Stepping into homeownership for the first time represents one of the most significant financial decisions you'll make in your lifetime. For buyers navigating the competitive Seattle housing market, securing the right mortgage for first time homebuyers requires understanding loan programs, qualification requirements, and local market dynamics. With median home prices in King County continuing to challenge budgets, especially in neighborhoods across Seattle, Bellevue, and Redmond, first-time buyers need strategic guidance to maximize their purchasing power while minimizing unnecessary costs. This comprehensive guide breaks down everything you need to know about financing your first home purchase in the Greater Seattle area.

Understanding First Time Homebuyer Status and Benefits

The definition of a first-time homebuyer extends beyond those who have never owned property. According to federal housing guidelines, you qualify as a first-time buyer if you haven't owned a primary residence in the past three years. This means even if you previously owned a home, you may still access programs designed specifically for first-time purchasers.

Key advantages available to first-time buyers include:

- Lower down payment requirements on certain loan programs

- Reduced mortgage insurance costs through specific products

- Access to down payment assistance programs in Washington State

- Seller concession allowances that can cover closing costs

- Tax credits and deductions for mortgage interest

Understanding your status matters because it unlocks financial benefits that can save thousands of dollars throughout the homebuying process. The Consumer Financial Protection Bureau provides comprehensive resources to help you navigate these advantages and understand your rights as a homebuyer.

Why Seattle First-Time Buyers Face Unique Challenges

The Greater Seattle housing market presents distinct obstacles that differ from national trends. Tech industry growth has driven demand in neighborhoods throughout Seattle, Shoreline, and Kirkland, creating competition that requires strategic financing approaches.

Buyers working at Amazon, Microsoft, or Google often have complex compensation structures including RSUs and stock grants. These income sources can be leveraged for mortgage qualification, but require specialized underwriting expertise to maximize approval amounts. Traditional lenders may not count unvested stock compensation, potentially limiting your buying power in markets where properties regularly sell above asking price.

