For veterans and active-duty service members in the Greater Seattle area, va loans represent one of the most powerful home financing tools available in 2026. These government-backed mortgages offer unmatched benefits including zero down payment requirements, no private mortgage insurance, and competitive interest rates that can save eligible borrowers tens of thousands of dollars over the life of their loan. Whether you're stationed at Joint Base Lewis-McChord, working in Seattle's thriving tech sector after your service, or settling in neighborhoods from Shoreline to Everett, understanding how va loans work is essential for maximizing your hard-earned military benefit.

What Makes VA Loans Different from Conventional Mortgages

VA loans stand apart from traditional financing options through several distinctive advantages that directly benefit eligible service members. The Department of Veterans Affairs doesn't issue loans directly but guarantees a portion of each loan, which allows approved lenders to offer significantly more favorable terms than conventional products.

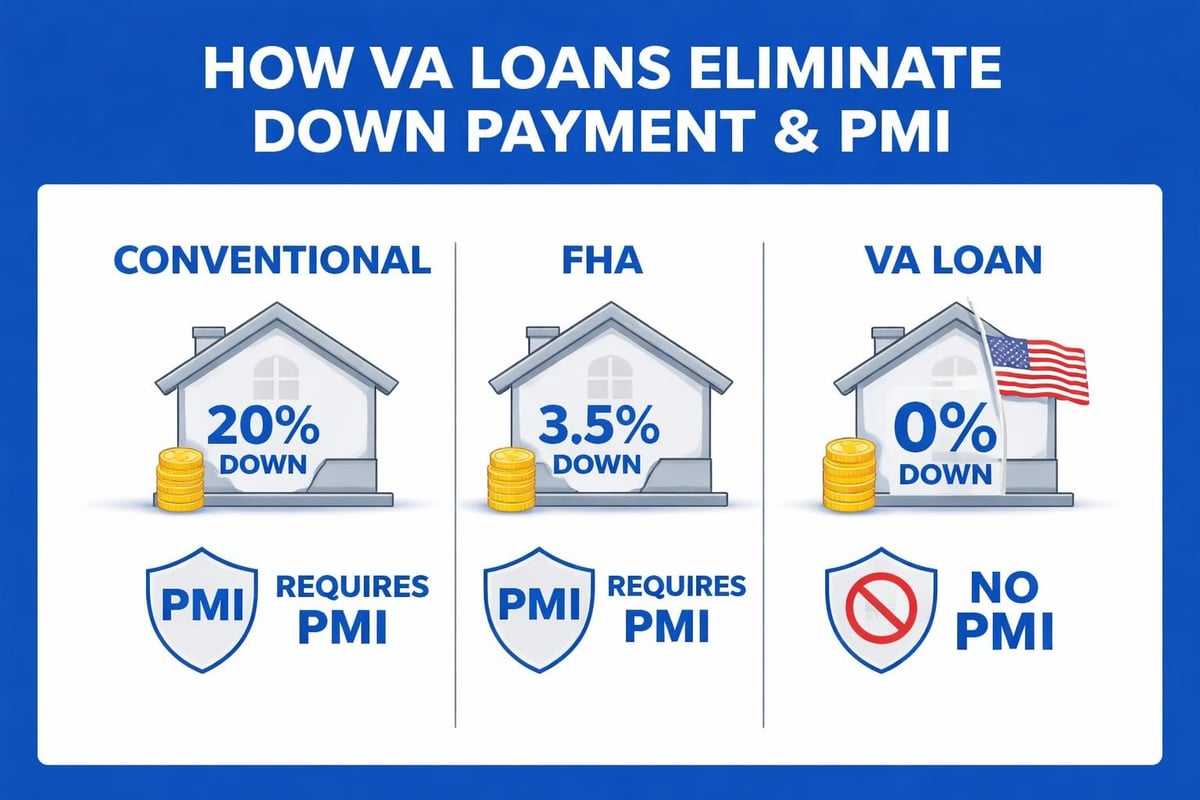

The most notable difference is the zero down payment requirement. While conventional loans typically require 3-20% down and FHA loans require 3.5%, qualified veterans can finance 100% of a home's purchase price in most cases. For a median-priced home in Seattle at approximately $825,000 in 2026, this eliminates the need for a $165,000 down payment that would be required with a conventional 20% down loan.

