Navigating the home financing process in Seattle's competitive real estate market requires more than just comparing interest rates online. A qualified mortgage professional serves as your guide through complex lending guidelines, documentation requirements, and strategic decision-making that can save you thousands of dollars over the life of your loan. Whether you're purchasing your first home in Shoreline, refinancing in Lynnwood, or securing a jumbo loan for a property in Lake Forest Park, understanding what a mortgage professional does and how they add value is essential to making confident financing decisions.

Understanding the Core Responsibilities of a Mortgage Professional

The term mortgage professional encompasses licensed loan officers, mortgage brokers, and loan originators who facilitate home financing transactions. These professionals act as intermediaries between borrowers and lenders, managing the entire loan process from initial consultation through closing.

Primary duties include:

- Assessing borrower financial profiles and qualifying capacity

- Explaining loan program options and qualifying requirements

- Collecting and organizing required documentation

- Submitting loan applications to appropriate lenders

- Coordinating with underwriters, processors, and title companies

- Problem-solving obstacles that arise during underwriting

- Ensuring timely closing within contract deadlines

Unlike bank loan officers who represent a single institution, independent mortgage brokers work with multiple lenders. This structure allows them to shop rates and programs across various wholesale channels, often securing better terms than borrowers could obtain directly. According to professional mortgage industry standards, uniformity in data sharing and transaction processing has streamlined how mortgage professionals coordinate complex loan files.

Licensing and Regulatory Requirements

Every mortgage professional operating in Washington State must hold an active Mortgage Loan Originator (MLO) license through the Nationwide Multistate Licensing System (NMLS). This credential requires passing the SAFE Mortgage Loan Originator Test, completing 20 hours of pre-licensing education, and maintaining continuing education annually.

Licensing ensures professionals:

- Understand federal lending regulations like TILA and RESPA

- Maintain ethical standards and fiduciary responsibility

- Stay current on changing guidelines and programs

- Submit to background checks and financial reviews

These regulatory frameworks protect consumers from predatory practices while establishing baseline competency standards. When selecting a mortgage professional in Seattle or surrounding areas like Mill Creek and Everett, verifying active licensing status through NMLS Consumer Access provides transparency about disciplinary history and professional credentials.

How Mortgage Professionals Add Strategic Value

Beyond administrative loan processing, experienced mortgage professionals provide strategic counsel that directly impacts your financial outcomes. This expertise becomes particularly valuable in markets like Seattle where home prices, inventory constraints, and competitive bidding create complex purchasing scenarios.

Income Qualification Expertise

For tech professionals working at Amazon, Microsoft, or Google, stock-based compensation presents unique qualification challenges. A knowledgeable mortgage professional understands how to document and calculate:

- Restricted Stock Units (RSUs) for debt-to-income ratios

- Performance bonuses with appropriate averaging periods

- Stock options and their treatment under various loan programs

- Sign-on bonuses and their continuity requirements

These income sources can significantly increase purchasing power when properly documented and presented to underwriters. A mortgage professional familiar with these compensation structures ensures you qualify for the maximum loan amount supported by your total income picture.

Program Selection and Structuring

The mortgage landscape includes dozens of distinct loan programs, each with specific qualifying criteria, rate structures, and strategic applications. An effective mortgage professional matches your financial profile and goals to optimal program choices.

| Loan Program | Best For | Key Advantage | Typical Rate Comparison |

|---|---|---|---|

| Conventional | Strong credit, 3-20% down | Lowest rates, flexible terms | Benchmark |

| FHA | Lower credit, 3.5% down | Accessible qualification | +0.25-0.50% |

| VA | Military service members | Zero down payment | -0.125-0.25% |

| Jumbo | Loan amounts over $802,650 | High-balance financing | +0.25-0.75% |

| Adjustable Rate | Short-term ownership plans | Lower initial payments | -0.50-1.00% |

In Seattle's high-cost market, where median home prices exceed conventional loan limits, jumbo loan expertise becomes particularly valuable. A mortgage professional who regularly structures jumbo financing understands how to navigate stricter qualification ratios, larger reserve requirements, and lender-specific overlays that can complicate approval.

Rate Negotiation and Timing Strategy

Interest rates fluctuate daily based on bond market movements, economic data releases, and Federal Reserve policy signals. A mortgage professional monitors these trends and advises on optimal timing for rate locks.

