Rising home prices and rapidly evolving loan programs are making 2026 a pivotal year for anyone pursuing a loan first time buyer journey. For many, the process seems overwhelming, but the right knowledge can turn challenges into opportunities.

This comprehensive guide demystifies each step, from preparing your finances and understanding loan options to navigating the application and closing. By following proven strategies, first-time buyers can position themselves for success in today’s market.

Ready to unlock homeownership? Dive in and use the actionable tips ahead to make your loan first time buyer experience as smooth and rewarding as possible.

Step 1: Assessing Your Financial Readiness

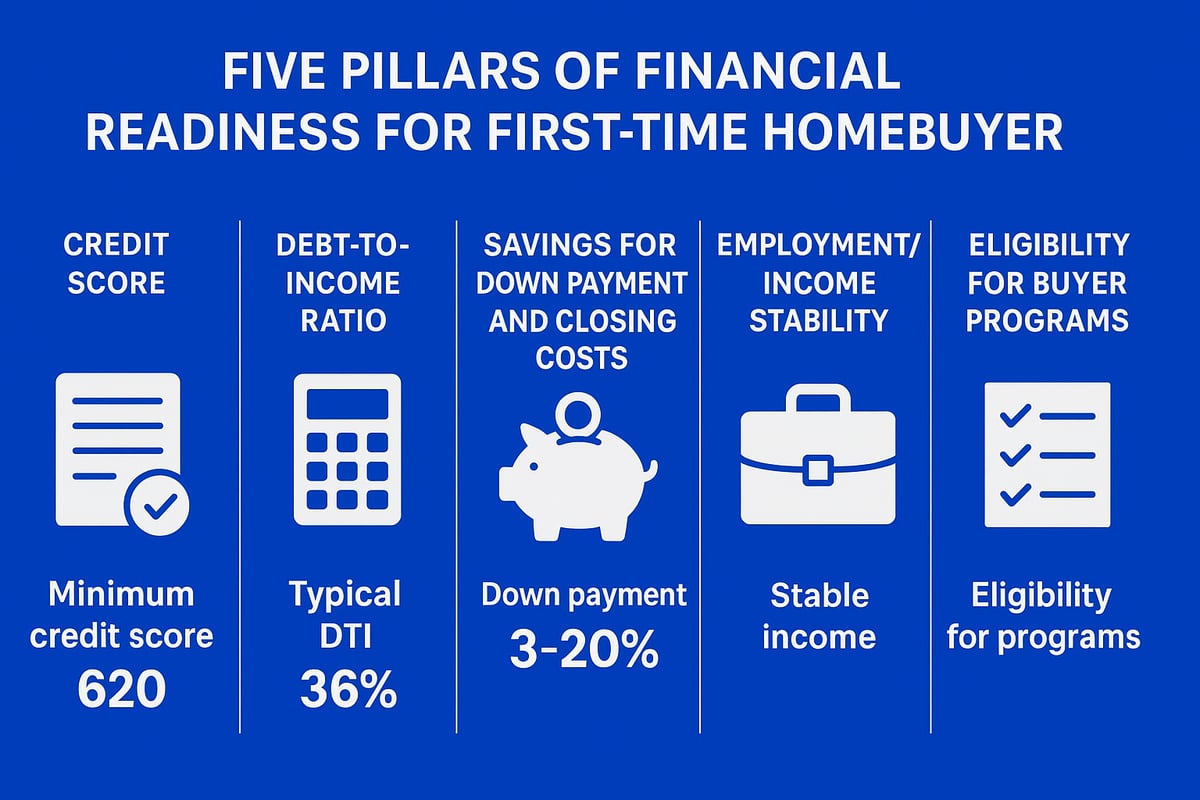

Before you begin the loan first time buyer process, it is essential to evaluate your financial health from every angle. Lenders closely review your credit, debts, savings, employment, and eligibility for special programs. By taking these steps, you can present yourself as a strong candidate and unlock the best financing opportunities.

