Seattle homeowners and buyers, 2026 is set to be a turning point for home loans refinance rates as interest rates fluctuate and new lending rules come into play. Navigating these changes can feel overwhelming, but with the right guidance, you can make confident decisions that benefit your financial future.

This guide is designed to help you understand and secure the best home loans refinance rates in Seattle and nearby areas like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. We will share expert-backed strategies, break down rate trends, and explain the refinance process step by step.

Stay with us to gain clarity, save money, and make empowered choices for your next refinance.

Understanding Home Loans Refinance Rates: Key Concepts for 2026

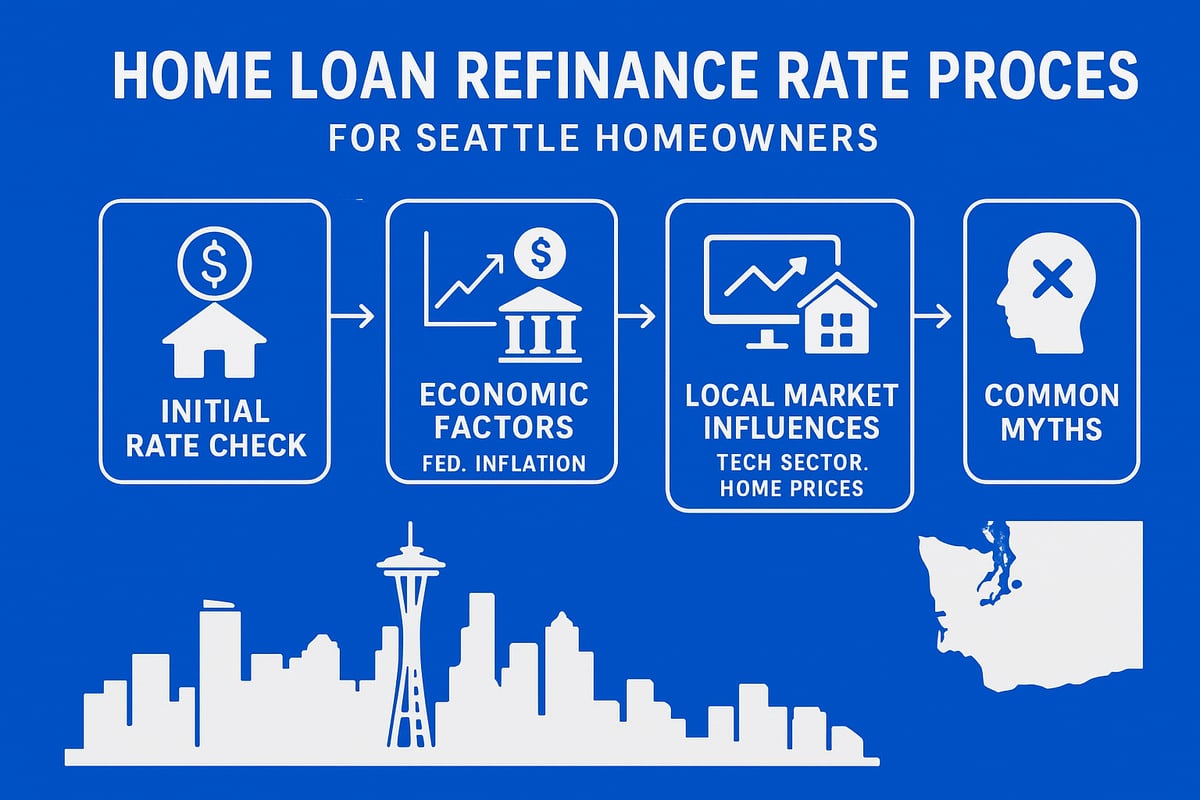

Navigating home loans refinance rates in Seattle and the surrounding area starts with a clear understanding of what these rates are and how they impact your financial future. Whether you live in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett, knowing these basics helps you make confident decisions.

What Are Home Loan Refinance Rates?

Home loans refinance rates are the interest rates offered when you replace your current mortgage with a new one, aiming to improve your payment terms or access equity. These rates often differ from purchase loan rates, as they reflect both current market trends and your personal financial profile. Common refinance types include fixed-rate, adjustable-rate, and cash-out refinances. For Seattle-area homeowners, understanding these options is crucial, and reviewing a Seattle refinance process guide can help clarify each step. Knowing your refinance rate options sets the stage for smart, local decisions.