Strategic rate management includes:

- Floating versus locking during application processing

- Short-term locks for quick closings versus extended locks for new construction

- Rate renegotiation options if markets improve before closing

- Understanding how discount points affect effective rates

For a purchase in Lynnwood with a 21-day closing timeline, your mortgage professional might recommend locking immediately to eliminate rate risk. Conversely, a refinance transaction with flexible timing might benefit from a float-down option if economic indicators suggest declining rates.

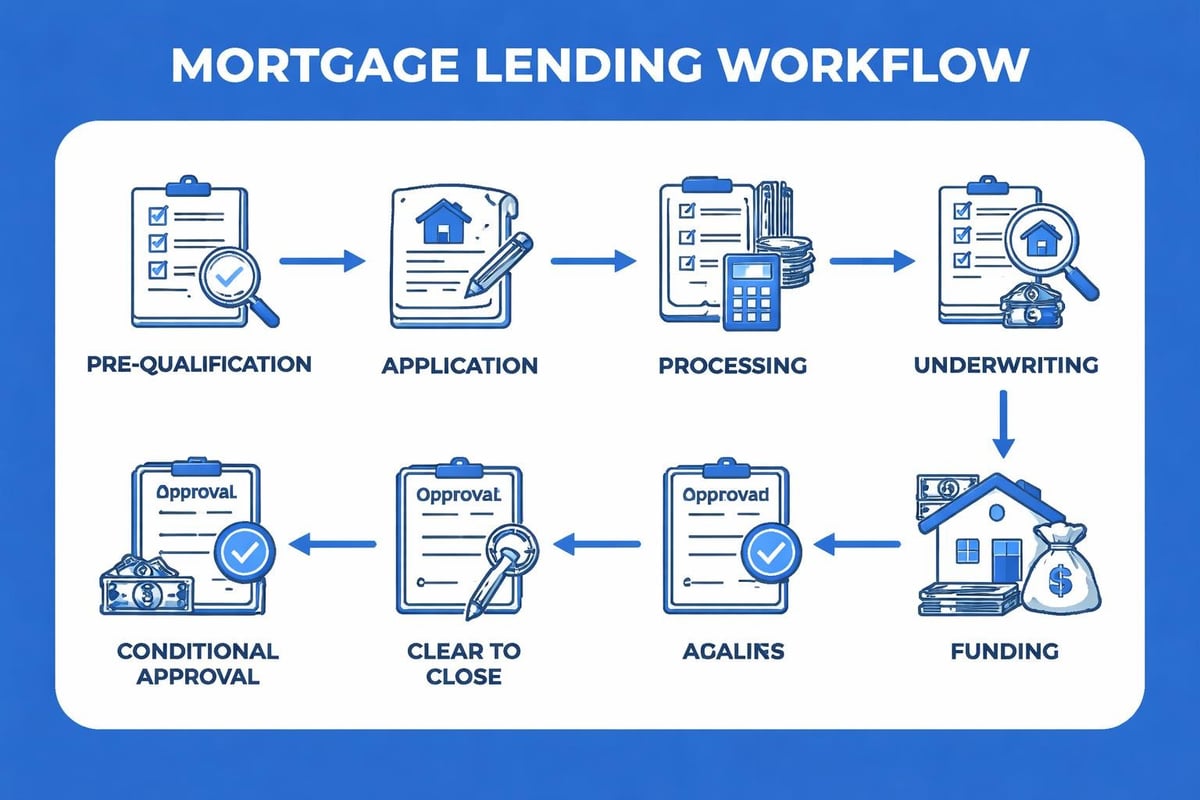

The Qualification and Application Process

Working with a mortgage professional begins with an initial consultation where they assess your financial readiness and outline realistic expectations for loan approval. This discovery phase establishes the foundation for a successful transaction.

Financial Assessment and Pre-Approval

A thorough pre-approval involves analyzing multiple financial components:

- Credit profile review examining scores, tradelines, and derogatory items

- Income documentation verifying employment, earnings history, and stability

- Asset verification confirming down payment funds and reserve requirements

- Debt analysis calculating existing obligations and qualifying ratios

- Property considerations reviewing target price ranges and property types

The mortgage professional compiles this information into a comprehensive pre-approval letter that demonstrates your qualification to sellers and listing agents. In competitive Seattle neighborhoods, pre-approval strength often determines whose offer gets accepted in multiple-bid situations.

