage rate. Lenders see larger down payments as a sign of lower risk, often resulting in better interest rates. For example, putting 5% down versus 20% could mean a higher rate and thousands more in interest over the life of your loan. Other factors, such as your credit score, also play a role. Shopping around and using online calculators can help you compare offers. Remember, the mortgage 20 down payment is just one piece of the puzzle when securing the best possible rate for your situation.

The Mortgage Reel: Local Expertise for Seattle & Bellevue Homebuyers

Navigating the mortgage 20 down payment decision in Seattle or Bellevue can feel overwhelming, especially with the region’s competitive housing market. The Mortgage Reel, led by Keith Akada, offers tailored guidance for buyers at every stage, from first-timers to seasoned investors.

With expertise in conventional, FHA, VA, and jumbo loans, The Mortgage Reel helps clients compare mortgage 20 down payment options with lower down payment strategies to find the right fit. Their team specializes in serving tech professionals, maximizing buying power with RSUs and equity compensation, and providing fast-track approvals to help buyers stand out.

Clients benefit from access to local down payment assistance programs, comprehensive homebuyer education, and a client-first approach that has earned over 750 five-star reviews. If you want clarity and confidence in your mortgage 20 down payment journey, schedule a consultation with The Mortgage Reel for expert, local advice.

After exploring the ins and outs of the 20 percent mortgage down payment, you might still have questions about what makes the most sense for your situation—whether it’s weighing the pros and cons, navigating down payment assistance, or understanding how current market trends in Seattle or Bellevue could impact your journey. If you’re ready for tailored guidance or just want to talk through your options with someone who understands the local landscape, I invite you to Let’s have a conversation. Together, we can clarify your goals and outline your next steps toward confident homeownership.