Veterans and active-duty service members looking to purchase a home in the Seattle area have access to one of the most powerful financing tools available: VA loans for house purchases. These government-backed mortgages offer exceptional benefits that can make homeownership significantly more accessible and affordable, particularly in competitive markets like Seattle, Bellevue, and Redmond. Understanding how VA-backed home loans work and what advantages they provide can help you make informed decisions about your home purchase strategy.

What Makes VA Loans for House Purchases Unique

VA loans stand apart from conventional and FHA financing through several distinctive features designed specifically for those who have served our country. The Department of Veterans Affairs doesn't directly lend money but guarantees a portion of the loan, which allows participating lenders to offer more favorable terms.

Zero Down Payment Requirement

Perhaps the most significant advantage of using VA loans for house purchases is the ability to finance 100% of the home's value. In Seattle's competitive real estate market, where median home prices consistently exceed $800,000, this benefit eliminates the need to save tens of thousands of dollars for a down payment.

This feature is particularly valuable for:

- First-time homebuyers building equity from day one

- Military families relocating frequently who haven't accumulated substantial savings

- Veterans transitioning to civilian life in high-cost areas like Shoreline or Lynnwood

- Service members competing against cash buyers in tight inventory markets

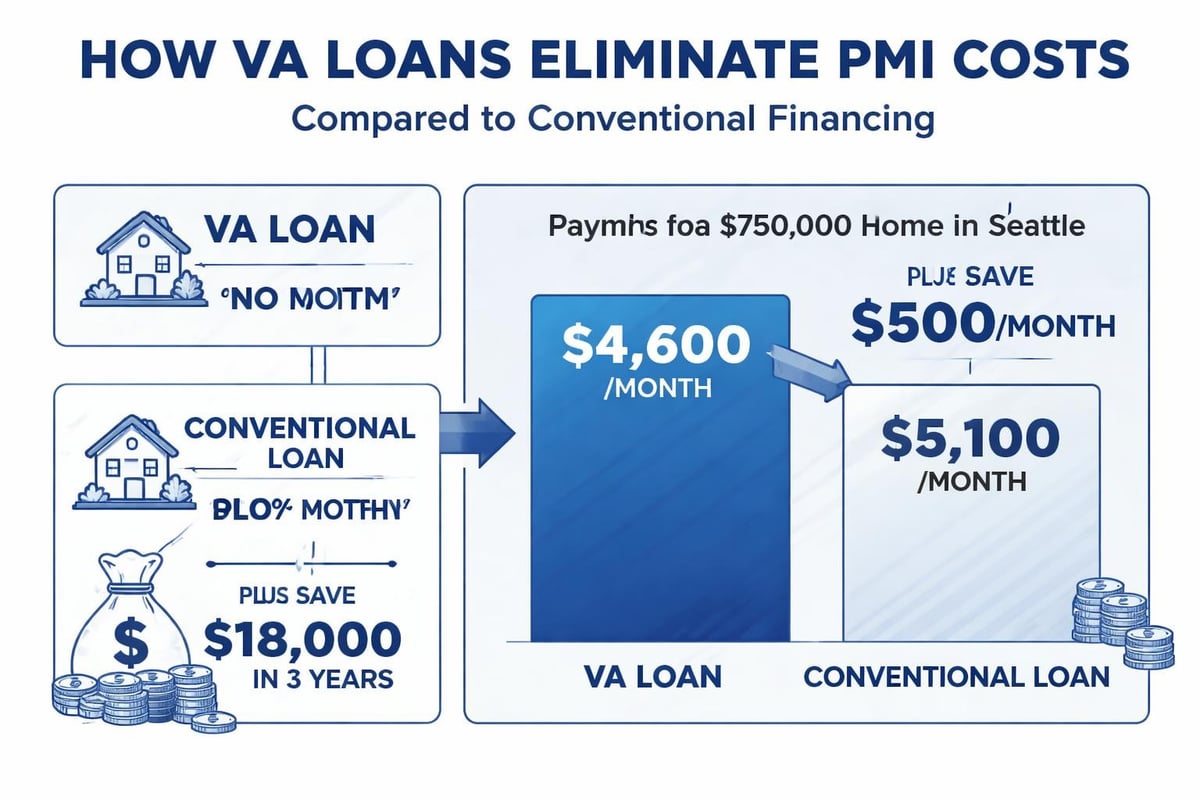

No Private Mortgage Insurance

Conventional loans typically require private mortgage insurance (PMI) when borrowers put down less than 20%. VA loans for house purchases eliminate this expense entirely, regardless of your down payment amount. For a $700,000 home in Mill Creek, this could translate to monthly savings of $350 to $500, significantly improving your purchasing power and cash flow.