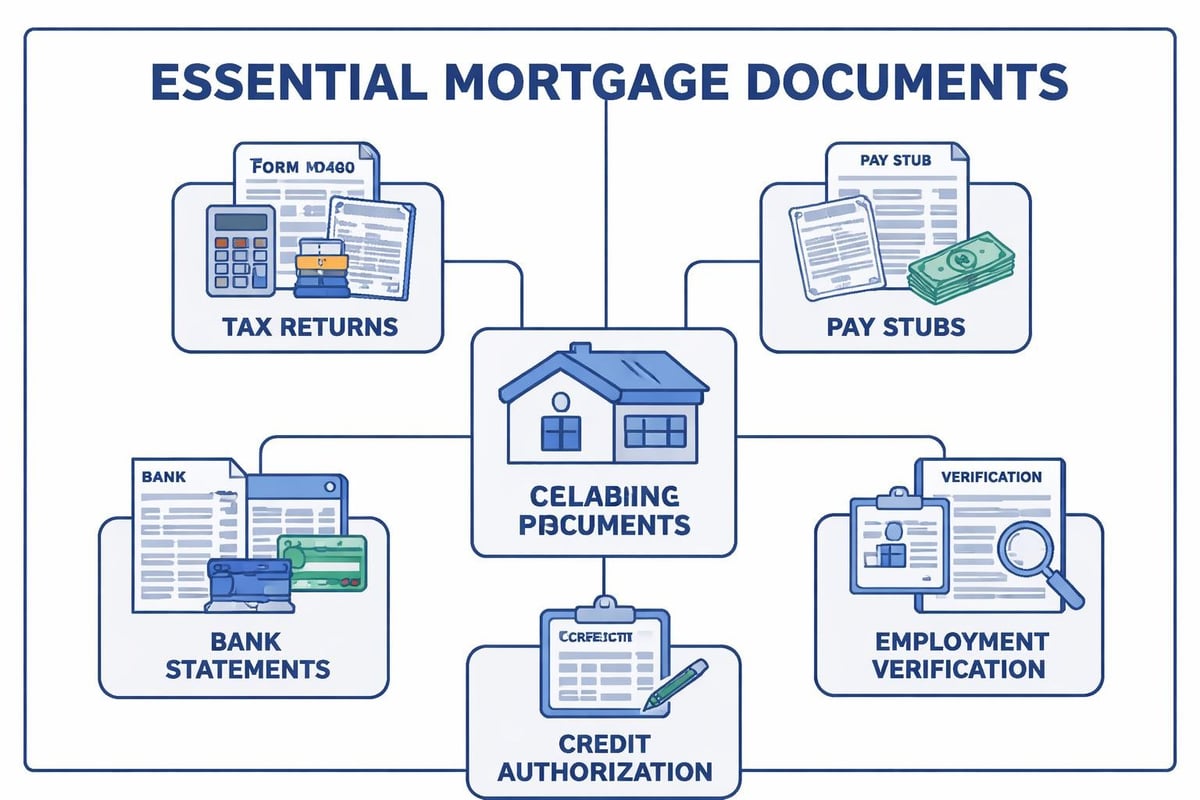

Documentation Coordination

One of the most valuable services a mortgage professional provides is managing the extensive documentation required for modern mortgage underwriting. Post-2008 financial reforms significantly increased verification requirements, creating complexity that overwhelms many borrowers.

Standard documentation includes:

- Two years of tax returns with all schedules

- 30-60 days of pay stubs showing year-to-date earnings

- Two months of bank statements for all accounts

- Explanation letters for large deposits or credit inquiries

- Employment verification directly from HR departments

- Gift letters and transfer documentation for down payment assistance

Your mortgage professional knows exactly what underwriters need, how documents should be formatted, and which explanations preempt common objections. This expertise accelerates processing timelines and prevents last-minute document requests that could delay closing.

Problem Solving and Transaction Management

Even well-qualified borrowers encounter obstacles during the mortgage process. Title issues, appraisal challenges, employment changes, and underwriting conditions require creative problem-solving and experienced guidance.

Common Challenges and Solutions

A skilled mortgage professional anticipates potential issues and implements proactive solutions:

Appraisal shortfalls: When a Lake Forest Park property appraises below purchase price, your mortgage professional explores options including renegotiating price, increasing down payment, or challenging the appraisal with additional comparables.

Employment verification delays: If HR departments are slow responding to verification requests, experienced professionals maintain direct contacts and escalation procedures to prevent closing delays.

Credit score fluctuations: New credit inquiries or balance changes during processing can impact approval. Your mortgage professional monitors credit and advises on maintaining scores through closing.

Income calculation disputes: When underwriters question income continuity or calculation methodology, your mortgage professional provides supporting documentation and guideline references to substantiate qualification.

