Seattle’s housing market is changing rapidly, and understanding your options has never been more important. As 2026 approaches, the landscape for rate home mortgage products across Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett is shifting.

This guide is designed to give you the clarity and confidence you need to navigate upcoming mortgage rate changes. You will learn about 2026’s projected rate trends, evolving lending requirements, and proven strategies for securing the best deals.

We will break down local market insights, compare loan types, and provide step-by-step actions so you can make informed decisions and achieve your homeownership goals.

2026 Mortgage Rate Outlook: What Seattle Homebuyers Need to Know

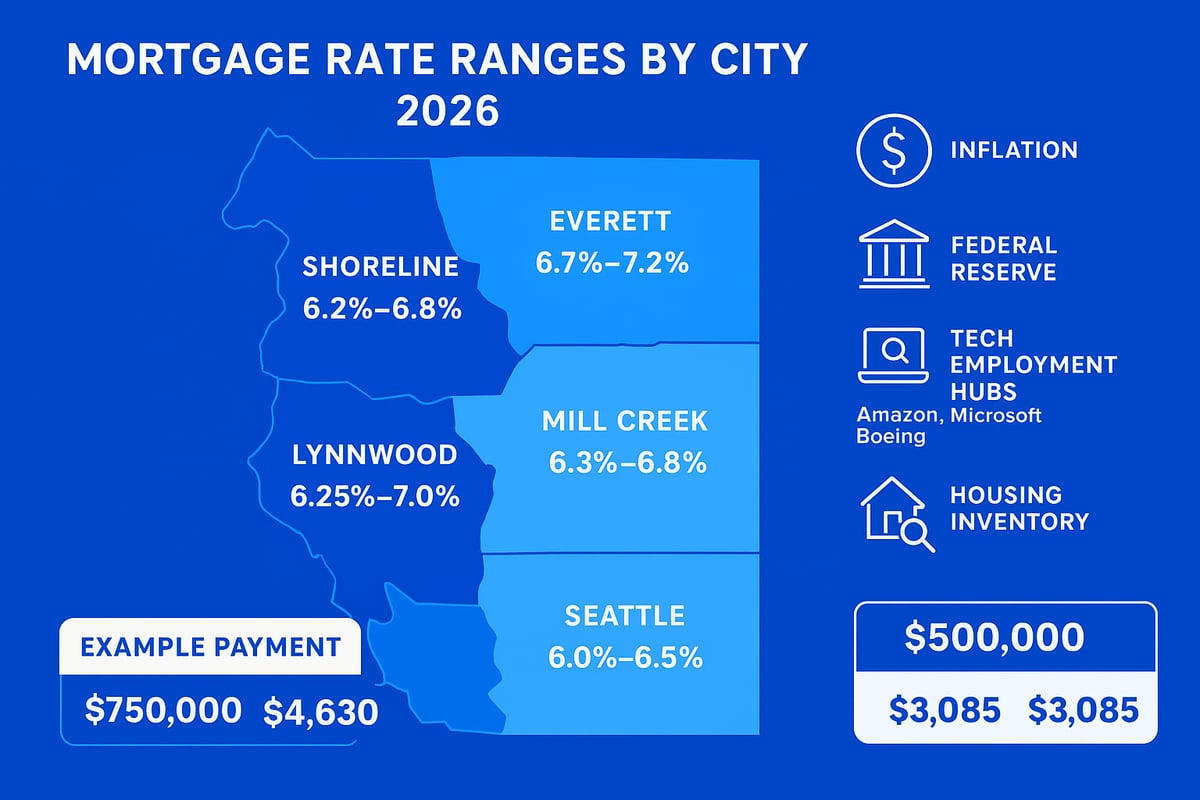

Seattle's housing market continues to draw attention as we enter 2026, with rate home mortgage trends at the center of every homebuyer's strategy. The national average for a 30-year fixed mortgage stands at 6.098% as of February 2026, while Seattle and surrounding cities like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett see local variations. Understanding where rates are headed is key to making informed decisions in this dynamic Pacific Northwest market.