Factors Impacting Refinance Rates in 2026

Several forces will shape home loans refinance rates in 2026. The Federal Reserve’s monetary policy and inflation trends play a significant role, directly affecting lenders’ costs. Economic forecasts for 2026 suggest potential shifts in employment and growth, especially in the tech-driven Seattle region. Housing market conditions, such as supply and demand in Puget Sound, further influence rate offers. Additionally, lender competition and advancements in mortgage technology can lead to more competitive rates and streamlined approval processes. Staying informed on these factors helps you anticipate rate changes and plan your refinance approach.

Local Market Dynamics: Seattle and Surrounding Areas

In Seattle and nearby cities like Shoreline, Lynnwood, and Everett, unique market dynamics influence home loans refinance rates. The region’s strong tech sector attracts high demand, while limited housing supply often keeps home prices elevated. For example, Seattle’s median home price can affect the rates lenders offer, especially for jumbo loans. Recent refinance activity in Lake Forest Park and Mill Creek shows that even small differences in property values or neighborhood trends can impact your rate. Understanding these local patterns ensures you are comparing rates that reflect your specific city and circumstances.

Common Rate Myths and Misconceptions

Many homeowners believe home loans refinance rates will always drop, but timing the market is unpredictable. Another common misconception is confusing APR (annual percentage rate) with the interest rate, when APR includes fees and costs beyond the rate itself. Credit scores and loan-to-value ratios also play a bigger role than many realize, affecting both eligibility and the rates you receive. By debunking these myths, Seattle-area borrowers can focus on factors within their control—like improving credit or choosing the right time based on personal goals—rather than relying on market guesses.

2026 Rate Trends and Forecasts: What Seattle Homeowners Need to Know

Seattle-area homeowners are closely watching 2026, as home loans refinance rates respond to shifting economic signals, housing supply, and evolving lending rules. Understanding what drives these rates locally and nationally is essential for making confident decisions in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett.