Understanding Your Credit Score and Its Impact

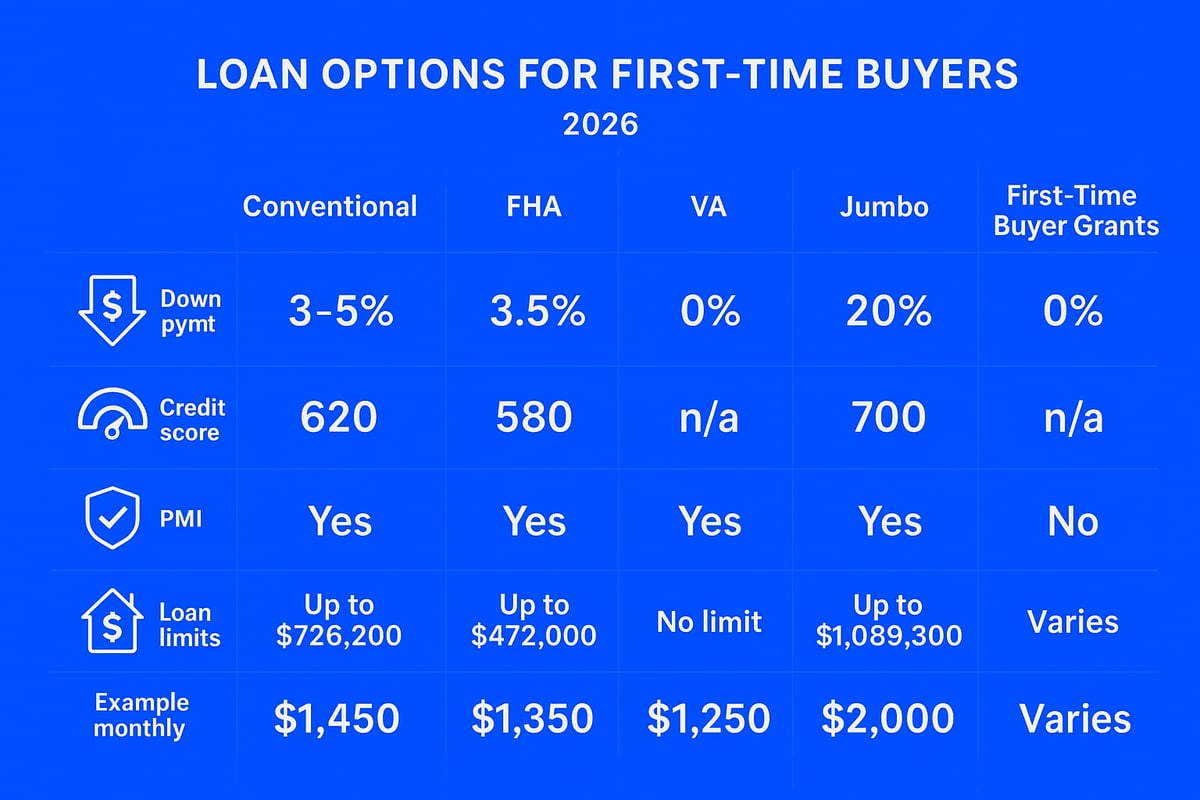

Your credit score is the foundation of the loan first time buyer journey. Lenders use your score to determine eligibility and set your interest rates. For a conventional loan, most lenders look for a minimum score of 620, while FHA loans typically accept scores as low as 580. VA loans may be flexible, but higher scores yield better rates. Jumbo loans often require 700 or higher.

Here is a quick comparison:

| Loan Type | Minimum Score | Typical Rate (2026) |

|---|---|---|

| Conventional | 620 | 6.1%–6.7% |

| FHA | 580 | 6.3%–7.0% |

| VA | 620 | 5.9%–6.5% |

| Jumbo | 700 | 6.4%–7.1% |

Check your credit early. Dispute errors, pay down debts, and avoid new credit inquiries. Keep utilization below 30% for the best results. Improving your score before applying can save you thousands over the life of your loan first time buyer experience.

Evaluating Your Debt-to-Income (DTI) Ratio

Lenders also review your debt-to-income ratio, or DTI, to see if you can comfortably handle a new mortgage. DTI measures your monthly debt payments divided by your gross monthly income. The lower your DTI, the better your loan first time buyer approval odds.

