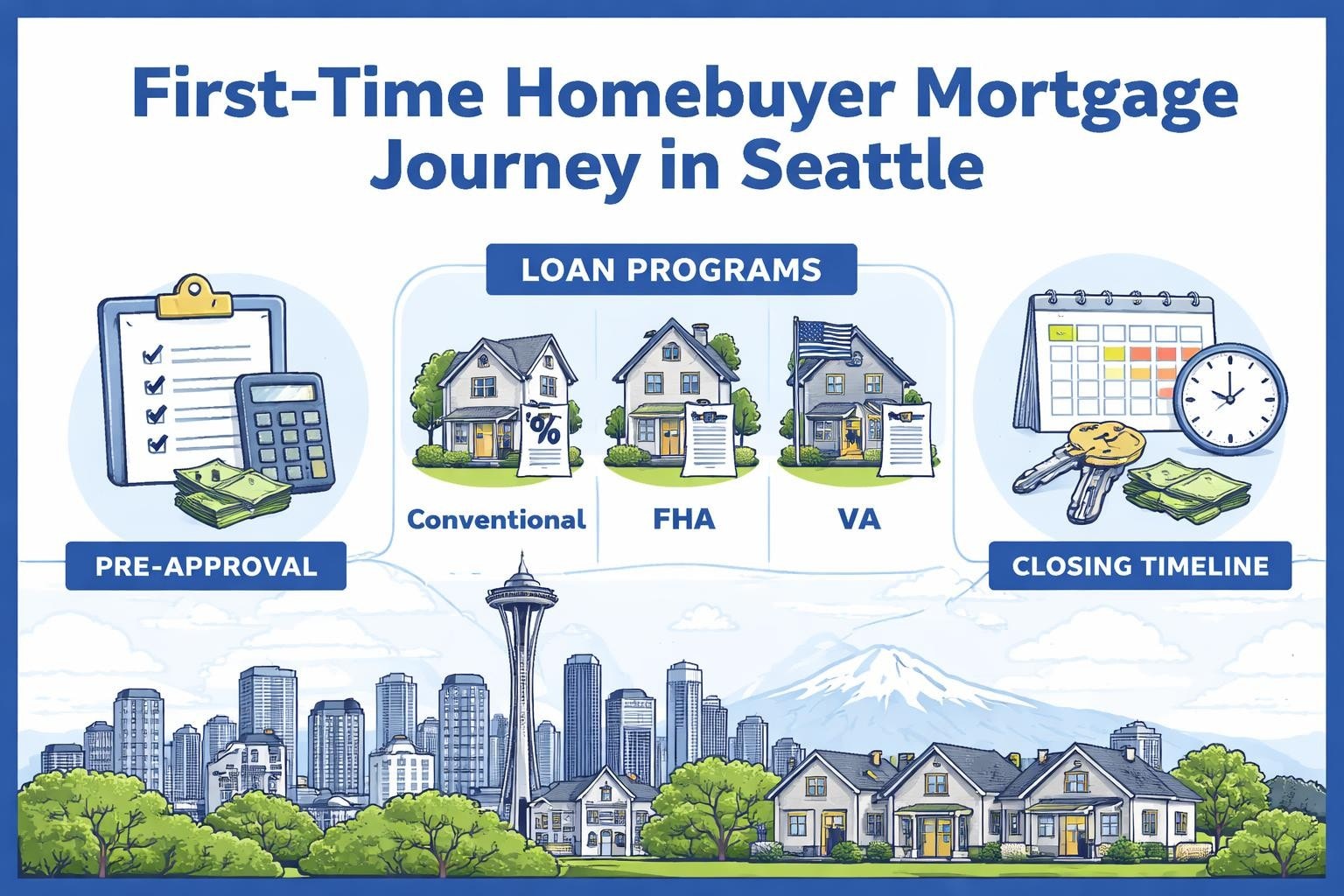

Thinking of buying a home in Seattle, Shoreline, or the surrounding area in 2026? As home values climb in Mill Creek and Everett, understanding conventional home financing is more important than ever for both buyers and homeowners. The right financing strategy can help you save money, increase your buying power, and put your dream home within reach.