VA Loan Eligibility Requirements in Washington State

Qualifying for VA loans for house purchases requires meeting specific service requirements and obtaining proper documentation. The VA eligibility criteria establish clear guidelines based on your service history and duty status.

Service History Standards

Different service categories have distinct minimum requirements:

| Service Category | Minimum Service Requirement | Additional Notes |

|---|---|---|

| Wartime Service | 90 consecutive days active duty | During qualifying wartime periods |

| Peacetime Service | 181 days active duty | Continuous service required |

| Post-9/11 Service | 90 aggregate days | Any period after September 10, 2001 |

| National Guard/Reserves | 6 years in Selected Reserve | Or 90 days active duty under Title 10 or 32 |

| Surviving Spouses | Varies by circumstance | May qualify if spouse died from service-connected disability |

Certificate of Eligibility

Before applying for VA loans for house purchases, you'll need to obtain your Certificate of Eligibility (COE). This document proves to lenders that you meet the service requirements. You can request your COE through three methods:

- Online through eBenefits – typically the fastest option, often generating instant results

- Through your lender – many experienced mortgage brokers can pull your COE directly

- By mail using VA Form 26-1880 – slower but necessary for some complex eligibility situations

Veterans working at Amazon, Microsoft, or other Seattle-area tech companies often prefer having their mortgage broker handle the COE process to streamline the overall timeline.

Understanding VA Loan Limits and Funding Fees

While the VA eliminated loan limits for most borrowers with full entitlement in 2020, understanding how the guarantee works remains important for planning your home purchase in the Seattle metro area.

VA Loan Limits Explained

Veterans with full entitlement can borrow any amount a lender approves based on creditworthiness and income qualification. However, borrowers with reduced entitlement (those who have an existing VA loan or have had a foreclosure) may face limits based on county conforming loan limits.

In King County and Snohomish County for 2026, the conforming loan limit is $806,500, which affects calculations for veterans using partial entitlement. Most borrowers purchasing in Lake Forest Park, Everett, or other area cities will have full entitlement available.

VA Funding Fee Structure

The VA funding fee is a one-time charge that helps sustain the VA loan program for future generations. This fee can be financed into your loan amount, meaning you don't need cash at closing to cover it.

Current VA Funding Fee Rates for 2026:

- First-time use, zero down: 2.15% of loan amount

- First-time use, 5% or more down: 1.50% of loan amount

- First-time use, 10% or more down: 1.25% of loan amount

- Subsequent use, zero down: 3.30% of loan amount

- Subsequent use, 5% or more down: 1.50% of loan amount

Important exemptions exist for veterans receiving VA disability compensation and surviving spouses, who pay no funding fee. For a $650,000 home purchase in Bellevue, a first-time user would pay approximately $13,975 in funding fees, which gets added to the loan balance rather than required as upfront cash.

The VA Home Purchase Process in Seattle

Navigating the home buying journey with VA loans for house purchases follows a structured path that differs slightly from conventional financing. Understanding each stage helps you move efficiently through competitive Seattle-area markets.

Step One: Financial Preparation and Pre-Approval

Before house hunting in Seattle or surrounding communities, obtain pre-approval from a VA-experienced lender. This process involves:

- Reviewing your credit history and score requirements (typically 620+ minimum)

- Analyzing your debt-to-income ratio (generally 41% maximum, though exceptions exist)

- Verifying income, including RSUs and stock compensation for tech employees

- Calculating your maximum purchasing power based on VA guidelines

Tech professionals working at Seattle-area companies should specifically discuss how their equity compensation affects VA loan qualification, as these income sources require specialized documentation and analysis.

