Finding a qualified mortgage loan broker near me has become a priority for homebuyers navigating Seattle's competitive real estate market in 2026. With mortgage rates fluctuating and lending guidelines evolving, working with a local mortgage broker who understands regional market dynamics and lender relationships can make the difference between a smooth transaction and a stressful experience. This guide explains what mortgage brokers do, how they differ from direct lenders, and what to look for when choosing a professional in the Greater Seattle area.

What Does a Mortgage Loan Broker Actually Do?

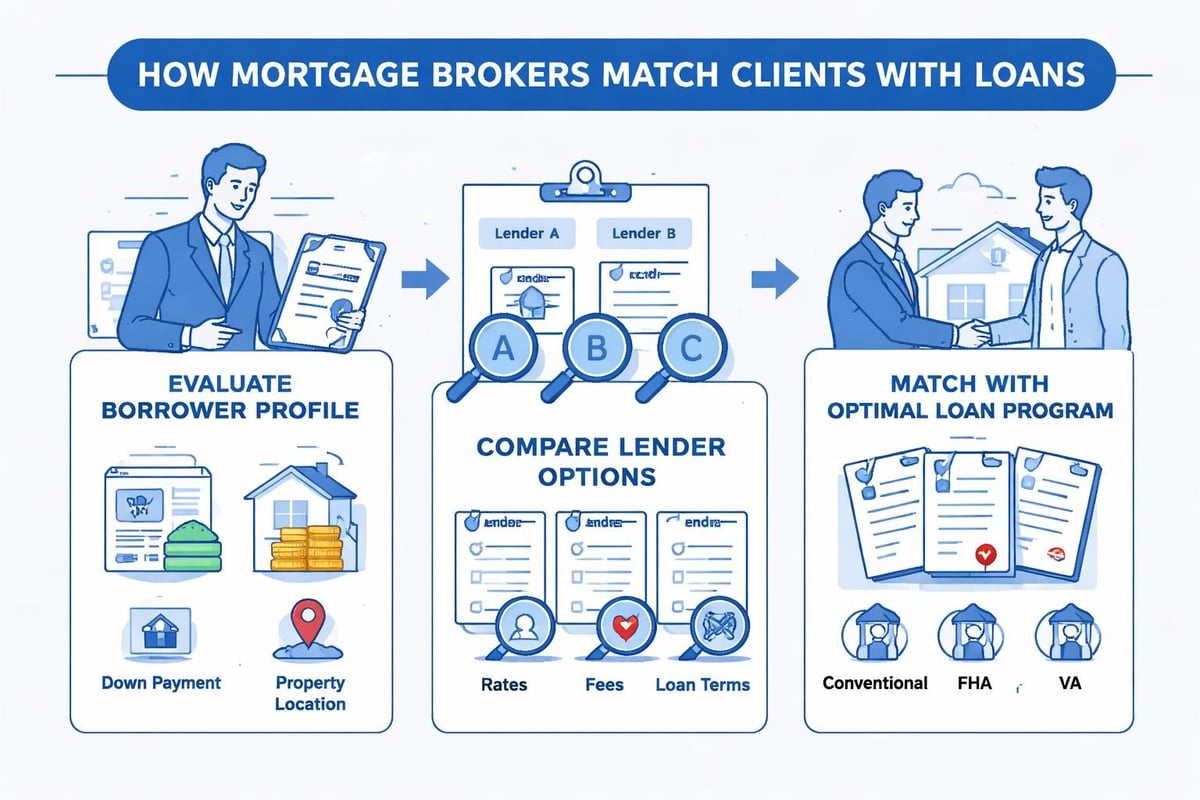

A mortgage loan broker serves as an intermediary between borrowers and lenders, helping you identify loan products that match your financial situation and homeownership goals. Unlike loan officers employed by a single bank or credit union, brokers have access to multiple lending sources and can compare rates, terms, and qualification requirements across different institutions.

The Broker Advantage in Seattle's Housing Market

When you search for a mortgage loan broker near me in Seattle, you're accessing a professional who works on your behalf rather than representing a single lender's interests. This distinction matters significantly in competitive markets like Bellevue, Redmond, and Kirkland, where pricing and speed can determine whether you secure a property.