In this guide, you will learn the basics of conventional home financing, explore updated requirements for 2026, weigh the pros and cons, follow a step-by-step approval process, and gain insights into the unique Seattle market. This comprehensive resource will demystify conventional home financing for 2026, empowering Seattle-area buyers and homeowners to make confident, strategic decisions.

Understanding Conventional Home Loans in 2026

Navigating the Seattle housing market in 2026 means mastering the essentials of conventional home financing. For buyers in Shoreline, Mill Creek, Lynnwood, and Everett, understanding what sets conventional loans apart is the first step to a confident purchase.

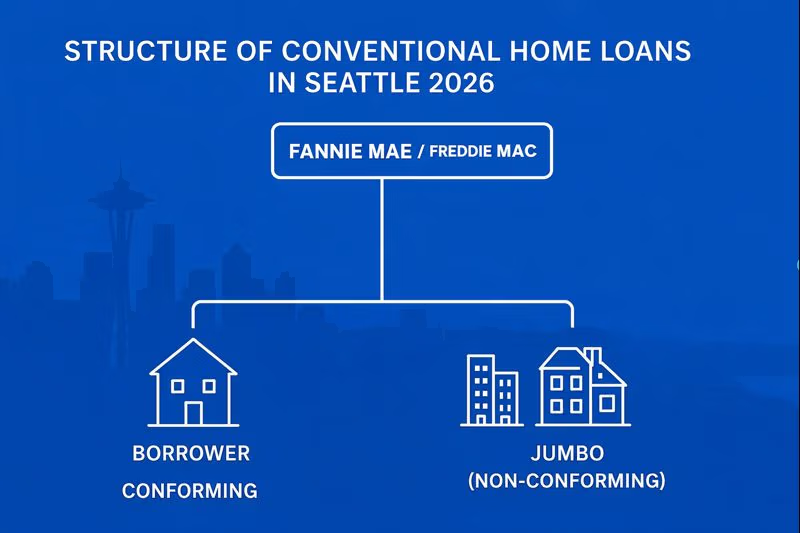

A conventional home loan is a mortgage not insured by the federal government. Instead, it is offered by private lenders and follows guidelines set by Fannie Mae and Freddie Mac. This is different from FHA, VA, and USDA loans, which are backed by federal agencies.

Comparing Conventional and Government-Backed Loans

To help clarify, here’s a side-by-side look at conventional home financing versus government-backed options:

| Feature | Conventional Loan | FHA Loan | VA Loan | USDA Loan |

|---|---|---|---|---|

| Minimum Down Payment | 3-5% (first-time buyers) | 3.5% | 0% | 0% |

| Credit Score Requirement | 620+ | 580+ | Varies | 640+ |

| Mortgage Insurance | PMI if <20% down | Upfront & annual MIP | No PMI | Annual fee |

| Eligibility | Broad | Flexible | Veterans/military | Rural/area limits |

Conventional home financing is often chosen by buyers who have stronger credit and can make a larger down payment. For instance, a tech professional in Mill Creek may opt for a conventional loan to avoid the ongoing mortgage insurance premiums associated with FHA loans.

Why Conventional Loans Remain Popular

According to NAR data, 64% of homebuyers in 2025 selected conventional home financing. This trend is expected to continue in 2026, especially in high-demand areas like Seattle and Everett. The appeal comes from competitive rates, flexible terms, and the ability to use the loan for a wide range of property types.

Conforming vs. Non-Conforming (Jumbo) Loans

Conventional home financing includes both conforming and non-conforming (jumbo) loans. Conforming loans meet the loan limit guidelines set for each county. In King and Snohomish Counties, these limits have risen to reflect 2026’s higher home values.

For example, if a Lynnwood buyer is purchasing a home above the conforming limit, they would need a jumbo loan. Jumbo loans allow buyers in places like Seattle and Bellevue to finance high-value homes but often require higher credit scores and larger down payments.

The Role of Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac are government-sponsored enterprises that buy and guarantee conforming conventional loans. Their presence in the Seattle mortgage market ensures liquidity and competitive rates for buyers and homeowners. Lenders across Lake Forest Park and Everett rely on these entities to keep the market moving smoothly.