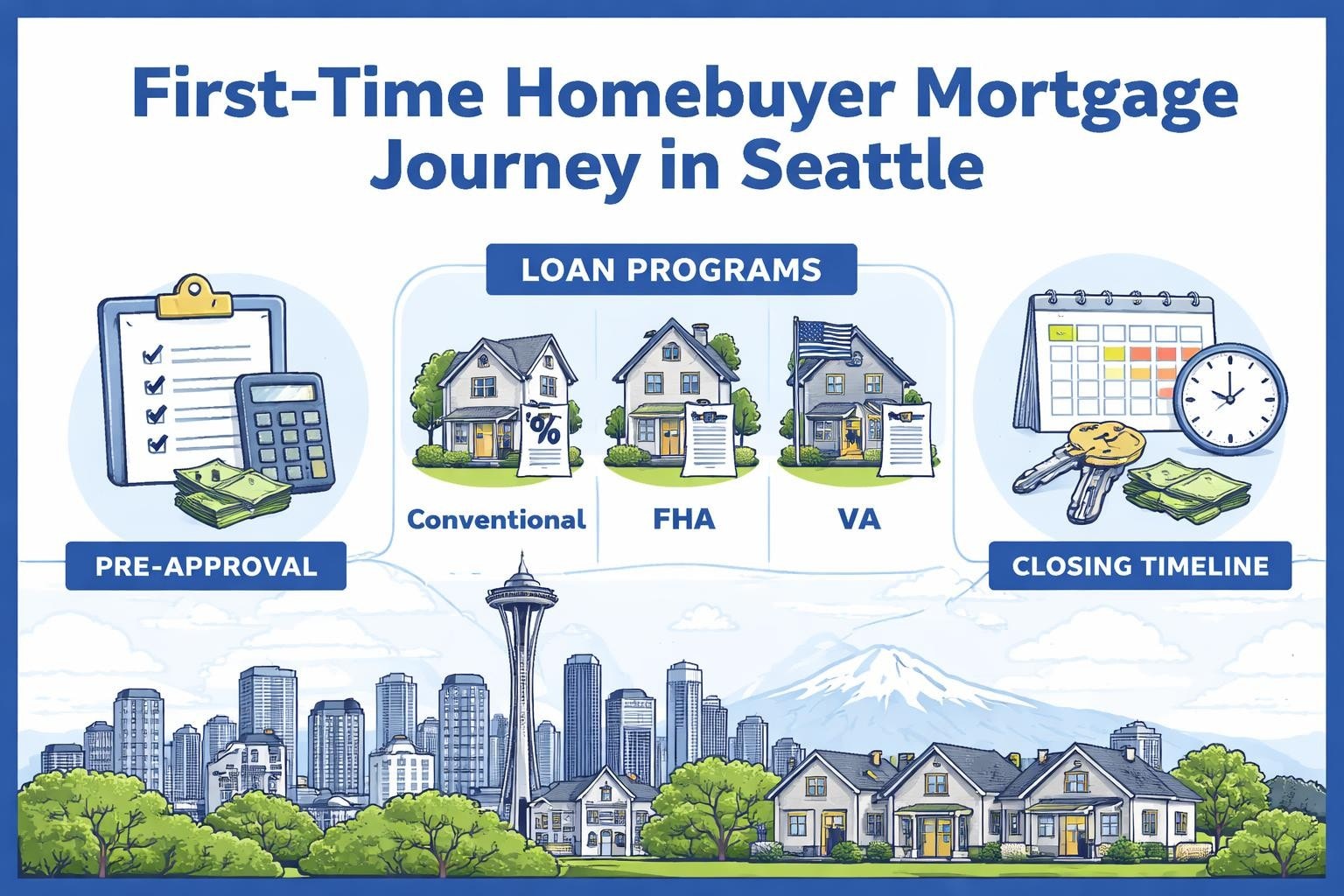

Mortgage Loan Programs for First Time Homebuyers

Selecting the appropriate loan program represents a critical decision that impacts your monthly payment, upfront costs, and long-term financial flexibility. Each program offers distinct advantages depending on your financial situation, credit profile, and homeownership goals.

Conventional Loans with Low Down Payments

Conventional mortgages backed by Fannie Mae and Freddie Mac offer first-time buyers competitive options with down payments as low as 3%. These loans provide flexibility and, once you reach 20% equity, allow you to eliminate private mortgage insurance without refinancing.

| Feature | 3% Down Conventional | 5% Down Conventional |

|---|---|---|

| Minimum Credit Score | 620 | 620 |

| PMI Requirement | Yes, until 20% equity | Yes, until 20% equity |

| Income Limits | None | None |

| Property Types | Most residential | Most residential |

| Debt-to-Income Max | Typically 50% | Typically 50% |

For buyers in Lynnwood or Mill Creek where home prices may be more accessible than central Seattle, a conventional loan with 5% down often provides the best long-term value. The ability to finance condos, single-family homes, and townhouses without restrictive property requirements makes conventional loans versatile for different property types common in the Seattle metro area.

FHA Loans: Government-Backed Accessibility

Federal Housing Administration loans serve buyers with smaller down payments or credit challenges. With a 3.5% down payment requirement and more flexible credit score standards, FHA loans provide access to homeownership for buyers who might not qualify for conventional financing.

FHA loan advantages include:

- Credit scores as low as 580 accepted (sometimes 500 with 10% down)

- Higher debt-to-income ratios allowed compared to conventional

- Gift funds permitted for down payment and closing costs

- Assumable loans that can be transferred to future buyers

The trade-off involves mandatory mortgage insurance for the life of the loan on most FHA mortgages with less than 10% down. This ongoing cost increases your monthly payment compared to conventional financing where PMI can be removed. However, for buyers purchasing homes in Everett or Lake Forest Park where prices remain relatively moderate, the accessibility of FHA financing often outweighs the insurance costs.

Research from Fannie Mae demonstrates that shopping multiple lenders can save first-time buyers thousands in interest and fees, making it essential to compare both conventional and government-backed options.

VA Loans for Veterans and Service Members

Veterans, active-duty service members, and qualifying surviving spouses can access VA loans with zero down payment and no monthly mortgage insurance. This program offers exceptional value for eligible buyers competing in Seattle's expensive market.

VA loans feature competitive interest rates, flexible credit requirements, and limited closing costs thanks to VA funding fee restrictions. For a veteran purchasing in Redmond or Bellevue where home prices frequently exceed $1 million, the ability to finance 100% of the purchase price provides substantial financial leverage.

USDA Loans in Eligible Areas

While most of the Greater Seattle metro area doesn't qualify, some properties in outer suburbs may be eligible for USDA financing. These zero-down payment loans serve moderate-income buyers in designated rural areas, though income limits apply.