Key services mortgage brokers provide:

- Pre-qualification and pre-approval letters that strengthen purchase offers

- Rate shopping across multiple wholesale lenders

- Guidance on loan programs including conventional, FHA, VA, and jumbo products

- Documentation review and application preparation

- Coordination with underwriters, processors, and closing teams

- Problem-solving when qualification challenges arise

Brokers also specialize in specific borrower profiles. In the Seattle tech corridor, many brokers focus on qualifying complex income structures including RSUs, stock compensation, and bonus income from employers like Amazon, Microsoft, and Google.

Understanding Mortgage Broker Licensing and Regulations

All mortgage brokers must be licensed under state and federal law. In Washington State, mortgage broker licensing requires education, testing, background checks, and ongoing compliance with the Department of Financial Institutions. This regulatory framework protects consumers and ensures brokers maintain professional standards.

The SAFE Act established nationwide minimum standards for mortgage loan originator licensing. Under these rules, individuals required to be licensed must complete pre-licensing education, pass the National Mortgage Licensing System exam, and maintain continuing education credits annually.

What Licensing Means for Borrowers

When you work with a licensed mortgage loan broker near me, you benefit from regulatory oversight that wasn't always standard in the mortgage industry. Licensed professionals must adhere to disclosure requirements, maintain surety bonds, and follow ethical lending practices.

| Requirement | Purpose | Consumer Benefit |

|---|---|---|

| Background check | Screen for criminal history and financial misconduct | Protection from predatory practices |

| Pre-licensing education | Ensure knowledge of lending laws and products | Competent advice and guidance |

| Continuing education | Stay current on regulation changes | Up-to-date information |

| Errors and omissions insurance | Financial protection for mistakes | Recourse if issues arise |

Mortgage Broker vs. Direct Lender: Understanding the Difference

A common question when researching mortgage loan broker near me is whether to work with a broker or apply directly with a bank. Both pathways have merits, but they function differently and serve distinct purposes.

How Brokers Access Wholesale Lending

Mortgage brokers work with wholesale lenders who don't market directly to consumers. These wholesale channels often offer more competitive pricing than retail bank branches because they have lower overhead costs. A loan broker acts as the intermediary who sources these wholesale rates and presents them to borrowers.

Direct lender characteristics:

- Single source of funding

- In-house underwriting and processing

- Limited product variety

- Retail pricing structure

Mortgage broker characteristics:

- Multiple lender relationships

- Access to wholesale pricing

- Broader product selection

- Ability to shop rates without multiple credit inquiries

In markets like Shoreline and Lynnwood, where property types range from condos to single-family homes and new construction, having access to diverse loan products helps match the right financing to each property and borrower situation.