Uses and Flexibility of Conventional Loans

Conventional home financing is highly adaptable. Buyers can use these loans to:

- Purchase a primary residence

- Refinance an existing home

- Buy a second home or vacation property

- Invest in rental or multi-unit properties

For those interested in investment opportunities, conventional loans offer robust options. In fact, you can learn more about investment mortgage loan options if you’re considering building a real estate portfolio in Seattle or the surrounding cities.

Property flexibility is another advantage. Conventional loans cover:

- Single-family homes

- Condominiums

- Townhomes

- Duplexes, triplexes, and fourplexes

This adaptability is crucial as buyers in Everett or Mill Creek seek homes that fit their lifestyle and long-term goals.

Key Insight: Adaptability for Seattle’s Market

The strength of conventional home financing lies in its ability to meet the diverse needs of buyers in Seattle, Shoreline, and beyond. Whether you are a first-time buyer in Lake Forest Park or an investor in Lynnwood, this loan type offers solutions tailored to local market conditions and personal circumstances.

Conventional home financing is expected to remain the backbone of Seattle-area home purchases in 2026. By understanding its features and requirements, buyers can make informed decisions and secure their future in a thriving market.

2026 Conventional Loan Requirements: What Seattle Buyers Need to Know

Navigating the world of conventional home financing in Seattle for 2026 means understanding updated approval standards. As home values climb in Mill Creek, Everett, and across the metro, lenders have refined requirements to ensure buyers are well-qualified. Whether you’re planning to purchase in Shoreline or refinance in Lynnwood, meeting these standards is the first step to a smooth, confident transaction.