These interventions require deep knowledge of underwriting standards, lender-specific policies, and creative structuring approaches. The difference between a mortgage professional and an order-taker becomes apparent when complications arise.

Coordination with Transaction Partners

Successful closings require seamless coordination among multiple parties. Your mortgage professional serves as the central communication hub connecting:

- Real estate agents representing buyers and sellers

- Escrow and title companies managing closing logistics

- Home inspectors identifying property conditions

- Appraisers valuing properties

- Insurance agents providing homeowners coverage

- Underwriters reviewing loan files

In Seattle's fast-paced market, where purchase agreements often specify 21-30 day closing timelines, this coordination becomes critical. A mortgage professional who maintains strong relationships with reliable partners and communicates proactively keeps transactions on track.

Specialized Expertise for Different Borrower Profiles

Not all mortgage professionals offer the same depth of expertise across borrower types and transaction scenarios. Identifying a professional whose specialization aligns with your situation improves outcomes significantly.

First-Time Homebuyers

First-time buyers in areas like Shoreline or Mill Creek benefit from mortgage professionals who provide educational guidance alongside transaction execution. These professionals explain foundational concepts without overwhelming jargon and help navigate down payment assistance programs, first-time buyer grants, and optimal program selection.

Real Estate Investors

Investment property financing involves different qualification ratios, down payment requirements, and rate structures than primary residences. Mortgage professionals serving investors understand how to:

- Calculate rental income using leases and tax returns

- Structure multiple simultaneous transactions

- Navigate DSCR (Debt Service Coverage Ratio) loan programs

- Optimize entity structuring for portfolio growth

High-Income Tech Professionals

Seattle's concentration of technology employers creates unique mortgage scenarios involving complex compensation packages. As noted in industry analysis of mortgage professional specialization, top performers develop niche expertise serving specific client demographics.

For Amazon or Microsoft employees, a mortgage professional with stock compensation expertise maximizes qualifying income by:

- Understanding vesting schedules and income continuity arguments

- Calculating two-year averages when RSU values fluctuate

- Documenting employer stock programs with proper verification

- Structuring jumbo loans that accommodate high loan amounts with strong income profiles

This specialization directly translates to increased purchasing power and smoother approval processes.

Technology and Process Efficiency

Modern mortgage professionals leverage technology platforms that streamline application, documentation, and communication workflows. These tools improve transparency and reduce processing timelines.

Digital Application Platforms

Online portals allow borrowers to:

- Complete initial applications from any device

- Upload documents securely with automatic organization

- Track loan status in real-time

- Communicate with loan teams through integrated messaging

- Receive automated updates on conditions and requirements

However, technology complements rather than replaces professional expertise. While platforms automate routine tasks, complex scenarios still require human judgment and creative problem-solving.

Advanced Underwriting Capabilities

Some mortgage professionals work with lenders offering proprietary underwriting systems that accelerate approval timelines. These platforms use automated valuation models, instant employment verification, and digital asset verification to compress traditional 30-45 day processing into 9-14 business days.

For buyers competing in Everett's market where quick closings provide competitive advantages, this capability can determine whether offers get accepted.

Selecting the Right Mortgage Professional

Choosing which mortgage professional to work with significantly impacts your financing experience and outcomes. Several evaluation criteria help identify qualified candidates.

Review and Reputation Analysis

Online reviews across platforms like Google, Zillow, and Yelp provide insight into client experiences. However, understanding how to interpret mortgage lender ratings requires examining review volume, recency, and response patterns rather than just average scores.

Key indicators of quality include:

- Consistent themes in positive reviews about communication and expertise

- High review volume indicating sustained client satisfaction

- Recent reviews demonstrating current performance

- Professional responses to occasional negative feedback

- Recognition through industry awards or top performer rankings

A mortgage professional with 750+ five-star reviews across multiple platforms demonstrates consistent execution over many transactions.

Communication Style and Availability

Your mortgage professional should maintain proactive communication throughout the process. Ask potential professionals about their typical response times, preferred communication channels, and availability for questions.

Questions to ask include:

- How quickly do you typically respond to emails and calls?

- Will I work directly with you or be handed off to a team?

- How often will you update me on loan progress?

- What's your process for handling urgent situations outside business hours?

In competitive Seattle markets where purchase agreements may require responses within hours, accessibility becomes critical.

