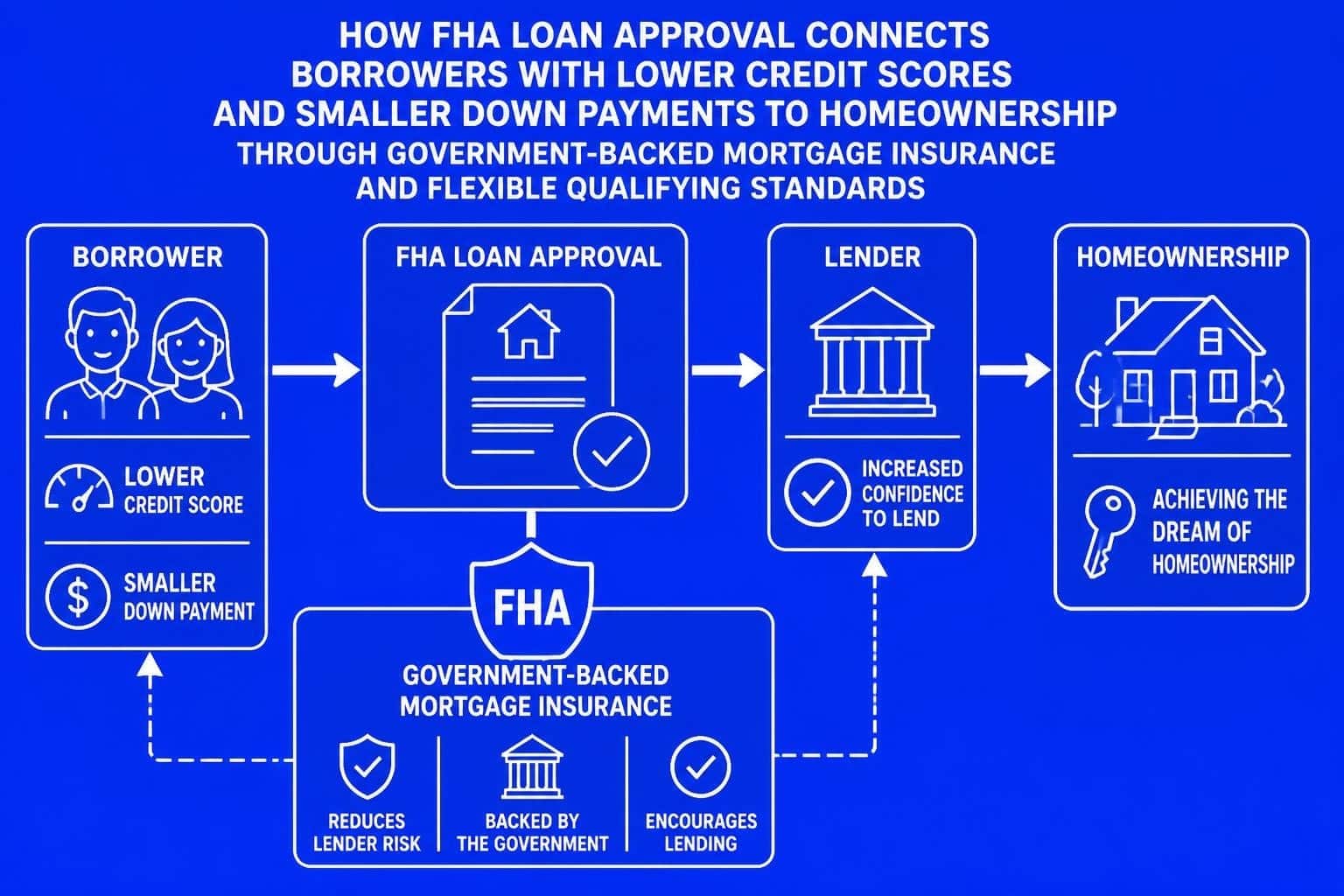

Check Your Credit

One of the first things you can do to make your buying power the strongest is to clean up your credit. The higher the credit score, the lower the interest rate you will qualify for, and an increase in mortgage product availibility. If you have concerns contact our trust advisor, we can provide advice or refer you to a credit specialist.

Debt to Income Ratios

A lender will determine how much you can afford by calculating your total monthly housing costs. To determine your cost ratio, take the principal, interest, taxes and insurance (PITI) total and divide by your total monthly pretax income.

The other ratio that is crucial for qualifying is to calculate your total debt ratio. To determine your debt ratio, take the PITI total plus all other monthly debt divided by your total monthly pretax income. Calculating your other monthly debt, credit cards use the minimum payment, auto loans use the monthly payment, if you have less then 10 months remaining on the loan you generally get to waive this payment from your total calculation.

Down Payment

Today’s market will require you to have a minimum down payment of 3% of the purchase price. Depending on the type of financing the down payment can be gifted or borrowed based on specific scenarios. Also consider if funds for the down payment are coming from investment accounts, you will be able to use either 60-70% of the actual account value. The underwriters know you will not receive 100% of the value for an investment. If funds are in a savings, checkings accounts (liquid), you will be able to use 100% of the value.

Leave a Reply