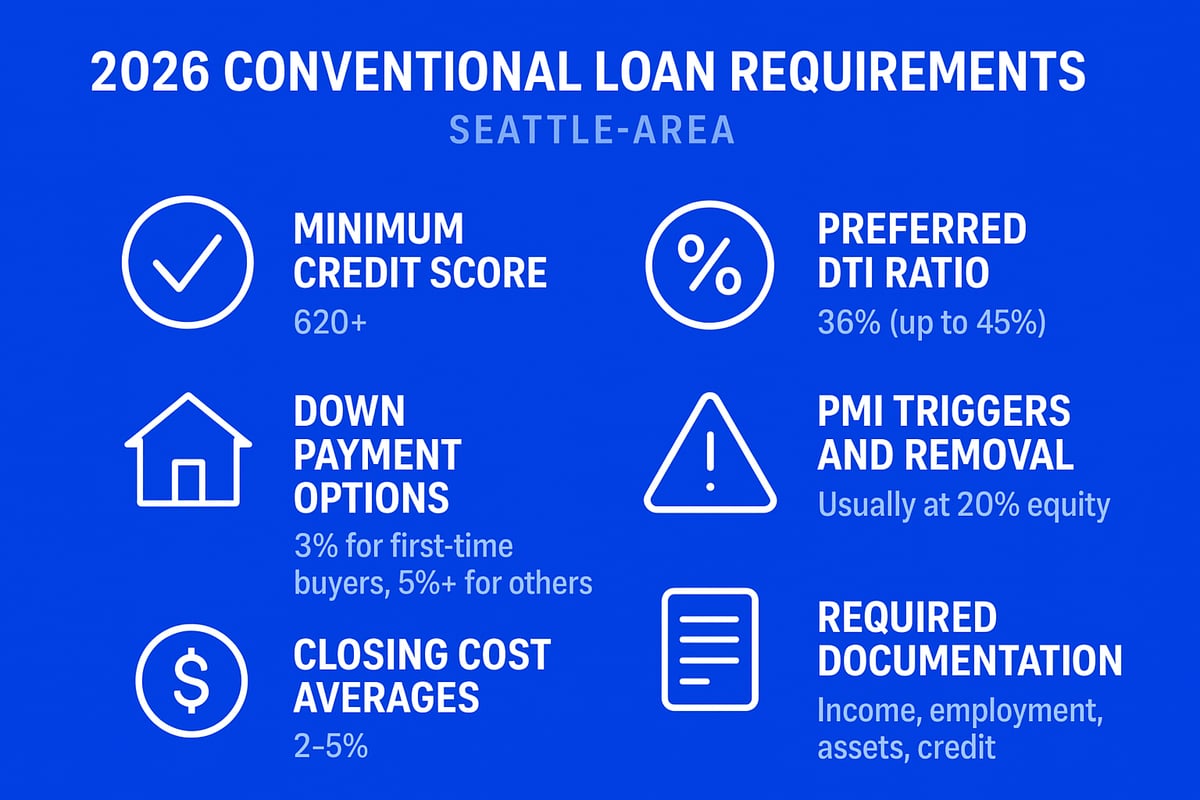

Minimum Credit Score Requirements

For 2026, most Seattle lenders require a minimum credit score of 620 for conventional home financing. If you’re aiming for a jumbo loan, like those often needed in Bellevue or high-value parts of Everett, expect a higher threshold—typically 700 or above.

Lenders assess your credit history closely. A strong score can unlock lower rates, saving thousands over the life of your loan. If your score is below the benchmark, take time to pay down debts and correct any errors before applying.

Debt-to-Income (DTI) Ratio Guidelines

Debt-to-income ratio is another key factor in conventional home financing. Seattle-area lenders generally look for a DTI of 36% or less, though some buyers may qualify with ratios up to 50% if they have strong compensating factors like high credit scores or substantial reserves.

To calculate DTI, divide your total monthly debt payments by your gross monthly income. For example, a Mill Creek buyer earning $10,000 monthly with $3,600 in debts would have a DTI of 36%. Keeping your DTI low improves your approval odds and could qualify you for better rates.

Down Payment Minimums and PMI

Down payment requirements for conventional home financing vary by scenario. First-time buyers in Lake Forest Park may qualify with as little as 3% down, while repeat buyers or those purchasing investment properties usually need 5% or more. Multi-unit or non-owner-occupied homes have higher minimums.

If your down payment is less than 20%, lenders require private mortgage insurance (PMI). This protects the lender, not the buyer, but can be removed once you reach 20% equity. For a detailed breakdown of down payment options and PMI strategies, see this guide: Conventional loan with 5% down.

Closing Costs in Seattle

Buyers should budget for closing costs, which typically range from 2% of the loan amount for conventional home financing. In Seattle, this could mean $12,000 on a $600,000 loan. Costs include lender fees, title insurance, escrow, prepaid taxes, and more.

In competitive markets like Shoreline and Everett, some buyers negotiate seller credits to offset these expenses. Review your loan estimate carefully and ask your lender for a full cost breakdown before closing.

Documentation Checklist

To secure conventional home financing in 2026, be prepared to provide thorough documentation:

- Recent pay stubs and W-2s or tax returns

- Bank statements for assets and reserves

- Employment verification

- Credit report authorization

Self-employed buyers in Lynnwood or Mill Creek should expect to show two years of business tax returns and profit-and-loss statements. Having these documents ready can help you move quickly in fast-paced Seattle markets.

Step-by-Step Example: Lake Forest Park Buyer

Consider a Lake Forest Park couple preparing for conventional home financing. First, they check credit scores (aiming for 700+). Next, they calculate DTI, making sure it’s below 36%. They gather pay stubs, bank statements, and tax returns, then consult with a local lender about down payment options and PMI.

By understanding these requirements and staying organized, Seattle-area buyers can position themselves for success—even in a highly competitive market.

Stricter requirements in 2026 reflect the need for stability in Seattle’s dynamic housing environment. Mastering these details empowers you to pursue your dream home in Everett, Mill Creek, or anywhere across the region with confidence.

Step-by-Step Guide: Securing a Conventional Loan in Seattle for 2026

Securing conventional home financing in Seattle in 2026 calls for careful planning and a clear understanding of each stage in the process. Whether you are purchasing in Shoreline, Mill Creek, or Everett, following a structured approach can maximize your buying power and streamline your journey to homeownership. Here is a detailed, step-by-step roadmap tailored to the Seattle area.

Step 1: Assess Financial Readiness and Set a Budget

Begin by evaluating your finances, including your credit score, income, monthly debts, and available savings. In Seattle, where home values can be high, understanding your budget is crucial for successful conventional home financing. Use online calculators or consult a mortgage expert to estimate your maximum purchase price and monthly payment.