National and Regional Economic Outlook

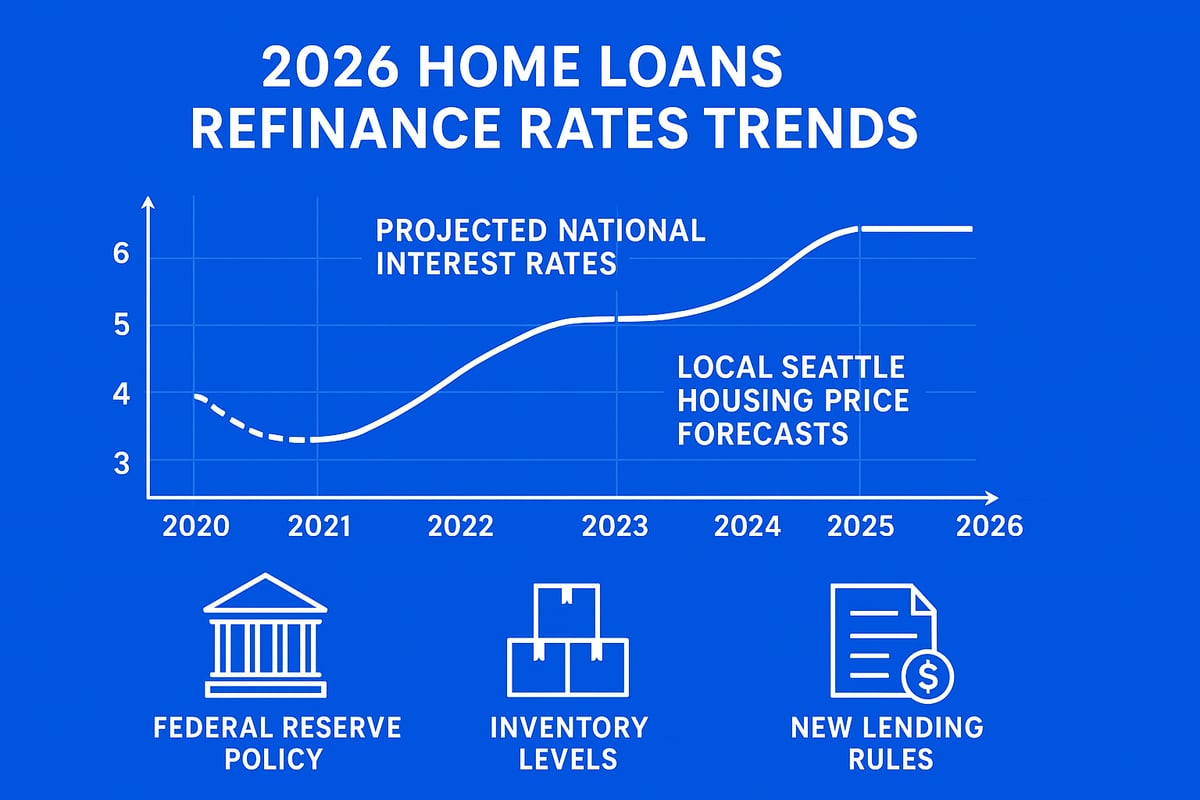

The national economy plays a foundational role in shaping home loans refinance rates. In 2026, the Federal Reserve’s interest rate policies and inflation targets are expected to influence borrowing costs across the country. Seattle homeowners should monitor these trends, as local rates often track with national benchmarks.

Forecasters predict moderate inflation and continued economic growth, though some volatility is possible. According to Fannie Mae’s 2026 Mortgage Rate Forecast, rates may trend below 6 percent by year-end. This projection, if realized, would impact refinance opportunities for Seattle, Everett, and the broader Puget Sound region.

It is important to note that while national shifts set the stage, local factors can amplify or soften the impact on your refinance options.

Seattle Area Housing Market Forecasts

Local housing dynamics are a key driver of home loans refinance rates in Seattle and nearby cities. In 2026, the market is expected to remain competitive, especially in high-demand neighborhoods of Shoreline, Lynnwood, and Mill Creek.

Median home values are projected to rise modestly, supported by strong tech sector employment and limited inventory. Everett and Lake Forest Park may see similar trends, with slight variation based on new construction and buyer demand.

Compared to national averages, Seattle’s refinance activity historically runs higher, reflecting both price appreciation and homeowner equity. Understanding these local patterns helps you anticipate how your city’s conditions will affect your refinance rate.

Anticipated Lending Rule Changes in 2026

Home loans refinance rates are also shaped by evolving lending standards. In 2026, updates from Fannie Mae and Freddie Mac may introduce new credit score thresholds or adjust qualifying ratios, directly impacting Seattle-area borrowers.

Lenders are increasingly leveraging digital tools for income and asset verification, which can streamline the refinance process, especially for tech professionals in Seattle, Bellevue, and Redmond. Watch for local policy shifts, such as changes to property tax assessments or city-level housing initiatives, which may influence loan eligibility.

Staying informed about these anticipated changes will help you prepare documentation and strengthen your refinance application.

Optimal Timing: When to Refinance in 2026

Timing is crucial when seeking the best home loans refinance rates. Historically, rates fluctuate in cycles that align with Federal Reserve announcements and broader market conditions.

In Seattle, spring and early summer often bring increased activity, which can affect lender pricing and processing times. Conversely, fall and winter may offer quieter windows for strategic rate locks, especially in Lynnwood or Lake Forest Park.

Consider using a rate lock to secure favorable terms if you anticipate upward movement. Monitoring seasonal trends and national economic data positions you to act confidently when the right opportunity arises.

Step-by-Step Guide to Refinancing Your Home Loan in Seattle

Refinancing your home in Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, or Everett is a strategic way to save money, access equity, or meet new financial goals. The process of evaluating home loans refinance rates can feel complex, but breaking it into clear steps makes it manageable and rewarding.

