Unlocking the path to homeownership in Seattle starts with understanding the va loan loan, a powerful benefit for veterans, active-duty service members, and their families. In 2026, Seattle’s fast-moving real estate market makes using your VA benefits more valuable than ever.

This guide is tailored for those in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. I will walk you through eligibility, required documentation, the application process, and unique local tips, plus highlight the latest 2026 updates.

Discover how the va loan loan can help you compete, save money, and secure your dream home. Real-life success stories and expert advice will provide a clear, step-by-step roadmap to make your home purchase smooth and successful.

Understanding VA Loans in Seattle: Key Benefits & Basics

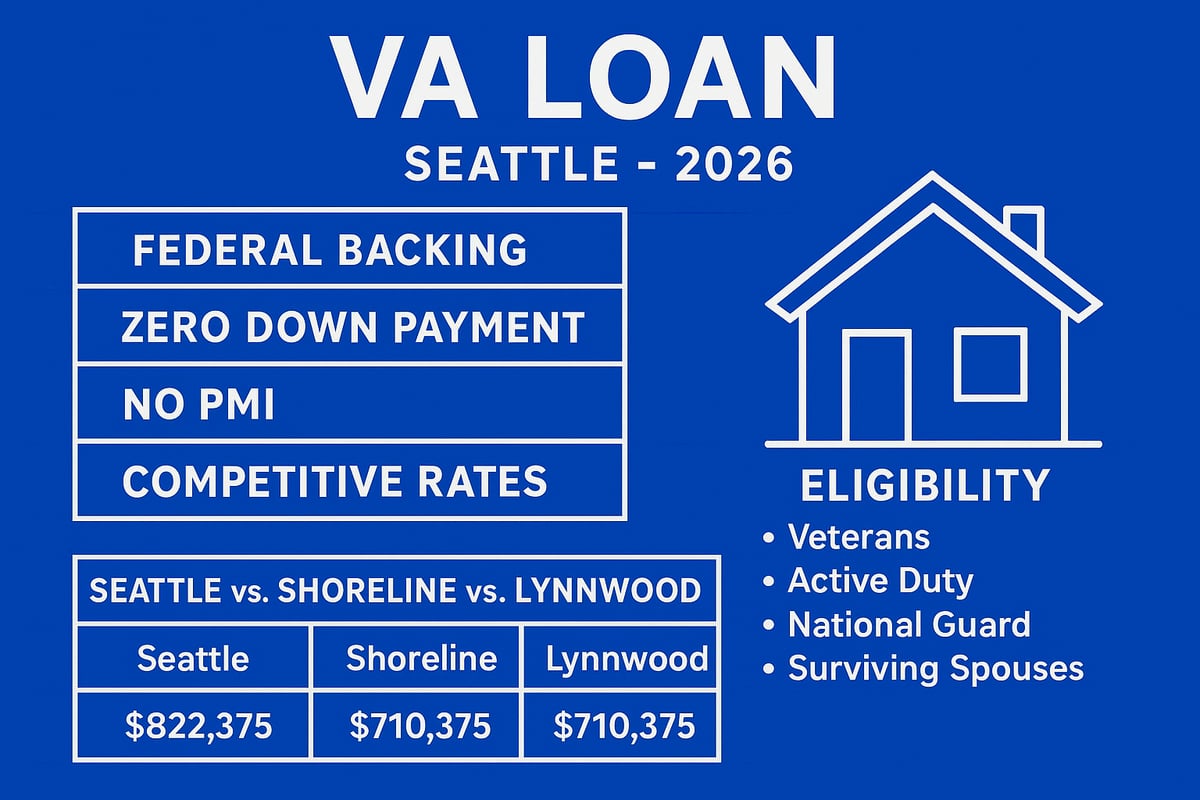

Navigating the Seattle-area housing market in 2026 can feel overwhelming, especially with prices climbing in neighborhoods like Shoreline, Lynnwood, and Mill Creek. For veterans and service members, the va loan loan program offers a powerful solution. Backed by the U.S. Department of Veterans Affairs, a va loan loan is a unique mortgage option designed specifically for those who have served, providing access to homeownership with terms that are hard to match in today's competitive market.