Step 2: Shop for Lenders and Compare Seattle-Specific Rates

Research local and national lenders, comparing interest rates, fees, and loan terms specific to the Seattle market. Conventional home financing rates may differ between King and Snohomish counties, so request quotes from multiple sources. Consider banks, credit unions, and mortgage brokers, and ask about lender credits or rate lock options.

Step 3: Gather Documentation and Apply for Pre-Approval

Prepare essential documents such as W-2s, tax returns, pay stubs, bank statements, and proof of assets. Submit these to your chosen lender for pre-approval. In competitive markets like Lynnwood and Mill Creek, having pre-approval for conventional home financing demonstrates to sellers that you are a serious and well-qualified buyer.

Step 4: Home Shopping—How Pre-Approval Strengthens Offers in Shoreline and Redmond

With pre-approval in hand, start searching for your ideal property in areas like Shoreline, Redmond, or Everett. Pre-approval gives you a competitive edge, especially when multiple offers are common. Stay informed about Seattle housing market trends 2026 to understand pricing and inventory, which can influence your strategy and timing.

Step 5: Submit an Offer and Negotiate with the Seller

Once you find a home that fits your needs and budget, work with your real estate agent to craft a strong offer. In fast-paced markets such as Mill Creek and Ballard, including your pre-approval letter with the offer can help you stand out. Be prepared to negotiate price, contingencies, and closing costs.

Step 6: Complete the Full Loan Application and Lock in Your Rate

After your offer is accepted, submit a complete loan application for conventional home financing. Your lender will verify your information and may request additional documents. This is also the time to lock your interest rate, protecting you from market fluctuations as you move toward closing.

Step 7: Home Appraisal and Underwriting Process

The lender orders a home appraisal to confirm the property’s value aligns with the purchase price. Underwriters review your application, credit, and documentation to ensure you meet all requirements for conventional home financing. If issues arise, your lender will guide you in resolving them promptly.

Step 8: Final Approval, Review Closing Disclosure, and Sign Documents

Once underwriting is complete, you receive a closing disclosure outlining all loan terms and costs. Review this carefully and ask questions if needed. At closing, sign the final documents and pay any required funds. You will then receive the keys to your new home in Seattle, Shoreline, or Lake Forest Park.

Example Timeline: From Offer to Keys in Seattle

A typical Seattle homebuyer may move from offer acceptance to closing in 21 to 30 days. In peak markets, some buyers secure keys in as little as 9 business days by staying organized and responsive throughout the conventional home financing process.

Tips for Expediting the Process in Fast-Moving Markets

- Respond quickly to lender requests for documents or clarifications.

- Work closely with a local mortgage broker familiar with Seattle and surrounding cities.

- Consider a fast-track approval program if facing multiple offers.

- Keep your credit and finances stable from application to closing.

Key Insight: The Value of Local Lender Relationships

In Seattle’s dynamic real estate market, strong relationships with local lenders can make a difference. These professionals understand the nuances of conventional home financing and can help you close quickly, giving you an advantage in competitive neighborhoods like Shoreline, Everett, and Mill Creek.

By following this step-by-step process, you can navigate the complexities of conventional home financing and achieve your goal of homeownership in the Seattle area with confidence.