Standard DTI limits by loan type:

| Loan Type | Max DTI (%) |

|---|---|

| Conventional | 43–45 |

| FHA | 50 |

| VA | Flexible |

| Jumbo | 38–43 |

To calculate, add up all monthly debts (credit cards, car loans, student loans) and divide by your gross income. For example, if you earn $8,000 monthly and pay $2,800 toward debts, your DTI is 35%. Lower your DTI by paying down balances and avoiding new obligations before applying for a loan first time buyer.

Building Your Savings for Down Payment and Closing Costs

Saving for your down payment and closing costs is a crucial step in the loan first time buyer process. Conventional loans may require as little as 3% down, FHA just 3.5%, and VA loans 0% down for eligible buyers. Closing costs typically add another 2%–5% of the home price.

For a $400,000 home, here is a sample estimate:

| Requirement | Amount |

|---|---|

| Down Payment (3%) | $12,000 |

| Closing Costs (3%) | $12,000 |

| Emergency Fund | $5,000+ |

| Total Needed | $29,000+ |

Explore Down Payment Home Loans Guide for strategies and programs that can help first-time buyers meet these requirements. Always keep a reserve for emergencies after closing, so your loan first time buyer journey starts on solid ground.

Reviewing Your Employment and Income Stability

Stable employment and verifiable income are non-negotiable for any loan first time buyer application. Most lenders want to see at least two years of consistent work history in the same field. Acceptable income sources include salary, hourly wages, bonuses, commissions, restricted stock units (RSUs), and self-employment, provided you can document them.

Prepare to provide:

- Recent pay stubs (last 30 days)

- W-2s or 1099s (last two years)

- Bank statements (last two months)

- Proof of RSUs or bonuses, if applicable

Tech professionals, for example, should gather vesting schedules and statements for RSUs. The more thorough your paperwork, the smoother your loan first time buyer approval process will be.

Checking Your Eligibility for First-Time Buyer Programs

Lenders define a first-time buyer as someone who has not owned a home in the past three years. Many state and federal programs set additional criteria, such as income limits or property types, to qualify for their loan first time buyer incentives.

In the Seattle area, some programs offer down payment assistance, reduced mortgage insurance, or lower interest rates for qualifying buyers. Benefits may include:

- Grants toward your down payment

- Deferred or forgivable loans

- Reduced PMI or special rate programs

Research local and federal offerings early. By leveraging these resources, you can maximize your buying power and make your loan first time buyer experience more affordable.

Step 2: Exploring Loan Options for First-Time Buyers

Choosing the right loan first time buyer program is a crucial step toward homeownership in 2026. Understanding each loan type helps you match your financial situation to the best possible financing. Let’s break down the main options available for first-time buyers.

Conventional Loans: Pros, Cons, and Requirements

A conventional loan first time buyer option is popular due to its flexibility and competitive rates. Most require a minimum 3 percent down payment and a credit score of at least 620, though higher scores qualify you for better rates.

Pros:

- Lower PMI costs if you put 20 percent down.

- PMI drops automatically when you reach 22 percent equity.

- Available for a wide range of property types.

Cons:

- Stricter credit and DTI requirements.

- Higher down payment than government-backed loans.

For 2026, conforming loan limits are projected to rise, especially in high-cost areas. For example, a $400,000 loan at 7 percent interest may have a monthly payment of around $2,660 (principal and interest only) for a 30-year fixed term. Comparing your options ensures you pick the right loan first time buyer program for your needs.