Key Benefits That Set VA Loans Apart

- No private mortgage insurance (PMI) regardless of down payment amount

- Competitive interest rates typically 0.25-0.50% lower than conventional loans

- Flexible credit requirements with most lenders approving scores from 580-620

- Limited closing costs with restrictions on what veterans can be charged

- Assumable loans that can be transferred to future qualified buyers

- No prepayment penalties allowing early payoff without fees

The absence of PMI alone saves borrowers hundreds of dollars monthly. On an $800,000 loan, conventional PMI could cost $400-$667 per month until reaching 20% equity, totaling $28,800-$48,000 over six years.

VA Loan Eligibility Requirements in Seattle

Understanding eligibility requirements for VA home loans is the first step toward leveraging this benefit. The VA has established clear service requirements that determine who qualifies for this program.

Active Duty Service Members qualify after serving 90 consecutive days during wartime or 181 days during peacetime. For National Guard and Reserve members, the requirement extends to six years of service, though members activated for federal service for at least 90 days may qualify sooner.

Veterans must have been discharged under conditions other than dishonorable and meet minimum service requirements. The specific length varies based on service period, but veterans who served during the Gulf War (August 1990 to present) typically need 24 months of continuous active duty or the full period for which called to active duty.

| Borrower Type | Minimum Service Requirement | Additional Notes |

|---|---|---|

| Active Duty | 90 days (wartime) or 181 days (peacetime) | Currently serving |

| Veterans | 24 months or full tour | Honorable discharge required |

| National Guard/Reserves | 6 years | Earlier if federally activated |

| Surviving Spouses | N/A | If spouse died in service or from service-connected disability |

Surviving spouses of service members who died in the line of duty or from service-connected disabilities may also qualify. Spouses of service members missing in action or prisoners of war may be eligible as well.

To obtain your Certificate of Eligibility (COE), you'll need discharge papers (DD Form 214) for veterans, current statement of service for active duty members, or retirement points statement for Guard and Reserve members. Most lenders can obtain your COE electronically within minutes through the VA's WebLGY system.

Understanding VA Loan Limits and Entitlement

While va loans are often described as having "no limit," the reality requires understanding how entitlement works. In 2026, the VA's basic entitlement is $36,000, and the additional entitlement calculation determines how much you can borrow without a down payment.

For most of King County, including Seattle, Bellevue, Redmond, and Kirkland, the conforming loan limit in 2026 is $1,209,750. Veterans with full entitlement can purchase homes up to this amount without any down payment. For loan amounts exceeding the county limit, veterans typically need to provide a down payment equal to 25% of the amount above the limit.

How Entitlement Restoration Works

Veterans who've used their VA loan benefit previously may have remaining entitlement available. If you sold your previous VA-financed home and paid off the loan, you can restore your full entitlement and use it again. This restoration happens automatically in most cases once the loan is satisfied.

Partial entitlement becomes relevant when veterans still have an existing VA loan on another property. You can use remaining entitlement for a second VA loan, though calculations become more complex. For example, if you used $200,000 of entitlement on a home in Mill Creek and still own that property, your remaining entitlement could support another loan based on the county limit minus what's already in use.

The VA loan limits page provides current figures for every county nationwide, and these limits adjust annually based on the Federal Housing Finance Agency's conforming loan limit changes.