What Is a VA Loan Loan?

A va loan loan is a mortgage product made possible by the federal government to honor military service. The VA guarantees a portion of each loan, making it less risky for lenders to offer favorable terms. This means qualified buyers in areas like Everett or Lake Forest Park can secure a home with minimal upfront costs and flexible financial guidelines.

Primary Benefits of VA Loan Loans

Choosing a va loan loan gives Seattle-area homebuyers several significant advantages:

- Zero Down Payment: Qualified borrowers can purchase a home without saving for a traditional down payment, freeing up cash for moving expenses or home improvements.

- No Private Mortgage Insurance (PMI): Unlike FHA or conventional loans, a va loan loan does not require PMI, even with less than 20 percent down.

- Competitive Interest Rates: VA loans typically offer lower rates compared to other mortgage products, reducing monthly payments.

- Flexible Credit Requirements: The VA encourages lenders to consider the whole financial picture, making it easier for buyers with unique income situations.

- Capped Closing Costs: The VA limits the fees lenders can charge, further reducing upfront expenses.

- Reusable Benefit: Eligible buyers can use their va loan loan benefit multiple times throughout their lives.

For a deeper look at these advantages and how they apply locally, review the VA loan benefits for Seattle residents.

The Seattle Market: Why VA Loan Loans Matter in 2026

Seattle's real estate market has seen steady growth, with median home prices surpassing $900,000 in some neighborhoods. The same trend is visible in Shoreline, Lynnwood, and Mill Creek, making low-down-payment options even more valuable. VA loan loan limits in 2026 are expected to be especially high in King and Snohomish counties, allowing veterans to compete for homes in desirable areas without large down payments.

2026 VA Loan Loan Limits Example Table

| County | 2026 Loan Limit | Median Home Price |

|---|---|---|

| King | $1,089,300 | $950,000 |

| Snohomish | $977,500 | $850,000 |

| Pierce | $977,500 | $675,000 |

Note: Limits let buyers use a va loan loan for more expensive homes in high-cost areas.

Who Is Eligible for a VA Loan Loan?

Eligibility is open to a wide range of military-connected individuals:

- Veterans with qualifying service

- Active-duty service members

- National Guard and Reserve members (with sufficient service)

- Surviving spouses of eligible veterans

Even if you served in the Public Health Service or are a National Guard member in Mill Creek with six years of service, you may qualify for a va loan loan. Always check service requirements and obtain your Certificate of Eligibility (COE) early.

VA Loan Loan vs. FHA and Conventional Loans

How does a va loan loan compare to other mortgage options for Seattle buyers? Consider the following:

| Feature | VA Loan Loan | FHA Loan | Conventional Loan |

|---|---|---|---|

| Down Payment | 0% | 3.5%+ | 3%-20%+ |

| PMI Required | No | Yes | Yes, <20% down |

| Credit Score Guidelines | Flexible | 580+ | 620+ |

| Loan Limits (2026, King) | $1,089,300 | $977,500 | $1,089,300 |

| Funding Fee | Yes, sometimes | Upfront MIP | No |

A va loan loan stands out for making homeownership accessible, especially in high-priced markets like Seattle.

Common Misconceptions and a Local Success Story

Some believe a va loan loan is harder to get or takes longer to close. In reality, with the right lender, VA loans in Seattle close as quickly as other mortgages. For example, a veteran in Everett recently used a va loan loan to purchase a $900,000 home with no down payment and no PMI, beating out other buyers with conventional financing.

Understanding these basics empowers you to make informed choices and take full advantage of your va loan loan benefit in the dynamic Seattle market.