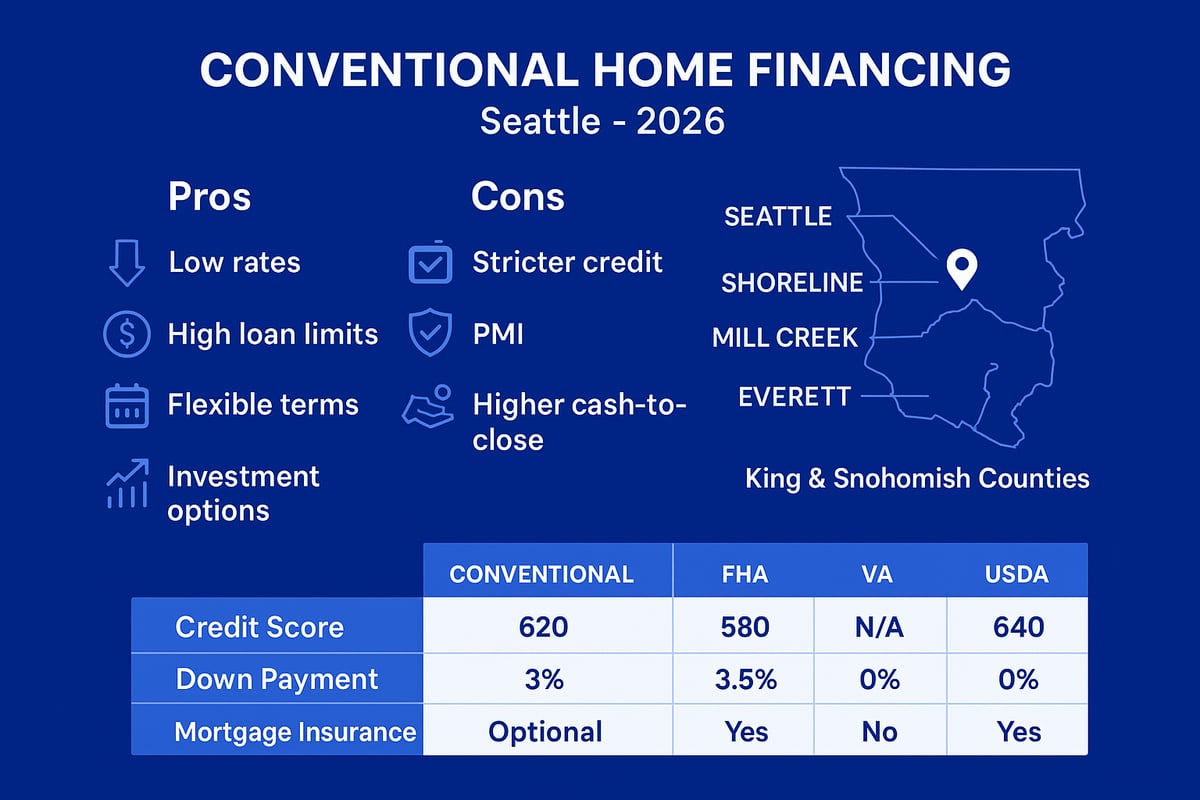

Pros and Cons of Conventional Home Financing in 2026

When exploring conventional home financing in Seattle, Shoreline, Mill Creek, and Everett, buyers and homeowners need to weigh both benefits and drawbacks. In 2026, understanding these factors is essential for making the smartest financial move in a dynamic market.

Pros of Conventional Home Financing

- Competitive Interest Rates: Buyers in Seattle and Everett often secure lower rates with strong credit profiles.

- Flexible Terms: Choose from various repayment periods and fixed or adjustable rates, ideal for both single-family homes and condos.

- High Loan Limits: In 2026, Seattle conforming loan limits have increased, allowing Mill Creek and Bellevue buyers to finance higher-priced homes without needing a jumbo loan.

- No Upfront Mortgage Insurance Premium (MIP): Unlike FHA loans, conventional home financing does not require an upfront MIP, reducing initial costs.

- Investment Property Options: Conventional loans support purchases of multi-unit or investment properties in places like Lynnwood or Shoreline, which FHA, VA, and USDA often restrict.

Cons of Conventional Home Financing

- Stricter Credit Standards: Lenders usually require a minimum credit score of 620, with higher thresholds for jumbo loans in Bellevue or Lake Forest Park.

- Private Mortgage Insurance (PMI): If your down payment is less than 20 percent, PMI is required until you reach sufficient equity, adding to monthly costs.

- Higher Down Payments and Closing Costs: Compared to FHA or VA, buyers in Everett and Mill Creek may need more cash upfront, especially for investment properties or multi-units.

- Tougher Debt-to-Income (DTI) Ratios: DTI guidelines are more stringent, which can be a hurdle for buyers in high-cost Seattle neighborhoods.