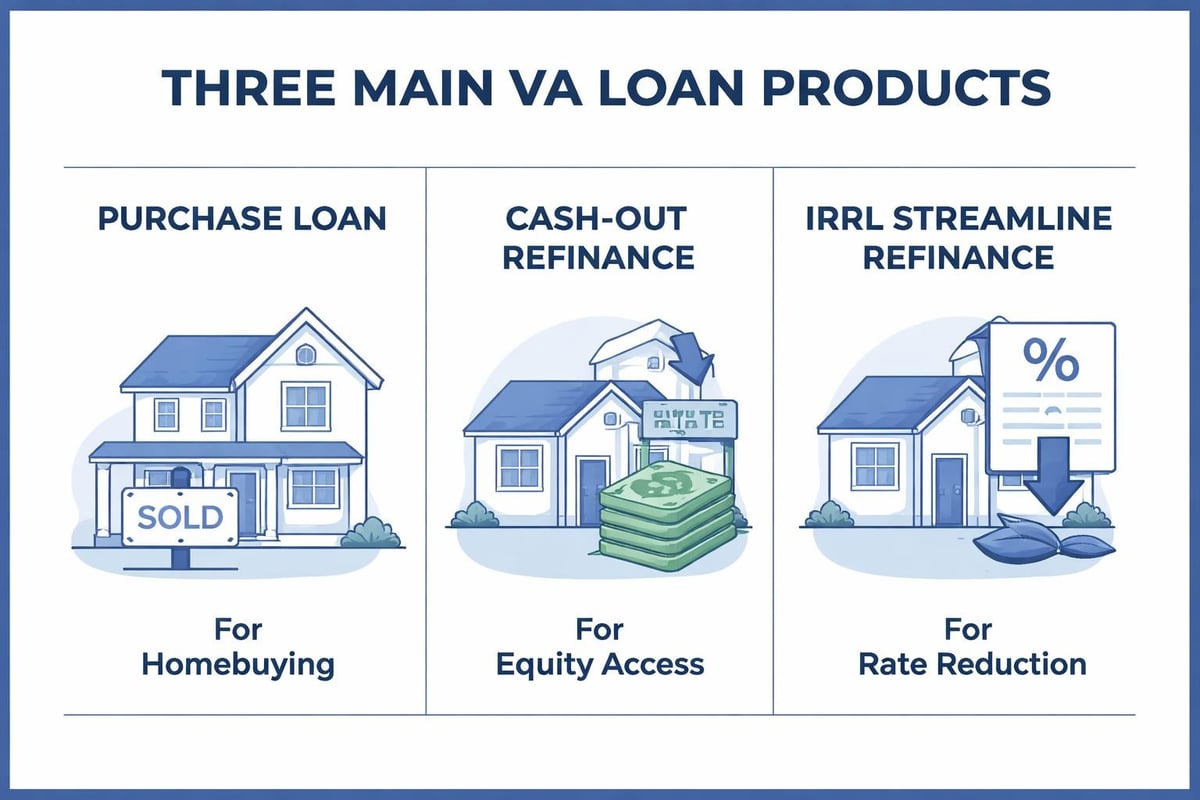

Types of VA Loan Products Available

The VA guarantee supports several different loan types designed to meet various homeownership and financial needs. Understanding which product fits your situation ensures you maximize the benefit.

VA Purchase Loans represent the most common type, allowing eligible borrowers to buy primary residences with zero down payment. These work for single-family homes, condominiums (in VA-approved projects), townhomes, and multi-unit properties up to four units, provided the veteran occupies one unit as their primary residence.

VA Cash-Out Refinance Loans enable homeowners to refinance existing mortgages-whether VA or conventional-and extract equity for any purpose. In Seattle's strong real estate market where many homes have appreciated significantly since purchase, veterans might refinance a $600,000 conventional mortgage on a home now worth $900,000, taking out up to $675,000 (75% LTV) while eliminating PMI and potentially securing a lower rate.

VA Interest Rate Reduction Refinance Loans (IRRRL), also called VA Streamline Refinances, allow veterans with existing VA loans to refinance to lower rates with minimal documentation. No appraisal is required in most cases, no income verification is needed, and closing costs can be rolled into the new loan amount.

Special Purpose VA Loan Programs

Native American Direct Loan (NADL) programs help eligible Native American veterans purchase, construct, or improve homes on Federal Trust Land. This specialized program operates differently from standard VA loans and is only available in specific situations.