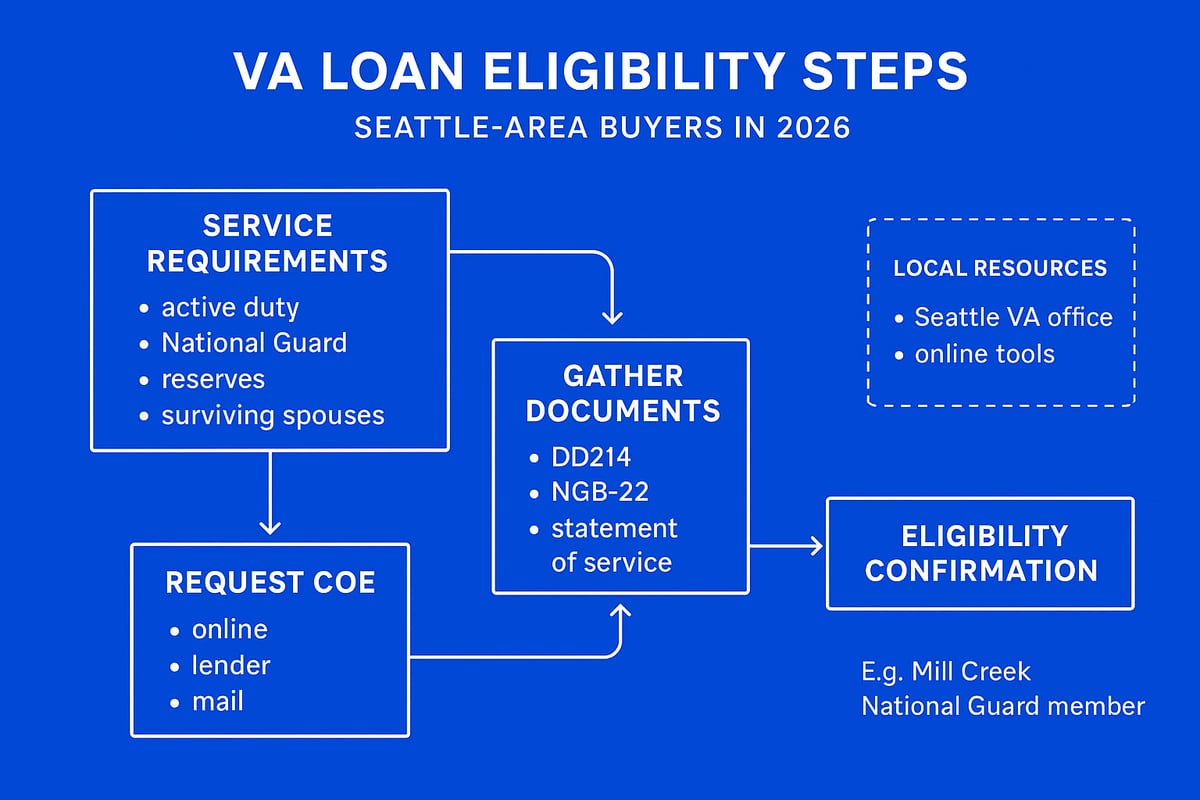

Step 1: Determining VA Loan Eligibility in 2026

Securing a va loan loan in Seattle starts with understanding if you qualify. The eligibility process is clear and structured, designed to honor the service of veterans, active-duty personnel, National Guard members, reservists, and certain surviving spouses throughout King, Snohomish, and nearby counties.

Seattle's competitive housing market makes it vital for buyers to confirm their va loan loan eligibility early. The Department of Veterans Affairs sets specific service requirements, which include:

- At least 90 consecutive days of active service during wartime, or

- 181 days of active service during peacetime, or

- More than six years in the National Guard or Reserves

For those discharged, the character of discharge matters. Most honorably and some generally discharged veterans will qualify. If your discharge status is “other than honorable,” options exist to apply for a discharge upgrade or a character of service review, ensuring you do not miss out on va loan loan benefits.

Special eligibility rules apply for surviving spouses who have not remarried, and for unique groups like Public Health Service officers. These exceptions expand access to the va loan loan program for families who have also served in critical ways. Always check the current VA Loan Eligibility Requirements to confirm your status, as rules may evolve for 2026.

One essential step is obtaining your Certificate of Eligibility (COE). The COE officially verifies your eligibility for a va loan loan and is required by all lenders before they process your application. You can request your COE online through the VA, ask your lender for assistance, or submit a paper application. Documents needed vary by service type:

- Veterans: DD214 (discharge papers)

- Active duty: Statement of service signed by your commander

- National Guard/Reserve: NGB-22 or NGB-23 forms

In Seattle and Snohomish County, a significant percentage of veterans meet the criteria for a va loan loan. However, common pitfalls include missing paperwork, name changes, or incomplete service records. If you encounter issues, local VA offices in Seattle and Lynnwood can help resolve them quickly, or you can use online resources to verify your service.