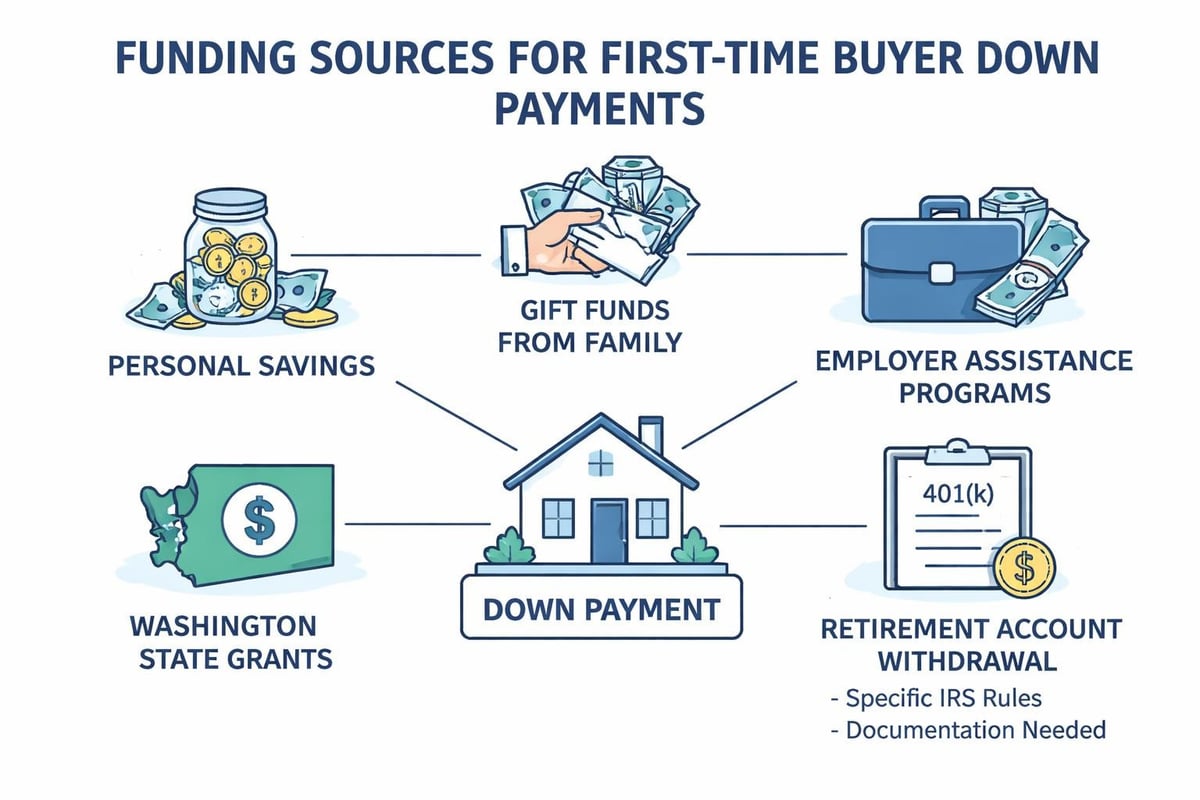

Down Payment Strategies and Assistance Programs

Accumulating funds for a down payment represents the primary barrier for most first-time buyers. Understanding your options and leveraging available assistance programs can accelerate your path to homeownership.

How Much Do You Really Need?

Contrary to popular belief, you don't need 20% down to purchase a home. Modern mortgage for first time homebuyers programs require significantly less, making homeownership achievable sooner than many buyers realize.

- 3% down: Conventional 97 LTV programs

- 3.5% down: FHA loans

- 0% down: VA and USDA loans

- 5% down: Standard conventional financing

On a $600,000 home in Shoreline, a 3% down payment equals $18,000 compared to $120,000 for a traditional 20% down payment. This difference can mean purchasing now versus waiting years to accumulate additional savings while home prices continue appreciating.

Washington State Down Payment Assistance

The Washington State Department of Financial Institutions provides resources about local assistance programs available to qualified buyers. These programs offer grants, low-interest loans, and matched savings accounts to help with down payments and closing costs.

Local programs through the Washington State Housing Finance Commission provide down payment assistance to income-qualified buyers. These resources can be combined with first-time buyer loan programs to minimize upfront cash requirements, particularly valuable in competitive markets where saving $50,000+ for a down payment may take years.