Quick Comparison Table

| Feature | Conventional | FHA | VA | USDA |

|---|---|---|---|---|

| Minimum Down Payment | 3% (first-time) | 3.5% | 0% | 0% |

| Upfront MIP/VA/USDA Fee | None | Yes | Yes | Yes |

| PMI or Annual Fee | PMI <20% down | Annual MIP | None | Annual Fee |

| Credit Score Minimum | 620+ | 580+ | Varies | 640+ |

| Investment Property Allowed | Yes | No | No | No |

Example: Bellevue Condo Buyer

Consider a Bellevue tech professional choosing between conventional home financing and FHA for a downtown condo. With excellent credit, a 10 percent down payment, and a competitive salary, they qualify for a conventional loan, avoiding the FHA’s upfront MIP and gaining flexibility for future investment property purchases.

Key Insights and Strategies

In 2025, 64 percent of U S buyers opted for conventional home financing, a trend poised to continue in Seattle, Shoreline, and Everett through 2026. Why? These loans suit a range of buyers, from first-timers in Lynnwood to seasoned investors in Lake Forest Park.

To maximize benefits, improve your credit score before applying, save for a higher down payment to remove PMI sooner, and compare local lender offers. For those with strong financials, conventional home financing provides unmatched flexibility and buying power in King and Snohomish counties.

Alternatives to Conventional Loans: FHA, VA, and USDA Options in Seattle

Looking beyond conventional home financing can open doors for many Seattle-area buyers, especially in competitive markets like Shoreline, Lynnwood, and Mill Creek. FHA, VA, and USDA loans each offer unique paths to homeownership, with distinct benefits and eligibility rules. Understanding how these alternatives compare to conventional home financing is crucial for making the best choice in 2026.

FHA Loans: Flexible Entry for Seattle Buyers

FHA loans remain a popular alternative to conventional home financing in Seattle, offering just 3.5 percent down for buyers with credit scores as low as 580. This is especially helpful for first-time buyers in Everett or Lake Forest Park who may not have large savings or perfect credit. FHA loans require both upfront and annual mortgage insurance premiums, which can add to monthly payments. However, the more lenient approval criteria make these loans accessible for many.

VA Loans: Zero Down for Veterans and Service Members

VA loans are a standout choice for eligible veterans and active-duty service members in Seattle, Shoreline, and beyond. With zero down payment and no private mortgage insurance, VA loans can make homeownership more affordable, particularly in higher-priced areas like Mill Creek. While the property must meet VA guidelines and buyers must have a valid Certificate of Eligibility, the savings can be substantial compared to conventional home financing, especially for those with modest reserves.

USDA Loans: Rural Opportunities Near Seattle

USDA loans support buyers seeking homes in eligible rural areas surrounding Seattle, including parts of Everett and Mill Creek. With zero down payment and competitive rates, USDA loans offer a compelling alternative to conventional home financing for those who qualify. Income limits apply, and the property must be in a designated location, but for buyers willing to look outside the city center, this option can mean significant savings.

Comparing Options: A Lynnwood First-Time Buyer Example

Consider a first-time buyer in Lynnwood weighing their choices. With limited savings and a moderate credit score, FHA could provide a low entry point, while a VA loan would be best if they have military service. If the home is in an eligible area, USDA could allow for zero down. Comparing these programs to conventional home financing, buyers should also explore first-time homebuyer programs in Seattle to maximize their purchasing power.

Pros and Cons of FHA, VA, and USDA Loans

| Loan Type | Down Payment | Credit Score | Insurance | Key Eligibility |

|---|---|---|---|---|

| FHA | 3.5% | 580+ | Upfront & annual MIP | Flexible income/credit |

| VA | 0% | 620+ | No PMI | Military service |

| USDA | 0% | 640+ | Annual fee | Rural area/income cap |

Each alternative to conventional home financing offers unique benefits, but also comes with restrictions and additional requirements.

When to Choose an Alternative Over Conventional

For buyers in Seattle, Shoreline, or Everett who do not meet the stricter standards of conventional home financing, exploring FHA, VA, or USDA loans can be the key to homeownership in 2026. Assess your eligibility, financial goals, and local housing options before deciding which route is best for your needs.

FAQs: Conventional Home Financing in Seattle and Surrounding Cities

Are you navigating conventional home financing in Seattle or nearby communities like Shoreline, Lynnwood, or Mill Creek? Here are answers to the most common questions from Seattle-area buyers and homeowners as they consider their next move in 2026.

Is a conventional loan a good option for first-time buyers in Seattle?