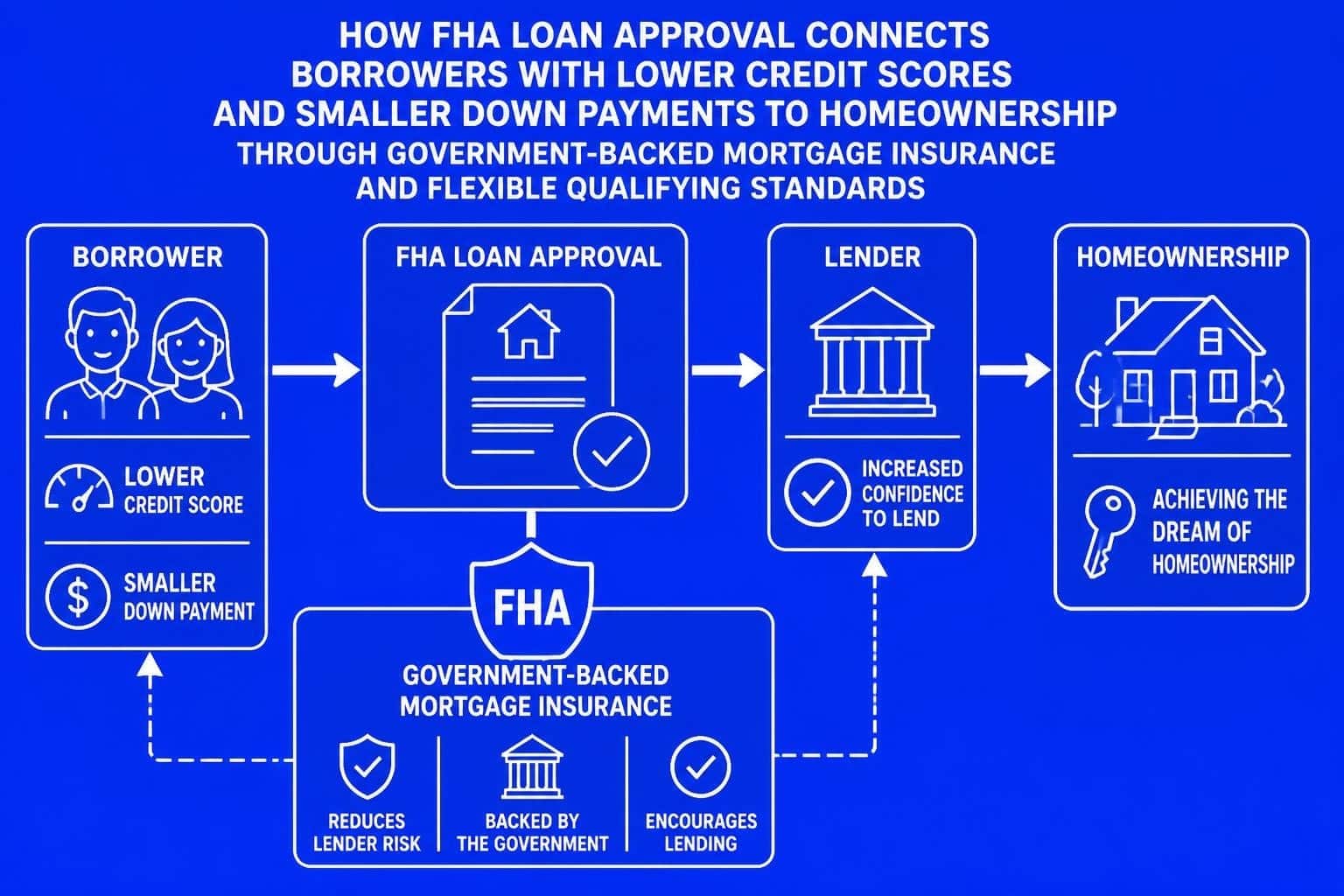

FHA Loans: Flexible Qualification for New Buyers

The FHA loan first time buyer route is attractive for those with lower credit scores or limited savings. FHA loans require only a 3.5 percent down payment and accept credit scores as low as 580.

Borrowers pay both an upfront and annual mortgage insurance premium, which increases the total cost. FHA loan limits vary by county and the property must meet specific condition standards.

For a $350,000 home, FHA monthly payments may be slightly higher than conventional due to insurance, but the lower entry barrier is a major advantage. To explore details and see if this is the right loan first time buyer option for you, review this FHA Home Loans Overview.

VA Loans: Exclusive Benefits for Veterans and Military

If you are a veteran or active-duty service member, the VA loan first time buyer program offers unmatched benefits. You can finance 100 percent of your home with no down payment and no PMI.

Eligibility:

- Service requirements for veterans, reservists, and some surviving spouses.

- Certificate of Eligibility (COE) needed.