Qualifying for a Mortgage: Credit, Income, and Debt

Understanding qualification requirements helps you prepare your financial profile before beginning your home search. Lenders evaluate three primary factors when approving mortgage applications: credit history, income stability, and existing debt obligations.

Credit Score Requirements by Loan Type

Your credit score significantly impacts both loan approval and interest rate. Higher scores unlock better rates, potentially saving tens of thousands over the life of your mortgage.

| Loan Type | Minimum Score | Competitive Score | Best Rates Score |

|---|---|---|---|

| Conventional | 620 | 680 | 740+ |

| FHA | 580 | 620 | 680+ |

| VA | No minimum | 620 | 680+ |

| USDA | 640 | 660 | 700+ |

Seattle-area buyers with credit scores below 700 should focus on improvement strategies before applying. Paying down credit card balances, correcting errors on credit reports, and avoiding new credit inquiries can raise scores significantly within 60-90 days.

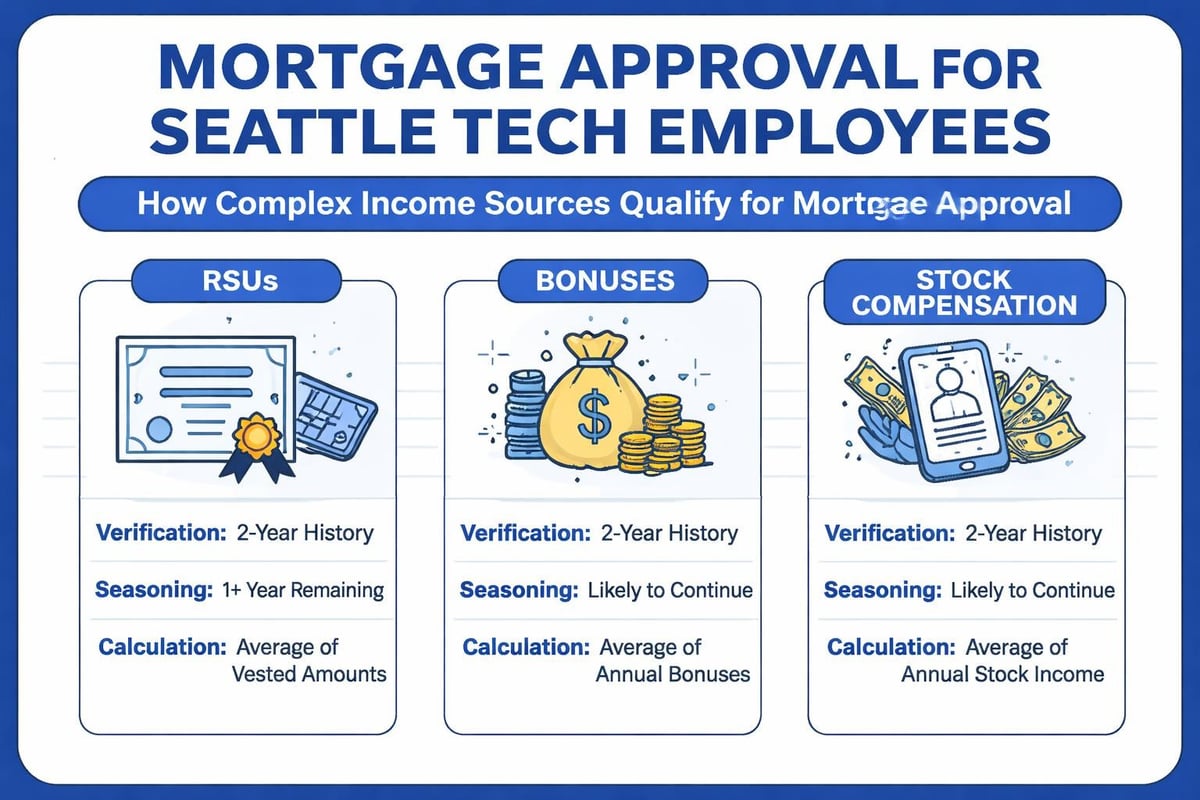

Income Documentation for Tech Professionals

Traditional W-2 employment offers straightforward qualification through pay stubs and tax returns. However, Seattle's concentration of tech industry jobs creates unique documentation scenarios for mortgage underwriting.