Step Two: House Hunting with VA Loan Considerations

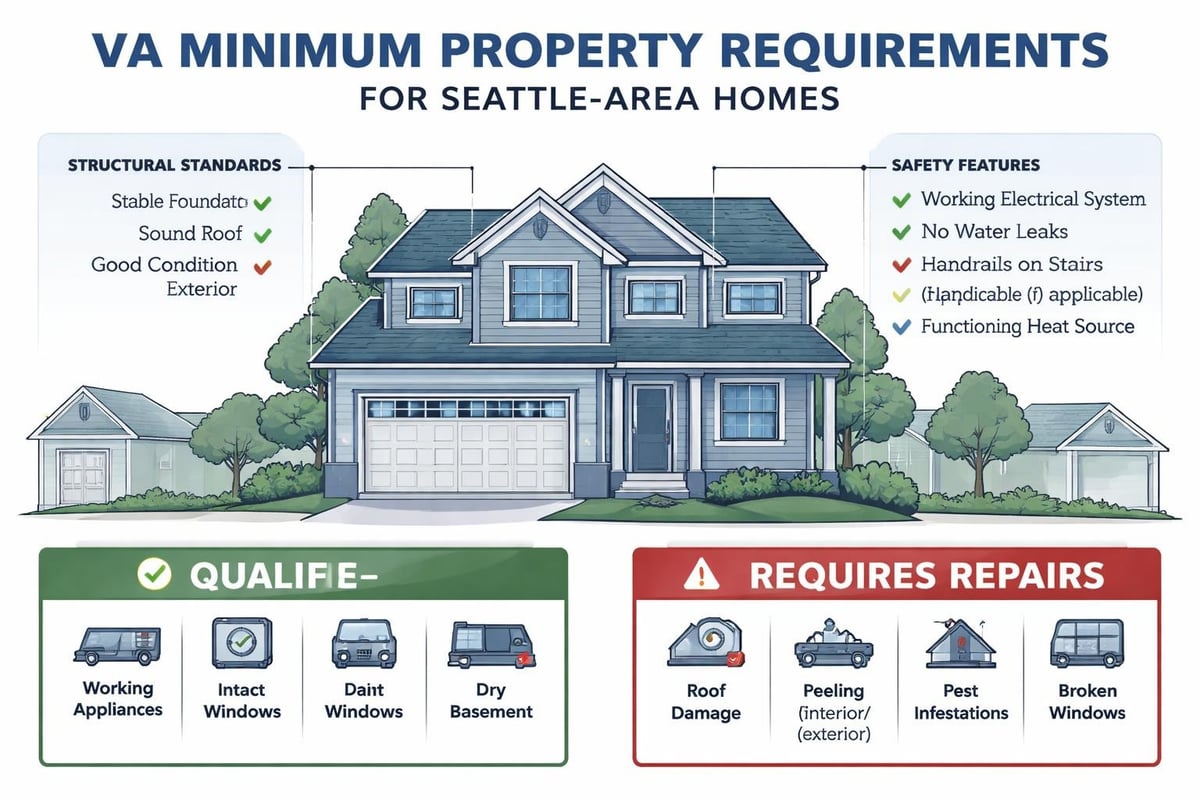

Not all properties qualify for VA financing. The home must meet minimum property requirements (MPRs) established by the VA to ensure safety, structural soundness, and sanitation. When searching in neighborhoods from Redmond to Lynnwood, keep these factors in mind:

- Properties must be move-in ready with functioning systems

- Manufactured homes built after June 15, 1976, are eligible with permanent foundations

- Condominiums require VA approval of the entire project

- Properties with certain safety hazards or deferred maintenance may require repairs before closing

Step Three: Making Competitive Offers

Seattle's housing market remains highly competitive in 2026, with multiple offers common on desirable properties. While VA loans for house purchases offer tremendous benefits, some sellers harbor misconceptions about VA financing causing delays or complications.

Strategies for strengthening your VA offer:

- Work with an experienced agent who can educate listing agents about VA advantages

- Get pre-approved by a lender known for fast VA closings (9-15 business days is achievable)

- Consider offering slightly above asking price if your budget allows

- Include a strong earnest money deposit showing commitment

- Write a personal letter explaining your service and connection to the area

The VA appraisal process often concerns sellers, but experienced mortgage brokers can typically order appraisals quickly and work through any condition requirements efficiently.