What to Look for When Choosing a Mortgage Broker

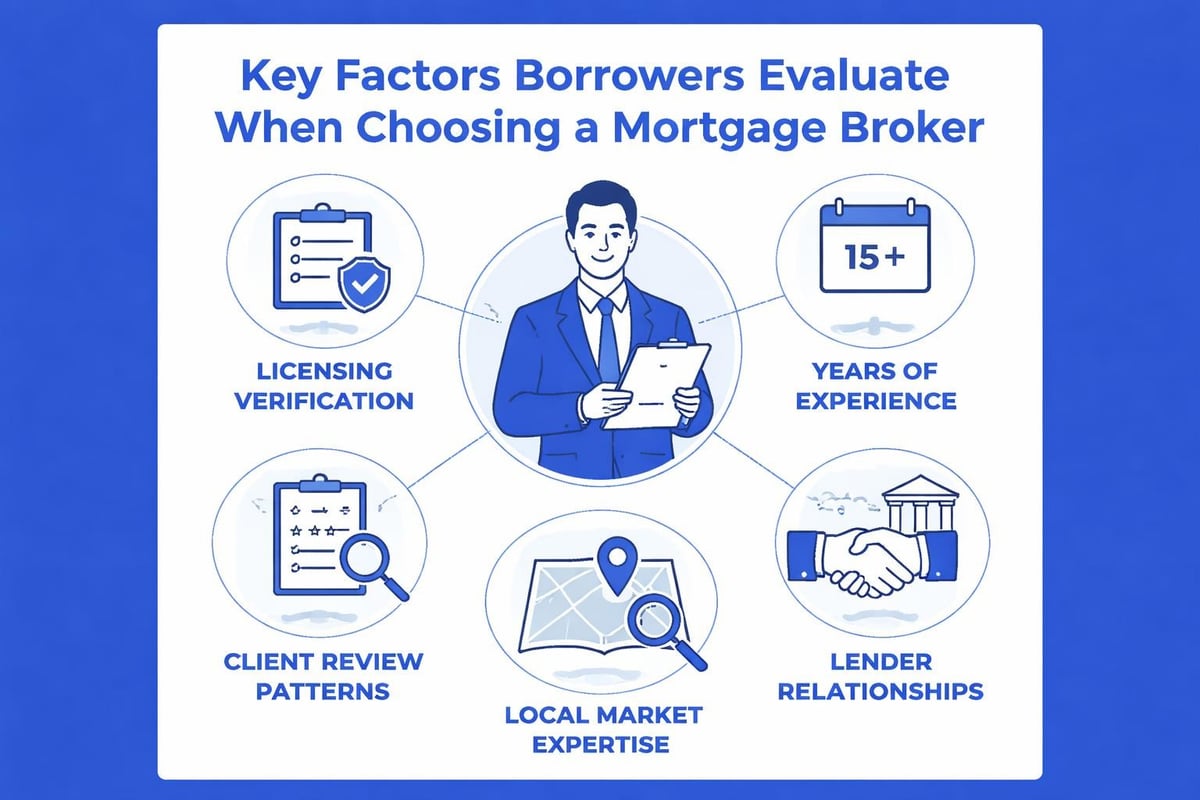

Not all mortgage brokers deliver the same experience or results. When searching for a mortgage loan broker near me in 2026, specific qualifications and track records separate exceptional professionals from average ones.

Experience and Market Knowledge

Years in the business matter, but so does current market activity. A broker who closed hundreds of loans during the 2020-2021 refinance boom may have different strengths than one actively navigating today's purchase-focused market. Look for professionals who demonstrate deep knowledge of Seattle-area neighborhoods, pricing trends, and local lender preferences.

Questions to ask prospective brokers:

- How many purchase transactions did you close in the past 12 months?

- Which lenders do you work with most frequently and why?

- What percentage of your clients are first-time homebuyers versus repeat buyers or refinances?

- How do you handle complex income documentation for tech employees?

- What is your average timeline from application to closing?

Client Reviews and Professional Reputation

In 2026, verified reviews across platforms like Google, Zillow, Redfin, Yelp, and WalletHub provide transparent insight into a broker's service quality. Pay attention to themes in reviews rather than individual comments. Consistent praise for communication, problem-solving, and closing efficiency indicates reliable performance.

Common Loan Programs Available Through Mortgage Brokers

When you connect with a mortgage loan broker near me, you gain access to a comprehensive range of financing options. Understanding these programs helps you have more productive initial conversations and set realistic expectations.

Conventional Loans

Conventional mortgages conforming to Fannie Mae and Freddie Mac guidelines remain the most common loan type in Seattle and surrounding areas. These loans typically require:

- Minimum 3% down payment for first-time buyers

- 5% down for subsequent purchases

- Credit scores of 620 or higher (though 680+ is more competitive)

- Debt-to-income ratios generally below 50%

Government-Backed Programs

FHA loans serve borrowers with lower credit scores or limited down payment funds. In Lake Forest Park and Mill Creek, FHA financing helps first-time buyers enter the market with as little as 3.5% down.

VA loans provide zero-down financing for eligible veterans and active-duty service members. With no private mortgage insurance requirement, VA loans often deliver the lowest monthly payments.

USDA loans apply in select areas outside Seattle's urban core, though availability is limited in King and Snohomish Counties.

Jumbo Loans for High-Value Properties

Seattle's median home prices frequently exceed conforming loan limits, making jumbo financing essential. In 2026, loans above $806,500 (the conforming limit for King County) require jumbo underwriting. These loans typically demand:

- Higher credit scores (usually 700+)

- Larger down payments (often 10-20%)

- Extensive income documentation

- Significant cash reserves

Tech professionals with substantial equity compensation often benefit from brokers who specialize in jumbo loan qualification and understand how to document stock-based income.