Complex compensation types requiring specialized qualification:

- Restricted Stock Units (RSUs) with vesting schedules

- Performance bonuses with historical averaging

- Stock options and equity grants

- Signing bonuses and relocation packages

Lenders experienced with tech industry compensation understand how to document and calculate these income sources. A $150,000 base salary with $75,000 in annual RSUs provides significantly more buying power than base salary alone, but requires proper documentation and underwriting expertise to count toward qualification.

Debt-to-Income Ratios Explained

Lenders calculate your debt-to-income (DTI) ratio by dividing monthly debt payments by gross monthly income. This metric determines how much house you can afford and whether you qualify for specific loan programs.

Most conventional loans allow DTI ratios up to 50%, while FHA loans may stretch slightly higher in compensating factor situations. For a buyer earning $10,000 monthly with $2,000 in existing debt (car payment, student loans, credit cards), a 45% DTI ratio allows total debts including the new mortgage payment up to $4,500.

Understanding DTI calculations before home shopping prevents disappointment from targeting properties outside your qualification range. Many buyers in Bellevue and Kirkland find that reducing existing debts or increasing income through documented bonuses expands their purchasing power substantially.

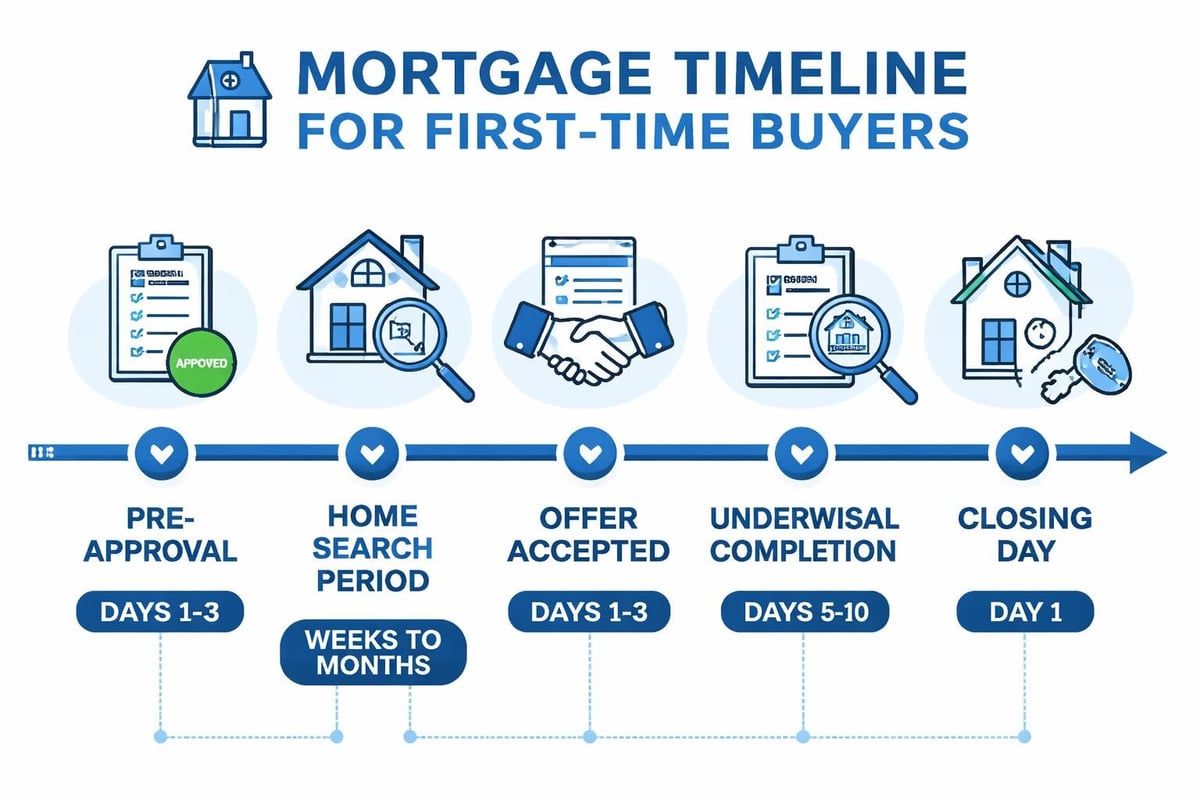

The Pre-Approval Process and Timeline

Obtaining pre-approval before house hunting provides critical advantages in competitive markets. A pre-approval letter demonstrates financial readiness to sellers and agents, strengthening your offer in multiple-bid situations common throughout the Seattle area.