Consider this real-world example: A National Guard member from Mill Creek, after six years of service and part-time activation, successfully qualifies for a va loan loan by providing complete service documentation and working with a local lender familiar with regional requirements.

To summarize, the path to va loan loan eligibility in Seattle involves:

- Meeting the minimum service requirements for your era and category

- Ensuring your discharge or service status meets VA guidelines

- Gathering and submitting the correct documentation for your COE

- Addressing any unique eligibility scenarios or paperwork issues early

- Using trusted resources to verify and troubleshoot your status

By starting with these steps, you set yourself up for a smooth homebuying process. For additional support, regional VA offices and online eligibility tools can provide tailored guidance to Seattle-area buyers.

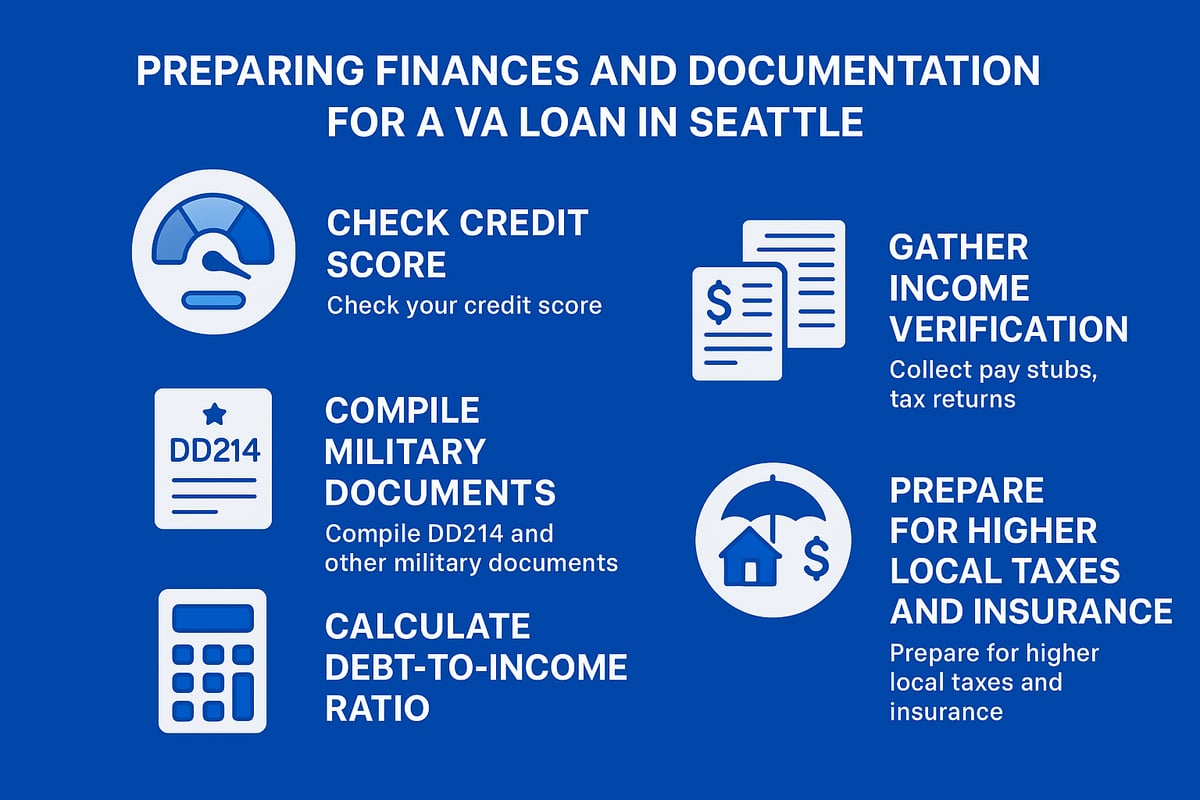

Step 2: Preparing Your Finances and Documentation

Navigating the Seattle housing market with a va loan loan requires careful financial preparation. Whether you are looking in Shoreline, Lynnwood, or Mill Creek, getting your finances in order is the foundation for a smooth and successful home purchase. Let’s break down the key steps every Seattle-area VA buyer should take before applying.