A funding fee applies, though some buyers are exempt. For example, a $400,000 VA loan could save you over $12,000 upfront compared to a conventional loan due to the absence of PMI and down payment. Choosing a VA loan first time buyer program can maximize your purchasing power and savings.

Jumbo Loans: Financing High-Value Properties

When your desired home exceeds conforming loan limits, a jumbo loan first time buyer solution becomes necessary. In 2026, jumbo loans start above $750,000 in many markets.

Expect stricter requirements:

- Minimum credit scores of 700 or higher.

- Down payments of 10 to 20 percent.

- Significant cash reserves.

For example, buying an $850,000 home in Seattle may require $85,000 down plus six months’ reserves. Jumbo loan first time buyer programs suit those with strong finances looking for luxury or high-value properties.

First-Time Buyer Programs and Grants

First-time buyer programs can make a substantial difference for anyone seeking a loan first time buyer plan. Federal, state, and local offerings include down payment assistance, grants, and reduced mortgage insurance.

2026 brings expanded opportunities:

- Increased income limits for program qualification.

- New grant options and forgivable loans.

- Ability to combine assistance with conventional or FHA loans.

For instance, Washington State Housing Finance Commission programs provide up to 4 percent of the purchase price for down payment support. Always check current offerings in your area to find the best loan first time buyer program that fits your goals.

Step 3: Getting Pre-Approved and Shopping for Lenders

Preparing for your home purchase means understanding how to navigate the loan first time buyer process efficiently. Pre-approval and lender shopping are crucial steps that can give you a significant advantage. Let's break down the essentials for 2026 so you can maximize your buying power and make informed decisions.

The Importance of Pre-Approval in 2026’s Competitive Market

In 2026, the loan first time buyer landscape is more competitive than ever. Pre-approval is no longer optional—it is a strategic move that positions you as a serious buyer. Sellers and agents often require pre-approval letters before considering offers, especially in fast-paced markets.

The difference between pre-qualification and pre-approval is significant. Pre-qualification is a quick estimate, while pre-approval involves a thorough review of your finances and credit. You will need to provide documents such as pay stubs, W-2s, and bank statements.

A typical timeline from loan first time buyer pre-approval to closing can range from 30 to 45 days. Getting pre-approved early can help you act quickly when you find the right property.

Comparing Lenders: Rates, Fees, and Service

The loan first time buyer should compare multiple lenders to secure the best deal. Rates and fees can vary widely, even for the same borrower profile.

Key factors to compare include:

- Annual Percentage Rate (APR)

- Origination and application fees

- Closing costs

- Customer service and responsiveness

For example, banks, credit unions, and mortgage brokers may all offer different rates for the same loan first time buyer scenario. Some lenders also offer fast-track approvals, which can give you an edge in a bidding war.

Understanding Rate Locks and Market Timing

A rate lock guarantees your interest rate for a set period, protecting you from market fluctuations during the loan first time buyer process. Typical lock periods are 30, 45, or 60 days, with longer locks sometimes costing more.

In 2026, mortgage rates may be volatile due to economic shifts. Timing your rate lock is crucial. For instance, rates could move significantly over a 60-day period, impacting your monthly payment.

Discuss with your lender the best time to lock and understand any associated fees or conditions for extending the lock if your closing is delayed.

Questions to Ask Your Lender

Before committing to a lender, the loan first time buyer should ask detailed questions to avoid surprises. Key topics include:

- What is included in the loan estimate?

- Are there prepayment penalties?

- How is escrow managed for taxes and insurance?

- What are the turnaround times for approvals and document reviews?

- How will communication be handled throughout the process?

Use a checklist to keep track of lender responses and ensure you understand all terms before moving forward.

Keith Akada – Mortgage Reel: Local Expertise and Fast-Track Approvals

Working with a local expert like Keith Akada and the Mortgage Reel team can be a game-changer for a loan first time buyer. Their education-first approach ensures you understand every step, from pre-approval to closing. They offer transparent guidance, fast-track approvals in as little as nine business days, and hyper-local insights for Seattle and the Eastside.