Adapted Housing Grants assist veterans with permanent service-connected disabilities in purchasing or modifying homes to accommodate their disabilities. While not traditional mortgage products, these grants can be combined with VA loans to create comprehensive solutions.

VA Loan Qualification Standards and Credit Requirements

Unlike eligibility, which determines whether you can use the VA loan benefit, qualification focuses on whether lenders will approve your specific loan application. While the VA guarantees loans, individual lenders establish their own credit and income standards within VA guidelines.

Most lenders in the Seattle market require minimum credit scores between 580-620, though some lenders offer programs for scores as low as 550. Higher scores naturally secure better interest rates. A veteran with a 720 score might receive a rate 0.50-0.75% lower than one with a 600 score on the same loan amount.

Debt-to-income (DTI) ratios measure your monthly debt obligations against gross monthly income. VA guidelines allow DTI ratios up to 41% without additional scrutiny, though many lenders approve loans with DTI ratios of 50-55% when compensating factors exist, such as substantial residual income, significant cash reserves, or excellent credit history.

Residual Income: The VA's Unique Requirement

Unlike conventional loans that focus primarily on DTI ratios, va loans require adequate residual income-the money remaining after all major monthly expenses. This ensures veterans can comfortably afford their homes while maintaining quality of life.

For the Pacific region, which includes Washington state, residual income requirements vary by family size and loan amount. A family of four purchasing a home with a loan over $79,999 in Seattle needs $1,062 in monthly residual income. This requirement often allows veterans with higher debt levels to qualify when conventional guidelines would deny them, recognizing that absolute cash flow matters more than percentage-based ratios.