Local Market Knowledge

While lending guidelines apply nationally, local market dynamics affect strategy and execution. A mortgage professional serving Seattle, Bellevue, Redmond, and Kirkland understands:

- Typical appraisal timelines and appraiser availability

- Local title company capabilities and closing procedures

- HOA documentation requirements for condominiums

- Competitive offer structures including escalation clauses and appraisal gaps

- Municipality-specific requirements for certain property types

This knowledge helps anticipate and navigate location-specific challenges that might surprise professionals primarily working in other markets.

Cost Structures and Compensation Models

Understanding how mortgage professionals are compensated provides transparency about potential conflicts of interest and cost optimization strategies.

Lender-Paid Compensation

Most mortgage professionals receive compensation from the lender rather than charging borrowers directly. This lender-paid model typically ranges from 0.50% to 2.50% of the loan amount, depending on loan type and lender policies.

This structure offers advantages:

- No upfront fees to work with a professional

- Compensation already factored into quoted rates

- Incentive alignment around successful closing

Borrower-Paid Origination

Some transactions involve borrower-paid origination fees, particularly for specialized programs or challenging scenarios requiring extra work. These fees should be clearly disclosed in initial Loan Estimates.

Rate and Fee Transparency

Reputable mortgage professionals provide transparent rate quotes showing how closing costs and interest rates interact. Lower rates typically involve higher upfront costs through discount points, while zero-cost options carry higher rates that recoup lender expenses through interest over time.

Your mortgage professional should explain these tradeoffs clearly and help you determine optimal cost structures based on how long you plan to keep the loan.

Industry Evolution and Future Trends

The mortgage industry continues evolving through regulatory changes, technological advancement, and market dynamics. Understanding these trends helps borrowers work effectively with mortgage professionals.

Regulatory Framework Development

Organizations like MISMO establish data standards that improve information sharing across the mortgage ecosystem. These standards reduce errors, accelerate processing, and enhance transparency.

Recent regulatory focus areas include:

- Artificial intelligence use in underwriting decisions

- Data privacy and cybersecurity requirements

- Fair lending oversight and disparate impact analysis

- Remote online notarization expansion

Mortgage professionals must continuously adapt to these evolving requirements while maintaining efficient service delivery.

Professional Designation Growth

Industry credentials beyond basic licensing demonstrate commitment to advanced expertise. Designations like Certified Mortgage Planner indicate professionals who view mortgages holistically within broader financial planning contexts.

These specialized credentials become particularly valuable for complex scenarios involving tax strategy, estate planning, or comprehensive wealth management integration.

Working Effectively with Your Mortgage Professional

Borrowers who actively participate in the mortgage process and maintain organized communication achieve better outcomes and smoother transactions.

Preparation Best Practices

Before engaging a mortgage professional, organize your financial documentation:

- Gather two years of tax returns with all schedules

- Collect recent pay stubs covering 30+ days

- Compile bank statements for all accounts (2-3 months)

- Document gift funds with transfer history

- List all debts with account numbers and monthly payments

- Note any credit issues requiring explanation

This preparation accelerates initial qualification and demonstrates your commitment to a smooth process.

Maintaining Open Communication

Share relevant information proactively rather than waiting for requests:

- Job changes or employment transitions

- Large deposits or withdrawals from accounts

- New credit applications or financing inquiries

- Property search updates and timeline adjustments

- Questions about documents or requirements

Early disclosure allows your mortgage professional to address potential issues before they impact approval or closing timelines.

Understanding Timeline Expectations

Realistic timeline expectations prevent stress and disappointment. Standard purchase transactions typically require:

- Pre-approval: 1-2 business days with complete documentation

- Processing: 3-5 business days to submit complete file to underwriting

- Initial underwriting: 2-5 business days for first review and conditions

- Condition satisfaction: 3-7 business days depending on documentation complexity

- Final approval: 1-2 business days after all conditions cleared

- Closing preparation: 2-3 business days for final document preparation

Advanced underwriting platforms can compress these timelines significantly, but borrower responsiveness remains the primary variable affecting speed.

Working with an experienced mortgage professional transforms the home financing process from an overwhelming challenge into a manageable journey with expert guidance at every step. Whether you're purchasing your first home, refinancing to optimize your current loan, or structuring complex financing for investment properties or jumbo purchases, the right professional expertise makes all the difference. Mortgage Reel, led by Keith Akada, brings over 25 years of Seattle-area lending experience with specialized expertise in stock compensation, competitive purchase scenarios, and accelerated closing timelines, backed by 750+ five-star reviews. If you're ready to explore your financing options with a trusted local expert, reach out to start your pre-approval conversation today.