VA Loan Types Beyond Purchase Loans

While VA purchase loans represent the most common use of this benefit, the VA offers several other loan programs worth understanding for your long-term financial strategy.

Interest Rate Reduction Refinance Loan (IRRRL)

The VA IRRRL, commonly called a "VA streamline refinance," allows you to refinance an existing VA loan to secure a lower interest rate. This program features:

- Minimal documentation requirements

- No appraisal needed in most cases

- No income verification required

- Reduced funding fee of 0.50%

- Ability to finance closing costs into the loan

Seattle homeowners who purchased when rates were higher can potentially save hundreds monthly through an IRRRL when market conditions improve.

VA Cash-Out Refinance

This option lets you tap your home's equity by refinancing into a larger loan amount. Common uses include:

- Consolidating high-interest debt

- Funding home improvements or renovations

- Covering education expenses

- Investing in additional real estate

The cash-out refinance requires a new appraisal and full income verification but offers competitive rates compared to home equity loans or lines of credit.

Native American Direct Loan Program

Veterans with Native American heritage may qualify for the NADL program when purchasing, building, or improving homes on federal trust land. This specialized program provides direct lending from the VA rather than through private lenders.

Maximizing Your VA Loan Benefits in Seattle Markets

Strategic use of VA loans for house purchases requires understanding both the program's advantages and the local real estate landscape. The Greater Seattle area presents unique opportunities and challenges for veterans entering the housing market.

Timing Your Purchase

Seattle's real estate market exhibits seasonal patterns that can affect your buying experience:

Spring and Summer (March-August):

- Highest inventory levels with more choices

- Increased competition from other buyers

- Generally higher prices due to demand

- Better weather for property inspections

Fall and Winter (September-February):

- Reduced competition with fewer active buyers

- Sellers may be more negotiable on price

- Limited inventory requiring patience

- Potential for faster closings with motivated sellers

Veterans stationed at Joint Base Lewis-McChord or working at Boeing should consider coordinating their home search with PCS timelines to avoid rushed decisions.

Working with VA-Experienced Professionals

The complexity of VA loans for house purchases in competitive markets makes choosing experienced professionals crucial. Your team should include:

| Professional | Key Qualifications | Why It Matters |

|---|---|---|

| Mortgage Broker | High volume of VA loans, local market knowledge | Understands nuances of VA guidelines and can close quickly |

| Real Estate Agent | Experience representing VA buyers | Can position offers competitively and educate sellers |

| Home Inspector | Familiar with VA MPRs | Identifies issues that could affect VA approval early |

| Escrow Officer | Regular VA transaction experience | Ensures smooth closing with proper documentation |

Common VA Loan Challenges and Solutions

Even with excellent benefits, VA loans for house purchases can present specific challenges in markets like Seattle. Being prepared with solutions helps you navigate smoothly.

Challenge: Seller Resistance

Some sellers or listing agents hesitate to accept VA offers due to outdated perceptions about difficult appraisals or slow closings.

Solution: Education and proof of capability matter. Provide sellers with data showing VA closings happen just as quickly as conventional loans when working with experienced lenders. Share your strong pre-approval letter and demonstrate financial readiness. Consider working with agents who regularly represent VA buyers successfully.

Challenge: Appraisal Conditions

VA appraisers may note repairs required before closing, such as peeling paint, missing handrails, or roof issues. In Seattle's older housing stock, these conditions appear relatively frequently.

Solution: Negotiate repair credits or ask sellers to complete work before closing. Alternatively, escrow holdbacks allow closing to proceed with funds set aside for repairs. Your mortgage broker can guide you through acceptable approaches that satisfy VA requirements while keeping the transaction moving forward.

Challenge: Condo Approval

Many Seattle-area condominiums lack VA approval, limiting your options in urban buildings popular with professionals working downtown.

Solution: Your lender can pursue condo approval for unapproved buildings if they meet VA criteria. This process takes 2-4 weeks but opens opportunities other VA buyers might overlook. Focus initially on VA-approved projects to maximize efficiency.

VA Loan Documentation Requirements

Gathering proper documentation before starting your home search accelerates the approval process for VA loans for house purchases. The VA home buying process requires specific paperwork that differs from conventional loans.