| Family Size | Loan ? $79,999 | Loan > $79,999 |

|---|---|---|

| 1 person | $492 | $580 |

| 2 people | $823 | $969 |

| 3 people | $990 | $1,166 |

| 4 people | $1,025 | $1,062 |

| 5+ people | $1,062 | $1,245 |

The VA Funding Fee and Closing Costs

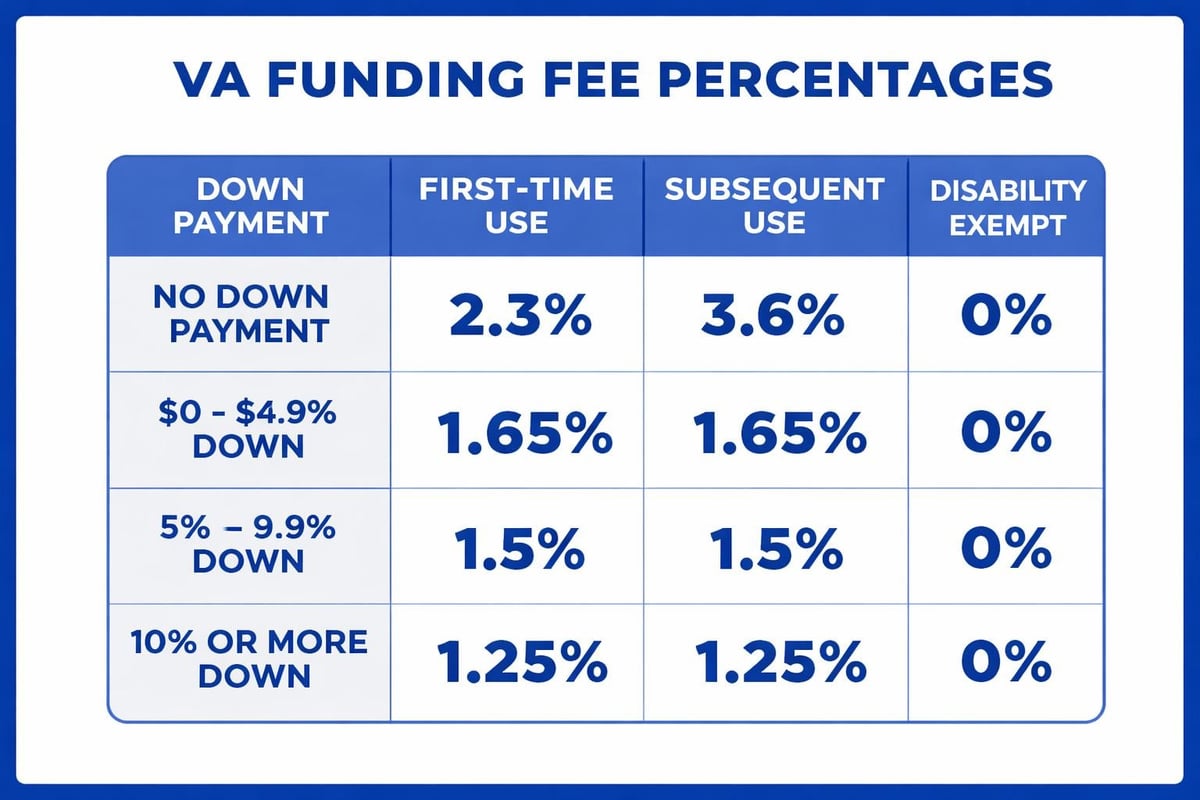

VA loans require a one-time funding fee that helps sustain the program for future generations of service members. This fee varies based on service category, down payment amount, and whether it's your first VA loan use.

For first-time use with zero down payment, the funding fee is 2.15% of the loan amount in 2026. On an $800,000 loan, that equals $17,200. Veterans making down payments reduce this fee: 10% or more down lowers it to 1.25%. For subsequent use, the zero-down fee increases to 3.3%.

Complete exemptions apply to veterans receiving VA disability compensation, those entitled to compensation but receiving retirement pay instead, and surviving spouses receiving Dependency and Indemnity Compensation. This exemption can save tens of thousands of dollars and represents a significant benefit for disabled veterans.

The funding fee can be financed into the loan amount rather than paid at closing, preserving the zero-down advantage. However, this increases your loan balance and monthly payment, so veterans with available cash might choose to pay it upfront.

Closing Cost Limitations and Seller Concessions

VA regulations limit what veterans can be charged at closing. Prohibited fees include attorney fees (unless required by state law and paid by both buyer and seller), loan application or processing fees, and various document preparation charges that are standard on conventional loans.

Sellers can pay up to 4% of the purchase price toward buyer closing costs, discount points, and prepaid items. In Seattle's competitive market, negotiating seller concessions has become more challenging in 2026, but it remains an option, particularly for homes that have been listed longer or in neighborhoods like Lynnwood or Everett where inventory levels are higher than in central Seattle.

VA Loans for Seattle's Unique Housing Market

The Greater Seattle housing market presents specific considerations for VA loan users. The region's median home prices consistently exceed national averages, making the higher conforming loan limits especially valuable for local veterans.

Condominium approvals require special attention in Seattle, where condo living is common in neighborhoods from Belltown to Capitol Hill. The VA maintains a list of approved condominium projects, and properties must be on this list before receiving VA financing. Many newer developments actively seek VA approval to attract veteran buyers, but always verify approval status before writing offers on condominiums.

For multi-unit properties, VA loans offer unique opportunities. Veterans can purchase duplexes, triplexes, or fourplexes with zero down payment, provided they occupy one unit as their primary residence. This strategy works particularly well in areas like Lake Forest Park or Shoreline where multi-family properties are more common and relatively more affordable than single-family homes.

Working with Tech Industry Compensation

Seattle's concentration of major tech employers creates opportunities for veteran employees with unique compensation structures. Veterans working at Amazon, Microsoft, Google, or other tech companies often receive significant portions of their income through restricted stock units (RSUs), stock options, or performance bonuses.

Qualifying this income for VA loans follows specific guidelines. RSUs typically require two years of receipt history, with lenders averaging the value over 24 months. Bonuses similarly need two-year histories with verification that they'll continue. Veterans with shorter tech employment histories but strong RSU packages might need to wait until establishing the required track record, though exceptions exist when employment letters confirm continuation and vesting schedules support ongoing income.

Property Requirements and the VA Appraisal

All VA loans require a VA appraisal conducted by a VA-approved appraiser. This appraisal serves dual purposes: establishing fair market value and ensuring the property meets VA Minimum Property Requirements (MPRs).