Several factors are shaping the direction of rate home mortgage options for Seattle-area buyers. The Federal Reserve's monetary policy remains a primary driver, with recent rate adjustments aimed at controlling inflation. As inflation rates fluctuate, the cost of borrowing responds accordingly. In Seattle, strong local employment—especially in the tech sector with companies like Amazon, Microsoft, and Boeing—bolsters economic stability and influences lender risk assessments. Housing supply, which continues to be tight in many neighborhoods, adds upward pressure on rates as demand remains strong.

When comparing Seattle to the national landscape, rate home mortgage averages tend to be slightly lower than the national figure, reflecting the region's lower default risks and higher median incomes. For instance, while the U.S. average sits at 6.098%, Seattle's 30-year fixed rates often range from 5.825% to 5.875% among top lenders. Neighboring cities such as Lynnwood and Everett may see marginally higher or lower rates based on property type, loan amount, and borrower profile. These differences are influenced by local economic growth and city-specific housing inventory.

Historical context provides valuable perspective for those tracking rate home mortgage shifts. From 2023 to 2025, rates in Seattle climbed from the low 5% range to over 6% before stabilizing in early 2026. Seasonal trends show that rates often fluctuate most in late spring and early fall, coinciding with peak homebuying periods. This means that timing your application can have a measurable impact on the final rate you secure.

To illustrate, consider a $750,000 home purchase in Seattle compared to a $500,000 home in Lynnwood. With a 20% down payment and excellent credit, a Seattle buyer might secure a 30-year fixed rate near 5.85%, resulting in a monthly principal and interest payment of roughly $3,544. In Lynnwood, the lower loan amount and similar rate home mortgage offer would yield a payment closer to $2,366. These calculations highlight how both loan size and location affect your bottom line.

| Loan Type | Seattle Rate Range | Lynnwood Rate Range | Example Payment (Seattle, $750k, 20% down) | Example Payment (Lynnwood, $500k, 20% down) |

|---|---|---|---|---|

| 30-Year Fixed | 5.825%–5.875% | 5.85%–5.90% | $3,544 | $2,366 |

| 15-Year Fixed | 4.99%–5.5% | 5.05%–5.55% | $5,012 | $3,286 |

| 5/1 ARM | 5.25%–5.75% | 5.30%–5.80% | $3,295 | $2,198 |

For the latest local figures, review Seattle mortgage rates today to see how current offerings compare across King and Snohomish counties.

As we look ahead, staying informed about the evolving rate home mortgage environment is crucial for Seattle buyers and homeowners. By tracking local economic indicators and understanding how national trends filter down to the Puget Sound region, you can position yourself to secure the most favorable rate possible.

Understanding Mortgage Rate Structures and Loan Types in 2026

Navigating the rate home mortgage landscape in Seattle and neighboring cities requires a clear understanding of loan structures and how different options can affect your monthly payment, qualification, and long-term financial security. Whether you’re buying in Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, choosing the right mortgage type is one of the most important decisions you’ll make.

Fixed-Rate vs. Adjustable-Rate: What’s Right for You?

The foundation of any rate home mortgage decision starts with choosing between a fixed-rate and an adjustable-rate mortgage (ARM). A fixed-rate mortgage offers predictable payments for the life of the loan, making it a popular choice for Seattle buyers who value stability. In contrast, ARMs such as the 5/1 ARM offer a lower initial rate that adjusts after a set period, which can be appealing if you plan to move or refinance within a few years.

For example, a 30-year fixed loan on a $750,000 Seattle home might offer a rate of 5.825%, while a 5/1 ARM could start closer to 5.25% but adjust after five years. The right option depends on your financial goals and how long you plan to stay in your home.

Popular Loan Types in Seattle and Surrounding Cities

Seattle’s competitive housing market means buyers often encounter a variety of rate home mortgage products. The most common options include:

- 30-Year Fixed: Consistent payments, ideal for long-term owners.

- 15-Year Fixed: Higher monthly payments, but lower total interest paid.

- 5/1 ARM: Lower initial rate, adjusts annually after five years.

- FHA Loans: Low down payment, flexible credit requirements.

- VA Loans: Exclusive to veterans and active-duty service members, often with no down payment.