Understanding Credit, Income, and DTI Requirements

The first step in preparing for a va loan loan is understanding your credit profile and income documentation. VA loans are flexible, but most Seattle lenders look for a minimum credit score around 620. Some local lenders may accept lower scores, but a higher score can unlock better rates.

Income stability is crucial. You will need to provide recent pay stubs, W-2s, and tax returns, especially if you have variable income from tech bonuses or restricted stock units (RSUs) in Redmond. Lenders also examine your debt-to-income (DTI) ratio, which should generally stay below 41 percent for a va loan loan, though some lenders in Everett and Lake Forest Park may allow higher ratios with strong compensating factors.

Document Checklist for Seattle-Area VA Loan Loan Applicants

Gathering the right documents early prevents delays. Here is a checklist for Seattle-area buyers using a va loan loan:

- Military discharge papers (DD214 for veterans, Statement of Service for active duty)

- Proof of income (recent pay stubs, W-2s, two years’ tax returns)

- Bank statements and asset documentation

- Government-issued photo ID

- Evidence of additional income (bonuses, RSUs, gig work)

- Documentation for co-borrowers, if applicable

For first-time buyers, exploring First-time home buyer programs can provide extra guidance and resources to help you prepare the required paperwork for your va loan loan application.

Special Considerations: Variable Income, Self-Employment, and Co-Borrowers

Many Seattle veterans work in industries with fluctuating income. If you earn bonuses, commissions, or stock-based compensation, provide consistent documentation covering at least two years. Self-employed or gig economy workers in Kirkland or Bellevue must submit tax returns, profit and loss statements, and sometimes business bank statements.

Co-borrowers, such as spouses, can strengthen your va loan loan application if their income is steady and well-documented. This is especially helpful in high-cost areas like Lynnwood or Shoreline, where combining incomes can improve your purchasing power.

Seattle-Specific Tips: Taxes, Insurance, and Real-Life Example

Seattle-area homes come with higher property taxes and insurance costs compared to other regions. Plan for these expenses in your budget, as they affect your overall loan qualification and monthly payment.

For example, a Lynnwood veteran working part time recently qualified for a va loan loan by combining their income with their spouse’s full-time salary. Preparing all documents in advance and accounting for local taxes helped ensure a seamless approval process.

Thorough preparation is the key to success in Seattle’s fast-paced market. By organizing your finances and documentation, you will be ready to move quickly when the right home appears.