MPRs focus on safety, soundness, and sanitation. The property must have adequate heating, safe electrical systems, clean water supply, and proper sewage disposal. The roof must have at least two years of remaining life, and there can be no evidence of active pest infestation or significant structural damage.

Common issues in Seattle-area homes include:

- Peeling paint on pre-1978 properties (lead-based paint concerns)

- Roof condition on older homes, particularly after harsh winter weather

- Crawl space moisture or inadequate ventilation in areas with high water tables

- Non-permitted additions or conversions that don't meet code requirements

- Wood-destroying organism damage from moisture-related issues

Unlike conventional appraisals, VA appraisers note required repairs in their reports. Sellers must complete these repairs before closing or establish escrow holdbacks. In competitive markets, some sellers prefer conventional or cash offers to avoid VA repair requirements, though many are willing to work with VA buyers when educated about the process.

The Application and Approval Process

Securing VA loan approval follows a structured timeline that benefits from early preparation. Most VA loans close in 30-45 days, though expedited timelines down to 15-20 days are possible with responsive borrowers and experienced loan teams.

Step 1: Obtain Your Certificate of Eligibility before beginning your home search. This confirms your eligibility and shows sellers you're a serious, qualified buyer.

Step 2: Get Pre-Approved with a lender experienced in VA loans. Pre-approval involves full income documentation, credit review, and underwriter evaluation. This carries significantly more weight than pre-qualification letters and demonstrates buying power in competitive situations.

Step 3: Work with a VA-Familiar Real Estate Agent who understands how to structure competitive offers while protecting your interests. Some Seattle-area agents specialize in veteran buyers and know how to position VA offers favorably.

Step 4: Submit Your Offer and Open Escrow. Once accepted, your lender orders the VA appraisal and begins formal underwriting.

Step 5: Complete Underwriting Requirements, providing any additional documentation requested. Common requests include explanation letters for credit inquiries, verification of employment, and updated bank statements.

Step 6: Clear to Close and Schedule Your Closing once all conditions are satisfied and final approval is issued.

Throughout this process, sample VA loan documents help you understand standard forms and requirements. Staying responsive to lender requests and avoiding major financial changes during the process ensures smooth execution.

Combining VA Loans with Other Benefits

Veterans often have access to additional programs that complement their VA loan benefits. Understanding how these work together maximizes your overall advantage.

VA Disability Benefits can improve qualification by providing stable, tax-free income that lenders count favorably. This income isn't subject to federal taxes, so lenders often gross it up by 15-25% when calculating qualifying income, effectively increasing buying power.

First-Time Homebuyer Programs offered by Washington state and some local municipalities can sometimes combine with VA loans for down payment assistance or closing cost grants. While VA loans don't require down payments, these programs might cover the funding fee or provide renovation funds.

Energy-Efficient Mortgages (EEMs) allow veterans to finance energy improvements into their VA loan up to $6,000 without additional approval, or higher amounts with energy audits. For older homes in neighborhoods like Mill Creek or Everett needing insulation upgrades or HVAC replacement, this provides valuable flexibility.

Common VA Loan Myths and Misconceptions

Several persistent myths about va loans create unnecessary hesitation among eligible veterans. Setting the record straight ensures you make informed decisions.

Myth: VA loans take longer to close than conventional loans. Reality: Experienced VA lenders close loans on similar timelines. The VA appraisal might add 3-5 days compared to conventional appraisals, but overall timelines are comparable when working with efficient teams.

Myth: Sellers won't accept VA offers. Reality: In balanced or buyer-favorable markets, sellers readily accept strong VA offers. Even in competitive situations, well-structured VA offers with solid pre-approvals and flexible terms compete successfully. Education makes the difference-when listing agents understand that VA loans close reliably, resistance decreases.

Myth: You can only use your VA loan benefit once. Reality: Veterans can use their benefit multiple times throughout their lives. After selling and paying off a VA loan, your entitlement restores for future use. Some veterans even maintain multiple simultaneous VA loans using partial entitlement.