Pre-Qualification vs. Pre-Approval

These terms are often confused, but represent different levels of lender commitment. Pre-qualification involves a preliminary assessment based on information you provide, while pre-approval requires documentation verification and underwriter review.

Pre-approval advantages:

- Sellers take your offers seriously in competitive situations

- You understand your actual buying power before searching

- Identifies potential credit or documentation issues early

- Expedites closing once you're under contract

- Locks interest rates during your home search

The pre-approval process typically takes 24-48 hours with responsive documentation submission. Having pay stubs, W-2s, tax returns, and bank statements organized accelerates the timeline significantly.

Documents Needed for Mortgage Pre-Approval

Gathering documentation before starting your application streamlines the process and prevents delays. Different loan programs require varying levels of documentation, but standard requirements apply to most mortgage for first time homebuyers applications.

- Income verification: Recent pay stubs, W-2s for past two years, tax returns

- Asset documentation: Bank statements for past two months, investment account statements

- Employment confirmation: Employer contact information, verification of employment

- Identification: Driver's license or government-issued ID

- Credit authorization: Permission for lender to pull credit reports

Self-employed buyers or those with complex income structures need additional documentation including profit and loss statements, business tax returns, and sometimes CPA-prepared financial statements.

Navigating the Seattle Housing Market as a First-Time Buyer

Market knowledge specific to Greater Seattle empowers better decisions about timing, neighborhoods, and offer strategies. Understanding local trends helps you compete effectively without overpaying.

Current Market Conditions in King County

Seattle's housing market in 2026 continues balancing strong demand from employment growth against interest rate impacts and inventory fluctuations. Neighborhoods in Seattle proper command premium prices, while surrounding areas like Lynnwood and Mill Creek offer relative affordability.

Median home prices vary significantly across submarkets. A budget of $700,000 might secure a smaller condo in downtown Seattle or Bellevue, while the same amount purchases a single-family home with a yard in Everett or Lake Forest Park. Understanding these geographic variations helps you target searches appropriately.

Making Competitive Offers with Limited Down Payment

Sellers sometimes perceive larger down payments as stronger offers due to reduced financing risk. However, well-structured offers with smaller down payments can compete successfully when paired with strong pre-approval letters and clean contract terms.

Working with a lender who closes quickly provides competitive advantages. The ability to close in 9-10 business days versus the standard 30-45 days makes your offer more attractive, even with a lower down payment. Reducing financing contingency periods from 21 days to 10 days signals confidence and reduces seller uncertainty.

Common Mistakes First-Time Buyers Should Avoid

Learning from others' errors saves money and stress throughout the homebuying process. These frequent mistakes impact first-time buyers across all markets, but carry particular weight in competitive, expensive areas like Seattle.

Skipping the Shopping Process

Research from the FHFA shows that first-time buyers who compare multiple lenders secure better terms and lower costs. Yet many buyers accept the first offer they receive without negotiating or exploring alternatives.

Interest rate differences of just 0.25% impact monthly payments significantly. On a $600,000 loan, that quarter-point equals approximately $85 monthly or over $30,000 in total interest over 30 years. Shopping three to five lenders ensures you're receiving competitive pricing.

Maxing Out Your Approval Amount

Just because you qualify for a certain loan amount doesn't mean you should borrow that much. Lenders approve based on their guidelines, which may exceed your comfort level for monthly payments.

Consider future financial goals, potential income changes, and lifestyle preferences when setting your budget. Buyers who purchase below their maximum approval maintain financial flexibility for emergencies, career transitions, or quality of life expenses.

Making Large Financial Changes During the Process

Once you're pre-approved and searching for homes, avoid major financial changes. New credit card applications, large purchases, job changes, or significant deposits all trigger underwriting questions that can delay or derail your closing.

Activities to avoid during your home purchase:

- Opening new credit accounts

- Making large unexplained deposits

- Changing jobs or employment status

- Co-signing loans for others

- Making major purchases on credit

These actions alter your financial profile from what underwriters initially approved, requiring re-verification and potentially changing your qualification status.

Closing Costs and Cash-to-Close Requirements

Beyond your down payment, closing costs represent a significant upfront expense that surprises many first-time buyers. Understanding these costs and strategies to minimize them prevents last-minute financial stress.