With over 750 five-star reviews, Mortgage Reel is known for supporting tech professionals, veterans, and investors. If you want to dive deeper into home loan education, explore their Home Ownership Education Resources for valuable tools and guidance.

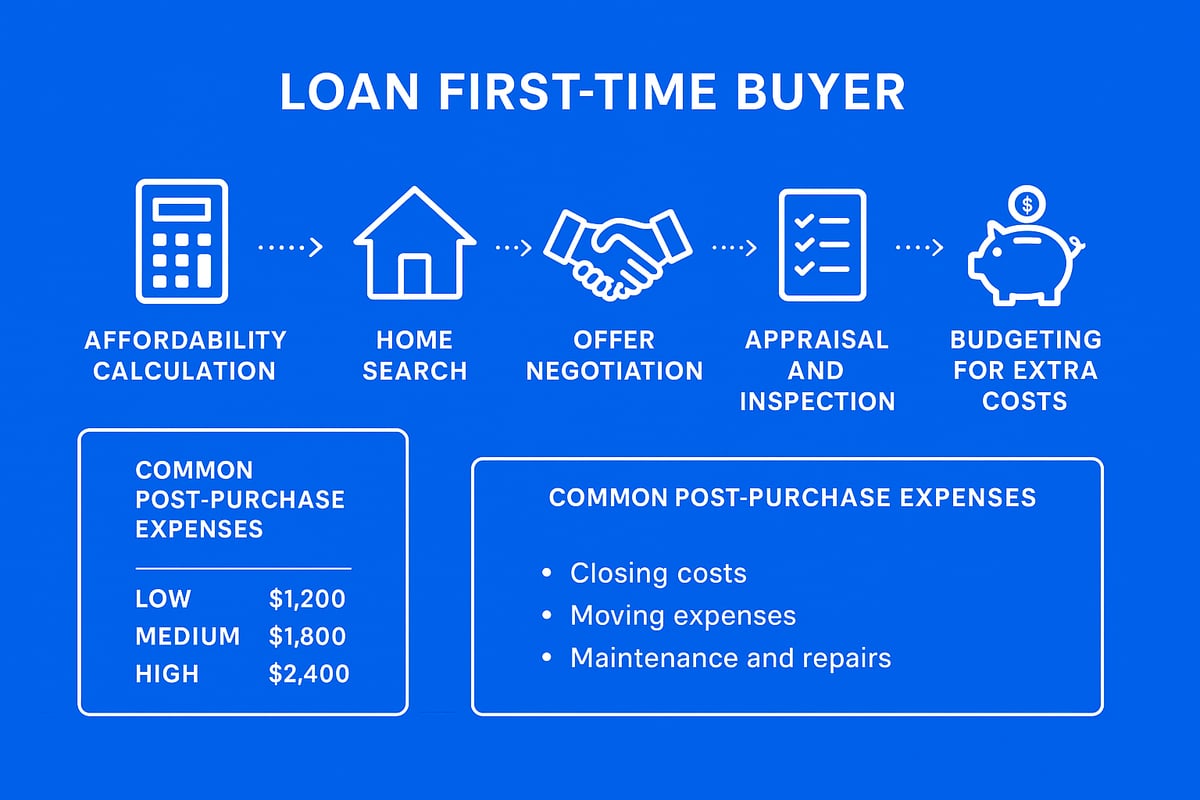

Step 4: Making a Smart Home Purchase Decision

Buying your first home is a significant milestone, and making smart decisions along the way is essential. For any loan first time buyer, taking a methodical approach at this stage can help prevent costly mistakes and set you up for lasting financial success. Let’s break down the critical steps to ensure you make a confident, informed choice.

Determining How Much Home You Can Afford

Understanding your budget is the foundation for any loan first time buyer. Start by using online affordability calculators and consulting with your lender to determine your comfortable price range. Factor in your income, debts, down payment, and estimated monthly costs.

| Home Price | Down Payment | Estimated Monthly Payment | Total Cash Needed |

|---|---|---|---|

| $400,000 | 5% ($20,000) | $2,600 | ~$30,000 |

| $500,000 | 5% ($25,000) | $3,200 | ~$37,500 |

Balance your wish list with what you can realistically afford. Remember, the right home is one that fits your lifestyle and leaves room in your budget for other goals.