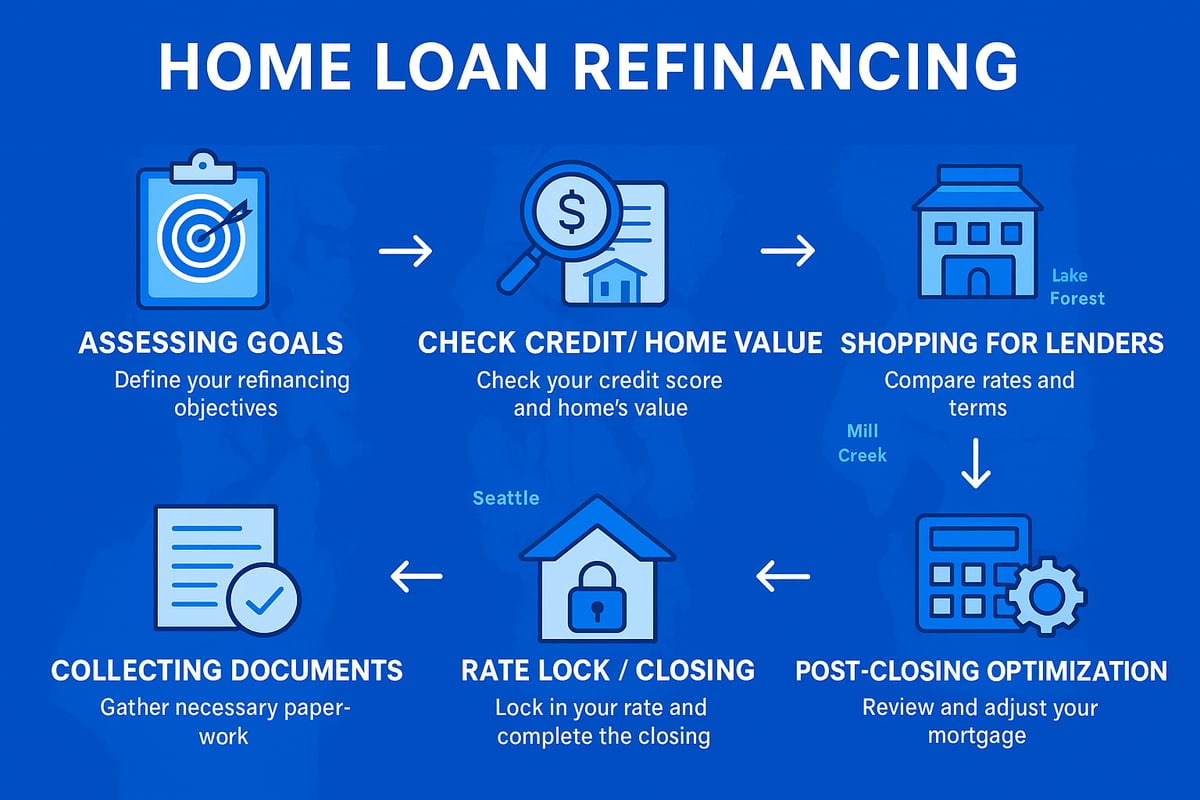

Step 1: Assess Your Financial Goals and Readiness

Start by clarifying why you want to refinance. Are you aiming to lower your monthly payment, shorten your loan term, or tap into equity for a remodel or debt consolidation? Each goal will shape which home loans refinance rates are most beneficial for your situation.

Calculate your break-even point by dividing total refinance costs by your expected monthly savings. For example, a Seattle homeowner saving $250 per month with $5,000 in costs will break even in 20 months. Knowing this timeline helps you decide if refinancing now fits your future plans.

Local case: A Mill Creek family refinanced to access cash for college tuition, while a Lynnwood couple reduced their rate, saving thousands over the loan term. Understanding your personal objectives is the foundation for a successful refinance.

Step 2: Check Your Credit and Home Equity

Your credit score and home equity are critical factors in qualifying for the best home loans refinance rates. Review your credit report for errors and pay down debts to improve your score before applying.

Next, estimate your home’s current value. In Seattle, Shoreline, and Lake Forest Park, strong appreciation may have increased your equity, improving your loan-to-value ratio (LTV). Lenders often require at least 20% equity for top rates, though FHA and VA options may allow less.

Knowing your LTV helps you set realistic expectations and plan the right loan structure. For more on this, see Understanding Loan-to-Value Ratios.

Step 3: Shop and Compare Lenders

Research both local and national lenders to find the most competitive home loans refinance rates. Seattle-area mortgage brokers often provide tailored advice and access to niche programs for tech professionals or investors.

Compare rate quotes, APRs, and lender fees side by side. Look for transparency and ask about rate lock policies. Using a broker with deep knowledge of Seattle, Everett, and Mill Creek markets ensures you receive guidance specific to your property type and goals.

Check Current Seattle mortgage rates for real-time data and trends to benchmark your offers. A small rate difference can make a significant impact on long-term savings.