Myth: VA loans are only for first-time homebuyers. Reality: No such restriction exists. Veterans can use VA loans whether they've owned dozens of homes or none.

Myth: You must be a veteran to assume a VA loan. Reality: Both veterans and non-veterans can assume existing VA loans, though assumption requirements apply. This feature becomes valuable in rising rate environments when existing loans carry lower rates than current market rates.

Strategies for Competitive Seattle Markets

Using va loans effectively in Seattle's competitive neighborhoods requires strategic approaches that strengthen your position against conventional and cash buyers.

Escalation clauses work particularly well with VA loans. These provisions automatically increase your offer price above competing offers up to a maximum amount, demonstrating commitment while maintaining price discipline. A veteran might offer $950,000 with an escalation clause to $1,000,000 in $5,000 increments above other offers, ensuring competitiveness without overpaying.

Appraisal gap coverage addresses seller concerns about valuation. Offering to cover differences between purchase price and appraised value up to a specific amount (perhaps $20,000-$40,000) shows financial strength and commitment. This requires cash reserves but significantly strengthens VA offers.

Quick closing timelines demonstrate capability. When you're already pre-approved and can close in 20-25 days rather than 45, you become more attractive to sellers motivated by timeline certainty.

Personal letters sometimes make emotional connections with sellers, particularly those with military connections themselves or family members who've served. While not universally effective, these can occasionally tip decisions in close situations.

Working with lenders who understand Seattle's market dynamics and can provide same-day pre-approval updates when you find properties gives you speed advantages critical in fast-moving situations.

The Future of VA Loans and Recent Updates

Staying current with VA home loan news and announcements ensures you leverage the most recent program improvements. The VA regularly enhances the program based on feedback and changing market conditions.

Recent years have brought significant positive changes including elimination of loan limits for veterans with full entitlement, expansion of qualifying income sources, and streamlined processes for previously challenging situations like surviving spouse eligibility.

Technology improvements continue accelerating processes. Digital document collection, electronic signatures, and automated verification systems reduce paperwork burden and speed timelines. These improvements benefit Seattle-area veterans particularly, as many work in tech industries and expect modern, efficient digital experiences.

Looking ahead to the remainder of 2026 and beyond, expect continued program evolution focused on expanding access and improving user experience while maintaining the fundamental benefits that make VA loans exceptional for eligible service members.

Refinancing Your Existing VA Loan

Veterans with existing VA loans should periodically evaluate refinancing opportunities. Two main options serve different purposes.

IRRRLs make sense when interest rates drop at least 0.50% below your current rate. These streamlined refinances require minimal documentation, no appraisal in most cases, and no income verification. You can refinance from a 6.5% rate to a 5.5% rate and save approximately $480 monthly on an $800,000 loan, totaling $5,760 annually.

The funding fee for IRRRLs is 0.5%, significantly lower than purchase or cash-out refinances. On that same $800,000 loan, the fee would be $4,000, recoverable in less than one year through monthly savings.

Cash-out refinances work when you need to access equity, consolidate debt, or switch from a conventional loan to a VA loan. These require full documentation and appraisals but offer flexibility conventional refinances don't. You might refinance your existing $700,000 conventional mortgage on a home now worth $1,000,000, taking out $750,000 (75% LTV), eliminating $200 monthly in PMI, and extracting $50,000 for home improvements or debt consolidation.

Understanding va loans thoroughly positions Seattle-area veterans to make confident homeownership decisions that honor their service through tangible financial benefits. These mortgages represent some of the strongest financing available, and eligible service members should explore how they fit their specific situations and goals. Whether you're a first-time buyer exploring options in Shoreline, a tech professional maximizing RSU income for a purchase in Redmond, or a veteran considering refinancing your current home in Lynnwood, working with experienced professionals who understand both VA guidelines and local market conditions ensures you capture every available advantage. Mortgage Reel specializes in helping Seattle-area veterans navigate VA loans with clarity and confidence, providing the education and execution needed to turn your military benefit into successful homeownership.