Navigating the Home Search and Offer Process

The home search can feel overwhelming, especially for a loan first time buyer in a competitive market. Partner with a real estate agent who specializes in helping first-time buyers and knows your local area well.

Be prepared for market conditions in 2026, which may include limited inventory or bidding wars. Identify your must-haves and nice-to-haves, and tour homes that fit your criteria. When you find the right one, move quickly but thoughtfully to make a strong, informed offer.

Structuring Your Offer and Negotiating Terms

Crafting a compelling offer is crucial for every loan first time buyer. Work with your agent to decide on contingencies such as inspection, financing, and appraisal. These protect your interests and provide exit options if issues arise.

Earnest money shows the seller you are serious. Typically, this is 1-3% of the purchase price and is credited toward your down payment at closing. Negotiate for seller concessions, like help with closing costs, to further improve your deal.

Home Appraisal and Inspection: What to Expect

Both appraisal and inspection are essential steps for a loan first time buyer. An appraisal confirms the home's value for your lender, while an inspection uncovers potential issues with the property.

Common problems found during inspections include roof repairs, outdated electrical systems, or plumbing leaks. If the appraisal comes in low, you may need to renegotiate with the seller or bring additional funds to close. Address repair requests promptly to keep your purchase on track.

Planning for Additional Costs Beyond the Purchase Price

Many loan first time buyer candidates focus on the sales price, but ongoing costs are equally important. Prepare for property taxes, homeowners insurance, HOA fees, and routine maintenance.

- Property taxes: Vary by location, often 1-2% of the home’s value annually

- Homeowners insurance: Required by lenders, average $1,200-$1,500 per year

- HOA fees: Common in condos or planned communities

- Maintenance: Budget 1% of the home’s value per year

To help offset upfront expenses, explore grants and assistance programs such as the Homebuyer Dream Program® Suite Information, which offers down payment and closing cost support for qualified first-time buyers in 2026. This can provide valuable relief and make homeownership more attainable.

Step 5: Navigating the Loan Application and Underwriting Process

Applying for a mortgage can feel overwhelming for any loan first time buyer, but understanding each step brings confidence and clarity. This stage is where your preparation pays off, as lenders closely examine your financial profile and documentation. Knowing what to expect and how to respond can smooth your path from application through final approval.

Submitting Your Loan Application: Step-by-Step

The first step for any loan first time buyer is submitting a complete mortgage application. Most lenders now offer online portals, though in-person options remain available. You will need to provide several documents, including:

- Proof of income (pay stubs, W-2s, tax returns)

- Bank statements for all accounts

- Identification (driver’s license or passport)

- Documentation for assets and debts

Double-check your paperwork for accuracy and completeness. Common mistakes, such as missing pages or outdated statements, can cause delays. If you are applying for a special program, such as the CalHFA Dream For All Program Announcement, be sure to include any required supplemental forms. Staying organized at this stage sets the tone for a smooth process.

Understanding the Underwriting Process

Once your application is submitted, underwriting begins. For a loan first time buyer, this is the lender’s detailed review of your credit, employment, assets, and the property itself. The underwriter verifies your information and assesses risk. They look for consistency across documents and may request clarification if numbers do not match.

Conditional approval is common at this stage, meaning you are approved if you meet certain requirements. The timeline can vary based on market conditions. As you navigate this process, being aware of projected market trends, such as those in the Fannie Mae Housing Forecast for 2026, can help you anticipate possible changes in approval criteria or timing.

Responding to Conditions and Requests

During underwriting, it is typical for a loan first time buyer to receive requests for additional information. This may include updated pay stubs, explanations for recent bank deposits, or proof of resolved debts. Responding quickly is crucial. Keep digital copies of all documents handy for fast turnaround.

If you are self-employed or have unique income sources, be prepared for extra documentation. Clear communication with your lender helps prevent misunderstandings. Remember, every request brings you one step closer to final approval, so treat each response as a priority.