Step 4: Gather Documentation and Apply

Prepare your documentation before applying. Lenders typically request:

- Recent pay stubs or proof of income

- W-2s or tax returns (especially for self-employed or tech professionals with RSUs)

- Bank statements

- Current mortgage statement

- Homeowners insurance and property tax info

Seattle lenders increasingly offer digital applications, streamlining the process for busy professionals in Shoreline and Lynnwood. Some lenders also provide expedited options for tech sector employees, reducing paperwork and turnaround time.

Apply with multiple lenders to compare pre-approvals and offers, and keep your documents organized to avoid unnecessary delays.

Step 5: Lock Your Rate and Close the Loan

Once you select a lender, discuss the best time to lock your home loans refinance rates. Rate lock windows typically range from 30 to 60 days, protecting you from market fluctuations during underwriting.

In Seattle, Everett, and Mill Creek, closing timelines often run 30-45 days, depending on appraisal requirements and lender efficiency. Review your loan estimate for closing costs, including appraisal, title, escrow, and origination fees. Some costs may be negotiable—ask your lender or broker for guidance.

Negotiate where possible, and confirm the final numbers before signing. A transparent closing process ensures you achieve your refinance goals smoothly.

Step 6: Post-Closing Steps and Maximizing Savings

After closing, set up your new mortgage payments and confirm escrow arrangements for taxes and insurance. Notify your insurer and county assessor of the refinance to update records.

Continue monitoring home loans refinance rates even after closing, especially if Seattle market conditions shift in your favor. For example, a Lake Forest Park homeowner who refinanced in early 2026 found a further rate drop six months later, allowing another round of savings.

Track your equity growth and consider future opportunities to leverage your property’s value for other financial objectives.