Essential Documents for VA Borrowers

Prepare these items before meeting with your mortgage broker:

Military and VA Documentation:

- DD-214 showing character of discharge

- Certificate of Eligibility (COE)

- Current Leave and Earnings Statement (if active duty)

- Reserve/Guard points statement (if applicable)

Financial Documentation:

- Two years of W-2 forms and tax returns

- Most recent 30 days of pay stubs

- Two months of bank statements for all accounts

- Documentation of other income sources (rental property, disability, etc.)

Tech Industry-Specific Items:

- RSU vesting schedules and grant agreements

- Stock option documentation showing strike prices and vesting

- Bonus history and projected future bonuses

- Equity compensation statements from employers

Veterans working at Microsoft, Amazon, Google, or other Seattle tech employers should expect additional scrutiny of equity compensation. Experienced mortgage brokers understand how to calculate and document these income sources properly to maximize your qualification amount.

Credit Requirements and Debt-to-Income Ratios

While the VA doesn't mandate minimum credit scores, most lenders require 620 or higher for automated underwriting approval. Seattle-area borrowers with lower scores may still qualify through manual underwriting, though this extends processing time.

The VA uses a debt-to-income (DTI) ratio guideline of 41%, though residual income calculations can allow higher ratios. Residual income represents the money remaining after paying all monthly debts and obligations. This Veterans Affairs-specific measure ensures you have adequate funds for living expenses beyond just making mortgage payments.

2026 Residual Income Requirements for Washington State:

| Family Size | Loan Amount ?$79,999 | Loan Amount $80,000+ |

|---|---|---|

| 1 person | $390 | $451 |

| 2 people | $654 | $755 |

| 3 people | $788 | $909 |

| 4 people | $888 | $1,025 |

| 5 people | $921 | $1,062 |

These amounts reflect the monthly income you must have remaining after paying your mortgage, debts, taxes, and estimated living expenses. This requirement protects veterans from overextending financially.

Strategic Considerations for Seattle Tech Professionals

Veterans working in Seattle's technology sector have unique advantages and considerations when using VA loans for house purchases. The combination of VA benefits and high earning potential creates exceptional opportunities.

Qualifying Stock Compensation

Tech professionals at companies like Amazon receive significant portions of total compensation through RSUs, stock options, and performance bonuses. Properly documenting and qualifying this income dramatically increases your purchasing power.

RSU Qualification Requirements:

- Minimum two-year vesting history for full income credit

- One year of vesting allows 50% income credit in some cases

- Documentation must show consistent vesting schedules

- Tax returns should reflect RSU income

For example, a software engineer earning $180,000 base salary plus $120,000 in annual RSU vesting can potentially qualify using $300,000 in total income. This dramatically increases purchasing power in expensive neighborhoods from Bellevue to Kirkland.

Jumbo VA Loans

While VA loans for house purchases technically have no upper limit, loans exceeding the conforming loan limit of $806,500 are considered jumbo. These require additional scrutiny:

- More extensive documentation requirements

- Larger cash reserves (typically 6-12 months)

- Excellent credit scores (usually 680+)

- Lower DTI ratios preferred

Seattle's median home price makes jumbo VA loans common. Working with a lender experienced in jumbo VA financing ensures smooth processing of these larger transactions.

Timing Around Stock Events

Tech employees should strategically time home purchases around equity compensation events:

- Post-vesting periods provide cash for earnest money and closing costs

- Pre-IPO situations may require waiting until lockup periods expire for income qualification

- Annual bonus cycles affect DTI calculations and available funds

Coordinating with your mortgage broker about upcoming equity events helps optimize timing and qualification strategies.

VA Loan Advantages Over Other Programs

Comparing VA loans for house purchases against conventional, FHA, and other financing options highlights why this benefit holds such tremendous value for eligible veterans in the Seattle market.