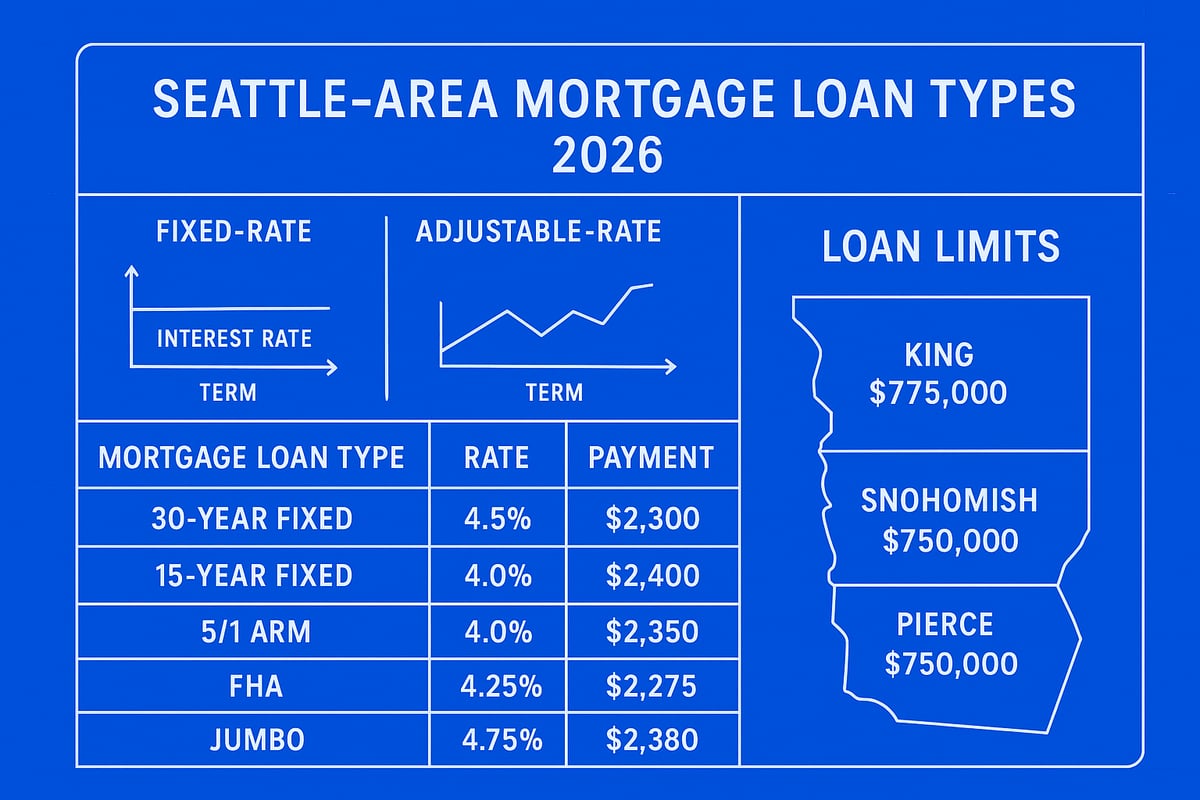

- Jumbo Loans: For homes above conforming loan limits, common in King and Snohomish counties.

Each loan type comes with its own rate range. In 2026, 30-year fixed rates in Seattle are averaging 5.825–5.875%, while 15-year fixed rates run 4.99–5.5%. Jumbo loans, necessary for higher-priced homes in Mill Creek or Seattle, are trending between 5.625% and 5.944%.

How Loan Limits Impact Your Choices

Loan limits are especially important in high-cost areas like Seattle, Shoreline, and Everett. For 2026, conforming loan limits in King and Snohomish counties are expected to remain elevated, enabling buyers to secure more competitive rates on homes up to the limit. Anything above becomes a jumbo loan, which often carries stricter requirements and slightly higher rates.

For instance, if you’re purchasing a $900,000 home in Mill Creek, a conventional loan might not cover the full amount, requiring you to explore jumbo options. This shift can impact not only your rate home mortgage but also your down payment and qualification standards.

| Loan Type | Loan Limit (2026) | Typical Rate | Down Payment Requirement |

|---|---|---|---|

| Conforming | $766,550 | 5.825%–5.875% | 3%–20% |

| Jumbo | >$766,550 | 5.625%–5.944% | 10%–20% |

| FHA | $977,500* | 5.375%–6.355% | 3.5% |

| VA | No limit | 5.25%–5.85% | 0% |

*Varies by county

FHA, VA, and USDA: Government-Backed Options

Government-backed loans offer unique benefits for qualified Seattle-area buyers. FHA loans are especially popular with first-time buyers due to their flexible credit requirements and low down payments. VA loans serve veterans and active military, providing zero down options and competitive rates. USDA loans, while less common in dense urban areas, offer affordable financing in select rural parts of Snohomish and Pierce counties.