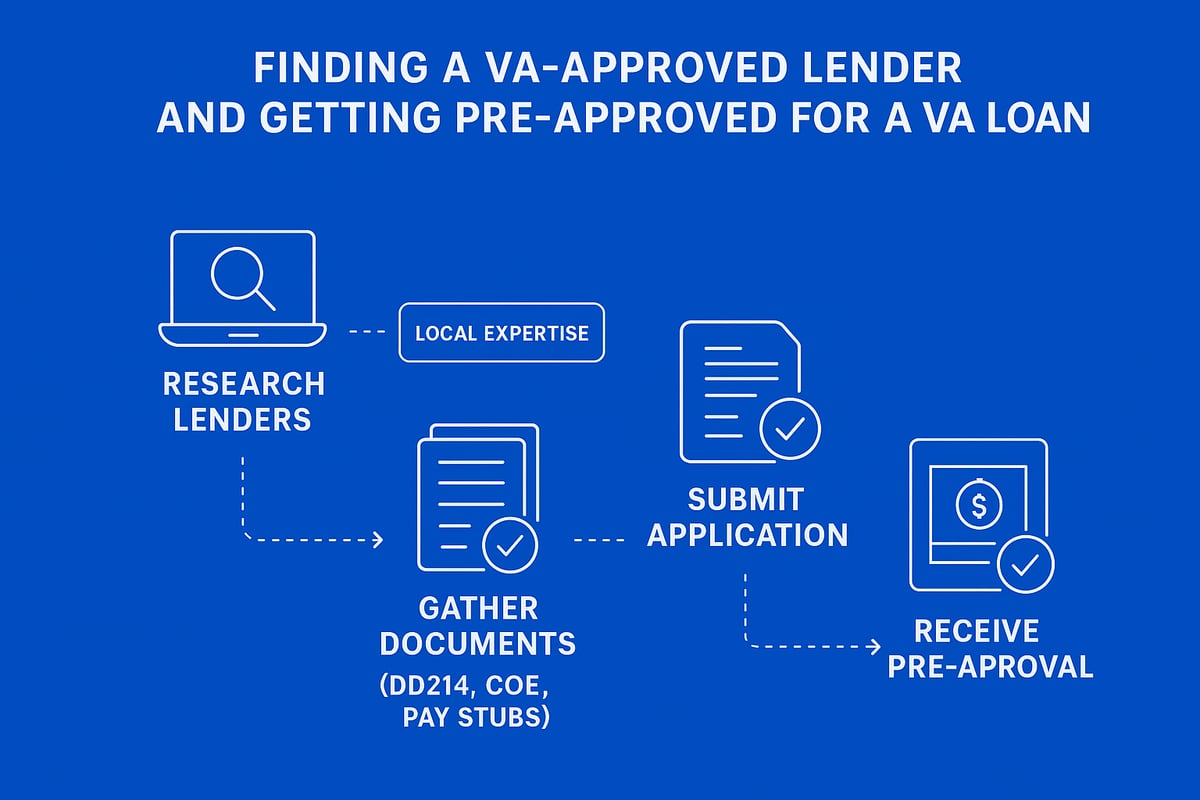

Step 3: Finding a VA-Approved Lender and Getting Pre-Approved

Navigating the Seattle housing market in 2026 means making smart, strategic decisions at every stage, especially when it comes to your va loan loan. The right lender and a solid pre-approval can make all the difference for veterans and service members in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

Selecting a VA-Approved Lender in Seattle

Start your va loan loan journey by choosing a VA-approved lender with a strong track record in Seattle and surrounding cities. Local lenders often understand the nuances of the Pacific Northwest market better than national banks. They can advise on unique Seattle home values and provide tailored guidance for buyers in Everett, Shoreline, or Mill Creek.

When evaluating lenders, consider:

- Experience with VA loans in King and Snohomish counties

- Responsiveness and communication style

- Familiarity with local property types, such as condos or multi-unit homes

A lender who knows the Seattle market can help you avoid common pitfalls and streamline your va loan loan process.

The Pre-Approval Process and Its Competitive Edge

Pre-approval is a crucial step that signals to sellers you are a serious, qualified buyer. For a va loan loan, pre-approval involves submitting essential documents like your Certificate of Eligibility (COE), recent pay stubs, tax returns, and military discharge papers (such as the DD214). Your lender will review your credit, income, and assets to determine how much you can borrow.

The Seattle area is known for multiple-offer situations. A pre-approval letter gives you a distinct edge, whether you are shopping in Lynnwood, Lake Forest Park, or the heart of Seattle itself. This preparation can help you move quickly when the right property comes on the market.

Comparing Lender Rates, Fees, and Service

Not all VA-approved lenders offer the same rates, fees, or service levels. It is wise to compare at least three lenders before finalizing your va loan loan application. Pay close attention to interest rates, origination charges, and whether the lender offers dedicated VA loan expertise.

Local lenders may provide more personalized service and faster turnaround times, which are vital in Seattle's fast-paced market. For a deeper understanding of why local expertise often beats national banks, see this guide on Comparing local lenders vs. big banks.

Making Your Offer Stand Out

Once you have your va loan loan pre-approval, use it to strengthen your purchase offer. Sellers in competitive Seattle neighborhoods look favorably on buyers with solid financing in place. An Everett veteran, for example, recently secured a home after their pre-approval letter tipped the scales in a multiple-offer scenario.