Yes, conventional home financing is a strong choice for first-time buyers in Seattle, Shoreline, and Lynnwood. With down payment options as low as 3 percent, competitive rates, and flexible terms, these loans suit many buyers. However, you will need a solid credit profile and verifiable income. For a quick explanation of key mortgage terms, see this Mortgage glossary and definitions.

How much do I need for a down payment in Shoreline or Everett?

For most buyers, conventional home financing requires a minimum of 3 percent down if you are a first-time buyer, or 5 percent or more for repeat buyers. Investment properties and multi-unit homes may need a higher down payment. In competitive markets like Everett and Mill Creek, a larger down payment can strengthen your offer.

What credit score do I need for a jumbo loan in Bellevue?

Jumbo loans, which go above Seattle’s conforming loan limits, generally require a higher credit score. In Bellevue or Lake Forest Park, you will want a score of at least 700, though some lenders may accept 680 with exceptional compensating factors. Higher scores can help you secure better rates and terms.

Can I use RSUs or bonus income to qualify in Redmond?

Yes, many lenders will count restricted stock units (RSUs) and bonus income toward your qualifying income for conventional home financing, especially in tech-heavy areas like Redmond and Seattle. You will need to provide a history of receiving this compensation and documentation to support its consistency.

How long does the approval process take in Seattle’s fast market?

In Seattle, Shoreline, and Bellevue, the typical timeline from pre-approval to closing is 21 to 30 days. However, fast-track programs and prepared documentation can reduce this to as little as 9 days, which is helpful in multiple-offer situations. Working with a local lender who understands the market can expedite the process.

Do I have to put 20 percent down to avoid PMI?

No, you do not need 20 percent down to get approved for conventional home financing, but putting less than 20 percent down means you will pay private mortgage insurance (PMI). As your home in Everett or Mill Creek appreciates, you can request PMI removal once your equity reaches 20 percent.

What are the closing cost averages for Mill Creek and Lake Forest Park?

Closing costs in Mill Creek, Lake Forest Park, and Seattle generally range from 2 percent of the loan amount. These costs include lender fees, appraisal, title insurance, and more. In some cases, you can negotiate seller credits to offset out-of-pocket expenses.

Can I refinance my conventional loan in 2026 if rates drop?

Absolutely. If mortgage rates decrease, Seattle-area homeowners can refinance their conventional home financing to potentially lower monthly payments or shorten their loan term. Always review costs and potential savings before refinancing.

How do I remove PMI once my home appreciates in value?

When your home in Everett or Shoreline gains enough equity (typically 20 percent), you can contact your lender to request PMI removal. An updated appraisal may be required to confirm your current loan-to-value ratio.

Are there special programs for tech professionals or investors?

While conventional home financing is available to all qualified buyers, some Seattle lenders offer specialized underwriting for tech professionals, including support for RSUs and bonus income. Investors will find flexible options for purchasing single-family or multi-unit properties, though higher down payments and stricter guidelines may apply.

If you have more questions about conventional home financing or want to explore the latest Seattle-area market trends, the Washington real estate market report Q1 2026 provides valuable insights and data.

Now that you have a clearer picture of the 2026 Seattle housing market and the ins and outs of conventional home financing, you might be wondering how these insights apply to your unique situation. Whether you’re a first-time buyer, a seasoned investor, or a tech professional navigating stock compensation, having a trusted expert by your side can make all the difference. I’m here to answer your questions, discuss your goals, and help you craft a strategy that fits your needs. If you’re ready to take the next step, Let’s have a conversation about your home financing journey.

Key Takeaways

- The article provides a comprehensive Guide to Conventional Home Financing: Insights for 2026, focusing on Seattle and surrounding areas.

- It explains conventional loans, contrasting them with FHA, VA, and USDA options, and highlights the importance of credit scores, down payments, and closing costs.

- Buyers will find a step-by-step guide for securing a conventional loan, emphasizing financial preparation, lender shopping, and documentation.

- The article also discusses the pros and cons of conventional financing, noting its appeal due to flexible terms and competitive rates.

- Finally, it offers insights on alternative financing options and answers common questions for buyers in the Seattle area.

Estimated reading time: 18 minutes