Understanding the differences between these loan types is crucial for selecting the right rate home mortgage. For a deeper dive into FHA programs and how their rate structures work, see FHA home loans explained.

Investment and Second Home Considerations

If you’re buying an investment property or second home in Lynnwood, Lake Forest Park, or Everett, expect slightly higher rates and stricter qualifying criteria. Lenders typically require larger down payments and may factor in projected rental income, especially for multi-unit properties. These nuances can influence your final rate home mortgage and should be part of your strategy if you’re expanding your real estate portfolio.

Comparing Payments: Conventional vs. Jumbo in Mill Creek

Let’s compare two scenarios for a $900,000 home in Mill Creek:

- Conventional Loan: If you put enough down to stay within the conforming limit, your rate home mortgage might be 5.85%, with a lower monthly payment and easier qualification.

- Jumbo Loan: If you need to borrow above the limit, expect a rate closer to 5.944%, with a higher monthly payment and stricter documentation for assets and income.

This difference can translate to hundreds of dollars each month, making it vital to understand all your loan options and how they fit your financial goals.

Seattle’s mortgage landscape in 2026 continues to evolve, with choices shaped by local loan limits, property values, and borrower profiles. By understanding the range of rate home mortgage products available, you can make informed decisions whether you’re buying in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett.

Factors That Influence Your Mortgage Rate in Seattle

Understanding what shapes your rate home mortgage is essential if you are buying or refinancing in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett. Local lenders evaluate several factors to determine the rate you will qualify for, and even small changes can affect your monthly payment and long-term costs.

Let us explore the main elements that impact your rate home mortgage, with real examples from across the Greater Seattle area.