Typical Closing Cost Breakdown

Closing costs generally range from 2-5% of the purchase price, varying based on loan type, property location, and lender fees. On a $650,000 home in Redmond, expect closing costs between $13,000 and $32,500.

| Cost Category | Typical Amount | Who Pays |

|---|---|---|

| Loan origination | 0.5-1% of loan | Buyer |

| Appraisal | $500-$750 | Buyer |

| Title insurance | Varies by price | Split/negotiable |

| Escrow/closing fee | $500-$1,500 | Split/negotiable |

| Recording fees | $200-$400 | Buyer |

| Prepaid property taxes | Varies | Buyer |

| Homeowner's insurance | Annual premium | Buyer |

Washington State customs differ from other regions regarding who pays specific fees. Understanding local practices helps you negotiate effectively and budget appropriately.

Seller Concessions and Lender Credits

Seller concessions allow sellers to contribute toward your closing costs, reducing your cash-to-close requirements. Different loan programs permit varying concession levels, typically ranging from 3% to 6% of the purchase price.

Requesting seller concessions in your offer provides a way to finance closing costs into your mortgage rather than paying them upfront. In slower market conditions or with motivated sellers, this strategy significantly reduces your immediate cash needs.

Lender credits offer another path to lower closing costs. By accepting a slightly higher interest rate, lenders provide credits that offset third-party fees and charges. This trade-off makes sense for buyers prioritizing lower upfront costs over long-term interest savings.

Working with Mortgage Professionals

Selecting the right mortgage professional impacts your experience, outcomes, and long-term satisfaction. The difference between an average loan officer and an exceptional one extends far beyond interest rates.

What to Look for in a Seattle Mortgage Broker

Experience with local markets, specialized knowledge of your employment situation, and a track record of reliable communication distinguish top mortgage professionals. For buyers working in tech industries throughout Seattle and Bellevue, finding a broker who understands complex compensation structures proves essential.

Look for professionals with:

- Licensed expertise in Washington State lending

- Specialized knowledge of your income type (W-2, tech compensation, self-employed)

- Proven track record with verifiable reviews across multiple platforms

- Lender relationships that provide access to competitive pricing

- Communication standards that match your expectations

HUD research demonstrates that homebuyer education and professional guidance improve both mortgage selection and long-term satisfaction with financing decisions.

Questions to Ask Your Lender

Interviewing potential lenders helps you identify the best fit for your situation. Don't hesitate to ask detailed questions about rates, fees, timelines, and their approach to your specific circumstances.

- What interest rate and APR can you offer based on my situation?

- What are your total lender fees and third-party costs?

- How do you handle complex income like RSUs or bonuses?

- What's your typical timeline from application to closing?

- How do you communicate throughout the process?

- Can you provide recent client references?

Transparent answers to these questions reveal professionalism, expertise, and whether the lender's approach aligns with your needs. Evasive responses or pressure tactics signal problems you'll likely encounter throughout the process.

Next Steps on Your Path to Homeownership

Starting your journey toward owning your first home involves strategic preparation and informed decision-making. Understanding mortgage for first time homebuyers options, qualification requirements, and local market dynamics positions you for success in the competitive Greater Seattle housing market.

Begin by reviewing your credit reports and scores to identify improvement opportunities. Calculate your realistic budget including not just monthly payments but maintenance, insurance, and reserves for unexpected expenses. Research neighborhoods throughout Seattle, Shoreline, Lynnwood, and surrounding communities to understand where your budget aligns with your lifestyle preferences.

Connect with experienced professionals who serve first-time buyers daily. A qualified mortgage broker familiar with local markets, complex income qualification, and various loan programs helps you navigate options and secure optimal financing for your specific situation.

Understanding your financing options and working with experienced professionals transforms the complex mortgage process into a manageable path toward homeownership. Whether you're a tech professional in Seattle navigating RSU qualification, a veteran exploring VA loan benefits, or a first-time buyer comparing FHA and conventional programs, having knowledgeable guidance makes all the difference in competitive markets. Keith Akada at Mortgage Reel brings over 25 years of experience helping first-time buyers throughout Seattle, Bellevue, Redmond, and Kirkland secure the right financing for their homeownership goals, with the ability to close in as few as 9 business days and expertise in qualifying complex tech compensation.