To maximize your advantage, ask your lender:

- How quickly can we close with a VA loan loan in this area?

- What is your experience with VA appraisals in Seattle?

- Are there any fees unique to King or Snohomish counties I should know about?

A strong pre-approval, paired with a trusted local lender, puts you in the best position to succeed in Seattle's 2026 housing market.

Step 4: Shopping for a Home and Making a VA-Backed Offer

Shopping for a home with a va loan loan in Seattle means understanding the specific property requirements set by the VA. Homes must meet minimum standards for safety, soundness, and sanitation. The VA appraisal process ensures the property is move-in ready, not just in good condition, but also free from major hazards. This protects buyers in Seattle, Shoreline, and Lynnwood from costly repairs after closing.

Seattle’s real estate market moves quickly, so buyers using a va loan loan need to stay agile. Homes in Mill Creek and Everett often receive multiple offers within days. To compete with cash and conventional buyers, get pre-approved early and have your documentation ready. Flexibility can also help—being open to seller timelines or minor repairs may make your offer more attractive.

Understanding va loan loan limits is crucial, especially in high-cost areas like Kirkland or Lake Forest Park. In 2026, King County’s limits may allow for larger purchases without a down payment. For homes above these limits, jumbo va loan loan options are available. For example, a Kirkland buyer used a va loan loan to purchase a townhome priced above the county limit, relying on 2026 VA Loan Limits in King County to plan their strategy.

Working with a real estate agent who understands va loan loan requirements is vital in the Seattle area. These agents can guide you on making your offer stand out—using earnest money, considering inspection waivers, or offering flexibility on closing dates. If a VA appraisal comes in below the purchase price, your agent can help renegotiate or find solutions, ensuring you do not lose your dream home.

Step 5: Navigating the VA Loan Underwriting and Closing Process

Securing your dream home in Seattle, Shoreline, or Lynnwood with a va loan loan means successfully navigating the final stages of the mortgage process. Underwriting and closing are where your preparation pays off. Understanding each step ensures you avoid surprises and move confidently toward homeownership.

The VA Appraisal and Underwriting Process

The va loan loan journey enters a critical phase with the VA appraisal. Unlike a standard appraisal, the VA review ensures the property meets minimum property requirements and is safe, sound, and sanitary. This protects both you and the lender.

Once the appraisal is complete, underwriting begins. Here, your lender reviews all documentation: credit, income, assets, and your Certificate of Eligibility. In Seattle and surrounding cities like Everett and Mill Creek, lenders may also review local factors such as property taxes and insurance costs to ensure you can comfortably afford payments.

Expect the underwriter to request clarification or extra documents if needed. This step is detailed but essential for final approval.

Funding Fee and Closing Costs

All va loan loan borrowers pay a one-time VA funding fee, unless exempt as a disabled veteran. For 2026, the fee varies based on your down payment and whether it’s your first or subsequent use.

| Borrower Type | Down Payment | Funding Fee (2026) |

|---|---|---|

| First-time use | None | 2.15% |

| First-time use | 5%+ | 1.5% |

| Subsequent use | None | 3.3% |

Some buyers in Lake Forest Park and Kirkland are exempt, saving thousands.

Closing costs for a va loan loan are limited. Allowable fees include:

- Appraisal and credit report

- Title insurance

- Recording fees

Non-allowable fees, like certain lender charges, cannot be passed to you, saving more at closing.

Timeline and What to Expect at Closing

In King and Snohomish counties, the average va loan loan closes in 30 to 45 days after offer acceptance. Pre-approval and quick document submission help keep your purchase on track, even in fast-moving Seattle markets.

On closing day, you’ll review and sign final documents. The lender funds the va loan loan, and you receive the keys to your new home. Bring identification and review your closing disclosure carefully.

A Lynnwood buyer recently saved $15,000 in closing costs and funding fees, thanks to careful planning and VA exemptions.

Troubleshooting and Local Example

Sometimes, va loan loan closings face delays, often due to missing documents or appraisal issues. Stay in regular contact with your lender and respond quickly to requests. If you hit a snag, Seattle-area resources such as home ownership education for veterans offer support and guidance.