How Your Credit Score Impacts Your Rate Home Mortgage

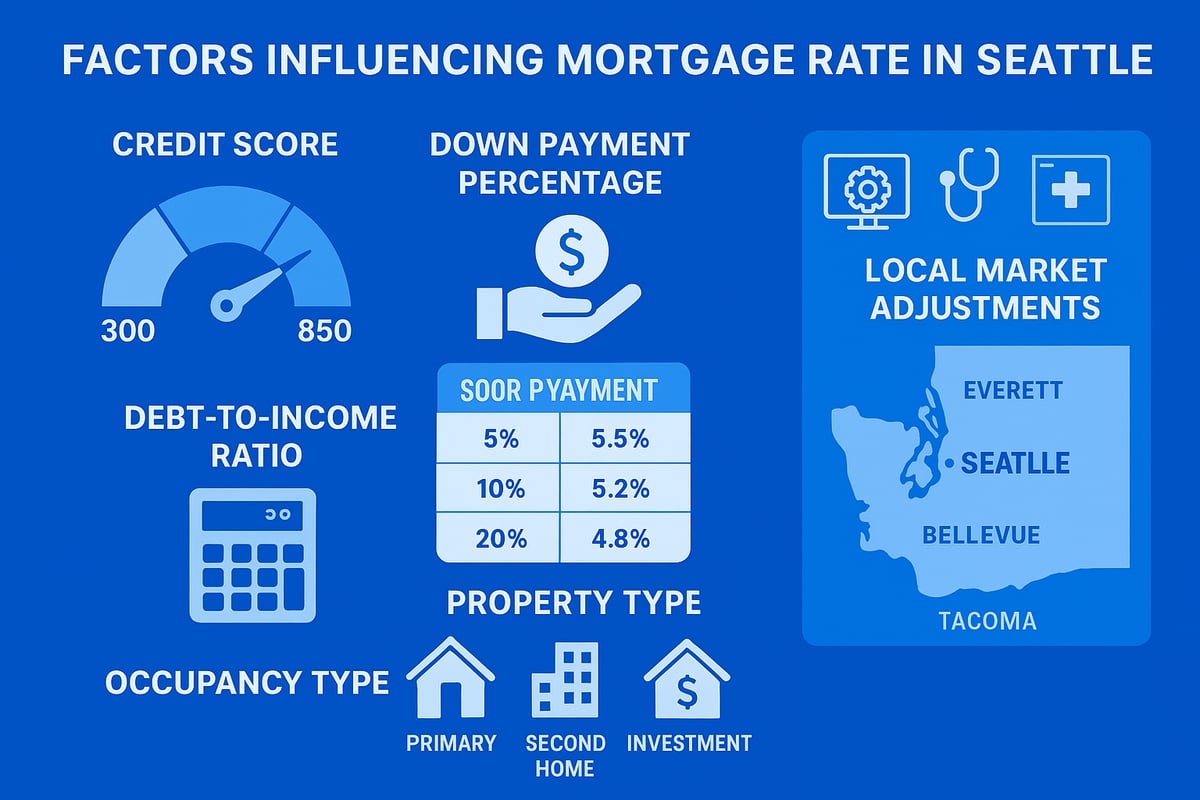

Your credit score is one of the most significant drivers of your rate home mortgage. In Seattle, lenders typically offer the best rates to borrowers with scores of 760 or higher. If your FICO score falls between 680 and 700, you may see a rate increase of 0.25 percent or more compared to top-tier borrowers.

A higher credit score signals lower risk to lenders, which can save you thousands over the life of your loan. For example, a buyer in Mill Creek with a 780 score might secure a 30-year fixed rate at 5.825 percent, while a similar borrower in Everett with a 690 score could be offered 6.1 percent for the same loan scenario.

Down Payment, LTV, and DTI: Core Rate Drivers

Your down payment amount and resulting loan-to-value (LTV) ratio have a direct effect on your rate home mortgage. Putting down 20 percent or more can often reduce your rate by up to 0.25 percent and eliminate private mortgage insurance (PMI). Lenders also consider your debt-to-income (DTI) ratio, which is the percentage of your monthly income that goes toward debt payments. Most Seattle lenders prefer a DTI below 43 percent for best rates.

If you are exploring different down payment strategies, review the down payment options in Washington to see how your upfront investment can impact your rate and long-term affordability.

Property Type and Occupancy: Local Market Nuances

The type of property you are buying and how you intend to use it will affect your rate home mortgage. Single-family homes in Seattle and Shoreline generally qualify for the lowest rates. Condos may carry a slightly higher rate due to perceived risk, and multi-unit properties or investment homes often have a rate premium of 0.125 to 0.5 percent.

Occupancy matters as well. Primary residences get the best pricing, while second homes and investment properties in Lynnwood, Lake Forest Park, and Everett may see higher rates and stricter underwriting.

Real Examples from Seattle and Surrounding Cities

Local market risk assessments can cause small rate adjustments across the region. For instance, a 20 percent down payment on a $600,000 home in Lake Forest Park could lower your rate home mortgage by 0.25 percent compared to a 5 percent down scenario. Here is a quick comparison:

| Scenario | Loan Amount | Down Payment | Estimated Rate | Monthly Payment* |

|---|---|---|---|---|

| Seattle, 760 FICO, 20% down | $480,000 | $120,000 | 5.825% | $2,728 |

| Everett, 690 FICO, 5% down | $570,000 | $30,000 | 6.1% | $3,456 |

*Assumes 30-year fixed, principal and interest only.

Each factor—credit, down payment, DTI, property type, and market—plays a key role in your rate home mortgage. Taking steps to optimize these elements can help you secure the most competitive terms in Seattle and nearby cities.