VA vs. Conventional Loans

Advantages of VA:

- Zero down payment (conventional requires 3-20%)

- No PMI regardless of down payment amount

- More lenient credit requirements

- Lower interest rates due to government guarantee

- Seller can pay all buyer closing costs

When Conventional Makes Sense:

- Purchasing non-eligible properties (investment homes, commercial)

- Avoiding funding fees if you're making large down payments

- Faster appraisals in extremely competitive situations

VA vs. FHA Loans

FHA loans serve many first-time buyers, but VA loans for house purchases provide superior benefits:

| Feature | VA Loan | FHA Loan |

|---|---|---|

| Down Payment | 0% | 3.5% minimum |

| Mortgage Insurance | None | Upfront + monthly MIP |

| Funding Fee/MIP | 2.15% (waived for disabled) | 1.75% upfront + 0.85% annual |

| Credit Requirements | Typically 620+ | Typically 580+ |

| Loan Limits | None with full entitlement | $498,257 in Seattle (2026) |

The absence of monthly mortgage insurance premiums gives VA loans a significant advantage over FHA financing, saving hundreds monthly on comparable loan amounts.

Protecting Your Investment After Purchase

Successfully using VA loans for house purchases represents just the beginning of your homeownership journey. The VA provides ongoing resources and protections that continue beyond closing.

VA Loan Servicing Protections

Veterans face special protections if financial difficulties arise:

- Foreclosure prevention counseling through VA Regional Loan Centers

- Loan modification options specific to VA loans

- Repayment plans for temporary hardship situations

- Refund of unused funding fee if you refinance within 36 months

The VA encourages borrowers experiencing difficulty to contact them early. Seattle-area veterans can reach the Seattle Regional Loan Center for assistance before problems become severe.

Using Your VA Benefit Multiple Times

Contrary to common misconception, you can use VA loans for house purchases multiple times throughout your lifetime. Your entitlement restores when you:

- Pay off the existing VA loan and sell the property

- Have another eligible veteran assume your VA loan

- Receive a one-time restoration while still owning the property (if you have remaining entitlement)

Veterans relocating from Seattle to other assignments can often keep their current VA-financed home as a rental property while purchasing a new primary residence with remaining entitlement.

Refinancing Opportunities

As your financial situation evolves, you can optimize your VA loan through refinancing:

- IRRRL to lower interest rates when market conditions improve

- Cash-out refinance to access equity for renovations or investments

- Conversion to fixed-rate if you initially chose an ARM

Monitoring interest rate trends and consulting with your mortgage broker annually ensures you're maximizing the benefits of your VA loan throughout ownership.

VA Loans and Seattle's Competitive Market

Understanding how to deploy VA loans for house purchases effectively in Seattle's competitive environment requires strategic thinking beyond just qualification and approval.

Multiple Offer Situations

When competing against numerous buyers in desirable Shoreline or Mill Creek neighborhoods, strengthen your VA offer by:

- Escalation clauses that automatically increase your bid up to a specified maximum

- Appraisal gap coverage where you agree to pay some difference if appraisal comes in low

- Quick closing timelines demonstrating your lender's efficiency

- Minimal contingencies while maintaining prudent protections

Your mortgage broker should provide a strong pre-approval letter specifically mentioning underwriting completion and rapid closing capability.

New Construction and VA Loans

Seattle-area new construction represents an excellent opportunity for VA buyers. Builders typically understand VA financing and appreciate the qualified buyer pool veterans represent. Benefits include:

- Customization options during construction

- New home warranties providing peace of mind

- No competing offers on newly released lots

- Energy-efficient features reducing long-term costs

When purchasing new construction in developments around Everett or Lake Forest Park, ensure the builder's timeline aligns with your VA loan approval. Most approvals remain valid for 120 days, with extensions available if construction delays occur.

Investment Property Limitations

VA loans for house purchases require occupancy as your primary residence. You cannot use VA financing for pure investment properties or vacation homes. However, multi-unit properties (up to 4 units) qualify if you occupy one unit as your primary residence.

This creates excellent opportunities for house hacking strategies where rental income from additional units helps offset your mortgage payment while building equity and providing cash flow.

VA loans for house purchases provide exceptional benefits that make homeownership more accessible and affordable for veterans throughout the Seattle area, from zero down payments to competitive interest rates without mortgage insurance. Whether you're a tech professional leveraging RSU income or a military family relocating to the Pacific Northwest, understanding these powerful financing tools positions you for success. Keith Akada at Mortgage Reel brings 25+ years of experience helping Seattle-area veterans navigate VA loans with transparency and strategic guidance, backed by 750+ five-star reviews and the ability to close in as few as 9 business days.