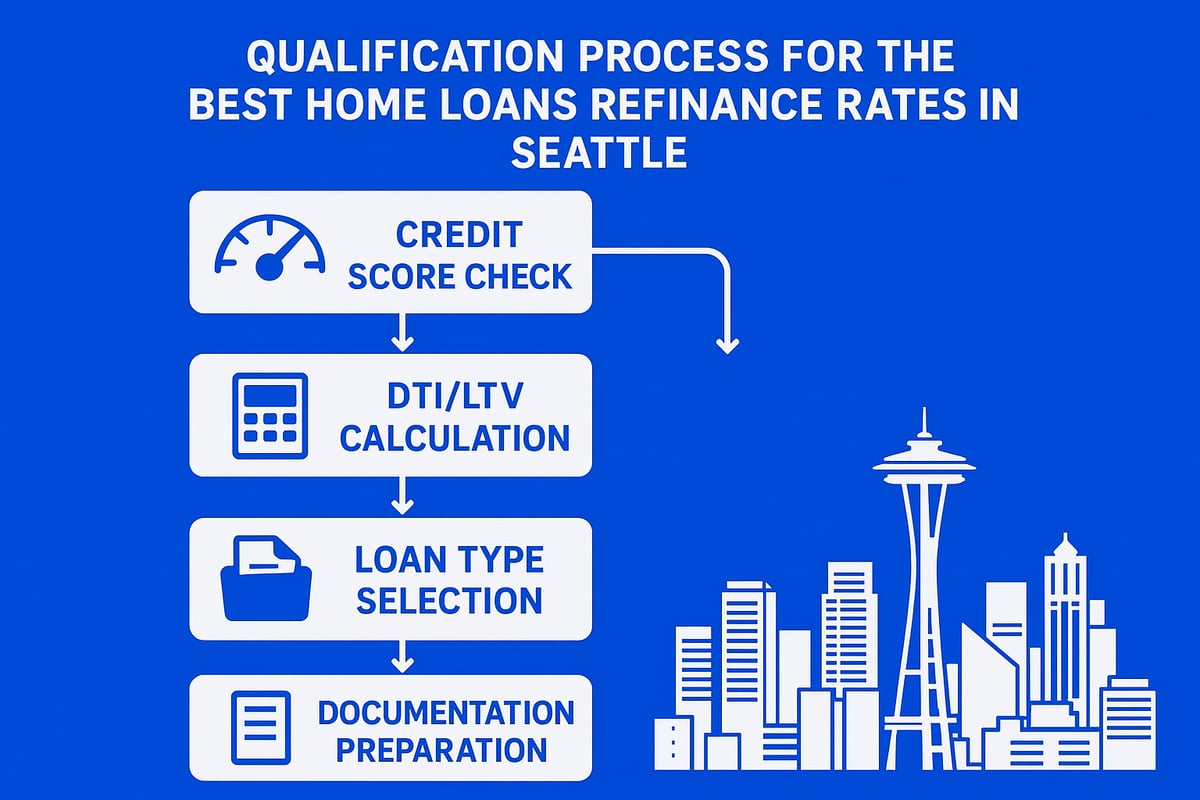

How to Qualify for the Best Refinance Rates in 2026

Qualifying for the best home loans refinance rates in Seattle and nearby cities starts with understanding what lenders look for in 2026. Whether you live in Shoreline, Lynnwood, Mill Creek, Lake Forest Park, or Everett, preparation and knowledge are your strongest advantages. Let’s break down what you need to know and do to secure top-tier rates in this competitive market.

Credit Score Strategies and Requirements

Your credit score is a cornerstone for accessing the best home loans refinance rates in Seattle. In 2026, most lenders require a minimum FICO score of 680 for prime rates, but 740 or higher unlocks the most competitive offers.

If your score falls below this, focus on paying down revolving debts, correcting credit report errors, and avoiding new credit inquiries. For example, a Lynnwood homeowner improved their score from 670 to 720 in six months by reducing card balances and setting up automatic payments.

Take these steps early, as even a small increase can lead to significant savings on home loans refinance rates. Review your credit at least three months before applying.

Debt-to-Income and Loan-to-Value Ratios

Lenders in Seattle and surrounding areas assess your debt-to-income (DTI) and loan-to-value (LTV) ratios to determine risk and eligibility for the best home loans refinance rates. DTI measures your monthly debt versus income, while LTV compares your loan balance to your home’s value.

Conventional loans generally require an LTV below 80 percent, while FHA and some jumbo programs may allow higher ratios. Calculate your numbers in advance and plan to pay down debt or build equity if needed to maximize your home loans refinance rates.

Choosing the Right Loan Type for Your Situation

Picking the right loan product is crucial for securing optimal home loans refinance rates. Fixed-rate mortgages offer stability, which appeals to families in Lake Forest Park and Mill Creek, especially if rates are expected to rise. Adjustable-rate mortgages (ARMs) may suit investors or tech professionals in Seattle who anticipate selling or refinancing again within a few years.

A cash-out refinance provides funds for renovations or debt consolidation but often comes with slightly higher rates. Rate-and-term refinances focus solely on lowering your interest or shortening your term. Match your choice to your financial goals and local market trends.

Documentation and Employment Verification Tips

Lenders in Seattle, Shoreline, and Lynnwood require a range of documents to approve home loans refinance rates. Be ready with:

- Recent pay stubs or W-2s

- Two years of tax returns (especially for self-employed or tech employees with RSUs)

- Bank and asset statements

- Proof of homeowner’s insurance

- Mortgage statements and property tax info

Tech professionals using RSUs or stock compensation should organize grant documents and vesting schedules early. To make the process smoother and avoid delays, work with a lender who understands Seattle’s unique employment landscape. For additional guidance, explore Home ownership education Seattle to better prepare for your refinance journey.

Costs, Fees, and Break-Even Analysis for Seattle Refinances

Navigating home loans refinance rates in Seattle means understanding the full cost picture before making a decision. Every refinance comes with its own set of fees, timelines, and tax implications, especially in markets like Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Here’s what Seattle-area homeowners need to know to make smart financial moves.

Understanding Typical Refinance Costs

When exploring home loans refinance rates in Seattle, it’s essential to factor in all associated costs. These typically include appraisal fees, origination charges, title insurance, and escrow services. In Seattle, appraisals often range from $600 to $900, while origination fees may vary between 0.5% and 1% of the loan amount.

Here’s a quick comparison for common refinance fees across Seattle and neighboring cities:

Some fees are negotiable, especially with lender competition in Lynnwood and Mill Creek. Always review the loan estimate to see which costs are fixed.

Calculating Your Break-Even Point

Before locking in home loans refinance rates, calculate your break-even point—the moment your monthly savings outweigh the upfront costs. Divide your total refinance costs by your monthly payment savings to find out how long it takes to recover your investment.