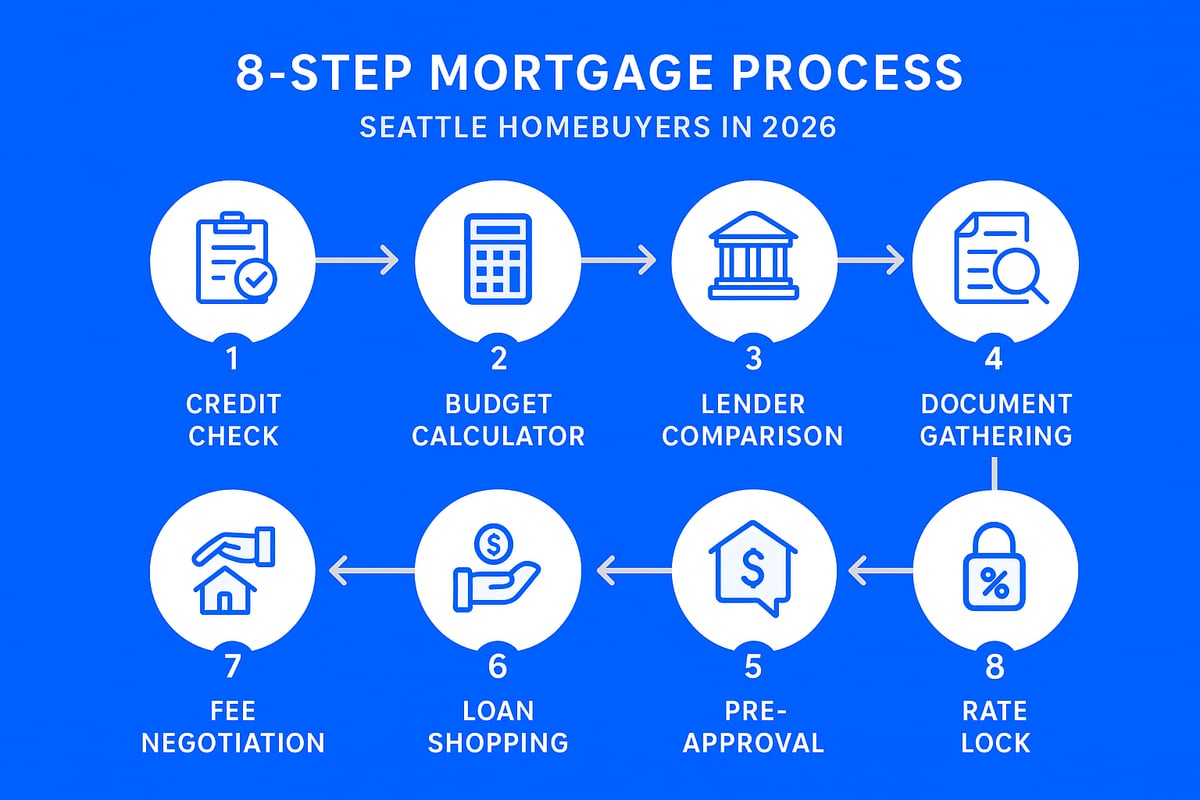

Step-By-Step Guide: Securing the Best Mortgage Rate in 2026

Navigating the Seattle-area mortgage market in 2026 requires a strategic, step-by-step approach. Whether you are buying your first home in Shoreline, moving up in Mill Creek, or investing in Everett, following these actionable steps will help you secure the best rate home mortgage for your needs.

Step 1: Review and Strengthen Your Credit

Start by checking your credit report for errors or outdated information. In Seattle and surrounding areas, a higher credit score directly lowers your rate home mortgage. Aim for at least 760 to access the most competitive rates. Address any issues immediately, as even a small increase in your score can save you thousands over the life of your loan.

Step 2: Determine Your Budget and Affordability

Use Seattle-specific affordability calculators to estimate your price range, factoring in property taxes, insurance, and HOA fees common in Lynnwood and Mill Creek. Consider your monthly income, debts, and lifestyle needs. This step helps you understand how much rate home mortgage you can comfortably manage without stretching your finances.

Step 3: Compare Lenders Across Seattle, Shoreline, and Everett

Research a mix of banks, credit unions, and local mortgage brokers. Each may offer different rate home mortgage options and fee structures. Look for lenders experienced with Seattle’s unique market, and do not hesitate to ask for detailed loan estimates. Comparing offers side by side ensures you do not miss out on favorable terms.

Step 4: Gather and Organize Documentation

Prepare essential documents such as W-2s, pay stubs, bank statements, and asset records. If you are a tech worker in Redmond or Bellevue, include RSU or stock compensation statements. Having documents ready speeds up the pre-approval process and shows sellers you are a serious buyer.

Step 5: Get Pre-Approved for a Competitive Edge

A pre-approval letter from a local expert is crucial in Seattle’s fast-paced market. It demonstrates to sellers that you are qualified, which can give you an advantage in bidding wars. Pre-approval timelines in Seattle often range from 9 to 30 days, depending on your situation and lender responsiveness.

| Task | Typical Timeline (Seattle Area) |

|---|---|

| Pre-Approval | 1-5 business days |

| Home Search/Bidding | 1-4 weeks |

| Loan Processing | 7-21 business days |

| Closing | 9-30 days |

Step 6: Shop Loan Options and Compare Rates

Explore loan products like conventional, FHA, VA, and jumbo loans. For homes above local conforming limits, you may need a jumbo loan. If you are considering homes in Mill Creek or Lake Forest Park above $850,000, review Jumbo home loans Washington for detailed rate and qualification guidelines. Always compare both interest rates and APRs to get a true picture of your total costs.