How Mortgage Brokers Handle Complex Income Documentation

For Seattle-area homebuyers working at major technology employers, income documentation extends beyond simple W-2 forms. Equity compensation in the form of RSUs, ESPP shares, and performance bonuses requires specialized underwriting knowledge.

Qualifying Stock Compensation

Most lenders allow RSUs and stock options to be counted as qualifying income if they meet specific criteria:

- Two-year history of receiving equity compensation

- Vesting schedule documentation

- Average income calculation based on recent grant values

- Consideration of tax implications

A knowledgeable mortgage loan broker near me can work with lenders who have established guidelines for technology sector compensation, rather than requiring manual underwriting or excluding this income entirely.

| Income Type | Typical Documentation | Underwriting Approach |

|---|---|---|

| Base salary | W-2 and pay stubs | Straightforward qualification |

| Annual bonus | Two-year history via W-2 | Average over 24 months |

| RSUs (vested) | Grant agreements, vesting schedule, tax returns | Average with continuance verification |

| Stock options | Exercise history, current holdings | Case-by-case evaluation |

The Mortgage Application Timeline in 2026

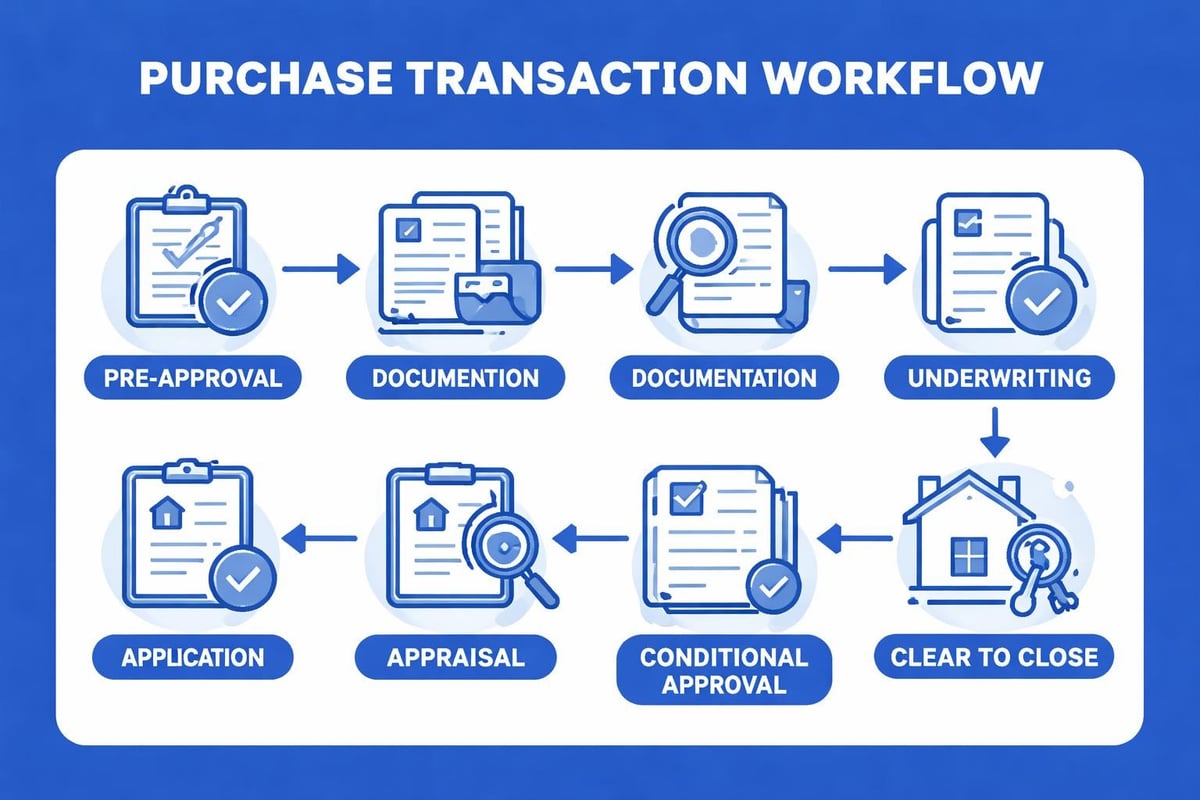

Understanding realistic timelines helps you plan effectively, especially in competitive neighborhoods where sellers expect quick closings. When working with an experienced mortgage loan broker near me, the process typically follows these phases.