Managing Timeline and Communication

Managing the loan first time buyer process means keeping track of milestones from application to closing. Typical stages include:

- Application submission

- Appraisal ordered and completed

- Conditional approval

- Final underwriting review

- Clear to close

Proactive communication with your lender and real estate agent is vital. Ask for regular updates and clarify preferred contact methods. Delays can occur if documents are missing or if questions go unanswered. By staying engaged and organized, you can help avoid common setbacks and keep your closing on track.

Final Loan Approval and Preparing for Closing

Once you receive final approval, you are “clear to close.” This is a key milestone for any loan first time buyer. Review your closing disclosure carefully, confirming that all amounts and fees match your expectations. If anything looks incorrect, address it with your lender immediately.

At the closing table, you will sign the final loan documents and pay any remaining costs. Bring valid ID and make sure funds for closing are ready. After signing, you will receive your keys and become a homeowner. Taking these final steps with care ensures a successful start to your new chapter.

Step 6: Closing on Your Home and Preparing for Homeownership

Reaching the closing stage is a major milestone for any loan first time buyer. This final step turns your dream into reality, but it also brings important paperwork, financial considerations, and planning for your new responsibilities. Here is what you need to know to finish strong and set yourself up for long-term success as a homeowner.

Understanding Closing Costs and Final Paperwork

As a loan first time buyer, you will encounter closing costs averaging 2 to 5 percent of your home’s purchase price. These cover fees for your lender, appraisal, title insurance, and taxes. For a $400,000 home, expect $8,000 to $20,000 in total closing costs.

You will receive a Closing Disclosure at least three days before closing. Review every detail, from loan amount to escrow payments. Bring valid ID and certified funds for your closing appointment. If you are in South Carolina, review SC Housing Mortgage Programs 2025 – 2026 for potential assistance to reduce these costs.

What Happens on Closing Day

On closing day, you will meet with your escrow officer or attorney to sign final documents. This includes your mortgage agreement, deed of trust, and tax forms. After all signatures are complete, your lender will fund the loan and the title will transfer.

You will usually receive your keys the same day or within 24 hours. For most loan first time buyer clients, the timeline from signing to move-in is smooth, provided all funds and paperwork are in order.

Setting Up Your Mortgage Payments and Escrow

After closing, set up your mortgage payments right away. Most lenders offer online portals for automatic payments, which helps loan first time buyer households avoid late fees. Your escrow account will manage property taxes and homeowners insurance, ensuring these bills are paid on time.

Your first payment is typically due the month after closing. Check your payment schedule and set reminders. Confirm that your escrow account is correctly funded to prevent any future issues.

Tips for New Homeowners: Financial and Maintenance Planning

As a loan first time buyer, budgeting for ongoing costs is essential. Create a home maintenance schedule to track seasonal tasks like HVAC servicing, gutter cleaning, and appliance checks. Build a reserve fund for unexpected repairs.

Typical annual maintenance costs range from 1 to 2 percent of your home’s value. For a $400,000 home, plan for $4,000 to $8,000 per year. Use local assistance programs where available to help with repairs or upgrades.

Protecting Your Investment: Insurance and Warranties

Lenders require you to maintain homeowners insurance to protect your property. Policies cover fire, theft, and liability. In 2026, average premiums range from $1,200 to $2,000 per year, depending on location and coverage.

Consider optional home warranties for major systems and appliances. This can be a smart move for a loan first time buyer seeking peace of mind during the first year of ownership. Review policy details to ensure adequate protection.

Leveraging Home Equity and Future Planning

Building equity is one of the key benefits of homeownership. Each mortgage payment increases your stake in the property. Over time, appreciation can add to your equity, providing future financial flexibility.

A loan first time buyer may eventually use equity for renovations, education, or refinancing to secure a better rate. Stay informed about market trends and consult with your lender to explore options as your needs evolve.

You’ve just explored every essential step to confidently navigate your first home loan in 2026, from assessing your finances to understanding Seattle’s unique market and closing with peace of mind. As you prepare for this exciting milestone, remember you don’t have to figure it all out alone—I’m here to offer guidance shaped by years of local expertise and a true focus on your goals. If you’re ready to talk through your options or want personalized answers to your questions, Let’s have a conversation.