Step 7: Negotiate Lender Fees and Ask About Credits

Once you have selected a lender, review the loan estimate for origination fees, points, and third-party charges. Negotiate wherever possible. Some Seattle lenders may offer credits to offset closing costs, particularly for buyers with strong profiles or larger down payments. Do not hesitate to ask for these incentives.

Step 8: Lock Your Rate at the Right Time

Monitor market trends and consider locking your rate home mortgage during periods of stability or after major Federal Reserve announcements. In volatile times, locking early can protect you from sudden increases. For a deeper look at market timing and rate movement, see the Seattle housing market forecast for 2026.

Real-World Example: Tech Professional in Redmond

A tech worker in Redmond used RSUs as part of their income to qualify for a jumbo loan on a $1.2M home. By preparing documentation early, comparing rate home mortgage offers from three local lenders, and locking in during a favorable market window, they closed in 14 days and saved over $300 monthly compared to national averages.

Final Thoughts

Securing the best rate home mortgage in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett is all about preparation and timing. Follow these steps, leverage local expertise, and stay informed about market trends. With a clear plan, you can confidently navigate the 2026 mortgage landscape and achieve your homeownership goals.

Expert Insights: Working with a Trusted Seattle Mortgage Broker

Navigating the Seattle mortgage landscape in 2026 requires more than rate shopping—it demands expert guidance. A trusted local broker brings deep knowledge of rate home mortgage options specific to Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. This expertise can make all the difference when rates fluctuate and competition intensifies.

Why Choose a Local Seattle Mortgage Broker?

A Seattle-based broker offers several advantages:

- Access to a wide range of lenders, including exclusive rate home mortgage products not always available at banks.

- Ability to compare real-time offers, ensuring clients secure the most competitive rates and terms.

- In-depth understanding of local underwriting, especially for tech professionals with RSUs or bonus income.

- Personalized strategy sessions tailored to Seattle’s dynamic market and fast-paced bidding environment.

Brokers also help clients interpret complex rate forecasts. For example, by referencing Fannie Mae’s updated mortgage rate projections, a broker can help you decide when to lock in your rate home mortgage or whether to consider an adjustable option.

Navigating Complex Borrower Scenarios

Seattle’s diverse workforce means many buyers have unique financial profiles. Whether you are self-employed, earn RSUs at Amazon or Microsoft, or are purchasing an investment property in Everett or Mill Creek, a skilled broker knows how to present your file to lenders for the best outcome. They understand local loan limits and can advise on jumbo financing for homes in Bellevue or Mill Creek, where price points often exceed conforming thresholds.

Real-World Success: Bellevue Family Case Study

Consider a Bellevue family who recently needed a jumbo rate home mortgage for their new home. With a broker’s guidance, they leveraged RSU income, navigated strict underwriting, and closed in just nine business days. This speed and expertise often give buyers a critical edge in Seattle’s competitive market.

Transparent, Education-First Guidance

A reputable broker will walk you through every step, explaining the “why” behind each recommendation. Look for brokers with a track record—750+ five-star reviews is a strong benchmark. They should offer clarity on fees, rate structures, and how rate home mortgage options impact your monthly budget.

Before selecting a broker, ask about their experience with local programs in Lynnwood or Lake Forest Park, and request examples of recent client success. A great broker will always put education and transparency first, empowering you to make informed decisions in Seattle’s ever-changing market.

As you look ahead to Seattle’s evolving mortgage landscape in 2026, having the right guidance can make all the difference. Whether you’re a first time buyer, a tech professional navigating RSU income, or a seasoned investor, I’m here to help you turn uncertainty into opportunity with clear strategy and proven expertise. Let’s talk through your goals, explore the best rate options, and create a plan that fits your unique situation—no pressure, just honest advice. Ready to move forward with confidence? Let’s have a conversation and start planning your next steps.