For example, a Lake Forest Park homeowner who pays $5,000 in closing costs and saves $200 per month will break even in 25 months. Use online calculators or consult a local broker for tailored estimates.

Want more ways to maximize your savings? Check out these how to lower your mortgage payment strategies that can further improve your break-even timeline.

Hidden Fees and How to Avoid Them

Not all costs tied to home loans refinance rates are obvious upfront. Watch for “junk fees” like excessive courier charges, processing fees, or padded administrative costs. Seattle and Everett lenders may differ in transparency, so always request a fee breakdown.

To avoid unnecessary charges:

- Compare at least three lender quotes.

- Ask for written explanations of all fees.

- Negotiate or waive non-essential items.

Rely on an experienced Seattle-area mortgage broker to help spot and challenge questionable charges.

Tax Implications and Deductibility

Refinancing can affect your taxes, but not all costs are deductible. Generally, interest paid on home loans refinance rates may be tax-deductible, but fees like appraisal and title are not. A cash-out refinance could also trigger capital gains considerations if you later sell your home.

Seattle’s property tax rates can influence your escrow setup. Consult a tax advisor to clarify which costs you can deduct and how to plan for any tax impact post-refinance.

Comparing No-Closing-Cost vs. Traditional Refinances

Seattle homeowners often ask if a no-closing-cost refinance is worth it. With no-closing-cost home loans refinance rates, lenders typically charge a slightly higher rate in exchange for covering your upfront fees.

Consider this example for a Mill Creek homeowner:

| Option | Closing Costs | Rate | Monthly Payment |

|---|---|---|---|

| Traditional | $5,000 | 5.50% | $2,200 |

| No-Closing-Cost | $0 | 5.875% | $2,250 |

While you save on initial outlay, you may pay more over time. Review your long-term plans and compare both options carefully to see which aligns with your goals.

Seattle-Area FAQ: 2026 Home Loan Refinance Rates Answered

Seattle area homeowners and buyers often have pressing questions about home loans refinance rates, especially as the market evolves in 2026. Below, I address the most common queries I hear as a licensed mortgage broker serving Seattle, Shoreline, Lynnwood, Lake Forest Park, Mill Creek, and Everett. Each answer is tailored to our local landscape, empowering you to make informed decisions.

What Is the Current Average Refinance Rate in Seattle?

As of mid 2026, Seattle’s average home loans refinance rates are tracking closely with national trends, but local factors often create slight variances. According to the Fannie Mae 2026 Housing and Interest Rate Projections, national mortgage rates are expected to hover between 5.5% and 6.25%. In Seattle, rates may be at the higher end of this range due to strong demand and limited housing inventory. Always compare lender offers and monitor daily rate updates to find the most favorable terms for your refinance.

How Do Refinance Rates Differ Between Seattle, Shoreline, Lynnwood, and Everett?

Home loans refinance rates can vary between Seattle and neighboring cities such as Shoreline, Lynnwood, and Everett. Factors like median home prices, local competition among lenders, and property types influence rate offers. For example, according to the Seattle Housing Market Forecast 2026, Seattle’s higher median home values may result in slightly lower rates for high-credit borrowers, while Lynnwood and Everett may offer competitive options for first-time refinancers. Always request personalized quotes based on your location and property specifics.

Is Now a Good Time to Refinance in 2026?

Timing your refinance in 2026 depends on where home loans refinance rates are trending and your personal financial goals. Historically, spring and early summer see increased activity in Seattle as buyers and refinancers take advantage of favorable conditions. Monitor rate trends, local inventory, and consult with a mortgage expert to determine if locking in a rate now will maximize your savings. Remember, waiting for the “perfect” moment can lead to missed opportunities, especially in fast-moving markets like Mill Creek and Lake Forest Park.

Can Tech Professionals Use RSUs/Stock Compensation for Refinancing?

In Seattle, many homeowners work in tech and receive RSUs or stock compensation, which can play a role in qualifying for home loans refinance rates. Most lenders will consider vested RSUs as income if you provide the appropriate documentation and a history of consistent vesting. For example, tech professionals in Redmond or Bellevue should prepare detailed pay statements and brokerage records to streamline the process. Work with a lender experienced in handling complex compensation packages to ensure you leverage every advantage.

What Are the Best Refinance Options for Investors in Seattle?