Pre-Approval Phase (1-3 Days)

Before house hunting, obtain a comprehensive pre-approval that includes:

- Credit report review

- Income and asset verification

- Debt obligation analysis

- Preliminary underwriting approval

Strong pre-approval letters carry more weight with listing agents in Everett and throughout King County, particularly when multiple offers compete.

Application to Clear-to-Close (15-25 Days)

Once you're under contract, the formal application process begins:

- Application submission and initial disclosure (Day 1)

- Documentation collection and review (Days 2-5)

- Appraisal ordering and completion (Days 3-12)

- Underwriting review and conditional approval (Days 7-15)

- Condition clearance and final approval (Days 12-20)

- Clear-to-close status (Days 18-25)

Advanced underwriting platforms and experienced broker coordination can compress this timeline significantly. Some lenders now offer nine-business-day closings when all documentation is complete and properties appraise smoothly.

Cost Structure: How Mortgage Brokers Get Paid

Transparency about compensation helps you understand the mortgage loan broker near me relationship. Brokers are compensated through lender-paid commissions, borrower-paid fees, or a combination of both.

Lender-Paid Compensation

Most wholesale lenders pay brokers a percentage of the loan amount (typically 0.5% to 2.5%) as an origination fee built into the interest rate. This structure means you don't write a separate check to the broker, but the cost is reflected in your rate.

Borrower-Paid Origination

Some brokers charge direct origination fees to the borrower while offering lower interest rates. This approach can benefit borrowers who plan to keep loans long-term and want to minimize monthly payments.

Fee comparison example:

- Lender-paid: 0% origination fee, 6.75% interest rate

- Borrower-paid: 1% origination fee ($8,000 on $800,000 loan), 6.50% interest rate

Your broker should present both options with break-even analysis showing how long it takes for the lower rate to offset the upfront fee.

Questions to Ask During Your Initial Consultation

Your first conversation with a mortgage loan broker near me should establish whether they're the right fit for your situation. Come prepared with specific questions that reveal their expertise and approach.

Loan Product Knowledge

- Which loan programs do you recommend for my situation and why?

- How do current rates compare to recent averages?

- What down payment options minimize monthly costs while avoiding PMI?

Process and Communication

- How frequently will you update me during the process?

- Who handles my file day-to-day (you or a team member)?

- What happens if issues arise during underwriting?

Market-Specific Expertise

- How familiar are you with the neighborhoods I'm considering?

- Do you have relationships with appraisers who know these areas?

- What percentage of your business comes from repeat clients and referrals?

Local Market Considerations for Seattle Homebuyers

Seattle's real estate landscape in 2026 presents unique challenges that benefit from local broker expertise. Inventory constraints, competitive bidding, and neighborhood-specific pricing patterns all influence your financing strategy.

Appraisal Challenges

Properties in rapidly appreciating neighborhoods sometimes appraise below contract price, creating funding gaps. Experienced brokers anticipate this risk and structure offers accordingly, potentially including appraisal gap coverage or recommending lenders with more current comparable sale data.

Condominium Financing

Seattle's condo market requires special attention to warrantability. Buildings must meet Fannie Mae, Freddie Mac, FHA, or VA project approval standards. A knowledgeable mortgage loan broker near me maintains updated lists of approved buildings and can quickly assess whether a specific property qualifies for conventional financing.

New Construction Considerations

Builder partnerships in areas like Mill Creek often come with preferred lender incentives. However, these may not always deliver the best overall value. Brokers help you evaluate whether builder credits outweigh potentially higher rates or fees.

Why Local Expertise Matters in Greater Seattle

Geographic knowledge extends beyond knowing neighborhood names. Effective mortgage brokers understand property tax variations between jurisdictions, HOA fee structures in different developments, and which lenders have strong relationships with local title companies and real estate attorneys.

Lender Overlay Variations

While base lending guidelines come from Fannie Mae, Freddie Mac, FHA, and VA, individual lenders add their own overlays. Some lenders avoid condos with litigation history, while others decline properties with certain foundation types or specific HOA structures. A broker with deep lender knowledge can match your property to institutions most likely to approve quickly.