In Everett, a recent buyer resolved a last-minute appraisal concern by providing updated documentation, allowing their va loan loan to close on time. Proactive communication and local expertise make all the difference.

VA Loan FAQs for Seattle, Shoreline, and Surrounding Areas

Navigating the va loan loan process in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett can raise many questions. Below, I answer the most common concerns I hear from local buyers.

Can I use a va loan loan to buy a condo or multi-family property in Seattle?

Yes, you can use a va loan loan for condos if the project is VA-approved. Multi-unit properties (up to four units) are also eligible, provided you occupy one unit as your primary residence. Always verify condo approval with your lender.

What are the current va loan loan limits for King and Snohomish counties in 2026?

For 2026, loan limits reflect the area's rising home values. In high-cost areas like Seattle, King, and Snohomish counties, limits are higher than the national average. For the latest specifics, see this VA Loan Limits for 2026 resource.

How quickly can I close with a va loan loan in a competitive Seattle market?

With a strong lender and organized paperwork, closing can happen in as little as 21–30 days. Local experience matters—buyers in Everett and Lynnwood often close as fast as those using conventional loans.

Are va loan loans assumable if I sell my home in Everett or Lynnwood?

Yes, a qualified buyer can assume your va loan loan, often keeping the original low rate. This makes your home more attractive to buyers, especially as rates change.

Can I have more than one va loan loan at a time in Washington State?

It is possible to have more than one va loan loan if you have remaining entitlement and meet occupancy requirements. This is common for those relocating within the Puget Sound region.

How does the VA funding fee work, and who is exempt in 2026?

The VA funding fee helps cover the program cost. In 2026, disabled veterans and some surviving spouses are exempt. Others pay a one-time fee (often financed into the loan), which varies based on down payment and use.

Tips for tech professionals using RSUs or stock income to qualify for a va loan loan?

Seattle-area lenders familiar with tech income can help document RSUs and bonuses. Consistent vesting and a two-year history support your application, especially in Redmond and Kirkland.

Where can I get help if I have trouble making payments on my va loan loan?

Reach out to your lender or the regional VA office immediately. They can offer payment plans, forbearance, or connect you with local housing counselors in Seattle, Shoreline, and beyond.

Resources for VA Loan Homebuyers in Greater Seattle

Navigating the va loan loan process in Seattle, Shoreline, and nearby cities is easier with the right support. Whether you are just starting or ready to close, these resources will help you at every stage.

Essential VA Loan Loan Resources

- Request your Certificate of Eligibility (COE): Start your va loan loan journey online at VA.gov or ask your lender for help.

- Check eligibility and calculate loan amounts: Use the VA loan calculators on official sites to understand your options in Seattle, Lynnwood, and Mill Creek.

- Find VA-approved lenders and real estate agents: Look for professionals with experience in Shoreline, Lake Forest Park, and Everett to ensure a smooth transaction.

- Stay current on 2026 updates: Watch the VA Loan Limits are Changing…Again (2026 Update) video for a detailed explanation of new loan limits and their impact on your buying power.

- Veteran support organizations: Connect with local and national groups for homebuyer education, counseling, and financial advice.

- Recommended reading: Explore guides from VA.gov, Military OneSource, and the Consumer Financial Protection Bureau for trusted information.

- Education classes and workshops: Sign up for Seattle-area homebuyer workshops tailored for veterans and active-duty personnel.

- Regional VA offices and housing counselors: Contact local offices for one-on-one support or legal guidance during your va loan loan process.

An Everett veteran recently joined a VA homebuyer workshop, gaining confidence and practical knowledge to secure a va loan loan in this competitive market. These resources ensure you have the support, tools, and up-to-date information to achieve your homeownership goals in Greater Seattle.

As we’ve explored together, navigating the VA loan process in Seattle for 2026 involves more than just paperwork—it’s about understanding your options, maximizing your benefits, and making informed decisions every step of the way. Whether you’re a first time homebuyer or a seasoned investor, having a trusted local expert can make all the difference. If you’d like to discuss your unique situation, clarify next steps, or simply get your questions answered in detail, I invite you to Let’s have a conversation.