Investors in Seattle, Shoreline, and Lynnwood can access tailored refinance products such as multi-unit loans, DSCR (Debt Service Coverage Ratio) loans, and bank statement programs. These options often come with unique qualification criteria and slightly different home loans refinance rates compared to owner-occupied properties. For example, an investor refinancing a duplex in Everett may find a DSCR loan beneficial, while a Lake Forest Park investor might prefer a traditional cash-out refinance to access equity for future purchases.

How Fast Can I Close a Refinance in the Seattle Area?

Closing times for home loans refinance rates in Seattle, Bellevue, Redmond, and Kirkland typically range from 21 to 35 days, depending on your lender and the complexity of your file. Local lenders familiar with Seattle’s market often close faster due to streamlined processes and established relationships with title companies. If you’re refinancing in Mill Creek or Everett, prepare your documentation in advance and respond quickly to lender requests to expedite your timeline. Using digital applications and e-signatures can further speed up the process.

As you look ahead to refinancing your home in Seattle or the surrounding areas in 2026, having a trusted expert by your side is invaluable. I’ve walked you through rate trends, local market shifts, and actionable steps to help you make informed decisions with confidence. If you want clarity on your unique situation—whether you’re a tech professional leveraging RSUs, an investor, or a homeowner aiming for better terms—let’s connect and discuss your goals. Together, we can build a strategy tailored to your needs.

Let’s have a conversation

Key Takeaways

- 2026 will witness fluctuating home loans refinance rates in Seattle due to new lending rules and market dynamics.

- Understanding the refinance process, including factors affecting rates and local market trends, is crucial for homeowners.

- Home buyers should plan their refinances strategically, considering timing and local economic conditions to secure the best rates.

- Common myths about refinance rates can mislead homeowners; accurate knowledge helps in making informed decisions.

- Utilizing expert advice and tailored strategies enhances the potential for savings and beneficial financial outcomes.

Estimated reading time: 1 minute

Mortgage refinance rates in 2026 are expected to remain sensitive to inflation trends, Federal Reserve policy, and overall economic conditions. While rates may fluctuate throughout the year, homeowners should focus less on predicting exact rate movements and more on evaluating refinance opportunities based on long-term savings, break-even timelines, and personal financial goals.

Refinance rates are typically slightly higher than purchase mortgage rates due to differences in risk and loan pricing. Lenders often view refinances as higher risk than purchase transactions, which can affect pricing. This difference is especially relevant in higher-balance loans common in Seattle-area refinances.

Mortgage refinance rates in Seattle are influenced by national factors such as inflation, bond markets, and Federal Reserve decisions, as well as local factors including home values, loan size, property type, and lender competition. Borrower-specific factors like credit score, loan-to-value ratio, and debt-to-income ratio also play a significant role.

Refinancing in 2026 can make sense if it aligns with your financial strategy. Homeowners refinance for many reasons, including lowering monthly payments, reducing interest over time, shortening the loan term, accessing home equity, or improving cash flow. The decision should be based on total cost analysis, not just the interest rate.

To determine whether refinancing makes sense, homeowners should compare current loan terms with proposed refinance terms, calculate closing costs, and determine the break-even point. If you plan to stay in the home beyond the break-even period and the refinance supports your long-term financial goals, it may be a strong option.

Yes. Refinancing can still be beneficial even if rates are higher, depending on the strategy. Examples include removing mortgage insurance, switching from an adjustable-rate mortgage to a fixed-rate loan, consolidating debt, or restructuring the loan term for better cash flow or long-term planning.

There is no legal limit to how often you can refinance, but lenders may impose seasoning requirements depending on loan type. The more important consideration is whether refinancing again provides meaningful financial benefit after accounting for costs and reset timelines.

Trying to time the market is risky. Instead of waiting for the “perfect” rate, homeowners should evaluate refinancing opportunities based on available options today, potential savings, and flexibility. In some cases, refinancing now with a plan to adjust later can be a more effective strategy.

The mortgage refinance process typically takes 30 to 45 days, depending on documentation, appraisal requirements, and lender turnaround times. Preparation and clear financial goals can help streamline the process.

Homeowners should speak with a local mortgage professional who understands both refinance strategy and the Seattle housing market. Local insight can be especially valuable when evaluating high-balance loans, property values, and market-specific pricing differences.