Regional factors affecting loan approval:

- Seattle-area property tax rates varying by jurisdiction

- HOA fee thresholds that trigger additional scrutiny

- Waterfront property restrictions

- Mixed-use building financing limitations

- Seismic retrofit requirements for older buildings

Red Flags to Avoid When Choosing a Broker

Not every mortgage loan broker near me delivers ethical, competent service. Watch for warning signs that indicate you should continue your search.

Pressure Tactics and Unrealistic Promises

Legitimate brokers provide honest assessments of what you qualify for and realistic timelines. Be cautious of professionals who:

- Guarantee specific rates without reviewing your full financial profile

- Promise approvals despite credit or income challenges

- Pressure you to move forward before you're ready

- Discourage you from comparing their services to competitors

Poor Communication Patterns

Responsiveness during the shopping phase predicts behavior during your transaction. Brokers who take days to return calls or provide vague answers to direct questions likely won't improve once you're under contract.

Lack of Transparency About Fees

Request a detailed Loan Estimate within three business days of application. This document, required by federal law, breaks down all costs associated with your loan. Brokers who hesitate to discuss fees or provide clear explanations warrant skepticism.

Working with Multiple Brokers: Best Practices

Some borrowers contact several brokers simultaneously to compare options. While this approach has merit, understand how it affects your credit and process efficiency.

Credit Inquiry Consolidation

Mortgage credit inquiries within a 45-day window count as a single pull for scoring purposes. This protection allows rate shopping without damaging your credit score. However, submitting full applications to multiple brokers creates unnecessary paperwork and potential confusion.

Recommended approach:

- Interview 2-3 brokers via phone or video consultation

- Request rate quotes based on your scenario (no credit pull needed)

- Choose one broker for formal application

- Give them opportunity to match or beat competing offers

This strategy provides market insight while streamlining the actual application process.

Technology and the Modern Mortgage Experience

In 2026, mortgage loan broker near me searches increasingly prioritize digital capabilities alongside personal service. The best brokers combine high-touch consultation with efficient technology platforms.

Digital Documentation and Communication

Expect secure portals for uploading tax returns, pay stubs, and bank statements. Electronic disclosure signing and mobile-friendly interfaces have become standard. However, technology should enhance rather than replace human expertise and accessibility.

Rate Lock Platforms

Real-time rate lock technology allows you to secure pricing when markets are favorable, even outside business hours. Some brokers provide apps that send alerts when rates drop to your target threshold.

Special Considerations for Investment Properties

If you're searching for a mortgage loan broker near me to finance rental properties or second homes, qualification differs from primary residence purchases.

Investment Property Requirements

Conventional investment property loans typically require:

- 15-25% down payment

- Six months cash reserves (PITI payment)

- Credit scores of 680+

- Lower debt-to-income ratio allowances

- Documentation of rental income for properties you already own

Brokers experienced with investor financing understand how to count projected rental income, structure entities for multiple properties, and identify portfolio lenders for borrowers exceeding conventional loan count limits.

Bridge Loans and Contingent Offers

Seattle's competitive market makes contingent offers (dependent on selling your current home) less attractive to sellers. Bridge financing provides alternatives worth discussing with your mortgage loan broker near me.

Bridge Loan Mechanics

These short-term loans allow you to access equity in your current home for down payment on a new property before selling. Once your existing home closes, you pay off the bridge loan.

Bridge loan considerations:

- Higher interest rates than traditional mortgages

- Fees typically 1-2% of loan amount

- 6-12 month terms

- Qualification based on carrying both payments temporarily

Not all brokers have bridge loan access, making this a specific question during initial consultations if you anticipate needing this strategy.

Finding the right mortgage loan broker near me in Seattle means identifying a licensed professional who combines deep lender relationships, local market expertise, and clear communication with competitive pricing and efficient execution. Whether you're a first-time buyer in Lynnwood, a tech professional purchasing in Bellevue, or an investor expanding your portfolio in Everett, the right broker partnership simplifies your transaction and often saves you thousands over the life of your loan. Keith Akada brings over 25 years of experience serving Greater Seattle homebuyers through Mortgage Reel, with specialized expertise in complex income qualification, jumbo financing, and fast closings backed by 750+ five-star reviews across major platforms.